Introduction to Econometrics 3rd Edition by James Stock, James Stock

النسخة 3الرقم المعياري الدولي: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, James Stock

النسخة 3الرقم المعياري الدولي: 978-9352863501 تمرين 13

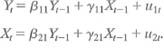

Consider the following two-variable VAR model with one lag and no intercept:

a. Show that the iterated two-period-ahead forecast for Y can be written as and derive values for

and derive values for  1 and

1 and  2 in terms of the coefficients in the VAR.

2 in terms of the coefficients in the VAR.

b. In light of your answer to (a), do iterated multiperiod forecasts differ from direct multiperiod forecasts Explain.

a. Show that the iterated two-period-ahead forecast for Y can be written as

and derive values for 1 and 2 in terms of the coefficients in the VAR.b. In light of your answer to (a), do iterated multiperiod forecasts differ from direct multiperiod forecasts Explain.

التوضيح موثّق

موثّق

a) The vector autoregression (VAR) model...

Introduction to Econometrics 3rd Edition by James Stock, James Stock

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255