Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

النسخة 17الرقم المعياري الدولي: 978-0078025778Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

النسخة 17الرقم المعياري الدولي: 978-0078025778 تمرين 15

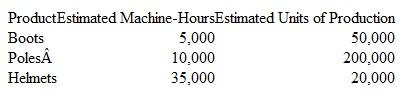

Downhill Fast manufactures three ski products: boots, poles, and helmets. The company allocates manufacturing costs lo each product line based on machine-hours. A large portion of its manufacturing overhead cost is incurred by the Maintenance Department. This year, the department anticipates that it will incur $250,000 in total costs. The following estimates pertain to the upcoming year:

Carol Safooma. the company's cost accountant, suspects that unit costs are being distorted by using a single activity base to allocate Maintenance Department costs to products. She is considering the implementation of an activity-based costing system (ABC).

Carol Safooma. the company's cost accountant, suspects that unit costs are being distorted by using a single activity base to allocate Maintenance Department costs to products. She is considering the implementation of an activity-based costing system (ABC).

Under the proposed ABC system, the maintenance costs wouid be allocated to the following activity cost pools using the number of work orders as an activity base: (l) the equipment set-up pool, and (2) the custodial pool. Of the 2.400 work orders filed with the Maintenance Department each year, approximately 600 relate to equipment set-up activities, whereas 1.800 relate to custodial functions.

Equipment set-ups correlate with the number of production runs associated with each product line. Thus, the equipment set-up pool would be allocated based on the number of production runs required for each product. Custodial services correlate w ith square feet of production space, and w ould be allocated based on the space required to produce each product line. The following table provides a summary of annual production activity and square footage requirements:

Instructions

Instructions

a. Calculate the amount of Maintenance Department costs that would be allocated to each product line (on a per-unit basis) using machine-hours as a single activity base.

b. Calculate the amount of Maintenance Department costs that would be allocated to each product line (on a per-unit basis) using the proposed ABC system.

c. Are cost allocations currently being distorted using machine-hours as a single activity base? Defend your answer.

Carol Safooma. the company's cost accountant, suspects that unit costs are being distorted by using a single activity base to allocate Maintenance Department costs to products. She is considering the implementation of an activity-based costing system (ABC).Under the proposed ABC system, the maintenance costs wouid be allocated to the following activity cost pools using the number of work orders as an activity base: (l) the equipment set-up pool, and (2) the custodial pool. Of the 2.400 work orders filed with the Maintenance Department each year, approximately 600 relate to equipment set-up activities, whereas 1.800 relate to custodial functions.

Equipment set-ups correlate with the number of production runs associated with each product line. Thus, the equipment set-up pool would be allocated based on the number of production runs required for each product. Custodial services correlate w ith square feet of production space, and w ould be allocated based on the space required to produce each product line. The following table provides a summary of annual production activity and square footage requirements:

Instructions a. Calculate the amount of Maintenance Department costs that would be allocated to each product line (on a per-unit basis) using machine-hours as a single activity base.

b. Calculate the amount of Maintenance Department costs that would be allocated to each product line (on a per-unit basis) using the proposed ABC system.

c. Are cost allocations currently being distorted using machine-hours as a single activity base? Defend your answer.

التوضيح موثّق

موثّق

a. Maintenance department costs allocate...

Financial & Managerial Accounting 17th Edition by Jan Williams ,Susan Haka,Mark Bettner,Joseph Carcello

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255