Deck 14: Income Taxation of Trusts and Estates

Full screen (f)

Question

Question

The governing instrument for the Lopez Trust contains no definitions of income and principal.The Trust is located in a state that has adopted the Uniform Act.In the current year,the trust reports the following receipts and disbursements:

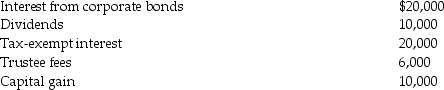

What is the trust's net accounting income?

What is the trust's net accounting income?

What is the trust's net accounting income? Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A trust document does not mention the treatment for depreciation.The state has adopted the Uniform Act.The trust document states that depreciation is a charge against corpus.The trust results are the following:

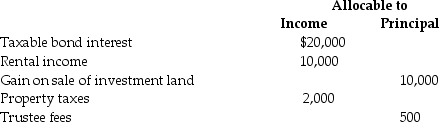

Calculate net accounting income.

Calculate net accounting income.

Calculate net accounting income. Question

Question

Question

A trust document does not define income and principal.The state in which the trust is operated has adopted the Uniform Act.The trust reports the following:

What is the amount of trust's net accounting income?

What is the amount of trust's net accounting income?

What is the amount of trust's net accounting income? Question

Question

Question

Question

Question

Question

Question

Question

Question

A trust document does not define income or principal.The state in which the trust is operated has adopted the Uniform Act,including allocation of depreciation to income.The trust reports the following:

Proceeds from stock sale

Proceeds from stock sale

What is the amount of the trust's net accounting income?

What is the amount of the trust's net accounting income?

Proceeds from stock sale What is the amount of the trust's net accounting income? Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A trust reports the following results:

All of the items are allocated to income except the capital gains.Calculate the maximum amount of trustee fees that are deductible.

All of the items are allocated to income except the capital gains.Calculate the maximum amount of trustee fees that are deductible.

All of the items are allocated to income except the capital gains.Calculate the maximum amount of trustee fees that are deductible. Question

Question

Question

Question

Question

Question

Question

Question

A trust reports the following results:

All of the items above are allocated to income.Calculate the maximum amount of trustee fees that are deductible.

All of the items above are allocated to income.Calculate the maximum amount of trustee fees that are deductible.

All of the items above are allocated to income.Calculate the maximum amount of trustee fees that are deductible. Question

A trust reports the following results:

The trust must distribute all of its income annually.Calculate taxable income after the distribution deduction.

The trust must distribute all of its income annually.Calculate taxable income after the distribution deduction.

The trust must distribute all of its income annually.Calculate taxable income after the distribution deduction. Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The Tucker Trust was established six years ago.The trust is required to distribute all of the trust income at least annually to Betty for life.Capital gains are credited to principal.The current year results of the trust are as follows:

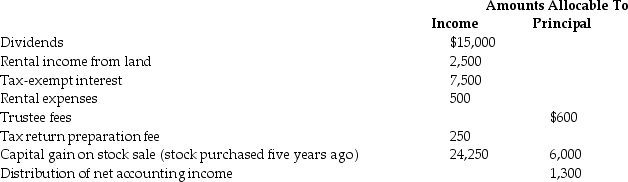

Payment of estimated taxes

Payment of estimated taxes

Compute (a)distributable net income (DNI), (b)the distribution deduction, (c)trust taxable income,and (d)Betty's reportable income and its classification.Charge all of the deductible expenses against rent income.

Payment of estimated taxesCompute (a)distributable net income (DNI), (b)the distribution deduction, (c)trust taxable income,and (d)Betty's reportable income and its classification.Charge all of the deductible expenses against rent income.

Question

A simple trust has the following results:

Calculate the distribution deduction.

Calculate the distribution deduction.

Calculate the distribution deduction. Question

Question

Question

Question

The Williams Trust was established six years ago.The trust document allows the trustee to distribute income in its discretion to beneficiaries Carol and Karen for the next 15 years.The trust will then be terminated and the trust assets will be divided equally between Carol and Karen.Capital gains are part of principal.

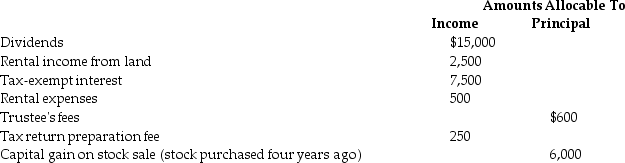

The current year income and expenses of the trust are reported below.

Distribution of net accounting income to:

Distribution of net accounting income to:

Compute (a)distributable net income (DNI), (b)distribution deduction, (c)trust taxable income,and (d)Carol's and Karen's reportable income and its classification.Charge all of the deductible expenses against the rental income.

Compute (a)distributable net income (DNI), (b)distribution deduction, (c)trust taxable income,and (d)Carol's and Karen's reportable income and its classification.Charge all of the deductible expenses against the rental income.

The current year income and expenses of the trust are reported below.

Distribution of net accounting income to: Compute (a)distributable net income (DNI), (b)distribution deduction, (c)trust taxable income,and (d)Carol's and Karen's reportable income and its classification.Charge all of the deductible expenses against the rental income. Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/105

Play

Full screen (f)

Deck 14: Income Taxation of Trusts and Estates

1

The executor or administrator is responsible for all the following estate duties except

A)preserving the estate's existence as a separate taxpayer.

B)collecting the assets.

C)paying the debts and taxes.

D)distributing the property.

A)preserving the estate's existence as a separate taxpayer.

B)collecting the assets.

C)paying the debts and taxes.

D)distributing the property.

A

2

The governing instrument for the Lopez Trust contains no definitions of income and principal.The Trust is located in a state that has adopted the Uniform Act.In the current year,the trust reports the following receipts and disbursements:

What is the trust's net accounting income?

What is the trust's net accounting income?$10,000 - $500 - $200 = $9,300.The gain on the sale of stock and the rest of the sales proceeds constitute corpus.

3

This year,the Huang Trust received $20,000 of dividends and $30,000 of tax-free interest.It distributes all of its receipts to its beneficiary.How should the beneficiary treat the distribution?

The beneficiary is deemed to receive $20,000 of taxable dividend income and $30,000 of tax-free interest.

4

A trust has net accounting income of $15,000.In addition,the trust has a $10,000 capital gain,which is not included in net accounting income.The trust is required to distribute the trust income to the beneficiary.The beneficiary will receive

A)$10,000.

B)$15,000.

C)$24,700.

D)$25,000.

A)$10,000.

B)$15,000.

C)$24,700.

D)$25,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

5

For purposes of trust administration,the term "sprinkling" relates to the mandatory distribution of income among various beneficiaries.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

6

An inter vivos trust may be created by all of the following except

A)a grantor.

B)a trustor.

C)an executor.

D)a transferor.

A)a grantor.

B)a trustor.

C)an executor.

D)a transferor.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

7

Texas Trust receives $10,000 interest on U.S.Treasury bonds and $15,000 interest on State of New York bonds.All $25,000 is distributed to the trust beneficiary,Gary.Which of the following statements is correct?

A)Gary has $25,000 of ordinary gross income.

B)Gary has $10,000 of taxable interest income and $15,000 of tax-free interest income.

C)Gary has no taxable income because the trust must pay the tax.

D)Gary has $10,000 of capital gain and $15,000 of tax-free interest income.

A)Gary has $25,000 of ordinary gross income.

B)Gary has $10,000 of taxable interest income and $15,000 of tax-free interest income.

C)Gary has no taxable income because the trust must pay the tax.

D)Gary has $10,000 of capital gain and $15,000 of tax-free interest income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

8

The term "trust income" when not preceded by an explanatory word relates most closely to

A)gross income.

B)taxable income.

C)distributable net income.

D)net accounting income.

A)gross income.

B)taxable income.

C)distributable net income.

D)net accounting income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

9

Identify which of the following statements is false.

A)A conduit approach-that is,the income has the same character in the hands of the beneficiary as it has to the trust-governs for fiduciary income taxation.

B)Essentially,an estate or trust is taxed on any income it earns,whether retained or distributed.

C)Many of the same rules that determine the calculation of taxable income for individuals apply to trusts.

D)Trusts receive a personal exemption.

A)A conduit approach-that is,the income has the same character in the hands of the beneficiary as it has to the trust-governs for fiduciary income taxation.

B)Essentially,an estate or trust is taxed on any income it earns,whether retained or distributed.

C)Many of the same rules that determine the calculation of taxable income for individuals apply to trusts.

D)Trusts receive a personal exemption.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

10

Beneficiaries of a trust may receive

A)an income interest only.

B)a remainder interest only.

C)both an income and a remainder interest.

D)Any of the above is correct.

A)an income interest only.

B)a remainder interest only.

C)both an income and a remainder interest.

D)Any of the above is correct.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

11

If a state has adopted the Revised Uniform Principal and Income Act,which of the following statements is correct?

A)The state law definition of trust income will preempt any other definitions.

B)The definition of trust income in the trust document will preempt all other definitions.

C)Under state law,tax-exempt interest will not be allocated to income.

D)The definition of principal in the trust document must classify capital gains as principal.

A)The state law definition of trust income will preempt any other definitions.

B)The definition of trust income in the trust document will preempt all other definitions.

C)Under state law,tax-exempt interest will not be allocated to income.

D)The definition of principal in the trust document must classify capital gains as principal.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

12

Identify which of the following statements is false.

A)For purposes of trust administration,the term "sprinkling" relates to the discretionary authority of the trustee to distribute income among various beneficiaries.

B)The IRS may terminate an estate as a taxpayer after the expiration of a reasonable period of time for performance of the administrative duties.

C)Assets in a revocable trust do not avoid probate.

D)Assets in a revocable trust are included in the gross estate.

A)For purposes of trust administration,the term "sprinkling" relates to the discretionary authority of the trustee to distribute income among various beneficiaries.

B)The IRS may terminate an estate as a taxpayer after the expiration of a reasonable period of time for performance of the administrative duties.

C)Assets in a revocable trust do not avoid probate.

D)Assets in a revocable trust are included in the gross estate.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

13

The conduit approach for fiduciary income tax means

A)the distributed income has the same character in the hands of the beneficiary as it has to the trust.

B)the distributed income goes to all beneficiaries proportionately.

C)the distributed income is determined by the trustee annually.

D)the distributed income of a remainder interest is determined by the property.

A)the distributed income has the same character in the hands of the beneficiary as it has to the trust.

B)the distributed income goes to all beneficiaries proportionately.

C)the distributed income is determined by the trustee annually.

D)the distributed income of a remainder interest is determined by the property.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

14

Revocable trusts means

A)the transferor may not demand the assets be returned.

B)income or estate tax savings for the grantor.

C)the assets in the trust avoid probate.

D)the grantor is always the beneficiary.

A)the transferor may not demand the assets be returned.

B)income or estate tax savings for the grantor.

C)the assets in the trust avoid probate.

D)the grantor is always the beneficiary.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements regarding the taxation of a trust is incorrect?

A)An irrevocable trust's income is taxed to the grantor.

B)Trusts are generally not taxed at favorable rates for income shifting.

C)Trusts are not subject to double taxation.

D)A trust's long-term capital gains are taxed at a top rate of 15%.

A)An irrevocable trust's income is taxed to the grantor.

B)Trusts are generally not taxed at favorable rates for income shifting.

C)Trusts are not subject to double taxation.

D)A trust's long-term capital gains are taxed at a top rate of 15%.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements is incorrect?

A)The income tax rules governing estates and trusts are generally identical.

B)Income generated by property owned by an estate or trust is reported on that entity's tax return.

C)Subchapter K contains the special rules applicable to estates and trusts.

D)All of the above are correct.

A)The income tax rules governing estates and trusts are generally identical.

B)Income generated by property owned by an estate or trust is reported on that entity's tax return.

C)Subchapter K contains the special rules applicable to estates and trusts.

D)All of the above are correct.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

17

Identify which of the following statements is false.

A)State trust law preempts the trust document when defining income.

B)The Uniform Act on principal and income requires depreciation to be charged against income.

C)A statement in the trust instrument concerning the allocation of depreciation to principal or income overrides a provision of state law.

D)The Uniform Act allocates royalties to both principal and income.

A)State trust law preempts the trust document when defining income.

B)The Uniform Act on principal and income requires depreciation to be charged against income.

C)A statement in the trust instrument concerning the allocation of depreciation to principal or income overrides a provision of state law.

D)The Uniform Act allocates royalties to both principal and income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

18

Briefly discuss some of the reasons for using a revocable trust.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

19

A tax entity,often called a fiduciary,includes all of the following except

A)estates.

B)complex trusts.

C)testamentary trusts.

D)All of the above are fiduciaries.

A)estates.

B)complex trusts.

C)testamentary trusts.

D)All of the above are fiduciaries.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

20

Briefly discuss the reasons for establishing a trust.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

21

A simple trust

A)may make charitable distributions.

B)may make discretionary distributions of principal.

C)may accumulate income.

D)is required to distribute all of its income currently.

A)may make charitable distributions.

B)may make discretionary distributions of principal.

C)may accumulate income.

D)is required to distribute all of its income currently.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

22

A trust receives no standard deduction when computing taxable income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

23

A trust document does not mention the treatment for depreciation.The state has adopted the Uniform Act.The trust document states that depreciation is a charge against corpus.The trust results are the following:

Calculate net accounting income.

Calculate net accounting income. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

24

The personal exemption available to a trust is adjusted annually based on changes in the consumer price index.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

25

Charitable contributions made by a fiduciary

A)are limited to 50% of fiduciary income.

B)must be authorized in the trust instrument in order to be deductible.

C)flows through to be deducted on the beneficiary's tax return.

D)are subject to the 2% floor.

A)are limited to 50% of fiduciary income.

B)must be authorized in the trust instrument in order to be deductible.

C)flows through to be deducted on the beneficiary's tax return.

D)are subject to the 2% floor.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

26

A trust document does not define income and principal.The state in which the trust is operated has adopted the Uniform Act.The trust reports the following:

What is the amount of trust's net accounting income?

What is the amount of trust's net accounting income? Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

27

Little Trust,whose trust instrument is silent with respect to depreciation,collects rental income of $20,000 and pays property taxes of $1,000.Depreciation expense is $5,000.

Little Trust is in a state where all depreciation is charged to principal.What is the trust's net accounting income?

Little Trust is in a state where all depreciation is charged to principal.What is the trust's net accounting income?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

28

Identify which of the following statements is false.

A)The personal exemption for a trust provides a tax savings when some income is allocated to principal.

B)Distributable net income (DNI)sets the ceiling on the amount of distributions taxed to the beneficiaries.

C)A complex trust must distribute all its income annually.

D)The beneficiaries of a simple trust are taxed on their share of DNI irrespective of the amount they receive.

A)The personal exemption for a trust provides a tax savings when some income is allocated to principal.

B)Distributable net income (DNI)sets the ceiling on the amount of distributions taxed to the beneficiaries.

C)A complex trust must distribute all its income annually.

D)The beneficiaries of a simple trust are taxed on their share of DNI irrespective of the amount they receive.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

29

List some common examples of principal and income items.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

30

A trust is required to distribute 10% of its income to Eleanor.In addition,the trustee in his discretion may distribute income to Eleanor and/or Marshall.The trust has net accounting income of $50,000,none of which is tax-exempt.The trust distributes the $5,000 mandatory payment to Eleanor and also distributes discretionary amounts of $5,000 to Eleanor and $5,000 to Marshall.How much must Eleanor include in income?

A)$5,000

B)$10,000

C)$50,000

D)none of the above

A)$5,000

B)$10,000

C)$50,000

D)none of the above

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

31

The exemption amount for an estate is

A)$0.

B)$100.

C)$300.

D)$600.

A)$0.

B)$100.

C)$300.

D)$600.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

32

A complex trust permits accumulation of current income,provides for charitable contributions,or distributes principal during the taxable year.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

33

Outline the classification of principal and income under the Revised Uniform Principal and Income Act.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

34

Yellow Trust must distribute 33% of its income annually to Patrick.In addition,the trustee in its discretion may distribute additional income to Minna or Patrick.In the current year,the trust has net accounting income and distributable net income of $150,000,none from tax-exempt sources.The trust makes a $50,000 mandatory distribution to Patrick and a discretionary distribution of $20,000 each to Patrick and Minna.What amounts of income do Patrick and Minna report?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

35

A trust document does not define income or principal.The state in which the trust is operated has adopted the Uniform Act,including allocation of depreciation to income.The trust reports the following:

Proceeds from stock sale

What is the amount of the trust's net accounting income?

Proceeds from stock sale What is the amount of the trust's net accounting income? Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

36

A client asks about the relevance of state law in classifying items as principal or income.Explain the relevance.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

37

Estates and trusts

A)are taxed on state and municipal bond interest.

B)are not taxed on capital gains.

C)receive a deduction for administrative expenses not otherwise deducted on the estate tax return (Form 706).

D)receive a $1,000 personal exemption.

A)are taxed on state and municipal bond interest.

B)are not taxed on capital gains.

C)receive a deduction for administrative expenses not otherwise deducted on the estate tax return (Form 706).

D)receive a $1,000 personal exemption.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

38

Explain to a client the significance of the income and principal categorization scheme used for fiduciary accounting purposes.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

39

Identify which of the following statements is false.

A)A trust receives no standard deduction when computing taxable income.

B)Trust tax preparation fees are miscellaneous itemized deductions and subject to the 2% nondeductible floor.

C)There is no limit on a fiduciary's charitable contribution deduction if such a contribution is authorized in the trust instrument.

D)All of the above are false.

A)A trust receives no standard deduction when computing taxable income.

B)Trust tax preparation fees are miscellaneous itemized deductions and subject to the 2% nondeductible floor.

C)There is no limit on a fiduciary's charitable contribution deduction if such a contribution is authorized in the trust instrument.

D)All of the above are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

40

A trust distributes 30% of its income to Mark and 20% to Nancy.The remaining 50% is accumulated.The trust's depreciation is $1,000.The trust instrument is silent regarding the depreciation deduction.State law requires the depreciation be charged to principal.What part of the depreciation deduction will be allocated to Mark?

A)$0

B)$200

C)$300

D)$1,000

A)$0

B)$200

C)$300

D)$1,000

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following is not an addition to trust taxable income when computing distributable net income (DNI)?

A)distribution deduction

B)capital gains allocated to principal

C)tax-exempt interest

D)personal exemption

A)distribution deduction

B)capital gains allocated to principal

C)tax-exempt interest

D)personal exemption

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

42

In the current year,a trust has distributable net income (DNI)of $30,000.During the year,the trust makes a mandatory distribution to Sarah of $5,000 and a discretionary distribution of $10,000 to Kyle.The trust has no tax-exempt income.The distribution deduction of the trust is

A)$30,000.

B)$15,000.

C)$10,000.

D)$5,000.

A)$30,000.

B)$15,000.

C)$10,000.

D)$5,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

43

A trust has the following results: The Uniform Act is followed.The trust document requires one-fifth of the income to be distributed annually to David and the remainder of the income to Patty.What is distributable net income?

A)$74,000

B)$72,000

C)$64,000

D)$62,000

A)$74,000

B)$72,000

C)$64,000

D)$62,000

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

44

Explain the three functions of distributable net income (DNI).

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

45

A trust that is required to distribute all of its income annually receives a personal exemption for the year of

A)$0,because it retains no income.

B)$100.

C)$300.

D)$600.

A)$0,because it retains no income.

B)$100.

C)$300.

D)$600.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

46

A trust reports the following results:

All of the items are allocated to income except the capital gains.Calculate the maximum amount of trustee fees that are deductible.

All of the items are allocated to income except the capital gains.Calculate the maximum amount of trustee fees that are deductible. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

47

Melody Trust has $60,000 of DNI for the current year,$20,000 of rental income and $40,000 of corporate bond interest.The trust instrument requires the trustee to distribute 30% of the trust income to Lee and 70% to Sarah,annually.The trust instrument does not require an allocation of the different types of income to the two beneficiaries.What is the amount and composition of the income reported by Lee and Sarah,respectively?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

48

A trust is required to distribute all of its income annually.It distributes all of the income and $2,000 of principal to the beneficiary.Which of the following statements is correct?

A)The trust is a complex trust and is allowed a $300 exemption.

B)The trust is a complex trust and is allowed a $100 exemption.

C)The trust is a simple trust and is allowed a $300 exemption.

D)The trust is a simple trust and is allowed a $100 exemption.

A)The trust is a complex trust and is allowed a $300 exemption.

B)The trust is a complex trust and is allowed a $100 exemption.

C)The trust is a simple trust and is allowed a $300 exemption.

D)The trust is a simple trust and is allowed a $100 exemption.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

49

The $3,000 limitation on deducting net capital losses does not apply to a trust.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

50

A trust must distribute all of its income annually.Capital gains are allocated to principal.The trust has dividend income of $12,000,capital gains of $6,000,and no expenses.Calculate the trust's taxable income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

51

Panther Trust has net accounting income and distributable net income of $100,000,$75,000 from taxable sources and $25,000 from tax-exempt sources.During the year,the trust makes a mandatory distribution to Julius and Steve of $50,000 each.How much of Steve's distribution is taxable?

A)$12,500

B)$25,000

C)$37,500

D)$50,000

A)$12,500

B)$25,000

C)$37,500

D)$50,000

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

52

Identify which of the following statements is true.

A)The personal exemption available to a trust is adjusted annually based on changes in the consumer price index.

B)Income received by a trust beneficiary has the same character it had at the trust level.

C)Distributable net income (DNI)excludes tax-exempt income.

D)All of the above are false.

A)The personal exemption available to a trust is adjusted annually based on changes in the consumer price index.

B)Income received by a trust beneficiary has the same character it had at the trust level.

C)Distributable net income (DNI)excludes tax-exempt income.

D)All of the above are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

53

Identify which of the following statements is true.

A)Beneficiaries of simple trusts are taxed currently on their pro rata share of taxable distributable net income (DNI)regardless of the actual amount distributed to them during the period.

B)The income received by the beneficiaries of the trust loses its character once it is distributed.

C)Capital losses remaining in the final year of a trust do not pass through to the beneficiaries succeeding to the trust property.

D)All of the above are false.

A)Beneficiaries of simple trusts are taxed currently on their pro rata share of taxable distributable net income (DNI)regardless of the actual amount distributed to them during the period.

B)The income received by the beneficiaries of the trust loses its character once it is distributed.

C)Capital losses remaining in the final year of a trust do not pass through to the beneficiaries succeeding to the trust property.

D)All of the above are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

54

A trust reports the following results:

All of the items above are allocated to income.Calculate the maximum amount of trustee fees that are deductible.

All of the items above are allocated to income.Calculate the maximum amount of trustee fees that are deductible. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

55

A trust reports the following results:

The trust must distribute all of its income annually.Calculate taxable income after the distribution deduction.

The trust must distribute all of its income annually.Calculate taxable income after the distribution deduction. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

56

A simple trust has a distributable net income (DNI)of $50,000 and net accounting income of $60,000,all from taxable sources.The trust has a sole beneficiary,Marty.The trust reports on a calendar tax year and distributes the $60,000 of 2008's net accounting income to Marty on January 20,2009.No other distributions are made in the current year.Marty's taxable income from the trust this year is

A)$0.

B)$49,700.

C)$50,000.

D)$60,000.

A)$0.

B)$49,700.

C)$50,000.

D)$60,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

57

Panther Trust has net accounting income and distributable net income of $100,000,$75,000 from taxable sources and $25,000 from tax-exempt sources.During the year,the trust makes a mandatory distribution to Julius and Steve of $50,000 each.The distribution deduction is

A)$25,000.

B)$50,000.

C)$75,000.

D)$100,000.

A)$25,000.

B)$50,000.

C)$75,000.

D)$100,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

58

Ebony Trust was established two years ago with Brent as the beneficiary.The trust instrument instructed the trustee last year to make discretionary distributions of income to Brent.Beginning in two years,the trustee is instructed to pay all of the trust income earned that year to Brent.What was the trust's personal exemption last year? What will the personal exemption be in two years?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

59

A trust is required to distribute all of its income currently.Two years ago,it had a $10,000 capital loss.Last year,it had a $3,000 capital gain.This year,the trust is terminated.Albert has a 40% interest in the trust,and Barbara has a 60% interest.Barbara receives a capital loss pass-through of

A)$0.

B)$2,400.

C)$4,200.

D)$7,000.

A)$0.

B)$2,400.

C)$4,200.

D)$7,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

60

Distributable net income (DNI)does not include capital gains allocated to principal.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

61

Fred,a cash-basis taxpayer,died on January 15,2012.In 2013,the estate made a $9,000 distribution from estate income to Fred's sole heir.The estate had $20,000 of taxable interest and a $10,000 net long-term capital gain allocable to corpus.The estate incurred $5,000 in expenses attributable to the estate income.What is the estate's distributable net income (DNI)?

A)$15,000

B)$20,000

C)$25,000

D)$30,000

A)$15,000

B)$20,000

C)$25,000

D)$30,000

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

62

Distributable net income (DNI)is not reduced by the charitable contribution deduction when calculating the deductible discretionary distributions for a complex trust.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

63

The distribution deduction for a complex trust is the lesser of the amount distributed or distributable net income,reduced by net tax-exempt income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

64

A trust has net accounting income and distributable net income (DNI)of $60,000,all from taxable sources.The trustee is required to distribute $40,000 of current income to Harry.In addition,the trustee makes a discretionary distribution to Harry of $10,000 and a discretionary distribution to Susan of $30,000.$20,000 of the $40,000 total discretionary distributions is from corpus.Gross income reportable by Harry is

A)$50,000.

B)$45,000.

C)$37,500.

D)$30,000.

A)$50,000.

B)$45,000.

C)$37,500.

D)$30,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

65

The Tucker Trust was established six years ago.The trust is required to distribute all of the trust income at least annually to Betty for life.Capital gains are credited to principal.The current year results of the trust are as follows:

Payment of estimated taxes

Compute (a)distributable net income (DNI), (b)the distribution deduction, (c)trust taxable income,and (d)Betty's reportable income and its classification.Charge all of the deductible expenses against rent income.

Payment of estimated taxesCompute (a)distributable net income (DNI), (b)the distribution deduction, (c)trust taxable income,and (d)Betty's reportable income and its classification.Charge all of the deductible expenses against rent income.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

66

A simple trust has the following results:

Calculate the distribution deduction.

Calculate the distribution deduction. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

67

Identify which of the following statements is true.

A)In a complex trust,distributable net income (DNI)does not act as a ceiling on the amount of the distribution deduction.

B)Distributable net income (DNI)is not reduced by the charitable contribution deduction when calculating the deductible discretionary distributions for a complex trust.

C)In a complex trust,distributable net income (DNI)is not reduced by the charitable contribution deduction when comparing DNI with the mandatory distributions in order to determine the amount of the distribution deduction.

D)All of the above are false.

A)In a complex trust,distributable net income (DNI)does not act as a ceiling on the amount of the distribution deduction.

B)Distributable net income (DNI)is not reduced by the charitable contribution deduction when calculating the deductible discretionary distributions for a complex trust.

C)In a complex trust,distributable net income (DNI)is not reduced by the charitable contribution deduction when comparing DNI with the mandatory distributions in order to determine the amount of the distribution deduction.

D)All of the above are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

68

Identify which of the following statements is true.

A)An individual cannot be both a tier-1 and tier-2 beneficiary in the same year.

B)Tier-2 beneficiaries potentially can receive more favorable tax treatment than tier-1 beneficiaries.

C)Bequests of specific sums of money when distributed out of an estate result in the recognition of gross income by the beneficiary receiving the bequest.

D)All of the above are false.

A)An individual cannot be both a tier-1 and tier-2 beneficiary in the same year.

B)Tier-2 beneficiaries potentially can receive more favorable tax treatment than tier-1 beneficiaries.

C)Bequests of specific sums of money when distributed out of an estate result in the recognition of gross income by the beneficiary receiving the bequest.

D)All of the above are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

69

Apple Trust reports net accounting income of $40,000,all from taxable sources.The trustee is required to distribute $15,000 annually to Megan.The trustee also makes discretionary distributions of $30,000,$7,500 to Megan and $22,500 to Caroline.The trust pays $5,000 of the discretionary distributions from corpus.What is the amount of the distribution deduction?

A)$40,000

B)$45,000

C)$15,000

D)$30,000

A)$40,000

B)$45,000

C)$15,000

D)$30,000

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

70

The Williams Trust was established six years ago.The trust document allows the trustee to distribute income in its discretion to beneficiaries Carol and Karen for the next 15 years.The trust will then be terminated and the trust assets will be divided equally between Carol and Karen.Capital gains are part of principal.

The current year income and expenses of the trust are reported below.

Distribution of net accounting income to:

Compute (a)distributable net income (DNI), (b)distribution deduction, (c)trust taxable income,and (d)Carol's and Karen's reportable income and its classification.Charge all of the deductible expenses against the rental income.

The current year income and expenses of the trust are reported below.

Distribution of net accounting income to: Compute (a)distributable net income (DNI), (b)distribution deduction, (c)trust taxable income,and (d)Carol's and Karen's reportable income and its classification.Charge all of the deductible expenses against the rental income. Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

71

A trust has distributable net income (DNI)of $50,000,including $30,000 tax-exempt interest income and $20,000 taxable interest income.The trust instrument requires that all income be distributed at least annually,30% to Jane and 70% to Joe.What is the amount and character of the income that Jane receives?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

72

Martha died and by her will,specifically bequeathed,and the executor distributed,$20,000 cash and a $70,000 house to Harold.The distributions were made in a year in which the estate had $65,000 of DNI,all from taxable sources.The maximum Harold will be required to report as gross income as a result of these distributions is

A)$0.

B)$20,000.

C)$65,000.

D)$70,000.

A)$0.

B)$20,000.

C)$65,000.

D)$70,000.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

73

An estate made a distribution to its sole beneficiary of $15,000 for the year.This distribution was not the result of a specific bequest.The estate had $40,000 of taxable interest and $34,000 of expenses attributable to earning that interest.What amount of the distribution is taxable to the beneficiary?

A)$40,000

B)$15,000

C)$6,000

D)$0

A)$40,000

B)$15,000

C)$6,000

D)$0

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

74

A trust has net accounting income of $30,000,but distributable net income (DNI)of only $25,000 because certain expenses are charged to principal.The trust is required to distribute $10,000 to Alice and it makes a discretionary distribution of $20,000 to Ben.The trust has no tax-exempt income.The amount that Ben reports as gross income is

A)$20,000.

B)$16,667.

C)$15,000.

D)none of the above

A)$20,000.

B)$16,667.

C)$15,000.

D)none of the above

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

75

Apple Trust reports net accounting income of $40,000,all from taxable sources.The trustee is required to distribute $15,000 annually to Megan.The trustee also makes discretionary distributions of $30,000,$7,500 to Megan and $22,500 to Caroline.The trust pays $5,000 of the discretionary distributions from corpus.What is the taxable amount of the Megan's tier-2 distribution?

A)$7,500

B)$6,250

C)$15,000

D)$22,500

A)$7,500

B)$6,250

C)$15,000

D)$22,500

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

76

Sukdev Basi funded an irrevocable simple trust in May 2008.The trust benefits Sukdev's son for life and grandson upon the son's death.One of the assets he transferred to the trust was Jetco stock,which had an FMV on the transfer date of $40,000.Sukdev's basis in the stock was $44,000,and he paid no gift tax on the transfer.The stock's value has dropped to $33,000,and the trustee thinks that now,October 2011,might be the time to sell the stock and take the loss deduction.For 2011,the trust will have $20,000 of income exclusive of any gain or loss.Sukdev's taxable income is approximately $15,000.What tax and nontax issues should the trustee consider concerning the possible sale of the stock?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

77

Describe the tier system for trust beneficiaries.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

78

Identify which of the following statements is true.

A)Tax-exempt income is allocated among beneficiaries in the proportion that total tax-exempt income bears to total distributable net income (DNI).

B)Both income required to be distributed currently and discretionary income distributions are included in tier-1 distributions.

C)Under the tier system,tier-2 beneficiaries are the first to absorb income.

D)All are false.

A)Tax-exempt income is allocated among beneficiaries in the proportion that total tax-exempt income bears to total distributable net income (DNI).

B)Both income required to be distributed currently and discretionary income distributions are included in tier-1 distributions.

C)Under the tier system,tier-2 beneficiaries are the first to absorb income.

D)All are false.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

79

Explain how to determine the deductible portion of trustee's fees.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

80

In the year of termination,a trust incurs a $20,000 NOL.In addition,it has a $30,000 NOL carryover from the two preceding tax years.The trust distributes 40% of its assets to Sam,30% of its assets to Alex,and 30% of its assets to Catherine.How much of the NOL can Sam (who has $150,000 of gross income)deduct on his return in the year that the trust terminates?

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 105 flashcards in this deck.