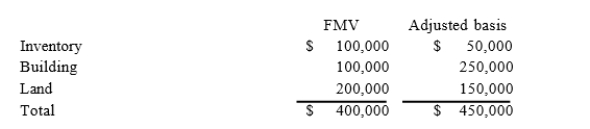

Phillip incorporated his sole proprietorship by transferring inventory, a building, and land to the corporation in return for 100 percent of the corporation's stock. The property transferred to the corporation had the following fair market values and tax-adjusted bases.  The fair market value of the corporation's stock received in the exchange was $400,000. The transaction met the requirements to be tax-deferred under §351.a. What amount of net gain or loss does Phillip realize on the transfer of the property to his corporation? b. What amount of gain or loss does Phillip recognize on the transfer of the property to his corporation? c. What is the corporation's adjusted basis in each of the assets received in the exchange?

The fair market value of the corporation's stock received in the exchange was $400,000. The transaction met the requirements to be tax-deferred under §351.a. What amount of net gain or loss does Phillip realize on the transfer of the property to his corporation? b. What amount of gain or loss does Phillip recognize on the transfer of the property to his corporation? c. What is the corporation's adjusted basis in each of the assets received in the exchange?

Correct Answer:

Verified

b. Phillip does not ...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q61: Celeste transferred 100 percent of her stock

Q62: Which of the following statements does not

Q63: Keegan incorporated his sole proprietorship by transferring

Q64: Keegan incorporated his sole proprietorship by transferring

Q65: Robin transferred her 60 percent interest to

Q67: Juan transferred 100 percent of his stock

Q68: Which of the following statements best describes

Q69: Packard Corporation transferred its 100 percent interest

Q70: Which of the following statements does not

Q71: Francine incorporated her sole proprietorship by transferring

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents