Deck 10: Property, Plant, and Equipment: Acquisition and Disposal

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On August 1, 2010, Robbins traded in an old plant asset for a newer model that would be more productive and efficient.Data relative to the old and new plant assets follow:  A total of $10, 500 cash was given in the trade.What should be the cost of the new plant asset for financial accounting purposes?

A total of $10, 500 cash was given in the trade.What should be the cost of the new plant asset for financial accounting purposes?

A)$12, 000

B)$12, 500

C)$13, 500

D)$13, 000

A total of $10, 500 cash was given in the trade.What should be the cost of the new plant asset for financial accounting purposes?A)$12, 000

B)$12, 500

C)$13, 500

D)$13, 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Costs incurred by Mills Company that relate to its property, plant, and equipment assets might be recorded in one of the five following classes of accounts:

a. an expense account

b. an accumulated depreciation accoun

c. a land account

d. a building account

e. an equipment account Required:

For each of the costs identified below, indicate the type of account in which the cost should be recorded by placing the appropriate letter in the space provided.

a. an expense account

b. an accumulated depreciation accoun

c. a land account

d. a building account

e. an equipment account Required:

For each of the costs identified below, indicate the type of account in which the cost should be recorded by placing the appropriate letter in the space provided.

Question

Several expenditures are listed below:

Required:

Required:

If the expenditure would be capitalized to land, buildings, equipment, or other, so indicate with an "X." An example is given.

Required:If the expenditure would be capitalized to land, buildings, equipment, or other, so indicate with an "X." An example is given.

Question

Question

Question

Question

Question

Question

Assuming that the effects of interest capitalization are material, calculate the amount of interest costs to be capitalized by Marcus Corporation in 2010 in relation to the following events:

Question

Question

Question

Question

Question

Question

The Heavy Equipment Company decided to replace a gasoline engine with a diesel engine in one of its cranes.The new engine cost $8, 000, which Heavy paid in cash.The old engine is discarded at no cost to Heavy Equipment.

Required:

Required:

Question

Several expenditures are listed below:

Required:

Required:

Indicate whether or not each expenditure would be included in the cost of property, plant, and equipment.

Required:Indicate whether or not each expenditure would be included in the cost of property, plant, and equipment.

Question

Question

Robertson Company is making significant improvements to some of its assets, as follows.

Required:

Required:

a. Record the appropriate journal entry for replacing the furnace.

b. When rec ording the transaction associated with the van there is a choice between two methods. Provide the journal entries for each method.

Required:a. Record the appropriate journal entry for replacing the furnace.

b. When rec ording the transaction associated with the van there is a choice between two methods. Provide the journal entries for each method.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/87

Play

Full screen (f)

Deck 10: Property, Plant, and Equipment: Acquisition and Disposal

1

Advantages of using historical cost as the basis of valuation of property, plant, and equipment include all of the following except

A)it is a very reliable valuation

B)gains and losses from holding the asset are recognized in the period of value change

C)cost equals the fair market value at the date of acquisition

D)it is consistent with the valuation of other assets, liabilities, and stockholders' equity

A)it is a very reliable valuation

B)gains and losses from holding the asset are recognized in the period of value change

C)cost equals the fair market value at the date of acquisition

D)it is consistent with the valuation of other assets, liabilities, and stockholders' equity

B

2

Alternative terms for property, plant, and equipment include all of the following except

A)plant assets

B)fixed assets

C)long-term assets

D)operational assets

A)plant assets

B)fixed assets

C)long-term assets

D)operational assets

C

3

The president of Reindeer Corporation donated a building to Monday Corporation.The building had an original cost of $500, 000, a book value of $175, 000, and a fair market value of $250, 000.To record this donation, Monday will

A)make a memorandum entry

B)debit Building for $175, 000 and credit Gain for $175, 000

C)debit Building for $250, 000 and credit Gain for $250, 000

D)debit Building for $500, 000 and credit Gain for $500, 000

A)make a memorandum entry

B)debit Building for $175, 000 and credit Gain for $175, 000

C)debit Building for $250, 000 and credit Gain for $250, 000

D)debit Building for $500, 000 and credit Gain for $500, 000

C

4

An asset classified as property, plant, and equipment on the balance sheet must have which one of the following characteristics?

A)an expected life of more than one year

B)used in the normal course of business

C)tangible in nature

D)all of these

A)an expected life of more than one year

B)used in the normal course of business

C)tangible in nature

D)all of these

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

5

All of the following would be classified as property, plant, and equipment except

A)office buildings

B)machinery owned for standby purposes

C)equipment held for resale

D)equipment used in the operation of the business

A)office buildings

B)machinery owned for standby purposes

C)equipment held for resale

D)equipment used in the operation of the business

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

6

Randal's Rifles purchased some equipment by issuing a three-year 6% note for $8, 000 when the market rate for an obligation of this nature was 8%.The interest is payable annually.Actuarial information for three periods follows:

At the date of purchase, what amount should be debited to Equipment?

A)$7, 587.66

B)$6, 716.96

C)$6, 350.66

D)$6, 633.70

At the date of purchase, what amount should be debited to Equipment?

A)$7, 587.66

B)$6, 716.96

C)$6, 350.66

D)$6, 633.70

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

7

All of the following costs associated with acquiring a building should be capitalized except

A)the costs of building permits

B)the cost of a strike associated with the construction of the building

C)the contract price

D)the costs of excavation for the building

A)the costs of building permits

B)the cost of a strike associated with the construction of the building

C)the contract price

D)the costs of excavation for the building

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

8

The Roth Company incurred the following costs in the acquisition of a plant asset: What is the cost of the plant asset?

A)$2, 700

B)$2, 660

C)$2, 550

D)$2, 100

A)$2, 700

B)$2, 660

C)$2, 550

D)$2, 100

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

9

Which one of the following types of assets should not be classified as property, plant, and equipment?

A)leasehold improvements

B)fully-depreciated building (still in use)

C)idle land and buildings

D)long-lived tangible assets

A)leasehold improvements

B)fully-depreciated building (still in use)

C)idle land and buildings

D)long-lived tangible assets

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

10

Remy purchases a new machine by issuing an $18, 000 three-year note.The company will pay off the obligation by paying $6, 000 at the end of each year.The market rate for obligations of this type is 8%.The present value of an annuity at 8% for three periods is 2.577097.The machine will be recorded at a cost of

A)$ 6, 000.00

B)$ 9, 462.58

C)$15, 462.58

D)$18, 000.00

A)$ 6, 000.00

B)$ 9, 462.58

C)$15, 462.58

D)$18, 000.00

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

11

Regal recently purchased a building and the tract of land on which it is located.Regal plans to raze the building immediately and to erect a new building on the site.The value of the original building should be

A)written off as an extraordinary loss in the year the building is razed

B)capitalized as part of the cost of the land

C)depreciated over the period from the date of acquisition to the date that the building is to be razed

D)capitalized as part of the cost of the new building

A)written off as an extraordinary loss in the year the building is razed

B)capitalized as part of the cost of the land

C)depreciated over the period from the date of acquisition to the date that the building is to be razed

D)capitalized as part of the cost of the new building

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

12

During 2011, Ruby Corporation purchased three pieces of equipment at an auction for the lump sum of $200, 000.It cost Ruby $20, 000 to have the equipment delivered and installed.The equipment was appraised at the following values:

Machine 2 should be recorded on Ruby's books at

A)$105, 000

B)$120, 000

C)$ 77, 000

D)$ 70, 000

Machine 2 should be recorded on Ruby's books at

A)$105, 000

B)$120, 000

C)$ 77, 000

D)$ 70, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

13

Richards Corporation purchased some equipment by issuing a $20, 000 non-interest-bearing, four-year note when interest rates were 8%.Actuarial information for 8% and four periods follows:

In the entry to record this purchase, there would be a

A)$20, 000 debit to Equipment

B)$5, 299.40 credit to Discount on Notes Payable

C)$27, 209.78 credit to Notes Payable

D)$14, 700.60 debit to Equipment

In the entry to record this purchase, there would be a

A)$20, 000 debit to Equipment

B)$5, 299.40 credit to Discount on Notes Payable

C)$27, 209.78 credit to Notes Payable

D)$14, 700.60 debit to Equipment

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

14

On February 1, 2010, Rummel Corporation purchased a parcel of land as a factory site for $50, 000.An old building on the property was demolished, and construction began on a new building that was completed on December 12, 2010.Costs incurred during this period are listed below:

(Salvaged materials resulting from demolition were sold for $15, 000.)

Rummel should record the cost of the land and the cost of the new building, respectively, as

A)$48, 000 and $1, 022, 000

B)$50, 000 and $1, 022, 000

C)$63, 000 and $1, 032, 000

D)$63, 000 and $1, 017, 000

(Salvaged materials resulting from demolition were sold for $15, 000.)

Rummel should record the cost of the land and the cost of the new building, respectively, as

A)$48, 000 and $1, 022, 000

B)$50, 000 and $1, 022, 000

C)$63, 000 and $1, 032, 000

D)$63, 000 and $1, 017, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

15

According to GAAP, interest must be capitalized for

A)assets that are ready for use

B)assets constructed for a firm's own use

C)assets that are not being used in the earning activities of the company

D)inventories that are produced in large quantities on a repetitive basis

A)assets that are ready for use

B)assets constructed for a firm's own use

C)assets that are not being used in the earning activities of the company

D)inventories that are produced in large quantities on a repetitive basis

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

16

The debit for a sales tax paid on the purchase of a plant asset would be included in

A)the plant asset account

B)a separate deferred charge account

C)Miscellaneous Tax Expense

D)Accumulated Depreciation-Machinery

A)the plant asset account

B)a separate deferred charge account

C)Miscellaneous Tax Expense

D)Accumulated Depreciation-Machinery

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

17

Which one of the following types of costs should not be included in the cost of a building?

A)costs of remodeling and reconditioning

B)excavation costs

C)unanticipated costs resulting from the condition of the land

D)unanticipated construction costs, such as strike or fire losses

A)costs of remodeling and reconditioning

B)excavation costs

C)unanticipated costs resulting from the condition of the land

D)unanticipated construction costs, such as strike or fire losses

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

18

All of the following major types of assets would be included in the general category of property, plant, and equipment on the balance sheet except

A)wasting assets

B)furniture and fixtures

C)land purchased for future use

D)leasehold improvements

A)wasting assets

B)furniture and fixtures

C)land purchased for future use

D)leasehold improvements

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

19

The Ripple Corporation acquired land, buildings, and equipment from a bankrupt company at a lump-sum price of $500, 000.At the time of acquisition, Ripple paid $20, 000 to have the assets appraised.The appraisal disclosed the following values:

What costs should be assigned to the buildings?

A)$166, 667

B)$173, 333

C)$200, 000

D)$260, 000

What costs should be assigned to the buildings?

A)$166, 667

B)$173, 333

C)$200, 000

D)$260, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

20

Rodriguez Company made the following payments related to a land acquisition: The recorded cost of the land should be

A)$6, 450

B)$6, 585

C)$6, 745

D)$6, 865

A)$6, 450

B)$6, 585

C)$6, 745

D)$6, 865

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

21

Which is the best definition of start-up costs?

A)all activities associated with organizing a new entity

B)organization costs

C)one-time activities for opening a new facility, introducing a new product or service, conducting business in a new territory, conducting business with a new class of customer, initiating a new process in an existing facility, or starting some new operation

D)activities related to routine ongoing efforts to refine or otherwise improve the qualities of an existing product, service, process, or facility

A)all activities associated with organizing a new entity

B)organization costs

C)one-time activities for opening a new facility, introducing a new product or service, conducting business in a new territory, conducting business with a new class of customer, initiating a new process in an existing facility, or starting some new operation

D)activities related to routine ongoing efforts to refine or otherwise improve the qualities of an existing product, service, process, or facility

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

22

On April 1, 2010, Richer Corporation purchased a new machine on a deferred payment basis.A down payment of $5, 000 was made and 10 monthly installments of $14, 000 each are to be made beginning on May 1, 2010.The cash equivalent price of the machine was $130, 000.Richer incurred and paid installation costs amounting to $6, 000.The amount to be capitalized as the cost of the machine is

A)$130, 000

B)$136, 000

C)$140, 000

D)$145, 000

A)$130, 000

B)$136, 000

C)$140, 000

D)$145, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

23

When exchanging nonmonetary assets with another company, the preferred approach is to value the transaction based upon fair value of

A)the asset surrendered or asset received whichever is most evident

B)the asset surrendered unless the fair value of the asset received is easier to determine

C)the asset surrendered except for certain conditions

D)the asset surrendered

A)the asset surrendered or asset received whichever is most evident

B)the asset surrendered unless the fair value of the asset received is easier to determine

C)the asset surrendered except for certain conditions

D)the asset surrendered

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

24

Rupert Company exchanged one business automobile for another business automobile.The old automobile had an original cost of $40, 000, an undepreciated cost of $16, 000, and a market value of $21, 000 when exchanged.In addition, Rupert paid $9, 000 cash for the replacement automobile.The list price of the replacement automobile was $35, 000.The replacement will help generate significantly greater cash flows in the business.At what amount should the replacement automobile be recorded for financial accounting purposes?

A)$24, 000

B)$30, 000

C)$33, 000

D)$35, 000

A)$24, 000

B)$30, 000

C)$33, 000

D)$35, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

25

On May 15, 2010, Retread Company acquired a new forklift in exchange for an old forklift that it had acquired in 2000.The old forklift was purchased for $20, 000 and had a book value of $5, 000.On the date of the exchange, the old forklift had a market value of $6, 000.In addition, Retread paid $18, 000 cash for the new forklift, which had a list price of $25, 000.At what amount should Retread record the new forklift for financial accounting purposes?

A)$23, 000

B)$24, 000

C)$20, 000

D)$25, 000

A)$23, 000

B)$24, 000

C)$20, 000

D)$25, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

26

Early in 2010, Roper, Inc.purchased certain plant assets under a deferred payment contract.The agreement was to pay $50, 000 at year-end for each of the next three years.The plant assets should be valued at

A)present value of a $50, 000 annuity for three years discounted at the bank prime interest rate

B)$150, 000

C)present value of a $50, 000 annuity for three years discounted at the market interest rate

D)$150, 000 plus imputed interest

A)present value of a $50, 000 annuity for three years discounted at the bank prime interest rate

B)$150, 000

C)present value of a $50, 000 annuity for three years discounted at the market interest rate

D)$150, 000 plus imputed interest

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

27

When exchanging nonmonetary assets

A)boot must be associated with the transaction in order to recognize a gain or loss

B)recognized gain or loss can occur depending on the fair value of the asset surrendered and the fair value of the asset received

C)a loss can be recognized only when the fair value of the asset received plus boot is greater than the book value of the asset surrendered

D)recognized gain or loss can occur depending on the book value of the asset surrendered and the fair value of the asset surrendered

A)boot must be associated with the transaction in order to recognize a gain or loss

B)recognized gain or loss can occur depending on the fair value of the asset surrendered and the fair value of the asset received

C)a loss can be recognized only when the fair value of the asset received plus boot is greater than the book value of the asset surrendered

D)recognized gain or loss can occur depending on the book value of the asset surrendered and the fair value of the asset surrendered

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

28

On August 28, 2010, Ruggle Drilling Services purchased a machine with a contract price of $400, 000 and cash terms of 2/10, n/30.The company paid $8, 000 in transportation costs and $8, 000 for installation.Sales taxes of $22, 000 were paid on the invoice amount.The machine should be recorded as a plant asset in the amount of

A)$400, 000

B)$422, 000

C)$428, 000

D)$430, 000

A)$400, 000

B)$422, 000

C)$428, 000

D)$430, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

29

On May 7, 2010, Rabie Corporation purchased for $450, 000 a tract of land on which was located a warehouse and an office building.The following data were collected concerning the property:

What are the appropriate amounts that Rabie should record for the land, warehouse, and office building, respectively?

A)land, $ 70, 000; warehouse, $80, 000; office building, $150, 000

B)land, $100, 000; warehouse, $80, 000; office building, $220, 000

C)land, $100, 000; warehouse, $80, 000; office building, $270, 000

D)land, $112, 500; warehouse, $90, 000; office building, $247, 500

What are the appropriate amounts that Rabie should record for the land, warehouse, and office building, respectively?

A)land, $ 70, 000; warehouse, $80, 000; office building, $150, 000

B)land, $100, 000; warehouse, $80, 000; office building, $220, 000

C)land, $100, 000; warehouse, $80, 000; office building, $270, 000

D)land, $112, 500; warehouse, $90, 000; office building, $247, 500

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

30

Rust, Inc.exchanged a truck that cost $30, 000 (now 50% depreciated)for equipment with an appraised value of $25, 000.Rust paid boot of $6, 000.Rust should record the equipment at

A)$25, 000

B)$30, 000

C)$21, 000

D)$31, 000

A)$25, 000

B)$30, 000

C)$21, 000

D)$31, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

31

Ralley Company exchanged a piece of equipment with a fair market value of $20, 000 and a book value of $25, 000 for a truck with a fair market value of $16, 000 and boot of $4, 000.Ralley Company should record the truck at a cost of

A)$15, 000 and a recognized loss of $5, 000

B)$16, 000 and a recognized loss of $5, 000

C)$20, 000 and a recognized loss of $5, 000

D)$20, 000 and a recognized loss of $1, 000

A)$15, 000 and a recognized loss of $5, 000

B)$16, 000 and a recognized loss of $5, 000

C)$20, 000 and a recognized loss of $5, 000

D)$20, 000 and a recognized loss of $1, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

32

Robards Services exchanged an asset with a cost of $24, 000 (now 40% depreciated)for a nonmonetary asset worth $12, 000.Robards received $2, 000 boot.In the entry to record this exchange, Robards should record

A)a $10, 000 loss

B)a $400 gain

C)no gain or loss

D)a $400 loss

A)a $10, 000 loss

B)a $400 gain

C)no gain or loss

D)a $400 loss

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

33

On January 4, 2010, Rack Company traded in a used bulldozer with a carrying amount of $65, 000 for a new bulldozer having a list price of $120, 000 and paid cash difference of $40, 000 to the dealer.The used bulldozer had a fair value of $75, 000 on the date of exchange.At what amount should the new bulldozer be recorded on Rack's books?

A)$ 40, 000

B)$105, 000

C)$115, 000

D)$120, 000

A)$ 40, 000

B)$105, 000

C)$115, 000

D)$120, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

34

When boot is involved in the exchange of nonmonetary productive assets, normally

A)the entire gain or loss on the exchange should be recognized

B)no gain or loss on the exchange may be recognized

C)no gain is recognized, but a loss may be recognized to the extent that boot is received

D)no gain is recognized, but a loss may be recognized to the extent that boot is given

A)the entire gain or loss on the exchange should be recognized

B)no gain or loss on the exchange may be recognized

C)no gain is recognized, but a loss may be recognized to the extent that boot is received

D)no gain is recognized, but a loss may be recognized to the extent that boot is given

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

35

Performance Stage Company had a professional contract with Actor #1 that was recorded in its accounting records at $300, 000.Johnson Company had a contract with Actor #2 that was recorded in its accounting records at $280, 000.Performance traded Actor #1 to Johnson for Actor #2 by exchanging the actors' contracts.The fair value of each contract was $320, 000.What amount should be shown in the accounting records after the exchange of actor contracts?

A)I

B)II

C)III

D)IV

A)I

B)II

C)III

D)IV

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

36

Richmond, Inc.exchanged a piece of equipment with an original cost of $82, 000, accumulated depreciation to date of $40, 000, and a fair value of $46, 000 for a similar piece of equipment.The newly acquired equipment had a book value of $40, 000 and a fair market value of $46, 000.Richmond should record the equipment acquired at

A)$ 0

B)$40, 000

C)$42, 000

D)$46, 000

A)$ 0

B)$40, 000

C)$42, 000

D)$46, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

37

Renault Marina exchanged a boat with a cost of $80, 000 (now 75% depreciated)for another boat with a current fair value of $27, 000.No boot was paid or received.The new boat will perform the exact same function as the old boat.Renault should record the new boat at

A)$20, 000

B)$27, 000

C)$ 7, 000

D)$ 0

A)$20, 000

B)$27, 000

C)$ 7, 000

D)$ 0

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

38

A plant site donated by a city to Rupp Company, which plans to open a new factory, should be recorded on Rupp's books at

A)the nominal cost of taking title to it

B)its fair market value

C)zero value, but footnoted

D)the value assigned to it by the company's directors

A)the nominal cost of taking title to it

B)its fair market value

C)zero value, but footnoted

D)the value assigned to it by the company's directors

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

39

Property acquired through donation is recorded at

A)its book value

B)its fair market value

C)its cost

D)zero

A)its book value

B)its fair market value

C)its cost

D)zero

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

40

Macey Co.exchanged a piece of equipment that had cost $40, 000 (now 75% depreciated)for a truck with a current appraised value of $13, 000.Macey Co.gave the other company the piece of equipment and $8, 000.Macey Co.should record

A)a $5, 000 loss

B)the truck at $18, 000

C)a gain of $11, 000

D)the truck at $21, 000

A)a $5, 000 loss

B)the truck at $18, 000

C)a gain of $11, 000

D)the truck at $21, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

41

At the end of the year, any balance in Allowance for Repairs should be

A)closed to Repairs Expense

B)reported as a deferred credit

C)closed to Retained Earnings

D)reported as a contra account to the asset

A)closed to Repairs Expense

B)reported as a deferred credit

C)closed to Retained Earnings

D)reported as a contra account to the asset

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following events is most appropriately recorded as a reduction to accumulated depreciation?

A)an addition that increases the anticipated benefits of the old asset

B)an improvement that extends an asset's useful life

C)an improvement that increases the asset's expected benefits beyond that originally expected

D)a replacement of a better asset for the one currently used

A)an addition that increases the anticipated benefits of the old asset

B)an improvement that extends an asset's useful life

C)an improvement that increases the asset's expected benefits beyond that originally expected

D)a replacement of a better asset for the one currently used

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

43

An improvement made to a machine increased its production capacity by 25% without extending the machine's useful life.The cost of the improvement should be

A)recorded as an expense

B)debited to Accumulated Depreciation

C)capitalized in the machine account

D)allocated between Accumulated Depreciation and the machine account

A)recorded as an expense

B)debited to Accumulated Depreciation

C)capitalized in the machine account

D)allocated between Accumulated Depreciation and the machine account

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

44

Exhibit 10-1 Two construction companies, Fargo and Rambam, are in the construction business.Each owns a tract of land being held for development, but each company believes that the other's land is better suited to enhance the success of each planned development.Accordingly, they agree to exchange their land and have the following information:

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.For financial reporting purposes, Fargo should recognize a gain on this exchange in the amount of

A)$ 0

B)$ 50, 000

C)$100, 000

D)$200, 000

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.For financial reporting purposes, Fargo should recognize a gain on this exchange in the amount of

A)$ 0

B)$ 50, 000

C)$100, 000

D)$200, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

45

Rogaine Company exchanged inventory items that cost $47, 000 and normally sold for $65, 000 for a new delivery truck with a list price of $67, 000.The delivery truck should be recorded on Rogaine's books at

A)$47, 000

B)$65, 000

C)$67, 000

D)$82, 000

A)$47, 000

B)$65, 000

C)$67, 000

D)$82, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

46

Rebby Company received $60, 000 in cash and used equipment with a fair value of $140, 000 from Farley Corporation for Rebby's existing equipment, which had a fair value of $200, 000 and an undepreciated cost of $170, 000 recorded on its books.The transaction was undertaken because Rebby was revising its market strategy and planned to reduce the use of this type of equipment in its production.How much gain should Rebby recognize on this exchange, and at what amount should the acquired equipment be recorded, respectively?

A)0 and $150, 000

B)$ 3, 000 and $143, 000

C)$20, 000 and $170, 000

D)$30, 000 and $140, 000

A)0 and $150, 000

B)$ 3, 000 and $143, 000

C)$20, 000 and $170, 000

D)$30, 000 and $140, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

47

On January 1, 2010, Ringo purchased, for $100, 000, equipment having a useful life of eight years and an estimated salvage value of $4, 000.Ringo has recorded monthly depreciation on the equipment using the straight-line method.On March 1, 2015, the equipment was sold for $46, 000.As a result of this sale, Ringo should recognize

A)no gain or loss

B)an $8, 000 gain

C)an $8, 000 loss

D)a $12, 000 gain

A)no gain or loss

B)an $8, 000 gain

C)an $8, 000 loss

D)a $12, 000 gain

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

48

On August 1, 2010, Robbins traded in an old plant asset for a newer model that would be more productive and efficient.Data relative to the old and new plant assets follow: A total of $10, 500 cash was given in the trade.What should be the cost of the new plant asset for financial accounting purposes?

A)$12, 000

B)$12, 500

C)$13, 500

D)$13, 000

A total of $10, 500 cash was given in the trade.What should be the cost of the new plant asset for financial accounting purposes?A)$12, 000

B)$12, 500

C)$13, 500

D)$13, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

49

Which one of the following statements is true?

A)If a plant asset is self-constructed for less than it would cost to purchase, a profit should be recorded upon the completion of the construction.

B)When property, plant, or equipment is acquired through donation, a gain is credited.

C)Development stage enterprises need not report losses before sales are made.

D)Interest cannot be capitalized when an asset is substantially complete and ready for its intended use.

A)If a plant asset is self-constructed for less than it would cost to purchase, a profit should be recorded upon the completion of the construction.

B)When property, plant, or equipment is acquired through donation, a gain is credited.

C)Development stage enterprises need not report losses before sales are made.

D)Interest cannot be capitalized when an asset is substantially complete and ready for its intended use.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following costs incurred subsequent to the acquisition of a machine would be appropriately accounted for by debiting the accumulated depreciation account related to the machine?

A)the cost of cleaning and lubricating the machine

B)the cost of replacing the motor on the machine when the cost of the original motor is not known

C)the cost of moving the machine to another manufacturing plant

D)the cost of a new attachment to the machine that provides for more output per unit of time

A)the cost of cleaning and lubricating the machine

B)the cost of replacing the motor on the machine when the cost of the original motor is not known

C)the cost of moving the machine to another manufacturing plant

D)the cost of a new attachment to the machine that provides for more output per unit of time

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

51

On January 1, 2010, Rong Company signed a contract to have Rozy Associates construct a manufacturing facility at a cost of $14, 000, 000.It was estimated that it would take three years to complete the project.Also on January 1, 2010, to finance the construction cost, Rong borrowed $14, 000, 000 payable in seven annual installments of $2, 000, 000 plus interest at the rate of 9%.During 2010, Rong made progress payments totaling $5, 000, 000 under the contract, and the average amount of accumulated expenditures was $3, 000, 000 for the year.The excess borrowed funds were invested in short-term securities, from which Rong realized investment income of $330, 000.What amount should Rong report as capitalized interest at December 31, 2010?

A)$ 0

B)$ 270, 000

C)$ 510, 000

D)$1, 260, 000

A)$ 0

B)$ 270, 000

C)$ 510, 000

D)$1, 260, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

52

Under GAAP, which one of the following types of costs should not be capitalized?

A)rearrangements

B)routine maintenance

C)replacements

D)additions

A)rearrangements

B)routine maintenance

C)replacements

D)additions

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

53

According to GAAP, interest cost incurred to finance construction of an asset must be capitalized in which of the following situations?

A)when the asset is inventory that is routinely manufactured in large quantities on a repetitive basis

B)when an asset is used in other than the earning activities of the firm

C)when an asset is ready for its intended use

D)when an asset is being constructed for a firm's own use

A)when the asset is inventory that is routinely manufactured in large quantities on a repetitive basis

B)when an asset is used in other than the earning activities of the firm

C)when an asset is ready for its intended use

D)when an asset is being constructed for a firm's own use

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

54

In 2010, Golf Oil Company incurred costs of $7 million drilling oil wells.Thirty percent of the drilling resulted in oil being found.The rest of the drilling was unsuccessful.If Golf uses the successful-efforts method of accounting, the oil and gas properties will be valued on the December 31, 2010 balance sheet at

A)$7, 000, 000

B)$4, 900, 000

C)$4, 200, 000

D)$2, 100, 000

A)$7, 000, 000

B)$4, 900, 000

C)$4, 200, 000

D)$2, 100, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

55

Exhibit 10-1 Two construction companies, Fargo and Rambam, are in the construction business.Each owns a tract of land being held for development, but each company believes that the other's land is better suited to enhance the success of each planned development.Accordingly, they agree to exchange their land and have the following information:

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.After the exchange, Fargo should record its newly acquired land on its books at

A)$300, 000

B)$400, 000

C)$450, 000

D)$500, 000

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.After the exchange, Fargo should record its newly acquired land on its books at

A)$300, 000

B)$400, 000

C)$450, 000

D)$500, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

56

Required disclosure for property, plant, and equipment in the financial statements is based upon

A)age and depreciation method

B)age and nature

C)nature and function

D)function and depreciation method

A)age and depreciation method

B)age and nature

C)nature and function

D)function and depreciation method

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

57

The sale of a depreciable asset resulting in a gain indicates that the proceeds from the sale were

A)less than current market value

B)greater than cost

C)greater than book value

D)less than book value

A)less than current market value

B)greater than cost

C)greater than book value

D)less than book value

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

58

The Rothchild Company purchased a machine on October 1, 2010, for $80, 000.At the time of acquisition, the machine was estimated to have a useful life of five years and an estimated salvage value of $5, 000.Rothchild has recorded monthly depreciation using the straight-line method.On April 1, 2012, the machine was sold for $50, 000.What should be the loss recognized from the sale of the machine?

A)$ 0

B)$2, 500

C)$5, 000

D)$7, 500

A)$ 0

B)$2, 500

C)$5, 000

D)$7, 500

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

59

All of the following are arguments in favor of including only the incremental fixed overhead costs in the cost of a self-constructed asset, except that the

A)cost of the asset is the additional cost incurred to produce it

B)overhead would be incurred whether or not the construction took place

C)asset cost will more closely approximate the cost of a purchased asset

D)decision to construct the asset should be based on the total incremental cost and not include allocated fixed overhead

A)cost of the asset is the additional cost incurred to produce it

B)overhead would be incurred whether or not the construction took place

C)asset cost will more closely approximate the cost of a purchased asset

D)decision to construct the asset should be based on the total incremental cost and not include allocated fixed overhead

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

60

Exhibit 10-1 Two construction companies, Fargo and Rambam, are in the construction business.Each owns a tract of land being held for development, but each company believes that the other's land is better suited to enhance the success of each planned development.Accordingly, they agree to exchange their land and have the following information:

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.For financial reporting purposes, Rambam should recognize a gain on this exchange in the amount of

A)$ 0

B)$ 50, 000

C)$100, 000

D)$200, 000

The exchange of land was made, and based on the difference in appraised fair value, Rambam paid $50, 000 cash to Fargo.

-

Refer to Exhibit 10-1.For financial reporting purposes, Rambam should recognize a gain on this exchange in the amount of

A)$ 0

B)$ 50, 000

C)$100, 000

D)$200, 000

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

61

Ralph Company exchanged a machine for some land.The machine had cost $15, 000, was 70% depreciated, and could be sold for $4, 100.Calvin paid $600 in addition to giving up the machine.

Required:

a. Compute the amount at which the land should be recorded.

b. Assume, instead, that Ralph exchanged the machine for a new, more efficient machine with a fair value of , while still paying as before. Compute the gain or loss that would be recorded on the sale of the old machine by Ralph

Required:

a. Compute the amount at which the land should be recorded.

b. Assume, instead, that Ralph exchanged the machine for a new, more efficient machine with a fair value of , while still paying as before. Compute the gain or loss that would be recorded on the sale of the old machine by Ralph

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

62

Two alternative methods of accounting for the cost of oil and gas properties have been widely used.The method that capitalizes all costs associated with all wells is the

A)successful-efforts method

B)full-cost method

C)variable-cost method

D)specific-cost method

A)successful-efforts method

B)full-cost method

C)variable-cost method

D)specific-cost method

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

63

A major difference between IFRS and GAAP regarding valuation of property, plant, and equipment is that

A)IFRS allow valuation increases to be recorded in certain circumstances, but GAAP does not permit increases

B)IFRS and GAAP differ greatly on accounting for nonmonetary exchanges

C)IFRS require capitalization of all repairs and maintenance while GAAP does not

D)IFRS allocate lump-sum purchase costs based on relative book values rather than relative market values

A)IFRS allow valuation increases to be recorded in certain circumstances, but GAAP does not permit increases

B)IFRS and GAAP differ greatly on accounting for nonmonetary exchanges

C)IFRS require capitalization of all repairs and maintenance while GAAP does not

D)IFRS allocate lump-sum purchase costs based on relative book values rather than relative market values

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

64

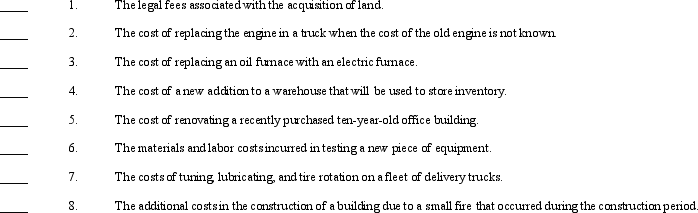

Costs incurred by Mills Company that relate to its property, plant, and equipment assets might be recorded in one of the five following classes of accounts:

a. an expense account

b. an accumulated depreciation accoun

c. a land account

d. a building account

e. an equipment account Required:

For each of the costs identified below, indicate the type of account in which the cost should be recorded by placing the appropriate letter in the space provided.

a. an expense account

b. an accumulated depreciation accoun

c. a land account

d. a building account

e. an equipment account Required:

For each of the costs identified below, indicate the type of account in which the cost should be recorded by placing the appropriate letter in the space provided.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

65

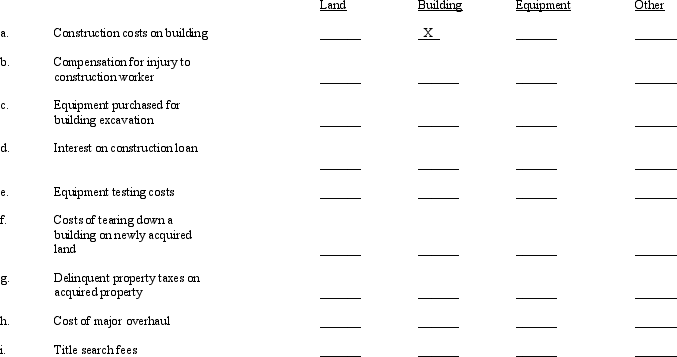

Several expenditures are listed below:

Required:

If the expenditure would be capitalized to land, buildings, equipment, or other, so indicate with an "X." An example is given.

Required:If the expenditure would be capitalized to land, buildings, equipment, or other, so indicate with an "X." An example is given.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

66

Mirror Corp.has agreed to expand its operations by opening a manufacturing plant in Burns, Texas.In return, Burns will donate an abandoned building and the 5 acres on which it sits to Mirror.The land originally cost $1, 000, 000 and the building $3, 000, 000.The building's current book value is $380, 000, and current appraisals are: land $6, 000, 000 and building $2, 600, 000.Mirror has also agreed to provide 100 jobs for the next 5 years to Burns' city residents.Mirror estimates that the wages to these residents will amount to $4, 000, 000.

Required:

Prepare the journal entry to record this acquisition on Mirror's books.

Required:

Prepare the journal entry to record this acquisition on Mirror's books.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

67

During 2010, Redford Company acquired a new piece of equipment for its manufacturing process.In order to purchase the equipment, Redford made a down payment of $50, 000 and issued a $200, 000 five-year, 7% note.The annual payment of principal and interest was to be $48, 778.The market rate of interest for obligations of this kind is 12%.The present value factor for an ordinary annuity of 5 years at 12% is 3.604776.

Required:

a. Prepare the journal entry to record the acquisition

b. Assume that the equipment had an est ablished cash price of . Prepare the jounal entry to record the transaction under this additional assumption

Required:

a. Prepare the journal entry to record the acquisition

b. Assume that the equipment had an est ablished cash price of . Prepare the jounal entry to record the transaction under this additional assumption

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

68

The costs of drilling an unsuccessful well are expensed under

A)the successful-efforts method

B)the full-cost method

C)both the successful-efforts method and the full-cost method

D)neither the successful-efforts method nor the full-cost method

A)the successful-efforts method

B)the full-cost method

C)both the successful-efforts method and the full-cost method

D)neither the successful-efforts method nor the full-cost method

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

69

Under IFRS, which of the following must be expensed?

A)maintenance only

B)repairs only

C)rearrangements only

D)maintenance, repairs, and rearrangements

A)maintenance only

B)repairs only

C)rearrangements only

D)maintenance, repairs, and rearrangements

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

70

Smith Delivery Services bought a truck by paying $44, 000 cash down and signing a $148, 000 non-interest-bearing note due in five years for the balance.Current interest rates were 8%.Actuarial information for five periods at 8% follows:

Required:

Compute the amount that should be charged to the asset account.

Required:

Compute the amount that should be charged to the asset account.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

71

Assuming that the effects of interest capitalization are material, calculate the amount of interest costs to be capitalized by Marcus Corporation in 2010 in relation to the following events:

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

72

On January 3, 2010, Mercury Company began self-constructing an asset that qualified for interest capitalization.On January 5, Mercury borrowed $300, 000 on an 8% construction loan.In addition, Mercury had $400, 000 of 6% notes payable and $700, 000 of 9% bonds payable outstanding.By December 31, expenditures (occurring evenly throughout the year)of $800, 000 had been made on the asset.Investment of unused funds during the year yielded $1, 200 of interest revenue.

Required:

Compute the amount of interest that should be capitalized during 2010.

Required:

Compute the amount of interest that should be capitalized during 2010.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

73

Concerning current accounting for oil and gas properties, which statement is true?

A)The successful-efforts method must be used.

B)The reserve-recognition method must be used.

C)Either the successful-efforts method or the full-cost method may be used.

D)The full-cost method must be used.

A)The successful-efforts method must be used.

B)The reserve-recognition method must be used.

C)Either the successful-efforts method or the full-cost method may be used.

D)The full-cost method must be used.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

74

When an operating asset is made up of significant individual components, IFRS require the company to

A)group those components into no more than three groups for depreciation

B)combine the components into one unit and use a weighted average useful life

C)ignore the components for accounting purposes

D)account for each component individually

A)group those components into no more than three groups for depreciation

B)combine the components into one unit and use a weighted average useful life

C)ignore the components for accounting purposes

D)account for each component individually

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

75

Mark Company exchanged a worn-out tractor that had cost $20, 000 and was half depreciated for a new tractor with a fair value of $12, 000.Mark paid an additional $2, 500 cash.The transaction lacked commercial substance.

Required:

Compute the amount at which Mark should record the new tractor.

Required:

Compute the amount at which Mark should record the new tractor.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

76

Cooper, Inc.is constructing a building that qualifies for interest capitalization.The following information is available:

Capitalization period: January 1, 2010-December 31, 2011 Expenditures on project (incurred evenly):

Amounts borrowed and outstanding (all debt incurred January 1, 2010):

Required:

a. Compute the amount of interest that should be capitalized in 2010 and 2011 . (Round interest rates to the ne arest hundredths e.g., .)

b. Assume that in 2010 umused borowed funds were invested and eaned interest revemue amounting to . How much interest should be capitalized to the asset account in 2011 ?

Capitalization period: January 1, 2010-December 31, 2011 Expenditures on project (incurred evenly):

Amounts borrowed and outstanding (all debt incurred January 1, 2010):

Required:

a. Compute the amount of interest that should be capitalized in 2010 and 2011 . (Round interest rates to the ne arest hundredths e.g., .)

b. Assume that in 2010 umused borowed funds were invested and eaned interest revemue amounting to . How much interest should be capitalized to the asset account in 2011 ?

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

77

The Heavy Equipment Company decided to replace a gasoline engine with a diesel engine in one of its cranes.The new engine cost $8, 000, which Heavy paid in cash.The old engine is discarded at no cost to Heavy Equipment.

Required:

Required:

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

78

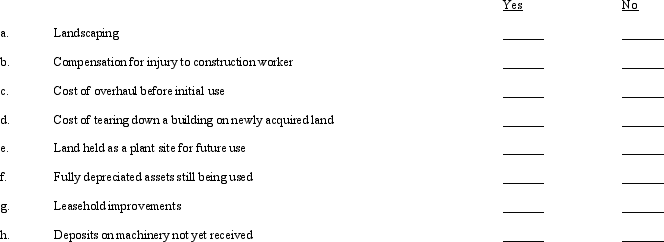

Several expenditures are listed below:

Required:

Indicate whether or not each expenditure would be included in the cost of property, plant, and equipment.

Required:Indicate whether or not each expenditure would be included in the cost of property, plant, and equipment.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

79

On August 1, Silver Company exchanged a machine for a similar machine owned by Wrangler Company and also received $7, 000 cash from Wrangler Company.Silver's machine had an original cost of $70, 000, accumulated depreciation to date of $34, 500, and a fair market value of $60, 000.Wrangler's machine had a book value of $45, 000 and a fair value of $53, 000.

Required:

Prepare the necessary journal entry by Silver Company to record this transaction assuming

a. Siver will use the newly acquired machine in the same manner as the old one.

b. Silver's use of the new machine will be substantially different from the old one.

Required:

Prepare the necessary journal entry by Silver Company to record this transaction assuming

a. Siver will use the newly acquired machine in the same manner as the old one.

b. Silver's use of the new machine will be substantially different from the old one.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

80

Robertson Company is making significant improvements to some of its assets, as follows.

Required:

a. Record the appropriate journal entry for replacing the furnace.

b. When rec ording the transaction associated with the van there is a choice between two methods. Provide the journal entries for each method.

Required:a. Record the appropriate journal entry for replacing the furnace.

b. When rec ording the transaction associated with the van there is a choice between two methods. Provide the journal entries for each method.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 87 flashcards in this deck.