Deck 11: Corporate Liquidating Distributions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Ball Corporation owns 80% of Net Corporation's stock and Jack owns the remaining 20% of Net Corporation's stock.Ball's basis in the Net stock is $200,000 and Jack's basis in the Net stock is $100,000.Under a plan of complete liquidation,Ball Corporation receives property with an adjusted basis of $400,000 and an FMV of $800,000 and Jack receives property with an adjusted basis of $50,000 and an FMV of $200,000.Ball and Jack's recognized gains on the liquidation are:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Dusty Corporation owns 90% of Palace Corporation's stock and Susan owns the remaining stock.Dusty Corporation's stock basis is $300,000 and Susan's stock basis is $20,000.Under a plan of complete liquidation,Dusty Corporation receives property with a $400,000 adjusted basis and a $540,000 FMV and Susan receives property with a $20,000 adjusted basis and a $60,000 FMV.The bases of the properties are:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Ball Corporation owns 80% of Net Corporation's stock and Jack owns the remaining 20% of Net Corporation's stock.Ball's basis in the Net stock is $200,000 and Jack's basis in the Net stock is $100,000.Under a plan of complete liquidation,Ball Corporation receives property with an adjusted basis of $400,000 and an FMV of $800,000 and Jack receives property with an adjusted basis of $50,000 and an FMV of $200,000.Ball and Jack's bases in the property received are:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Cowboy Corporation owns 90% of the single class of stock in Doggie Corporation.The other 10% is owned by Miguel,an individual.Cowboy's basis in its Doggie Corporation stock is $100,000 and Miguel's basis is $50,000.Doggie Corporation distributes property having an adjusted basis of $150,000 and an FMV of $500,000 to Cowboy Corporation,and $60,000 of money to Miguel as a liquidating distribution.Doggie and Cowboy Corporations must recognize gain of:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Prime Corporation liquidates its 85%-owned subsidiary Bass Corporation under the provisions of Secs.332 and 337.Bass Corporation distributes land to its minority shareholder,John,who owns a 15% interest.The property received by John has a $55,000 FMV.The land was used in the Bass Corporation's business and has a $65,000 adjusted basis and is subject to a $10,000 liability,which is assumed by John.John's basis in his stock is $25,000.What gain or loss will John and Bass Corporation recognize on the distribution of the land?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

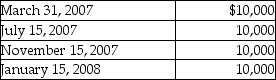

Sandy,a cash method of accounting taxpayer,has a basis of $46,000 in her 500 shares of Newt Corporation stock.She receives the following distributions as part of Newt's plan of liquidation.  The amount of the final distribution is not known on December 31,2007.What are the tax consequences of the distributions?

The amount of the final distribution is not known on December 31,2007.What are the tax consequences of the distributions?

A)Sandy will recognize a loss of $4,500 in 2007 and a $1,500 loss in 2008.

B)Sandy will recognize the entire loss in 2007.

C)Sandy will recognize the entire loss in 2008.

D)None of the above is correct.

The amount of the final distribution is not known on December 31,2007.What are the tax consequences of the distributions?A)Sandy will recognize a loss of $4,500 in 2007 and a $1,500 loss in 2008.

B)Sandy will recognize the entire loss in 2007.

C)Sandy will recognize the entire loss in 2008.

D)None of the above is correct.

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/102

Play

Full screen (f)

Deck 11: Corporate Liquidating Distributions

1

Riverwalk Corporation is liquidated,with Juan receiving $5,000 in money and other property having a $6,000 FMV.Juan's basis in his Riverwalk stock is $8,000.Upon liquidation,Juan must recognize a gain of

A)0)

B)$2,000.

C)$3,000.

D)$11,000.

A)0)

B)$2,000.

C)$3,000.

D)$11,000.

C

2

Identify which of the following statements is false.

A)The tax attributes of the liquidating corporation carry over to the shareholders when the liquidation is conducted under the general liquidation rules.

B)Baker Corporation was formed in a Sec.351 exchange three years ago by Emil,Fred,and George who own equal stock interests.The corporation can be liquidated tax-free under the special liquidation rules of Secs.332 and 337.

C)The terms "liquidation" and "dissolution" are synonymous.

D)All of the above are false.

A)The tax attributes of the liquidating corporation carry over to the shareholders when the liquidation is conducted under the general liquidation rules.

B)Baker Corporation was formed in a Sec.351 exchange three years ago by Emil,Fred,and George who own equal stock interests.The corporation can be liquidated tax-free under the special liquidation rules of Secs.332 and 337.

C)The terms "liquidation" and "dissolution" are synonymous.

D)All of the above are false.

D

3

Bluebird Corporation owns and operates busses and has decided to liquidate its operations.Victor,who owns 80% of the company's stock,will receive all of the busses,repair parts inventory,and all tools and equipment.He plans to start a bus company in another town.Penny,who owns 20% of the stock,wants nothing to do with the new bus business and will receive a cash distribution.Bluebird will incur about $20,000 of expenses in connection with the liquidation.What tax issues should Victor,Penny,and Bluebird consider with respect to the liquidation?

Penny and Victor should consider the following tax issues:

• What gains or losses does Bluebird recognize on the two distributions?

• Does Bluebird have to file a corporate tax return for the portion of the final tax year that it is in existence? If so,what income and expenses are included in the return?

• Can Bluebird deduct the liquidation expenses on its final tax return?

• What are the amounts and characters of the gain or loss that Penny and Victor recognize upon surrendering their Bluebird stock?

• What basis does Victor take for the noncash assets that he receives?

• What happens to Bluebird's tax attributes? Bluebird Corporation will need to recognize any gain realized on the distribution of the Bluebird busses,support vehicles,repair parts inventory,tools,and equipment.Bluebird recognizes no loss on the disposition of these items because they are distributed to a related party (Victor owns 80% of Bluebird).Penny recognizes no gain on the distribution because she receives only cash.Victor and Penny will need to determine their realized and recognized gains on the liquidation.Bluebird Corporation can deduct the liquidation expenses in its final tax return.Any NOLs incurred in the final year can be carried back to the two preceding tax years.A substantial cost may be incurred in liquidating the corporation.Perhaps Victor should consider buying Penny's stock and keep operating Bluebird Corporation in the new city.This way the liquidation tax (e.g.,on corporate and shareholder-level gains)will be avoided.

• What gains or losses does Bluebird recognize on the two distributions?

• Does Bluebird have to file a corporate tax return for the portion of the final tax year that it is in existence? If so,what income and expenses are included in the return?

• Can Bluebird deduct the liquidation expenses on its final tax return?

• What are the amounts and characters of the gain or loss that Penny and Victor recognize upon surrendering their Bluebird stock?

• What basis does Victor take for the noncash assets that he receives?

• What happens to Bluebird's tax attributes? Bluebird Corporation will need to recognize any gain realized on the distribution of the Bluebird busses,support vehicles,repair parts inventory,tools,and equipment.Bluebird recognizes no loss on the disposition of these items because they are distributed to a related party (Victor owns 80% of Bluebird).Penny recognizes no gain on the distribution because she receives only cash.Victor and Penny will need to determine their realized and recognized gains on the liquidation.Bluebird Corporation can deduct the liquidation expenses in its final tax return.Any NOLs incurred in the final year can be carried back to the two preceding tax years.A substantial cost may be incurred in liquidating the corporation.Perhaps Victor should consider buying Penny's stock and keep operating Bluebird Corporation in the new city.This way the liquidation tax (e.g.,on corporate and shareholder-level gains)will be avoided.

4

Robot Corporation is liquidated,with Marty receiving property having an adjusted basis of $60,000 and an FMV of $90,000.The property is subject to a $80,000 mortgage,which Marty assumes.Marty's basis in the Robot stock surrendered is $50,000.Marty must recognize

A)a $40,000 loss.

B)no gain or loss.

C)a $60,000 gain.

D)none of the above

A)a $40,000 loss.

B)no gain or loss.

C)a $60,000 gain.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

5

The adjusted basis of property received in a complete liquidation is its fair market value on the distribution date.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

6

Are liquidation and dissolution the same? Explain your answer.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

7

In general,a noncorporate shareholder that receives a distribution in complete liquidation of the liquidating corporation recognizes his or her entire realized gain as a capital gain.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

8

Liquidation rules generally are applied the same to the following organizations except for

A)subsidiary corporations (80% controlled).

B)C corporations.

C)S corporations.

D)subsidiary corporations (less than 80% controlled).

A)subsidiary corporations (80% controlled).

B)C corporations.

C)S corporations.

D)subsidiary corporations (less than 80% controlled).

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

9

In a complete liquidation of a corporation,which of the following is false?

A)All stock of the liquidating corporation is canceled or redeemed.

B)The corporation ceases to be a going concern.

C)The corporation divests itself of substantially all its properties.

D)The liquidation of a corporation means it has undergone dissolution.

A)All stock of the liquidating corporation is canceled or redeemed.

B)The corporation ceases to be a going concern.

C)The corporation divests itself of substantially all its properties.

D)The liquidation of a corporation means it has undergone dissolution.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

10

Generally,a corporation recognizes a gain,but not a loss,on a liquidating distribution.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

11

Riverwalk Corporation is liquidated,with Juan receiving $5,000 in money,other property having a $6,000 FMV,and a $1,000 mortgage on the property.Juan's basis in his River walk stock is $8,000.Upon liquidation,Juan must recognize a gain of

A)0)

B)$2,000.

C)$3,000.

D)$11,000.

A)0)

B)$2,000.

C)$3,000.

D)$11,000.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

12

Texas Corporation is undergoing a complete liquidation and distributes land to Robert,one of its shareholders,in exchange for all of Robert's stock.The land has a basis of $300,000 and an FMV of $400,000 on Texas Corporation's books and is subject to a $325,000 liability.Robert assumes the liability on the property.Robert's basis in his Texas Corporation stock is $100,000.What is the amount of gain or loss recognized by Robert on the distribution?

A)$175,000 gain

B)$25,000 gain

C)$25,000 loss

D)No gain or loss is recognized.

A)$175,000 gain

B)$25,000 gain

C)$25,000 loss

D)No gain or loss is recognized.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

13

When a corporation liquidates,it performs three activities.What is the general order of these activities in a plan of liquidation?

A)pay debts,distribute property to shareholders,and wind up its affairs

B)wind up its affairs,distribute property to shareholders,pay debts

C)pay debts,wind up its affairs,and distribute property to shareholders

D)wind up its affairs,pay debts,and distribute property to shareholders

A)pay debts,distribute property to shareholders,and wind up its affairs

B)wind up its affairs,distribute property to shareholders,pay debts

C)pay debts,wind up its affairs,and distribute property to shareholders

D)wind up its affairs,pay debts,and distribute property to shareholders

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

14

Section 336 prevents recognition of a loss when making a pro rata distribution of property to a related person.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

15

Liquidation and dissolution have the same legal meaning.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

16

Moya Corporation adopted a plan of liquidation last year.All but a nominal amount of Moya's assets are distributed to its shareholders within the year.Which of the following statements is not true?

A)The liquidation of Moya Corporation means the corporation has undergone dissolution.

B)Moya Corporation retains its state charter.

C)Moya Corporation's existence is preserved.

D)Moya Corporation has been liquidated for tax purposes.

A)The liquidation of Moya Corporation means the corporation has undergone dissolution.

B)Moya Corporation retains its state charter.

C)Moya Corporation's existence is preserved.

D)Moya Corporation has been liquidated for tax purposes.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

17

Identify which of the following statements is true.

A)The method of accounting used by shareholders involved in a complete liquidation is relevant when determining the year in which the shareholder's gain or loss should be reported.

B)An accrual method of accounting taxpayer recognizes his/her realized gain on a corporate liquidation when there has been actual or constructive receipt of the liquidating distribution(s).

C)If a shareholder assumes or acquires liabilities of the liquidating corporation,the amount of these liabilities does not reduce the amount realized by the shareholder.

D)All of the above are false.

A)The method of accounting used by shareholders involved in a complete liquidation is relevant when determining the year in which the shareholder's gain or loss should be reported.

B)An accrual method of accounting taxpayer recognizes his/her realized gain on a corporate liquidation when there has been actual or constructive receipt of the liquidating distribution(s).

C)If a shareholder assumes or acquires liabilities of the liquidating corporation,the amount of these liabilities does not reduce the amount realized by the shareholder.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

18

Property received in a corporate liquidation by a noncorporate shareholder has

A)a basis equal to its basis on the liquidating corporation's books increased by any gain recognized by the shareholder upon receipt of the property.Its holding period includes the holding period of the shareholder's stock.

B)a basis equal to its basis on the liquidating corporation's books increased by any gain recognized by the shareholder upon receipt of the property.Its holding period commences on the day after the distribution date.

C)a basis equal to its FMV reduced by any liabilities assumed by the shareholder.Its holding period commences on the day after the distribution date.

D)a basis equal to its FMV.Its holding period commences on the day after the distribution date.

A)a basis equal to its basis on the liquidating corporation's books increased by any gain recognized by the shareholder upon receipt of the property.Its holding period includes the holding period of the shareholder's stock.

B)a basis equal to its basis on the liquidating corporation's books increased by any gain recognized by the shareholder upon receipt of the property.Its holding period commences on the day after the distribution date.

C)a basis equal to its FMV reduced by any liabilities assumed by the shareholder.Its holding period commences on the day after the distribution date.

D)a basis equal to its FMV.Its holding period commences on the day after the distribution date.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

19

In a complete liquidation,a liability assumed by a shareholder reduces the shareholder's amount realized.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

20

Identify which of the following statements is true.

A)In general,a noncorporate shareholder that receives a distribution in complete liquidation of the liquidating corporation recognizes his or her entire realized gain as a capital gain.

B)The basis for nonmoney property received by a noncorporate shareholder as part of a liquidating distribution is the same as its basis on the books of the liquidating corporation.

C)The liquidating corporation does not recognize gains and losses when making a distribution of nonmoney property.

D)All of the above are false.

A)In general,a noncorporate shareholder that receives a distribution in complete liquidation of the liquidating corporation recognizes his or her entire realized gain as a capital gain.

B)The basis for nonmoney property received by a noncorporate shareholder as part of a liquidating distribution is the same as its basis on the books of the liquidating corporation.

C)The liquidating corporation does not recognize gains and losses when making a distribution of nonmoney property.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

21

Identify which of the following statements is true.

A)With limited exceptions,a loss can be recognized by a liquidating corporation when it makes a liquidating distribution of property that has declined in value.

B)When computing the corporate-level gain on a liquidating distribution,the FMV of the property cannot exceed the liability assumed or acquired by the shareholder.

C)The FMV of property distributed by a liquidating corporation can be less than the amount of the liability assumed or acquired by the shareholder.

D)All of the above are false.

A)With limited exceptions,a loss can be recognized by a liquidating corporation when it makes a liquidating distribution of property that has declined in value.

B)When computing the corporate-level gain on a liquidating distribution,the FMV of the property cannot exceed the liability assumed or acquired by the shareholder.

C)The FMV of property distributed by a liquidating corporation can be less than the amount of the liability assumed or acquired by the shareholder.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

22

Barnett Corporation owns an office building that cost $900,000.Barnett has taken $600,000 of depreciation on the building.The property is subject to a $600,000 mortgage.The office building has a current FMV of $400,000.Barnett Corporation is liquidated and the office building is distributed to a single individual shareholder who assumes the mortgage.Barnett Corporation must recognize

A)no gain or loss.

B)a $100,000 gain.

C)a $300,000 gain.

D)none of the above

A)no gain or loss.

B)a $100,000 gain.

C)a $300,000 gain.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

23

John and June,husband and wife,have owned Ruby Corporation for a number of years.Their basis in the Ruby stock,which they own jointly,is $200,000.The Ruby stock is Sec.1244 stock.Ruby Corporation liquidates,and John and June receive the following from the corporation: accounts receivable,$30,000 FMV; a car,$21,000 FMV; office furniture,$11,000 FMV; and $25,000 in cash.What is the amount and character of their gain or loss?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

24

Dexer Corporation is owned 70% by Amy and 30% by Brad.Dexer Corporation owns Eagle Corporation stock with a $50,000 adjusted basis and a $30,000 FMV.The stock is not disqualified property.As part of a complete liquidation,the Eagle Corporation stock is distributed to Amy.Amy's basis in her Dexer stock is $40,000.Dexer Corporation will recognize

A)no loss.

B)a $10,000 loss.

C)a $20,000 loss.

D)none of the above

A)no loss.

B)a $10,000 loss.

C)a $20,000 loss.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

25

Identify which of the following statements is true.

A)The loss realized on the sale of a property is disallowed when such property was received by a corporation as a contribution of capital in a transaction having as its principal purpose the recognition of loss pursuant to the corporation's subsequent liquidation later in the same taxable year.

B)Losses claimed in a tax return filed before the adoption of the plan of liquidation are not restricted by Sec.336(d)(2).

C)Properties acquired by a liquidating corporation as a capital contribution occurring within three years of the adoption of a plan of liquidation are generally presumed to have a tax avoidance motive.

D)All of the above are false.

A)The loss realized on the sale of a property is disallowed when such property was received by a corporation as a contribution of capital in a transaction having as its principal purpose the recognition of loss pursuant to the corporation's subsequent liquidation later in the same taxable year.

B)Losses claimed in a tax return filed before the adoption of the plan of liquidation are not restricted by Sec.336(d)(2).

C)Properties acquired by a liquidating corporation as a capital contribution occurring within three years of the adoption of a plan of liquidation are generally presumed to have a tax avoidance motive.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

26

Specialty Corporation distributes land to one of its shareholders,Sam,as part of a plan of liquidation.The land,which was used in Specialty's business,has an adjusted basis of $50,000 and an FMV of $130,000 on the date of distribution.Sam's basis in Specialty Corporation stock is $100,000.What is the amount and character of the gain/loss recognized by Specialty Corporation? What is the amount and character of the gain/loss recognized by Sam?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

27

Under a plan of complete liquidation,Coast Corporation distributes land with a $300,000 adjusted basis and a $400,000 FMV to William,a 25% shareholder.William has a $200,000 basis in his Coast stock.The land is inventory in the hands of Coast Corporation.Coast Corporation must recognize

A)no gain.

B)$100,000 of ordinary income.

C)$100,000 of long-term capital gain.

D)$200,000 of ordinary income.

A)no gain.

B)$100,000 of ordinary income.

C)$100,000 of long-term capital gain.

D)$200,000 of ordinary income.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

28

How is the gain/loss calculated if a shareholder has acquired stock at different times and at varying prices?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

29

Identify which of the following statements is true.

A)A liquidating distribution of property other than a disqualified property that is made ratably to all shareholders (based on their stockholdings)will permit the recognition of loss on the portion of the distribution that is made to a related person.

B)A subsidiary corporation can recognize losses on distributions to either the parent corporation or minority shareholders in a Sec.332 liquidation.

C)Section 336 prevents recognition of a loss when making a pro rata distribution of property to a related person.

D)All of the above are false.

A)A liquidating distribution of property other than a disqualified property that is made ratably to all shareholders (based on their stockholdings)will permit the recognition of loss on the portion of the distribution that is made to a related person.

B)A subsidiary corporation can recognize losses on distributions to either the parent corporation or minority shareholders in a Sec.332 liquidation.

C)Section 336 prevents recognition of a loss when making a pro rata distribution of property to a related person.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

30

Albert receives a liquidating distribution from Glidden Corporation as part of a complete redemption of its stock.Albert receives cash of $5,000 and other property with an adjusted basis of $6,000 and an FMV of $10,000.Albert's basis in the Glidden stock surrendered is $8,000.How much gain does he recognize?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

31

Toby made a capital contribution of a pretzel maker having a $2,000 adjusted basis and a $200 FMV to Keke Corporation in exchange for additional stock last year.Later that same year,Keke sold the pretzel maker for $300.This year,Keke adopted a plan of liquidation.Previously,Keke had never used the pretzel maker in connection with the conduct of its trade or business.The sale was reported on Keke's current tax return.What reporting option does Keke Corporation not have because of its plan of liquidation?

A)File an amended tax return for the tax year in which the tax loss was originally claimed.

B)Recapture the loss on the tax return for the year the plan for liquidation was adopted.

C)Recognize a gain of $100 for the current year.

D)none of the above

A)File an amended tax return for the tax year in which the tax loss was originally claimed.

B)Recapture the loss on the tax return for the year the plan for liquidation was adopted.

C)Recognize a gain of $100 for the current year.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

32

Under the general liquidation rules,Missouri Corporation is liquidated,with Jefferson receiving $5,000 in cash plus other property having a $6,000 FMV and assuming a $2,000 mortgage on the property.Jefferson's basis in his Missouri stock is $8,000.What is Jefferson's amount realized and gain or loss recognized on the liquidation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

33

Charlene and Dennis each own 50% of Brewster Corporation and have owned it for five years.The adjusted bases of their Brewster stock are $80,000 and $40,000 respectively.Brewster Corporation liquidates and distributes $60,000 to Charlene in exchange for her stock.It distributes a parcel of land with a $140,000 FMV which is subject to a $90,000 mortgage to Dennis in exchange for his stock.Dennis assumes the mortgage and also receives $10,000 in cash.

a)What is the character and amount of each shareholder's gain or loss?

b)What is each shareholder's basis in the property received in the liquidation?

a)What is the character and amount of each shareholder's gain or loss?

b)What is each shareholder's basis in the property received in the liquidation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

34

The stock of Cooper Corporation is 70% owned by Carole and 30% owned by Carole's brother,Chris.During 2013,Chris transferred property (basis of $100,000 and FMV of $120,000)as a contribution to the capital of Cooper.During February 2014,Cooper adopted a plan of liquidation and subsequently made a pro rata distribution of the property back to Carole and Chris.At the time of the liquidation,the property had an FMV of $80,000.What amount of loss can be recognized by Cooper on the distribution of property?

A)$0

B)$6,000

C)$12,000

D)$20,000

A)$0

B)$6,000

C)$12,000

D)$20,000

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

35

Last year,Toby made a capital contribution of a pretzel maker having a $2,000 adjusted basis and a $200 FMV to Keke Corporation in exchange for additional stock.This year,Keke Corporation adopted a plan of liquidation.Prior to the adoption of the liquidation plan,Keke had not used the pretzel maker in connection with the conduct of its trade or business.Which of the following statements is true?

A)Keke Corporation may recognize a loss of $1,800.

B)Keke Corporation may recognize a loss of $200.

C)Keke Corporation's basis for determining the loss will be $2,000.

D)Keke Corporation's basis for determining the loss will be $200.

A)Keke Corporation may recognize a loss of $1,800.

B)Keke Corporation may recognize a loss of $200.

C)Keke Corporation's basis for determining the loss will be $2,000.

D)Keke Corporation's basis for determining the loss will be $200.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

36

Under the general liquidation rules,Kansas Corporation is liquidated,with Sam Topeka receiving $20,000 in cash plus other property having a $24,000 FMV.Sam Topeka's basis in his Kansas stock is $32,000.What is Sam Topeka's amount realized and gain recognized on the liquidation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

37

Lake Corporation distributes a building used in its business to Sandy in exchange for all of her Lake stock.Sandy's basis in her stock is $30,000 and the property she receives has a $90,000 FMV.As part of the distribution,Sandy assumes a liability associated with the property of $65,000.The property's basis prior to the liquidating distribution was $25,000.What are the tax consequences of the distribution to Sandy? To Lake Corporation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

38

Identify which of the following statements is true.

A)A loss recognized by a shareholder upon complete liquidation of a corporation may not qualify for ordinary loss treatment if the stock is Sec.1244 stock.

B)The loss that is recognized by an individual shareholder on the liquidation of a corporation is a capital loss,up to certain limits,if the stock is Sec.1244 stock.

C)The loss recognized by a corporate shareholder on the worthlessness of the controlled subsidiary's stock is an ordinary loss.

D)All of the above are false.

A)A loss recognized by a shareholder upon complete liquidation of a corporation may not qualify for ordinary loss treatment if the stock is Sec.1244 stock.

B)The loss that is recognized by an individual shareholder on the liquidation of a corporation is a capital loss,up to certain limits,if the stock is Sec.1244 stock.

C)The loss recognized by a corporate shareholder on the worthlessness of the controlled subsidiary's stock is an ordinary loss.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

39

Jack Corporation is owned 75% by Sherri and 25% by Mark.Sherri and Mark have $125,000 and $50,000 bases in their stock,respectively.Jack Corporation adopts a plan of liquidation on March 1.On April 12,Sherri receives the following property as a liquidating distribution: cash of $30,000; land,$125,000 FMV; and 150 shares of Green Corporation stock,$30,000 FMV.The land is subject to a $20,000 mortgage.On the same date,Mark receives $10,000 FMV of Green stock (50 shares)and cash of $45,000 as a liquidating distribution.The land has a basis of $50,000 and the stock has a basis of $70,000 in Jack Corporation's hands.Both are capital assets to Jack Corporation and have been held for a number of years.

a)What is the amount and character of Jack Corporation's recognized gain or loss on the liquidating distributions?

b)What are the amounts and characters of Sherri and Mark's recognized gains or losses?

c)What are the bases of the land and stock to Sherri and Mark?

a)What is the amount and character of Jack Corporation's recognized gain or loss on the liquidating distributions?

b)What are the amounts and characters of Sherri and Mark's recognized gains or losses?

c)What are the bases of the land and stock to Sherri and Mark?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

40

Mary receives a liquidating distribution from Snell Corporation as part of a redemption of all of its stock.Mary's basis in the Snell stock is $10,000.In exchange for her stock,Mary receives property with an $8,000 basis and a $15,000 FMV that is subject to a $3,000 mortgage.Mary also receives cash of $5,000.What is Mary's recognized gain?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

41

Parent Corporation for ten years has owned all of the stock of Subsidiary Corporation,which manufactures widgets.Parent's basis in Subsidiary's stock is $500,000.Subsidiary Corporation is insolvent and has no assets to redeem any of the stock that Parent Corporation owns when it liquidates.Nearly all of Subsidiary's gross income during the past five years has come from nonpassive activities.Parent can recognize

A)a $500,000 short-term capital loss.

B)a $500,000 long-term capital loss.

C)a $500,000 ordinary loss.

D)a $500,000 bad debt deduction.

A)a $500,000 short-term capital loss.

B)a $500,000 long-term capital loss.

C)a $500,000 ordinary loss.

D)a $500,000 bad debt deduction.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

42

Carly owns 25% of Base Corporation's single class of stock and Premier Corporation owns the remaining 75%.Carly's basis in the Base stock is $200,000 and Premier Corporation's basis in the Base stock is $600,000.Carly receives property with a $175,000 adjusted basis and a $250,000 FMV and Premier Corporation receives property with a $600,000 adjusted basis and a $750,000 FMV in complete liquidation of Base Corporation.All of Base's cash is used to pay its liabilities.Which of following statements is correct concerning the tax effects of the liquidation?

A)Neither Carly nor Premier Corporation will recognize a gain.

B)Carly will recognize some gain but Premier Corporation will not recognize any gain.

C)Both Carly and Premier will recognize some gain.

D)Carly will not recognize any gain but Premier will recognize some gain.

A)Neither Carly nor Premier Corporation will recognize a gain.

B)Carly will recognize some gain but Premier Corporation will not recognize any gain.

C)Both Carly and Premier will recognize some gain.

D)Carly will not recognize any gain but Premier will recognize some gain.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

43

A subsidiary recognizes no gain or loss on a distribution to a parent corporation owning more the majority of the subsidiary's stock in a complete liquidation.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

44

The liquidation of a subsidiary corporation must be completed within one tax year to receive nonrecognition treatment.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

45

When a subsidiary corporation is liquidated into its parent corporation under a formal plan of liquidation,the distributions must take place within

A)a six-month period.

B)a 12-month period.

C)the current and next tax years.

D)the current and next three tax years.

A)a six-month period.

B)a 12-month period.

C)the current and next tax years.

D)the current and next three tax years.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

46

Ball Corporation owns 80% of Net Corporation's stock and Jack owns the remaining 20% of Net Corporation's stock.Ball's basis in the Net stock is $200,000 and Jack's basis in the Net stock is $100,000.Under a plan of complete liquidation,Ball Corporation receives property with an adjusted basis of $400,000 and an FMV of $800,000 and Jack receives property with an adjusted basis of $50,000 and an FMV of $200,000.Ball and Jack's recognized gains on the liquidation are:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

47

What event determines when a cash or accrual method of accounting taxpayer reports a liquidating distribution?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

48

Dusty Corporation owns 90% of Palace Corporation's stock and Susan owns the remaining stock.Dusty Corporation's stock basis is $300,000 and Susan's stock basis is $20,000.Under a plan of complete liquidation,Dusty Corporation receives property with a $400,000 adjusted basis and a $540,000 FMV and Susan receives property with a $20,000 adjusted basis and a $60,000 FMV.The bases of the properties are:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

49

Ball Corporation owns 80% of Net Corporation's stock and Jack owns the remaining 20% of Net Corporation's stock.Ball's basis in the Net stock is $200,000 and Jack's basis in the Net stock is $100,000.Under a plan of complete liquidation,Ball Corporation receives property with an adjusted basis of $400,000 and an FMV of $800,000 and Jack receives property with an adjusted basis of $50,000 and an FMV of $200,000.Ball and Jack's bases in the property received are:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

50

Cowboy Corporation owns 90% of the single class of stock in Doggie Corporation.The other 10% is owned by Miguel,an individual.Cowboy's basis in its Doggie Corporation stock is $100,000 and Miguel's basis is $50,000.Doggie Corporation distributes property having an adjusted basis of $150,000 and an FMV of $500,000 to Cowboy Corporation,and $60,000 of money to Miguel as a liquidating distribution.Doggie and Cowboy Corporations must recognize gain of:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

51

Under Illinois Corporation's plan of liquidation,the corporation distributes land to one of its shareholders,Springer.The land,which is used in Illinois trade or business,has a $20,000 adjusted basis and a $60,000 FMV on the distribution date.What are the tax consequences of this distribution to Illinois and Springer?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

52

A subsidiary must recognize depreciation recapture income when the subsidiary is liquidated into the parent.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

53

Market Corporation owns 100% of Subsidiary Corporation's stock.Market Corporation completely liquidates Subsidiary Corporation,receiving land with a $400,000 adjusted basis and a $500,000 FMV in exchange for Subsidiary stock,which has a $300,000 adjusted basis.Market Corporation has a basis in the land of

A)$300,000.

B)$400,000.

C)$500,000.

D)none of the above

A)$300,000.

B)$400,000.

C)$500,000.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

54

Under what circumstances does a liquidating corporation not recognize a gain or loss when making a distribution?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

55

Identify which of the following statements is true.

A)A parent corporation cannot liquidate a subsidiary corporation (having but a single class of stock)and avoid recognizing its realized gain unless the parent corporation owns at least 80% of the subsidiary's stock.

B)The liquidation of a subsidiary corporation must be completed within one tax year to receive nonrecognition treatment.

C)The provisions permitting a tax-free liquidation of a subsidiary corporation apply to both corporate and noncorporate shareholders of the subsidiary.

D)All of the above are false.

A)A parent corporation cannot liquidate a subsidiary corporation (having but a single class of stock)and avoid recognizing its realized gain unless the parent corporation owns at least 80% of the subsidiary's stock.

B)The liquidation of a subsidiary corporation must be completed within one tax year to receive nonrecognition treatment.

C)The provisions permitting a tax-free liquidation of a subsidiary corporation apply to both corporate and noncorporate shareholders of the subsidiary.

D)All of the above are false.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

56

Parent Corporation owns 100% of the single class of stock of Subsidiary Corporation.Parent's basis in the Subsidiary stock is $500,000 when Parent completely liquidates Subsidiary Corporation within a single tax year.The Subsidiary Corporation assets have a $700,000 adjusted basis and an $800,000 FMV at liquidation.As a result of the liquidation,Parent must recognize a

A)$0 gain.

B)$200,000 gain.

C)$300,000 gain.

D)none of the above

A)$0 gain.

B)$200,000 gain.

C)$300,000 gain.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

57

Explain the difference in tax treatment between a partial liquidation and a complete liquidation.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

58

Chip and Dale are each 50% owners of Tree Corporation,a holding company.They have each held their stock since the company was formed five years ago.Tree's money is invested almost entirely in stocks,bonds,rental real estate,and land.All of the stocks are traded on the New York Stock Exchange except for 1,000 shares of Conifer Corporation stock.Conifer is privately held by 50 individuals.Last year,Conifer reported about $2 million in net income.During a meeting with Chip and Dale,you discover that they plan to liquidate Tree Corporation as soon as possible to avoid the personal holding company tax.What tax issues should Chip and Dale consider with respect to this liquidation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

59

Identify which of the following statements is false.

A)Minority shareholders involved in a Sec.332 subsidiary liquidation must recognize a gain or loss under the Sec.331 general liquidation rules.

B)The parent corporation takes a basis in property received when liquidating a subsidiary corporation in a Sec.332 liquidation equal to its basis to the subsidiary corporation.

C)Section 332 is applicable to both the parent corporation and the minority shareholders if they exist.

D)Property received by a minority shareholder takes a basis equal to its fair market value.

A)Minority shareholders involved in a Sec.332 subsidiary liquidation must recognize a gain or loss under the Sec.331 general liquidation rules.

B)The parent corporation takes a basis in property received when liquidating a subsidiary corporation in a Sec.332 liquidation equal to its basis to the subsidiary corporation.

C)Section 332 is applicable to both the parent corporation and the minority shareholders if they exist.

D)Property received by a minority shareholder takes a basis equal to its fair market value.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

60

Identify which of the following statements is false.

A)Liquidating distributions made to minority shareholders in the tax-free liquidation of a controlled subsidiary corporation are treated by the liquidating corporation in the same way as nonliquidating distributions.

B)Sec.337(a)provides that the liquidating corporation recognizes no gain or loss on the distribution of property to the 80% distributee in a complete Sec.332 liquidation.

C)The depreciation recapture provisions in Secs.1245 and 1250 override the Sec.337(a)nonrecognition rule if a controlled subsidiary corporation is liquidated into its parent corporation.

D)A corporation that distributes the stock of a subsidiary may elect to treat the distribution as a sale of the subsidiary's assets.

A)Liquidating distributions made to minority shareholders in the tax-free liquidation of a controlled subsidiary corporation are treated by the liquidating corporation in the same way as nonliquidating distributions.

B)Sec.337(a)provides that the liquidating corporation recognizes no gain or loss on the distribution of property to the 80% distributee in a complete Sec.332 liquidation.

C)The depreciation recapture provisions in Secs.1245 and 1250 override the Sec.337(a)nonrecognition rule if a controlled subsidiary corporation is liquidated into its parent corporation.

D)A corporation that distributes the stock of a subsidiary may elect to treat the distribution as a sale of the subsidiary's assets.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

61

Lake City Corporation owns all of the stock in Columbia Corporation.Pursuant to a plan of complete liquidation,Columbia distributes land having a $500,000 FMV and a $200,000 basis to Lake City.Lake City's basis in the land will be

A)0)

B)$200,000.

C)$500,000.

D)cannot be determined from the facts presented

A)0)

B)$200,000.

C)$500,000.

D)cannot be determined from the facts presented

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

62

The general rule for tax attributes of liquidating corporations is

A)they disappear when the liquidation is complete.

B)they carry over for five years.

C)they disappear only for controlled subsidiary corporations.

D)they carry over for an indefinite period of time.

A)they disappear when the liquidation is complete.

B)they carry over for five years.

C)they disappear only for controlled subsidiary corporations.

D)they carry over for an indefinite period of time.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

63

During 2013,Track Corporation distributes property to Cindy as part of a complete liquidation.Property included in the distribution is $30,000 in cash,land with a $40,000 adjusted basis and a $60,000 FMV,and a copyright without an ascertainable FMV and having a zero basis.The first payment to Cindy of $8,000 for use of the copyrighted property occurs in 2014.Cindy has a basis in the Track stock of $95,000 immediately preceding the liquidation.The minimum amount of gain that Cindy must recognize is a

A)$3,000 gain in 2014.

B)$0 gain in 2013.

C)$3,000 gain in 2013,which is reported on an amended current-year tax return that is filed in 2014.

D)none of the above.

A)$3,000 gain in 2014.

B)$0 gain in 2013.

C)$3,000 gain in 2013,which is reported on an amended current-year tax return that is filed in 2014.

D)none of the above.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

64

Identify which of the following statements is false.

A)An individual taxpayer,who is assessed an additional payment of money based on stock ownership in a corporation whose stock is redeemed in a complete liquidation,may recognize a capital loss to the extent of the additional assessment.

B)The open transaction doctrine defers the shareholder's gain or loss from a liquidation until the assets can be valued by sale or collection.

C)The open transaction doctrine as applied to complete corporate liquidations refers to the numerous planning alternatives available when liquidating a corporation.

D)The IRS asserts that the open transaction doctrine should be used only in extraordinary circumstances.

A)An individual taxpayer,who is assessed an additional payment of money based on stock ownership in a corporation whose stock is redeemed in a complete liquidation,may recognize a capital loss to the extent of the additional assessment.

B)The open transaction doctrine defers the shareholder's gain or loss from a liquidation until the assets can be valued by sale or collection.

C)The open transaction doctrine as applied to complete corporate liquidations refers to the numerous planning alternatives available when liquidating a corporation.

D)The IRS asserts that the open transaction doctrine should be used only in extraordinary circumstances.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

65

Prime Corporation liquidates its 85%-owned subsidiary Bass Corporation under the provisions of Secs.332 and 337.Bass Corporation distributes land to its minority shareholder,John,who owns a 15% interest.The property received by John has a $55,000 FMV.The land was used in the Bass Corporation's business and has a $65,000 adjusted basis and is subject to a $10,000 liability,which is assumed by John.John's basis in his stock is $25,000.What gain or loss will John and Bass Corporation recognize on the distribution of the land?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

66

Greg,a cash method of accounting taxpayer,owns 100 shares of Parker Corporation stock with a basis of $20,000.Greg receives two liquidating distributions of $8,000 on March 3 of last year,and $8,000 on August 8 of this year.The amount of the second distribution is not known until June 15 of this year.Greg recognizes

A)a gain of $8,000 last year and a loss of $12,000 this year.

B)a loss of $2,000 last year and a loss of $2,000 this year.

C)no loss last year and a $4,000 loss this year.

D)none of the above

A)a gain of $8,000 last year and a loss of $12,000 this year.

B)a loss of $2,000 last year and a loss of $2,000 this year.

C)no loss last year and a $4,000 loss this year.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

67

Parent Corporation owns 100% of the stock of Subsidiary Corporation.The adjusted basis of its stock investment is $100,000.A plan of liquidation is adopted.Subsidiary distributes to Parent assets with a $325,000 FMV and a $275,000 adjusted basis.Subsidiary also distributes liabilities in the amount of $40,000.Subsidiary has a $150,000 E&P balance.

a)What is the amount and character of Subsidiary Corporation's recognized gain or loss on the distribution?

b)What is the amount and character of Parent Corporation's recognized gain or loss on the redemption of the Subsidiary stock?

c)What basis does Parent take in the assets?

d)What happens to parent Corporation's basis in the Subsidiary stock and to Subsidiary's tax attributes?

a)What is the amount and character of Subsidiary Corporation's recognized gain or loss on the distribution?

b)What is the amount and character of Parent Corporation's recognized gain or loss on the redemption of the Subsidiary stock?

c)What basis does Parent take in the assets?

d)What happens to parent Corporation's basis in the Subsidiary stock and to Subsidiary's tax attributes?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

68

Lake City Corporation owns all the stock in Columbia Corporation.Pursuant to a plan of complete liquidation,Columbia distributes land having a $500,000 FMV and a $200,000 basis to Lake City.Columbia's gain with respect to the distribution will be

A)no gain recognized.

B)$200,000.

C)$300,000.

D)$500,000.

A)no gain recognized.

B)$200,000.

C)$300,000.

D)$500,000.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

69

Identify which of the following statements is true.

A)Upon liquidation,any capitalized expenditures unamortized at the time of liquidation should be deducted if they have no further value to the corporation.

B)Shareholders who receive an installment obligation as part of their liquidating distribution ordinarily report the FMV of their obligation as part of the consideration received to calculate the amount of recognized gain or loss.

C)A liquidating corporation treats expenses associated with selling its property as an offset against the sales proceeds.

D)All the above are true.

A)Upon liquidation,any capitalized expenditures unamortized at the time of liquidation should be deducted if they have no further value to the corporation.

B)Shareholders who receive an installment obligation as part of their liquidating distribution ordinarily report the FMV of their obligation as part of the consideration received to calculate the amount of recognized gain or loss.

C)A liquidating corporation treats expenses associated with selling its property as an offset against the sales proceeds.

D)All the above are true.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

70

In a Sec.332 liquidation,can a subsidiary corporation recognize losses on distributions to either the parent corporation or minority shareholders?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

71

Hope Corporation was liquidated four years ago.Teresa reported a $40,000 long-term capital gain due to the liquidation on her individual tax return.This year,Teresa pays $6,000 as part of the settlement of a lawsuit against Hope.Due to the $6,000 payment,Teresa recognizes a

A)$6,000 long-term capital loss.

B)$6,000 short-term capital loss.

C)$6,000 ordinary loss.

D)none of the above

A)$6,000 long-term capital loss.

B)$6,000 short-term capital loss.

C)$6,000 ordinary loss.

D)none of the above

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

72

What basis do both the parent and minority shareholders take in the assets received in a Sec.332 liquidation?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

73

Sandy,a cash method of accounting taxpayer,has a basis of $46,000 in her 500 shares of Newt Corporation stock.She receives the following distributions as part of Newt's plan of liquidation. The amount of the final distribution is not known on December 31,2007.What are the tax consequences of the distributions?

A)Sandy will recognize a loss of $4,500 in 2007 and a $1,500 loss in 2008.

B)Sandy will recognize the entire loss in 2007.

C)Sandy will recognize the entire loss in 2008.

D)None of the above is correct.

The amount of the final distribution is not known on December 31,2007.What are the tax consequences of the distributions?A)Sandy will recognize a loss of $4,500 in 2007 and a $1,500 loss in 2008.

B)Sandy will recognize the entire loss in 2007.

C)Sandy will recognize the entire loss in 2008.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

74

Key Corporation distributes a patent with an indeterminable value to Gary as part of a plan of complete liquidation.In addition,Gary receives $40,000 cash and land with a $70,000 FMV and a $30,000 adjusted basis.Gary's basis in the Key stock (a capital asset)surrendered is $120,000.If Gary relies on the open transaction doctrine,at the liquidation date he must recognize a

A)$0 gain.

B)$10,000 capital loss.

C)$30,000 capital loss.

D)$70,000 capital gain.

A)$0 gain.

B)$10,000 capital loss.

C)$30,000 capital loss.

D)$70,000 capital gain.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

75

What attributes of a controlled subsidiary corporation are carried over to the parent when the subsidiary is liquidated?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

76

Liquidating expenses are generally deducted as ordinary and necessary business expenses.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

77

In a Sec.332 liquidation,what bases do both the parent and minority shareholders take in the assets received?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

78

Barbara owns 100 shares of Bond Corporation stock with a basis of $40,000.Barbara receives two liquidating distributions,including $16,000 paid last year and $20,000 paid in the current year.An additional distribution of an undetermined amount is expected next year.On last year's tax return,Barbara can recognize a loss of

A)$0.

B)$1,000.

C)$4,000.

D)$14,000.

A)$0.

B)$1,000.

C)$4,000.

D)$14,000.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

79

Parent Corporation owns 80% of the stock of an insolvent subsidiary corporation.Vic owns the remaining 20% of the stock.The courts determine the subsidiary to be bankrupt,and the shareholders receive nothing for their investment.How do they report their losses?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

80

What are the differences,if any,in the tax rules applying to distributions made to a parent corporation and a minority shareholder when a controlled corporation liquidates?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 102 flashcards in this deck.