Introductory Econometrics 4th Edition by Jeffrey Wooldridge

النسخة 4الرقم المعياري الدولي: 978-0324660609Introductory Econometrics 4th Edition by Jeffrey Wooldridge

النسخة 4الرقم المعياري الدولي: 978-0324660609 تمرين 12

Use INTQRT.RAW for this exercise.

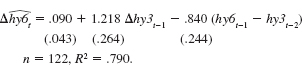

(i) In Example 18.7, we estimated an error correction model for the holding yield on six-month T-bills, where one lag of the holding yield on three-month T-bills is the explanatory variable. We assumed that the cointegration parameter was one in the equation hy6t = + hy3t-1 + ut. Now, add the lead change, hy3t-2, the contemporaneous change, hy3t-1, and the lagged change, hy3t-2, of hy3t- 1. That is, estimate the equation

and report the results in equation form. Test H0: = 1 against a two-sided alternative. Assume that the lead and lag are sufficient so that {hy3t-1} is strictly exogenous in this equation and do not worry about serial correlation.

(ii) To the error correction model in, add hy3t-2 and (hy6t-2 - hy3t-3). Are these terms jointly significant What do you conclude about the appropriate error correction model

Equation

(i) In Example 18.7, we estimated an error correction model for the holding yield on six-month T-bills, where one lag of the holding yield on three-month T-bills is the explanatory variable. We assumed that the cointegration parameter was one in the equation hy6t = + hy3t-1 + ut. Now, add the lead change, hy3t-2, the contemporaneous change, hy3t-1, and the lagged change, hy3t-2, of hy3t- 1. That is, estimate the equation

and report the results in equation form. Test H0: = 1 against a two-sided alternative. Assume that the lead and lag are sufficient so that {hy3t-1} is strictly exogenous in this equation and do not worry about serial correlation.

(ii) To the error correction model in, add hy3t-2 and (hy6t-2 - hy3t-3). Are these terms jointly significant What do you conclude about the appropriate error correction model

Equation

التوضيح

هذا السؤال ليس له إجابة موثقة من أحد الخبراء بعد، دع الذكاء الاصطناعي Copilot في كويز بلس يساعدك في إيجاد الحل.

Introductory Econometrics 4th Edition by Jeffrey Wooldridge

لماذا لم يعجبك هذا التمرين؟

أخرى 8 أحرف كحد أدنى و 255 حرفاً كحد أقصى

حرف 255