ABC Bank has $39 million invested in T-Bonds with a 16-year duration, $39 million in 6 month maturity T-Bills, and $75 million invested in consumer loans with a 3 year duration. If they are all portfolios of this bank, what is the duration of the bank's asset portfolio in years?

A) 5.95 years

B) 6.50 years

C) 7.23 years

D) 8.78 years

E) 9.51 years

Refer to the information below for questions 15-17:

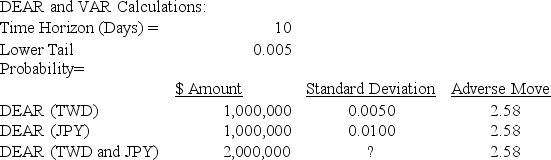

As a portfolio manager of Asian Investments and Co., you like to evaluate the Value-at-Risk of your currency holding of Taiwanese and Japanese assets. Use the historical data in the past 20 years, you obtain the following information regarding the exchange rate between USD ($) with Taiwanese Dollar (TWD) and Japanese Yen (JPY) : where DEAR is daily earnings-at-risk, standard deviation is the volatility calculated by the historical data, adverse move is the t-value of the lower bound of the distribution of asset value.

where DEAR is daily earnings-at-risk, standard deviation is the volatility calculated by the historical data, adverse move is the t-value of the lower bound of the distribution of asset value.

Correct Answer:

Verified

Q20: Maximizing a bank's profit, providing liquidity, and

Q21: Which one of the following is a

Q22: The number of futures contracts that a

Q23: If the coefficient of correlation between USD/TWD

Q24: In 2008, many banks encounter liquidity issues

Q26: What is Formosa International Bank's total net

Q27: Bank A has a loan to deposit

Q30: Please calculate the 10-day Value-at-Risk (VaR) for

Q34: Refer to the information below for questions

Q36: Which one of the following situations creates

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents