Introductory Econometrics 4th Edition by Jeffrey Wooldridge

النسخة 4الرقم المعياري الدولي: 978-0324660609Introductory Econometrics 4th Edition by Jeffrey Wooldridge

النسخة 4الرقم المعياري الدولي: 978-0324660609 تمرين 9

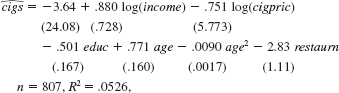

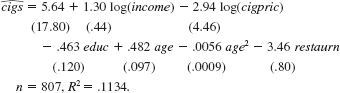

In Example 8.7, we computed the OLS and a set of WLS estimates in a cigarette demand equation.

(i) Obtain the OLS estimates in equation.

(ii) Obtain the i used in the WLS estimation of equation and reproduce equation. From this equation, obtain the unweighted residuals and fitted values; call these ui and yi , respectively. (For example, in Stata, the unweighted residuals and fitted values are given by default.)

(iii) Let . be the weighted quantities. Carry out the special case of the White test for heteroskedasticity by regressing

. be the weighted quantities. Carry out the special case of the White test for heteroskedasticity by regressing  being sure to include an intercept, as always. Do you find heteroskedasticity in the weighted residuals

being sure to include an intercept, as always. Do you find heteroskedasticity in the weighted residuals

(iv) What does the finding from part (iii) imply about the proposed form of heteroske-dasticity used in obtaining (8.36)

(v) Obtain valid standard errors for the WLS estimates that allow the variance function to be misspecified.

Equation

Equation

(i) Obtain the OLS estimates in equation.

(ii) Obtain the i used in the WLS estimation of equation and reproduce equation. From this equation, obtain the unweighted residuals and fitted values; call these ui and yi , respectively. (For example, in Stata, the unweighted residuals and fitted values are given by default.)

(iii) Let

. be the weighted quantities. Carry out the special case of the White test for heteroskedasticity by regressing being sure to include an intercept, as always. Do you find heteroskedasticity in the weighted residuals (iv) What does the finding from part (iii) imply about the proposed form of heteroske-dasticity used in obtaining (8.36)

(v) Obtain valid standard errors for the WLS estimates that allow the variance function to be misspecified.

Equation

Equation

التوضيح

هذا السؤال ليس له إجابة موثقة من أحد الخبراء بعد، دع الذكاء الاصطناعي Copilot في كويز بلس يساعدك في إيجاد الحل.

Introductory Econometrics 4th Edition by Jeffrey Wooldridge

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255