A model that attracted quite a bit of interest in macroeconomics in the 1970s was the St.

Louis model.The underlying idea was to calculate fiscal and monetary impact and long

run cumulative dynamic multipliers, by relating output (growth)to government

expenditure (growth)and money supply (growth).The assumption was that both

government expenditures and the money supply were exogenous.Estimation of a St.

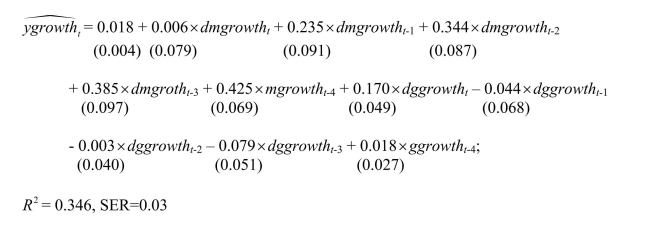

Louis type model using quarterly data from 1960:I-1995:IV results in the following

output (HAC standard errors in parenthesis):  where ygrowth is quarterly growth of real GDP, mgrowth is quarterly growth of real money supply (M2), and ggrowth is quarterly growth of real government expenditures. "d" in front of ggrowth and mgrowth indicates a change in the variable. (a)Assuming that money and government expenditures are exogenous, what do the

where ygrowth is quarterly growth of real GDP, mgrowth is quarterly growth of real money supply (M2), and ggrowth is quarterly growth of real government expenditures. "d" in front of ggrowth and mgrowth indicates a change in the variable. (a)Assuming that money and government expenditures are exogenous, what do the

coefficients represent? Calculate the h-period cumulative dynamic multipliers from these.

How can you test for the statistical significance of the cumulative dynamic multipliers

and the long-run cumulative dynamic multiplier?

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q24: In the distributed lag model, the dynamic

Q25: Money supply is linked to the monetary

Q26: Your textbook mentions heteroskedasticity- and autocorrelation- consistent

Q29: To estimate dynamic causal effects, your textbook

Q32: Consider the following model

Q33: The distributed lag model relating orange

Q35: GLS is consistent and BLUE if

Q37: Your textbook presents as an example of

Q39: It has been argued that Canada's aggregate

Q40: One of the central predictions of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents