Deck 10: Property Dispositions

ملء الشاشة (f)

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

سؤال

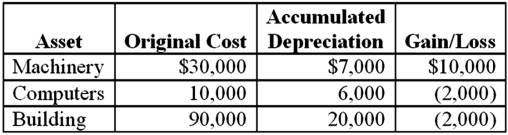

Brandon,an individual,began business four years ago and has never sold a §1231 asset.Brandon owned each of the assets for several years.In the current year,Brandon sold the following business assets:  Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

A)$7,000 ordinary income,$1,000 §1231 loss and $2,100 tax liability.

B)$6,000 ordinary income and $2,100 tax liability.

C)$7,000 §1231 gain and $2,450 tax liability.

D)$7,000 §1231 gain and $1,050 tax liability.

E)None of thesE.The depreciation recapture of $7,000 becomes ordinary income.The $4,000 §1231 loss becomes an ordinary loss and offsets the $3,000 §1231 gain on the machinery.The $1,000 net §1231 loss becomes ordinary and offsets the $7,000 ordinary gain.The remaining ordinary gain of $6,000 is taxed at 35 percent which results in $2,100 of tax.

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?A)$7,000 ordinary income,$1,000 §1231 loss and $2,100 tax liability.

B)$6,000 ordinary income and $2,100 tax liability.

C)$7,000 §1231 gain and $2,450 tax liability.

D)$7,000 §1231 gain and $1,050 tax liability.

E)None of thesE.The depreciation recapture of $7,000 becomes ordinary income.The $4,000 §1231 loss becomes an ordinary loss and offsets the $3,000 §1231 gain on the machinery.The $1,000 net §1231 loss becomes ordinary and offsets the $7,000 ordinary gain.The remaining ordinary gain of $6,000 is taxed at 35 percent which results in $2,100 of tax.

سؤال

سؤال

سؤال

سؤال

سؤال

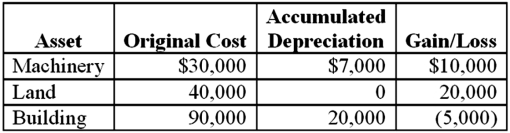

Brandon,an individual,began business four years ago and has sold §1231 assets with $5,000 of losses within the last 5 years.Brandon owned each of the assets for several years.In the current year,Brandon sold the following business assets:  Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

A)$25,000 ordinary income,$8,750 tax liability.

B)$25,000 §1231 gain and $3,750 tax liability.

C)$13,000 §1231 gain,$12,000 ordinary income,and $6,150 tax liability.

D)$12,000 §1231 gain,$13,000 ordinary income,and $6,350 tax liability.

E)None of thesE.Depreciation recapture of $7,000 becomes ordinary income.In addition,Brandon has a $23,000 §1231 gain and $5,000 §1231 loss,which nets to an $18,000 net §1231 gain.The 1231 lookback rule recharacterizes $5,000 of the §1231 gain to ordinary income.Thus,$12,000 (35%) of ordinary income and $13,000 (15%) of §1231 gain.The calculations results in $6,150 of tax.

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?A)$25,000 ordinary income,$8,750 tax liability.

B)$25,000 §1231 gain and $3,750 tax liability.

C)$13,000 §1231 gain,$12,000 ordinary income,and $6,150 tax liability.

D)$12,000 §1231 gain,$13,000 ordinary income,and $6,350 tax liability.

E)None of thesE.Depreciation recapture of $7,000 becomes ordinary income.In addition,Brandon has a $23,000 §1231 gain and $5,000 §1231 loss,which nets to an $18,000 net §1231 gain.The 1231 lookback rule recharacterizes $5,000 of the §1231 gain to ordinary income.Thus,$12,000 (35%) of ordinary income and $13,000 (15%) of §1231 gain.The calculations results in $6,150 of tax.

سؤال

سؤال

سؤال

سؤال

فتح الحزمة

قم بالتسجيل لفتح البطاقات في هذه المجموعة!

Unlock Deck

Unlock Deck

1/88

العب

ملء الشاشة (f)

Deck 10: Property Dispositions

1

The adjusted basis is the cost basis less cost recovery deductions.

True

2

Depreciation recapture changes both the amount and character of a gain.Depreciation recapture changes the character of the gain,not the amount.

False

3

Taxpayers can recognize a taxable gain even though an asset's real economic value has declined.

True

4

Assets held for investment and personal use assets are examples of capital assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

5

The gain or loss realized is the amount realized less the adjusted basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

6

An asset's tax adjusted basis is usually greater than its book adjusted basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

7

Unrecaptured §1250 gains apply only to individuals.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

8

Only accelerated depreciation is recaptured for §1245 assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

9

§1231 assets include all assets used in a trade or business.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

10

Ordinary gains and losses are obtained on the sale of investments.Capital gains and losses are obtained on the sale of investments.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

11

After application of the lookback rule,net §1231 gains become capital while net §1231 losses become ordinary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

12

The amount realized is the sale proceeds less the adjusted basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

13

Accounts receivable and inventory are examples of ordinary assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

14

All tax gains and losses are ultimately characterized as either ordinary or capital.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

15

The gain or loss realized is always recognized for tax purposes.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

16

For corporations,§291 recaptures 20 percent of the lesser of depreciation taken or the realized gain as ordinary income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

17

A parcel of land is always a capital asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

18

Generally,the amount realized is everything of value received in a sale less selling expenses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

19

§1250 recaptures the excess of accelerated depreciation over straight line depreciation on real property placed in service between 1981 and 1986 as ordinary income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

20

Unrecaptured §1250 gain is taxed at a maximum rate of 25 percent.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

21

Which of the following is not true regarding an asset's adjusted basis?

A)Tax adjusted basis is usually greater than book adjusted basis.

B)Tax adjusted basis is usually less than book adjusted basis.

C)Adjusted basis is cost basis less cost recovery deductions.

D)Tax adjusted basis may change over time.The tax adjusted basis is usually less than book adjusted basis because tax depreciation usually exceeds book depreciation.

A)Tax adjusted basis is usually greater than book adjusted basis.

B)Tax adjusted basis is usually less than book adjusted basis.

C)Adjusted basis is cost basis less cost recovery deductions.

D)Tax adjusted basis may change over time.The tax adjusted basis is usually less than book adjusted basis because tax depreciation usually exceeds book depreciation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

22

An installment sale is any sale where at least a portion of the sales proceeds is recognized in a subsequent taxable year.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

23

A simultaneous exchange must take place for a transaction to qualify as a like-kind exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

24

Which of the following realized gains results in a recognized gain?

A)Farm machinery traded for farm machinery.

B)Sale to a related party.

C)Involuntary conversion.

D)Iowa cropland exchanged for a Minnesota warehouse.Realized gains,but not losses,on sales to a related party are recognized.

A)Farm machinery traded for farm machinery.

B)Sale to a related party.

C)Involuntary conversion.

D)Iowa cropland exchanged for a Minnesota warehouse.Realized gains,but not losses,on sales to a related party are recognized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

25

Which of the following is not used in the calculation of the amount realized:

A)Cash.

B)Adjusted basis.

C)Fair market value of other property received.

D)Buyer's assumption of liabilities.

E)All of thesE.The amount realized is everything of value received (cash,fair market value of other property,and the buyer's assumption of liabilities) less selling costs.

A)Cash.

B)Adjusted basis.

C)Fair market value of other property received.

D)Buyer's assumption of liabilities.

E)All of thesE.The amount realized is everything of value received (cash,fair market value of other property,and the buyer's assumption of liabilities) less selling costs.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

26

§1239 recharacterizes 50 percent of the gain on sales to a related party as ordinary income.100 percent of the gain is recharacterized as ordinary income.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

27

A taxpayer that receives boot in a like-kind exchange resulting in a gain recognizes as gain the lesser of the fair market value of the boot received or the gain realized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

28

Losses on sales between related parties are realized but not recognized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

29

For a like-kind exchange,realized gain is deferred if the exchange is solely for like-kind property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

30

The §1231 lookback rule applies whether there is a net gain or loss.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

31

Which of the following is how gain or loss realized is calculated?

A)Cash less selling costs.

B)Cost basis less cost recovery.

C)Cash less cost recovery.

D)Amount realized less adjusted basis.

E)None of thesE.Gain or loss realized is simply the amount realized less adjusted basis.

A)Cash less selling costs.

B)Cost basis less cost recovery.

C)Cash less cost recovery.

D)Amount realized less adjusted basis.

E)None of thesE.Gain or loss realized is simply the amount realized less adjusted basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

32

Which of the following is not usually included in an asset's tax basis?

A)Purchase price

B)Sales tax

C)Shipping costs

D)Installation costs

E)None of these

A)Purchase price

B)Sales tax

C)Shipping costs

D)Installation costs

E)None of these

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

33

In a deferred like-kind exchange the like-kind property to be received must be identified within 45 days and acquired within 180 days from the initial exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

34

A net §1231 gain becomes ordinary while a net §1231 loss becomes long-term capital gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

35

Residential real property is not like-kind with non-residential real property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

36

Boot is not like-kind property involved in a like-kind exchange.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

37

For an installment sale,the gross profit percentage is the gain recognized divided by the gain realized.The gross profit percentage is the gain realized divided by the amount realized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

38

A loss realized for property destroyed in a hurricane is deferred under the involuntary conversion rules.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

39

The §1231 lookback rule recharacterizes §1231 gains if §1231 losses have created ordinary losses in the last 5 years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

40

Realized gains are recognized unless there is specific exception.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

41

Bozeman sold equipment that it uses in its business for $80,000.Bozeman bought the equipment two years ago for $75,000 and has claimed $20,000 of depreciation expense.What is the amount and character of Bozeman's gain or loss?

A)$25,000 §1231 gain.

B)$20,000 ordinary gain,and $5,000 §1231 gain.

C)$5,000 ordinary gain,and $20,000 §1231 gain.

D)$25,000 capital gain.

E)None of thesE.§1245 recaptures the lesser of depreciation taken ($20,000) or gain ($25,000) as ordinary income.The remaining $5,000 gain would be §1231 gain.

A)$25,000 §1231 gain.

B)$20,000 ordinary gain,and $5,000 §1231 gain.

C)$5,000 ordinary gain,and $20,000 §1231 gain.

D)$25,000 capital gain.

E)None of thesE.§1245 recaptures the lesser of depreciation taken ($20,000) or gain ($25,000) as ordinary income.The remaining $5,000 gain would be §1231 gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

42

Which of the following is not a §1245 asset if held for more than one year?

A)Machinery.

B)Automobile.

C)Building purchased in 1985 for which accelerated depreciation was elected.

D)Land.

E)None of thesE.Land is not subject to cost recovery and is a 1231 asset,but not a §1245 asset.

A)Machinery.

B)Automobile.

C)Building purchased in 1985 for which accelerated depreciation was elected.

D)Land.

E)None of thesE.Land is not subject to cost recovery and is a 1231 asset,but not a §1245 asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

43

What is the character of land used in an active trade or business for two years?

A)Capital.

B)Ordinary.

C)§1231.

D)Investment.

E)None of thesE.Land and depreciable assets used in a trade or business for more than one year are §1231 assets.

A)Capital.

B)Ordinary.

C)§1231.

D)Investment.

E)None of thesE.Land and depreciable assets used in a trade or business for more than one year are §1231 assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

44

The sale of computer equipment used in a trade or business for 9 months results in the following type of gain or loss?

A)Capital.

B)Ordinary.

C)§1231.

D)§1245.

E)None of thesE.Assets used in a trade or business and held for one year or less are ordinary assets.

A)Capital.

B)Ordinary.

C)§1231.

D)§1245.

E)None of thesE.Assets used in a trade or business and held for one year or less are ordinary assets.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

45

Which of the following sections does not currently recapture or recharacterize a taxpayer's gain?

A)§1239.

B)§1244.

C)§1245.

D)§1250.

E)None of thesE.§1250 no longer applies since straight line depreciation is used for real property.

A)§1239.

B)§1244.

C)§1245.

D)§1250.

E)None of thesE.§1250 no longer applies since straight line depreciation is used for real property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

46

The sale of machinery at a loss that was used in a trade or business and held for more than one year results in the following type of loss?

A)Capital.

B)§291.

C)§1231.

D)§1245.

E)None of thesE.Assets used in a trade or business and held for more than one year are §1231 assets and do not require depreciation recapture.

A)Capital.

B)§291.

C)§1231.

D)§1245.

E)None of thesE.Assets used in a trade or business and held for more than one year are §1231 assets and do not require depreciation recapture.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

47

Which of the following sections recaptures or recharacterizes only corporate taxpayer's gains?

A)§291.

B)§1239.

C)§1245.

D)Unrecaptured §1250 gains.

E)None of thesE.For corporate taxpayers only,§291 recaptures 20% of the lesser of gain realized or accumulated depreciation on real property.

A)§291.

B)§1239.

C)§1245.

D)Unrecaptured §1250 gains.

E)None of thesE.For corporate taxpayers only,§291 recaptures 20% of the lesser of gain realized or accumulated depreciation on real property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

48

Leesburg sold a machine for $2,200 on November 10th of the current year.The machine was purchased for $2,600.Leesburg had taken $1,200 of depreciation deductions on the machine through the date of the sale.What is Leesburg's gain or loss realized on the machine?

A)$800 gain.

B)$1,000 gain.

C)$1,200 loss.

D)$1,400 loss.

E)None of thesE.The gain realized is the $2,200 amount realized less the $1,400 ($2,600 - $1,200) adjusted basis.

A)$800 gain.

B)$1,000 gain.

C)$1,200 loss.

D)$1,400 loss.

E)None of thesE.The gain realized is the $2,200 amount realized less the $1,400 ($2,600 - $1,200) adjusted basis.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

49

Which of the following transactions results solely in §1245 gain?

A)Sale of machinery held for less than one year.

B)Sale of machinery held for more than one year and where the gain realized exceeds the accumulated deprecation.

C)Sale of machinery held for more than one year and where the accumulated deprecation exceeds the gain realized.

D)Sale of land held for more than one year and where the amount realized exceeds the adjusted basis.

E)None of thesE.§1245 gain is the lesser of gain realized or accumulated depreciation.

A)Sale of machinery held for less than one year.

B)Sale of machinery held for more than one year and where the gain realized exceeds the accumulated deprecation.

C)Sale of machinery held for more than one year and where the accumulated deprecation exceeds the gain realized.

D)Sale of land held for more than one year and where the amount realized exceeds the adjusted basis.

E)None of thesE.§1245 gain is the lesser of gain realized or accumulated depreciation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

50

Which of the following does not ultimately result in a capital gain or loss?

A)Sale of a personal use asset.

B)Sale of inventory.

C)Gain on equipment used in a trade or business held for more than one year,if it is the only asset sale during the year.

D)Sale of capital stock in another company.

E)None of thesE.Inventory is always an ordinary asset because it is held in the ordinary course of a trade or business.

A)Sale of a personal use asset.

B)Sale of inventory.

C)Gain on equipment used in a trade or business held for more than one year,if it is the only asset sale during the year.

D)Sale of capital stock in another company.

E)None of thesE.Inventory is always an ordinary asset because it is held in the ordinary course of a trade or business.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

51

The sale of land held for investment results in the following type of gain or loss?

A)Capital.

B)Ordinary.

C)§1231.

D)§1245.

E)None of thesE.Assets held for investment generate capital gains or losses.

A)Capital.

B)Ordinary.

C)§1231.

D)§1245.

E)None of thesE.Assets held for investment generate capital gains or losses.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

52

Foreaker LLC sold a piece of land that it uses in its business for $52,000.Foreaker bought the land two years ago for $42,500.What is the amount and character of Foreaker's gain?

A)$9,500 §1221.

B)$9,500 §1231.

C)$9,500 §1245.

D)$9,500 §1250.

E)None of thesE.Land used in a trade or business is a §1231 asset.

A)$9,500 §1221.

B)$9,500 §1231.

C)$9,500 §1245.

D)$9,500 §1250.

E)None of thesE.Land used in a trade or business is a §1231 asset.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

53

Which of the following results in an ordinary gain or loss?

A)Sale of a machine at a gain.

B)Sale of stock held for investment.

C)Sale of a §1231 asset.

D)Sale of inventory.

E)None of thesE.Inventory is always an ordinary asset.Sale of a §1231 asset can generate either ordinary gain or capital loss.

A)Sale of a machine at a gain.

B)Sale of stock held for investment.

C)Sale of a §1231 asset.

D)Sale of inventory.

E)None of thesE.Inventory is always an ordinary asset.Sale of a §1231 asset can generate either ordinary gain or capital loss.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

54

Brad sold a rental house that he owned for $250,000.Brad bought the rental house five years ago for $225,000 and has claimed $50,000 of depreciation expense.What is the amount and character of Brad's gain or loss?

A)$25,000 ordinary and $50,000 unrecaptured §1250 gain.

B)$25,000 §1231 gain and $50,000 unrecaptured §1250 gain.

C)$75,000 ordinary gain.

D)$75,000 capital gain.

E)None of thesE.Unrecaptured §1250 recaptures the lesser of depreciation taken ($50,000) or gain ($75,000) .This amount is then taxed at no more than 25%.The remaining $25,000 gain would be §1231 gain.

A)$25,000 ordinary and $50,000 unrecaptured §1250 gain.

B)$25,000 §1231 gain and $50,000 unrecaptured §1250 gain.

C)$75,000 ordinary gain.

D)$75,000 capital gain.

E)None of thesE.Unrecaptured §1250 recaptures the lesser of depreciation taken ($50,000) or gain ($75,000) .This amount is then taxed at no more than 25%.The remaining $25,000 gain would be §1231 gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

55

Which of the following gains does not result solely in an ordinary gain or loss?

A)Sale of equipment held for less than a year.

B)Sale of inventory.

C)Sale of equipment where the gain realized exceeds the accumulated depreciation.

D)Sale of equipment where the accumulated depreciation exceeds the gain realized.

E)None of thesE.Depreciation recapture,resulting in ordinary income,is limited to accumulated depreciation.

A)Sale of equipment held for less than a year.

B)Sale of inventory.

C)Sale of equipment where the gain realized exceeds the accumulated depreciation.

D)Sale of equipment where the accumulated depreciation exceeds the gain realized.

E)None of thesE.Depreciation recapture,resulting in ordinary income,is limited to accumulated depreciation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

56

Sumner sold equipment that it uses in its business for $30,000.Sumner bought the equipment a few years ago for $80,000 and has claimed $40,000 of depreciation expense.Assuming that this is Sumner's only disposition during the year,what is the amount and character of Sumner's gain or loss?

A)$10,000 §1231 loss.

B)$10,000 §1245 loss.

C)$50,000 ordinary loss.

D)$10,000 capital loss.

E)None of thesE.There is no depreciation recapture when a §1231 asset is sold at a loss.

A)$10,000 §1231 loss.

B)$10,000 §1245 loss.

C)$50,000 ordinary loss.

D)$10,000 capital loss.

E)None of thesE.There is no depreciation recapture when a §1231 asset is sold at a loss.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

57

Which of the following is true regarding depreciation recapture?

A)Changes the character of a loss.

B)Changes the character of a gain.

C)Changes the amount of a gain.

D)Only applies to ordinary assets.

E)None of thesE.Depreciation recapture changes the character of the gain from §1231 to ordinary.

A)Changes the character of a loss.

B)Changes the character of a gain.

C)Changes the amount of a gain.

D)Only applies to ordinary assets.

E)None of thesE.Depreciation recapture changes the character of the gain from §1231 to ordinary.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

58

Bateman Corporation sold an office building that it used in its business for $800,000.Bateman bought the building ten years ago for $600,000 and has claimed $200,000 of depreciation expense.What is the amount and character of Bateman's gain or loss?

A)$40,000 ordinary and $360,000 §1231 gain.

B)$200,000 ordinary and $200,000 §1231 gain.

C)$400,000 ordinary gain.

D)$400,000 capital gain.

E)None of thesE.For corporations,§291 recapture is 20 percent of the lesser of depreciation taken or the realized gain as ordinary income.The remaining gain is §1231.

A)$40,000 ordinary and $360,000 §1231 gain.

B)$200,000 ordinary and $200,000 §1231 gain.

C)$400,000 ordinary gain.

D)$400,000 capital gain.

E)None of thesE.For corporations,§291 recapture is 20 percent of the lesser of depreciation taken or the realized gain as ordinary income.The remaining gain is §1231.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

59

Butte sold a machine to a machine dealer for $50,000.Butte bought the machine for $55,000 several years ago and has claimed $12,500 of depreciation expense on the machine.What is the amount and character of Butte's gain or loss?

A)$7,500 §1231 loss.

B)$5,000 §1231 loss.

C)$7,500 ordinary gain.

D)$7,500 capital gain.

E)None of thesE.§1245 recaptures the lesser of depreciation taken ($12,500) or gain ($7,500) as ordinary income.Any remaining gain would be §1231 gain.

A)$7,500 §1231 loss.

B)$5,000 §1231 loss.

C)$7,500 ordinary gain.

D)$7,500 capital gain.

E)None of thesE.§1245 recaptures the lesser of depreciation taken ($12,500) or gain ($7,500) as ordinary income.Any remaining gain would be §1231 gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

60

The sale of machinery for more than the original cost basis (before depreciation) ,used in a trade or business,and held for more than one year results in the following types of gain or loss?

A)Capital and Ordinary.

B)Ordinary only.

C)Capital and §1231.

D)§1245 and §1231.

E)None of thesE.Because the sales price exceeds the original basis,§1245 depreciation recapture and §1231 gain will be recognized.

A)Capital and Ordinary.

B)Ordinary only.

C)Capital and §1231.

D)§1245 and §1231.

E)None of thesE.Because the sales price exceeds the original basis,§1245 depreciation recapture and §1231 gain will be recognized.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

61

What is the primary purpose of a third-party intermediary in a deferred like-kind exchange?

A)To facilitate finding replacement property.

B)To help acquire the replacement property.

C)To prevent the seller from receiving cash (boot) that will taint the transaction.

D)To certify the taxpayer's Form 8824.

E)All of thesE.The receipt of cash in a transaction qualifies as boot and requires the recognition of gain.

A)To facilitate finding replacement property.

B)To help acquire the replacement property.

C)To prevent the seller from receiving cash (boot) that will taint the transaction.

D)To certify the taxpayer's Form 8824.

E)All of thesE.The receipt of cash in a transaction qualifies as boot and requires the recognition of gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

62

Why does §1250 recapture no longer apply?

A)Congress repealed the code section.

B)The Tax Reform Act of 1986 changed the depreciation of real property to the straight-line method.

C)§1245 recapture trumps §1250 recapture.

D)Because unrecaptured §1250 gains now apply to all taxpayers instead.

E)None of thesE.§1250 only recaptures excess depreciation,the excess of accelerated over straight-line depreciation.

A)Congress repealed the code section.

B)The Tax Reform Act of 1986 changed the depreciation of real property to the straight-line method.

C)§1245 recapture trumps §1250 recapture.

D)Because unrecaptured §1250 gains now apply to all taxpayers instead.

E)None of thesE.§1250 only recaptures excess depreciation,the excess of accelerated over straight-line depreciation.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

63

Ashburn reported a $105,000 net §1231 gain in year 6.Assuming Ashburn reported $60,000 of nonrecaptured §1231 losses during years 1-5,what amount of Ashburn's net §1231 gain for year 6,if any,is treated as ordinary income?

A)$0.

B)$45,000.

C)$60,000.

D)$105,000.

E)None of thesE.The 1231 lookback rule recharacterizes $60,000 of the §1231 gain to ordinary income,the amount of the prior 5 year losses that received ordinary loss treatment.

A)$0.

B)$45,000.

C)$60,000.

D)$105,000.

E)None of thesE.The 1231 lookback rule recharacterizes $60,000 of the §1231 gain to ordinary income,the amount of the prior 5 year losses that received ordinary loss treatment.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

64

When does unrecaptured §1250 gains apply?

A)When the taxpayer makes the election.

B)It applies only when non-corporate taxpayers sell depreciable real property at a gain.

C)It applies when §1245 recapture trumps §1250 recapture.

D)It applies only when real property purchased before 1986 is sold at a gain.

E)None of thesE.Unrecaptured §1250 gain only applies to the lesser of realized gain or accumulated depreciation on sales of real property by non-corporate taxpayers.

A)When the taxpayer makes the election.

B)It applies only when non-corporate taxpayers sell depreciable real property at a gain.

C)It applies when §1245 recapture trumps §1250 recapture.

D)It applies only when real property purchased before 1986 is sold at a gain.

E)None of thesE.Unrecaptured §1250 gain only applies to the lesser of realized gain or accumulated depreciation on sales of real property by non-corporate taxpayers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

65

Winchester LLC sold the following business assets during the current year: (1) automobile,$30,000 cost basis,$12,000 depreciation,proceeds $20,000; (2) machinery,$25,000 cost basis,$20,000 depreciation,proceeds $10,000; (3) furniture,$15,000 cost basis,$10,000 depreciation,proceeds $4,000; (4) computer equipment,$25,000 cost basis,$6,000 depreciation,proceeds $10,000; (5) Winchester had unrecaptured §1231 losses of $3,000 in the prior 5 years.What is the amount and character of Winchester's gains and losses before the 1231 netting process?

A)$3,000 ordinary loss,$0 §1231 loss.

B)$7,000 ordinary gain,$10,000 §1231 loss.

C)$7,000 ordinary loss,$4,000 §1231 gain.

D)$1,000 ordinary gain,$4,000 §1231 loss.

E)None of thesE.All of the assets are §1231 assets: automobile $2,000 gain,machinery $5,000 gain,furniture $1,000 loss,and equipment $9,000 loss.This results in $7,000 ordinary gain and $10,000 1231 loss.The 1231 lookback rule only applies when there is a net 1231 gain.

A)$3,000 ordinary loss,$0 §1231 loss.

B)$7,000 ordinary gain,$10,000 §1231 loss.

C)$7,000 ordinary loss,$4,000 §1231 gain.

D)$1,000 ordinary gain,$4,000 §1231 loss.

E)None of thesE.All of the assets are §1231 assets: automobile $2,000 gain,machinery $5,000 gain,furniture $1,000 loss,and equipment $9,000 loss.This results in $7,000 ordinary gain and $10,000 1231 loss.The 1231 lookback rule only applies when there is a net 1231 gain.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

66

Which of the following is not true regarding §1239?

A)It only applies to related taxpayers.

B)It only applies to gains on sales of depreciable property.

C)It only applies to gains on sales of non-residential real property.

D)It does not apply to losses.

E)None of thesE.§1239 only applies to gains on sales of depreciable property between related taxpayers.

A)It only applies to related taxpayers.

B)It only applies to gains on sales of depreciable property.

C)It only applies to gains on sales of non-residential real property.

D)It does not apply to losses.

E)None of thesE.§1239 only applies to gains on sales of depreciable property between related taxpayers.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

67

Koch traded machine 1 for machine 2.Koch originally purchased machine 1 for $75,000 and machine 1's adjusted basis was $40,000 at the time of the exchange.Machine 2's seller purchased it for $65,000 and machine 2's adjusted basis was $55,000 at the time of the exchange.What is Koch's adjusted basis in machine 2 after the exchange?

A)$40,000.

B)$50,000.

C)$55,000.

D)$75,000.

E)None of thesE.The exchange qualifies as a like-kind exchange.Since no boot was transferred,Koch's basis in the new machine is the basis in its old machine.

A)$40,000.

B)$50,000.

C)$55,000.

D)$75,000.

E)None of thesE.The exchange qualifies as a like-kind exchange.Since no boot was transferred,Koch's basis in the new machine is the basis in its old machine.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

68

Which of the following is not an involuntary conversion?

A)Destruction caused by a hurricane.

B)Imminent domain.

C)A foreclosure.

D)Fire damage.

E)All of these are involuntary conversions.

A)Destruction caused by a hurricane.

B)Imminent domain.

C)A foreclosure.

D)Fire damage.

E)All of these are involuntary conversions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

69

Which of the following is true regarding the §1231 lookback rule?

A)It only applies when a §1231 loss occurs.

B)It only applies when a §1231 gain occurs.

C)It only applies when a §1231 gain occurs and there is a nonrecaptured §1231 loss in the prior five years.

D)It only applies when a §1231 gain occurs and there is a nonrecaptured §1231 gain in the prior five years.

E)None of thesE.The lookback rule only recharacterizes a current year 1231 gain if there are 1231 losses from the prior 5 years.

A)It only applies when a §1231 loss occurs.

B)It only applies when a §1231 gain occurs.

C)It only applies when a §1231 gain occurs and there is a nonrecaptured §1231 loss in the prior five years.

D)It only applies when a §1231 gain occurs and there is a nonrecaptured §1231 gain in the prior five years.

E)None of thesE.The lookback rule only recharacterizes a current year 1231 gain if there are 1231 losses from the prior 5 years.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

70

How long does a taxpayer have to identify replacement property in a like-kind exchange?

A)The like-kind property to be received must be identified within 45 days.

B)The like-kind property to be received must be identified by the earlier of 45 days or the last day of the taxpayer's taxable year.

C)The like-kind property to be received must be identified within 180 days.

D)There is no deadline for the identification of replacement property.

E)All of thesE.The replacement property must be identified within 45 days.

A)The like-kind property to be received must be identified within 45 days.

B)The like-kind property to be received must be identified by the earlier of 45 days or the last day of the taxpayer's taxable year.

C)The like-kind property to be received must be identified within 180 days.

D)There is no deadline for the identification of replacement property.

E)All of thesE.The replacement property must be identified within 45 days.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

71

Brandon,an individual,began business four years ago and has never sold a §1231 asset.Brandon owned each of the assets for several years.In the current year,Brandon sold the following business assets: Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

A)$7,000 ordinary income,$1,000 §1231 loss and $2,100 tax liability.

B)$6,000 ordinary income and $2,100 tax liability.

C)$7,000 §1231 gain and $2,450 tax liability.

D)$7,000 §1231 gain and $1,050 tax liability.

E)None of thesE.The depreciation recapture of $7,000 becomes ordinary income.The $4,000 §1231 loss becomes an ordinary loss and offsets the $3,000 §1231 gain on the machinery.The $1,000 net §1231 loss becomes ordinary and offsets the $7,000 ordinary gain.The remaining ordinary gain of $6,000 is taxed at 35 percent which results in $2,100 of tax.

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?A)$7,000 ordinary income,$1,000 §1231 loss and $2,100 tax liability.

B)$6,000 ordinary income and $2,100 tax liability.

C)$7,000 §1231 gain and $2,450 tax liability.

D)$7,000 §1231 gain and $1,050 tax liability.

E)None of thesE.The depreciation recapture of $7,000 becomes ordinary income.The $4,000 §1231 loss becomes an ordinary loss and offsets the $3,000 §1231 gain on the machinery.The $1,000 net §1231 loss becomes ordinary and offsets the $7,000 ordinary gain.The remaining ordinary gain of $6,000 is taxed at 35 percent which results in $2,100 of tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

72

Alpha sold machinery,which it used in its business,to Beta,a related entity,for $40,000.Beta used the machinery in its business.Alpha bought the equipment a few years ago for $50,000 and has claimed $30,000 of depreciation expense.What is the amount and character of Alpha's gain?

A)$20,000 ordinary income under §1239.

B)$10,000 ordinary gain and $10,000 §1231 gain.

C)$20,000 ordinary gain.

D)$20,000 capital gain.

E)None of thesE.§1239 recharacterizes the entire gain as ordinary income when depreciable property is sold to a related party.

A)$20,000 ordinary income under §1239.

B)$10,000 ordinary gain and $10,000 §1231 gain.

C)$20,000 ordinary gain.

D)$20,000 capital gain.

E)None of thesE.§1239 recharacterizes the entire gain as ordinary income when depreciable property is sold to a related party.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

73

Each of the following is true except for:

A)A direct involuntary conversion occurs when property taken under imminent domain is replaced with other property.

B)Qualified replacement property rules are more restrictive than the like-kind property rules.

C)An indirect involuntary conversion occurs when property is destroyed and insurance proceeds are used to purchase qualified replacement property.

D)Losses realized in involuntary conversions are deferred.

E)All of these are truE.Losses realized in an involuntary conversion are realized;while losses realized in a like-kind exchange are deferred.

A)A direct involuntary conversion occurs when property taken under imminent domain is replaced with other property.

B)Qualified replacement property rules are more restrictive than the like-kind property rules.

C)An indirect involuntary conversion occurs when property is destroyed and insurance proceeds are used to purchase qualified replacement property.

D)Losses realized in involuntary conversions are deferred.

E)All of these are truE.Losses realized in an involuntary conversion are realized;while losses realized in a like-kind exchange are deferred.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

74

Which one of the following is not considered boot in a like-kind exchange?

A)Cash.

B)Other property.

C)Mortgage given.

D)Mortgage received.

E)All of thesE.Mortgage received is treated as transferring cash to the other party,and thus it is not boot to the recipient.

A)Cash.

B)Other property.

C)Mortgage given.

D)Mortgage received.

E)All of thesE.Mortgage received is treated as transferring cash to the other party,and thus it is not boot to the recipient.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

75

Mary traded furniture used in her business to a furniture dealer for some new furniture.Mary originally purchased the furniture for $45,000 and it had an adjusted basis of $20,000 at the time of the exchange.The new furniture had a fair market value of $40,000.Mary also gave $4,000 to the dealer in the transaction.What is Mary's adjusted basis in the new furniture after the exchange?

A)$20,000.

B)$24,000.

C)$36,000.

D)$40,000.

E)None of thesE.The exchange qualifies as a like-kind exchange.Since boot was given in the transaction,the fair market value of the boot given ($4,000) is added to the adjusted basis ($20,000) of the property given up.

A)$20,000.

B)$24,000.

C)$36,000.

D)$40,000.

E)None of thesE.The exchange qualifies as a like-kind exchange.Since boot was given in the transaction,the fair market value of the boot given ($4,000) is added to the adjusted basis ($20,000) of the property given up.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

76

Brandon,an individual,began business four years ago and has sold §1231 assets with $5,000 of losses within the last 5 years.Brandon owned each of the assets for several years.In the current year,Brandon sold the following business assets: Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?

A)$25,000 ordinary income,$8,750 tax liability.

B)$25,000 §1231 gain and $3,750 tax liability.

C)$13,000 §1231 gain,$12,000 ordinary income,and $6,150 tax liability.

D)$12,000 §1231 gain,$13,000 ordinary income,and $6,350 tax liability.

E)None of thesE.Depreciation recapture of $7,000 becomes ordinary income.In addition,Brandon has a $23,000 §1231 gain and $5,000 §1231 loss,which nets to an $18,000 net §1231 gain.The 1231 lookback rule recharacterizes $5,000 of the §1231 gain to ordinary income.Thus,$12,000 (35%) of ordinary income and $13,000 (15%) of §1231 gain.The calculations results in $6,150 of tax.

Assuming Brandon's marginal ordinary income tax rate is 35 percent,what effect do the gains and losses have on Brandon's tax liability?A)$25,000 ordinary income,$8,750 tax liability.

B)$25,000 §1231 gain and $3,750 tax liability.

C)$13,000 §1231 gain,$12,000 ordinary income,and $6,150 tax liability.

D)$12,000 §1231 gain,$13,000 ordinary income,and $6,350 tax liability.

E)None of thesE.Depreciation recapture of $7,000 becomes ordinary income.In addition,Brandon has a $23,000 §1231 gain and $5,000 §1231 loss,which nets to an $18,000 net §1231 gain.The 1231 lookback rule recharacterizes $5,000 of the §1231 gain to ordinary income.Thus,$12,000 (35%) of ordinary income and $13,000 (15%) of §1231 gain.The calculations results in $6,150 of tax.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

77

Which one of the following is not a requirement of a deferred like-kind exchange?

A)The like-kind property to be received must be identified within 45 days.

B)The exchange must be completed within the taxable year.

C)The like-kind property must be received within 180 days.

D)A third party intermediary is often used to facilitate the exchange.

E)All of thesE.The exchange must be completed by the due date of the taxpayer's return including extensions.

A)The like-kind property to be received must be identified within 45 days.

B)The exchange must be completed within the taxable year.

C)The like-kind property must be received within 180 days.

D)A third party intermediary is often used to facilitate the exchange.

E)All of thesE.The exchange must be completed by the due date of the taxpayer's return including extensions.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

78

The general rule regarding the exchanged basis in a like-kind exchange is:

A)The basis is equal to the fair market value of the new property.

B)The basis is equal to the fair market value of the old property.

C)The basis is equal to the adjusted basis of the old property.

D)The basis is equal to the cost basis of the old property.

E)All of thesE.The general rule is that the property receives a carryover basis from the old property.

A)The basis is equal to the fair market value of the new property.

B)The basis is equal to the fair market value of the old property.

C)The basis is equal to the adjusted basis of the old property.

D)The basis is equal to the cost basis of the old property.

E)All of thesE.The general rule is that the property receives a carryover basis from the old property.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

79

Which one of the following is not true regarding a like-kind exchange?

A)Loss on like-kind property is not recognized.

B)Gains on boot given are deferred.

C)Losses on boot given are not recognized.

D)Securities can be like-kind with any other securities.

E)All of thesE.Losses on boot,but not like-kind property,given are recognized currently.

A)Loss on like-kind property is not recognized.

B)Gains on boot given are deferred.

C)Losses on boot given are not recognized.

D)Securities can be like-kind with any other securities.

E)All of thesE.Losses on boot,but not like-kind property,given are recognized currently.

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

80

Arlington LLC traded machinery used in its business to a machinery dealer for some new machinery.Arlington originally purchased the machinery for $60,000 and it had an adjusted basis of $28,000 at the time of the exchange.The new machinery had a fair market value of $35,000.Arlington also received $2,000 of office equipment in the transaction.What is Arlington's gain or loss recognized on the exchange?

A)$0.

B)$2,000.

C)$7,000.

D)$9,000.

E)None of thesE.The gain recognized is the lesser of the fair market value of the boot ($2,000 of office equipment) or realized gain of $9,000 ($35,000 fair market value plus $2,000 boot less $28,000 adjusted basis) .

A)$0.

B)$2,000.

C)$7,000.

D)$9,000.

E)None of thesE.The gain recognized is the lesser of the fair market value of the boot ($2,000 of office equipment) or realized gain of $9,000 ($35,000 fair market value plus $2,000 boot less $28,000 adjusted basis) .

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.

فتح الحزمة

k this deck

فتح الحزمة

افتح القفل للوصول البطاقات البالغ عددها 88 في هذه المجموعة.