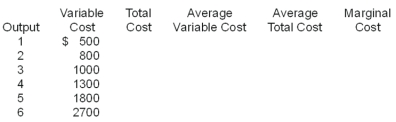

You should do this problem in three steps. First: Fill in Table 1. Assume fixed cost is $1000 and price is $575.

Table 1:

Table 2:

Second: Draw a graph of the firm's demand, marginal revenue, average variable cost, average total cost, and marginal cost curves on a piece of graph paper. Be sure to label the graph correctly. On the graph, indicate the break-even and shutdown points and the firm's short-run and long-run supply curves. Third: Calculate total profit in the space below, then answer questions a through d.

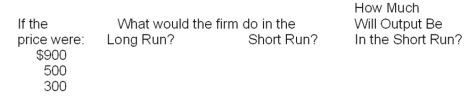

(a) The minimum price the firm will accept in the short run is $_______. (b) The minimum price the firm will accept in the long run is $_______. (c) The output at which the firm will maximize profits is ______. (d) The output at which the firm will operate most efficiently is _______.

Correct Answer:

Verified

Total profit= (Price ...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q342: Q349: Q356: Q357: Given the industry supply and demand shown Q359: (a) Find the total profit or total Q361: If economic profits are $100,000 and implicit Q362: (a) Find the total profit or total Q362: Given the information that follows,how much are Q364: (a) Find the total profit or total Q365: Given the information that follows,how much is Unlock this Answer For Free Now! View this answer and more for free by performing one of the following actions Scan the QR code to install the App and get 2 free unlocks Unlock quizzes for free by uploading documents![]()

![]()

![]()