Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

النسخة 17الرقم المعياري الدولي: 978-0078025778Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

النسخة 17الرقم المعياري الدولي: 978-0078025778 تمرين 36

Reporting Operating Cash Flows by the Direct Method

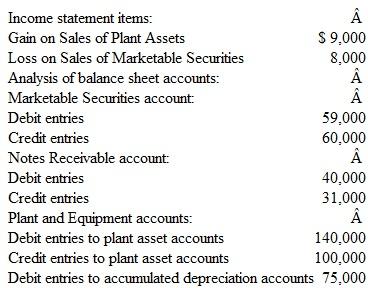

An analysis of the income statement and the balance sheet accounts of RPZ Imports at December 31, 2015, provides the following information:

Additional Information

1. Except as noted in 4, payments and proceeds relating to investing transactions were made in cash.

2. The marketable securities are not cash equivalents.

3. All notes receivable relate to cash loans made to borrowers, not to receivables from customers.

4. Purchases of new equipment during the year ($140,000) were financed by paying $50,000 in cash and issuing a long-term note payable for $90,000.

5. Debits to the accumulated depreciation accounts are made whenever depreciable plant assets are retired. Thus, the book value of plant assets sold or retired during the year was $25,000 ($100,000 - $75,000).

Instructions

a. Prepare the investing activities section of a statement of cash flows. Show supporting computations for the amounts of (1) proceeds from sales and marketable securities and (2) proceeds from sales from plant assets. Place brackets around numbers representing cash outflows.

b. Prepare the supplementary schedule that should accompany the statement of cash flows in order to disclose the noncash aspects of the company's investing and financing activities.

c. Does management have more control or less control over the timing and amount of cash outlays for investing activities than for operating activities? Explain.

An analysis of the income statement and the balance sheet accounts of RPZ Imports at December 31, 2015, provides the following information:

Additional Information

1. Except as noted in 4, payments and proceeds relating to investing transactions were made in cash.

2. The marketable securities are not cash equivalents.

3. All notes receivable relate to cash loans made to borrowers, not to receivables from customers.

4. Purchases of new equipment during the year ($140,000) were financed by paying $50,000 in cash and issuing a long-term note payable for $90,000.

5. Debits to the accumulated depreciation accounts are made whenever depreciable plant assets are retired. Thus, the book value of plant assets sold or retired during the year was $25,000 ($100,000 - $75,000).

Instructions

a. Prepare the investing activities section of a statement of cash flows. Show supporting computations for the amounts of (1) proceeds from sales and marketable securities and (2) proceeds from sales from plant assets. Place brackets around numbers representing cash outflows.

b. Prepare the supplementary schedule that should accompany the statement of cash flows in order to disclose the noncash aspects of the company's investing and financing activities.

c. Does management have more control or less control over the timing and amount of cash outlays for investing activities than for operating activities? Explain.

التوضيح موثّق

موثّق

Cash flow statement: It is part of finan...

Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255