Deck 8: Supply in a Competitive Market

Full screen (f)

Question

Use the following to answer question:

Figure 8.5

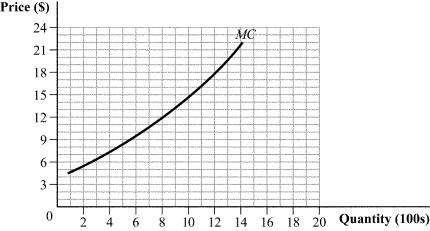

(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

Figure 8.5

(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

Question

Use the following to answer question:

Table 8.1

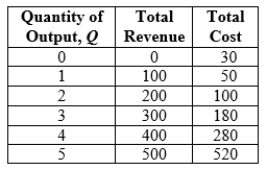

(Table 8.1) The level of output where marginal revenue equals marginal cost is:

A)3)

B)5)

C)2)

D) 4.

Table 8.1

(Table 8.1) The level of output where marginal revenue equals marginal cost is:

A)3)

B)5)

C)2)

D) 4.

Question

Use the following to answer question:

Figure 8.7

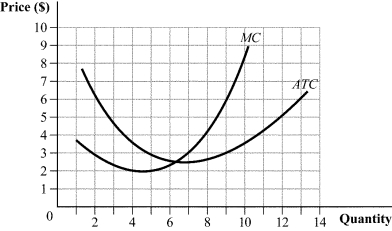

(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

Figure 8.7

(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

Question

Question

Use the following to answer question:

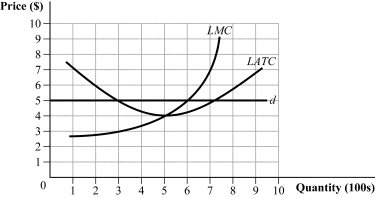

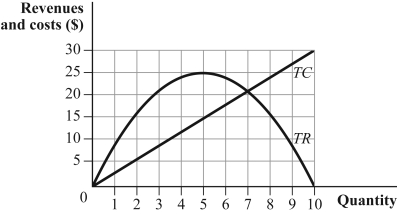

Figure 8.2

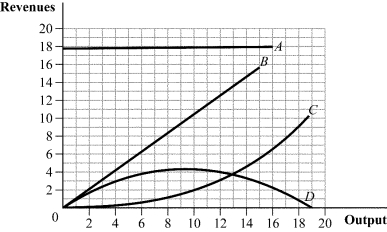

(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

Figure 8.2

(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

Question

Question

Use the following to answer question:

Table 8.2

(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

A) less; more

B) less; less

C) more; more

D) more; less

Table 8.2

(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

A) less; more

B) less; less

C) more; more

D) more; less

Question

Question

Question

Which of the following characteristics relate(s) to perfect competition?

A) I and II

B) II and III

C) II

D) III

A) I and II

B) II and III

C) II

D) III

Question

Use the following to answer question:

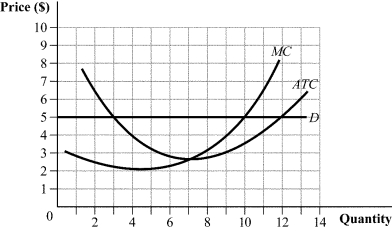

Figure 8.6

(Figure 8.6) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

Figure 8.6

(Figure 8.6) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

Question

Use the following to answer question:

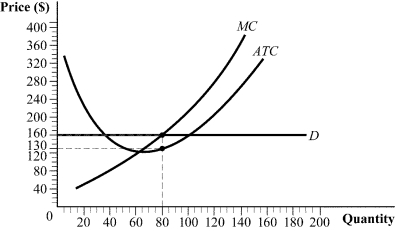

Figure 8.10

(Figure 8.10) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Figure 8.10

(Figure 8.10) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Question

Use the following to answer question:

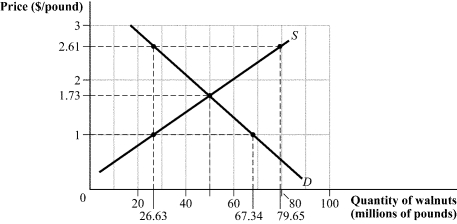

Figure 8.3

(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) II and III

D) I

Figure 8.3

(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) II and III

D) I

Question

Question

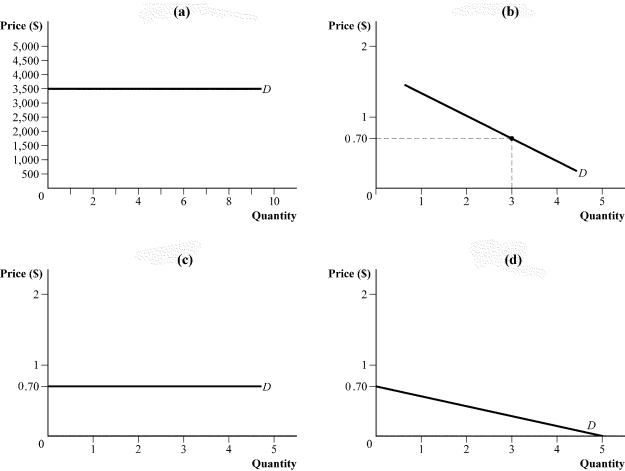

Use the following to answer question:

Figure 8.4

(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

A) panel a.

B) panel b.

C) panel c.

D) panel d.

Figure 8.4

(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

A) panel a.

B) panel b.

C) panel c.

D) panel d.

Question

Use the following to answer question:

Figure 8.9

(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

A) -$60.

B) $48.

C) $60.

D) -$20.

Figure 8.9

(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

A) -$60.

B) $48.

C) $60.

D) -$20.

Question

Use the following to answer question:

Figure 8.8

(Figure 8.8) Which of the following statements is (are) TRUE?

A) I

B) II and III

C) II

D) I and III

Figure 8.8

(Figure 8.8) Which of the following statements is (are) TRUE?

A) I

B) II and III

C) II

D) I and III

Question

Question

Which of the following statements is (are) TRUE of price-taking firms?

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

Question

Use the following to answer question:

Figure 8.1

(Figure 8.1) Which of the following statements is (are) TRUE?

A) II and III

B) III

C) I

D) I and II

Figure 8.1

(Figure 8.1) Which of the following statements is (are) TRUE?

A) II and III

B) III

C) I

D) I and II

Question

Question

Which of the following statements is (are) TRUE?

A) I, II, and III

B) II and III

C) III

D) II

A) I, II, and III

B) II and III

C) III

D) II

Question

Question

Use the following to answer question:

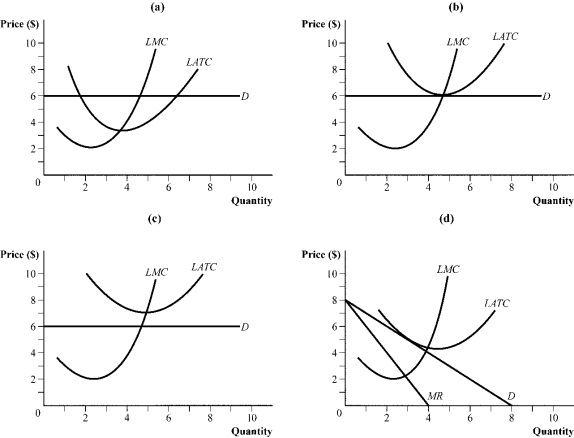

Figure 8.16

(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

Figure 8.16

(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

Question

Question

Question

Use the following to answer question:

Figure 8.15

(Figure 8.15) Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) I and III

D) III

Figure 8.15

(Figure 8.15) Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) I and III

D) III

Question

Question

Question

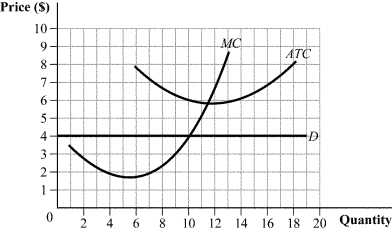

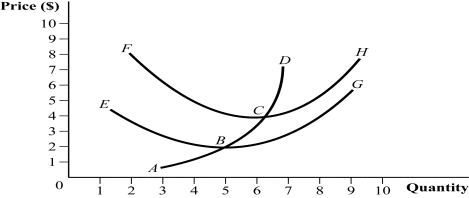

Use the following to answer question:

Figure 8.12

(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

A) B, C, and D.

B) A, B, C, and D.

C) E, B, C, and D.

D) B, C, and H.

Figure 8.12

(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

A) B, C, and D.

B) A, B, C, and D.

C) E, B, C, and D.

D) B, C, and H.

Question

Question

With which of the following scenarios should a perfectly competitive firm shut down in the short run?

A) II

B) III

C) II and III

D) I and III

A) II

B) III

C) II and III

D) I and III

Question

Question

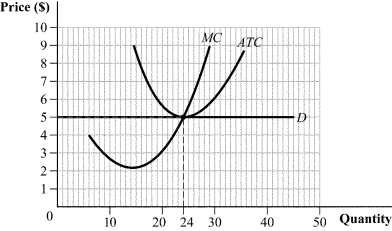

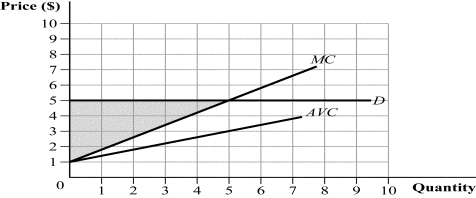

Use the following to answer question:

Figure 8.13

(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Figure 8.13

(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Question

Use the following to answer question:

Figure 8.11

(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Figure 8.11

(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Question

Question

Question

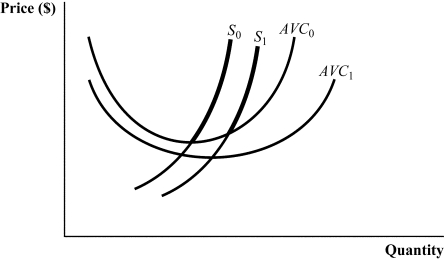

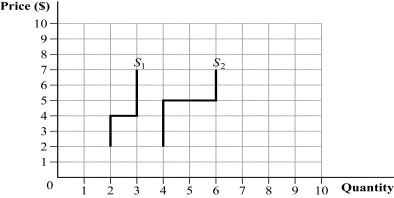

Use the following to answer question:

Figure 8.14

(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A)700.

B)250.

C) 1,050.

D) 500.

Figure 8.14

(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A)700.

B)250.

C) 1,050.

D) 500.

Question

Question

Question

Which of the following statements is (are) TRUE?

A) I, II, and III

B) II and III

C) I and III

D) I

A) I, II, and III

B) II and III

C) I and III

D) I

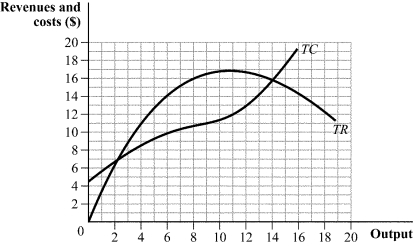

Question

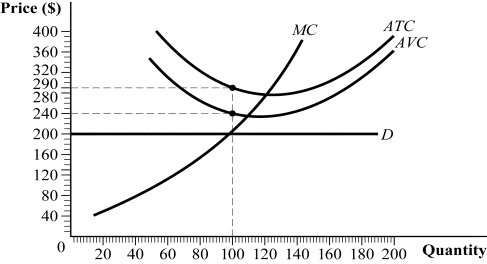

(Graph)  Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits. Question

Answer the following questions.

Question

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2.

Question

Question

Use the following to answer question:

Figure 8.18

(Figure 8.18) Which of the following statements is (are) TRUE?

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Figure 8.18

(Figure 8.18) Which of the following statements is (are) TRUE?

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Question

Use the following to answer question:

Figure 8.20

(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

Figure 8.20

(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

Question

Use the following to answer question:

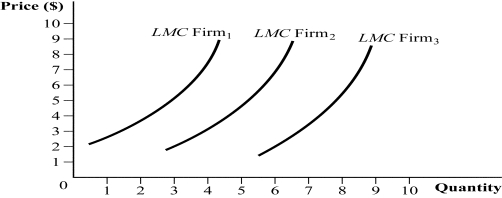

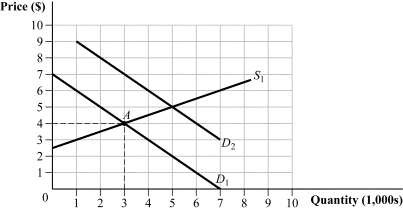

Figure 8.19

(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

A) II

B) III

C) II and III

D) I

Figure 8.19

(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

A) II

B) III

C) II and III

D) I

Question

Question

Answer the following questions.

Question

Question

Question

Use the following to answer question:

Figure 8.17

(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Figure 8.17

(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Question

A March 25, 2010, article at SunSentinel.com reported, "Strawberry farmers in Florida are facing such a sharp collapse in prices for their berries that many are deciding to simply leave huge tracts of the berries to rot in the fields. . . . Wholesale prices that were $17 to $19 for a flat of eight containers have now fallen to $5 to $6 a flat."

Question

Question

Use the following to answer question:

Figure 8.21

(Figure 8.21) Answer each of the following questions.

Figure 8.21

(Figure 8.21) Answer each of the following questions.

Question

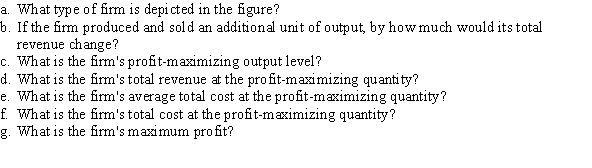

Complete the following table and identify the quantity that maximizes profit.

Question

Question

Suppose that there are 1,000 firms in a perfectly competitive industry, each with a short-run total cost curve given by TC = 800 + 8Q + 0.1Q2 and marginal cost curve given by MC = 8 + 0.2Q.

Question

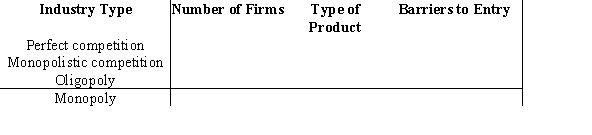

Complete the following table, choosing from this list: one, few, identical, some, unique, differentiated, identical or differentiated, many, none. Some words may be used more than once.

Question

Answer the following questions.

Question

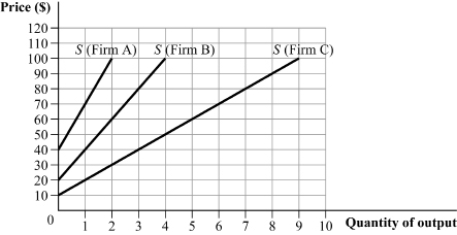

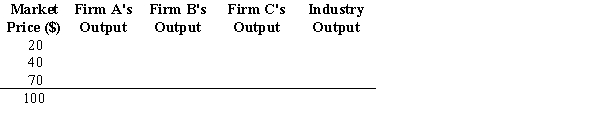

A perfectly competitive industry consists of 50 East Coast firms and 80 West Coast firms. Each of the East Coast firms has a short-run supply curve of QE = 20P, and each of the West Coast firms has a short-run supply curve of QW = 30P.

Question

Use the following to answer question:

Figure 8.26

(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

Figure 8.26

(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

Question

Question

Question

Question

Question

Question

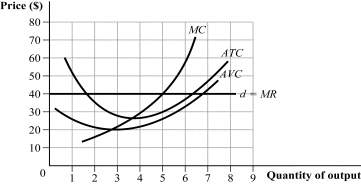

Use the following to answer question:

Figure 8.23

(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

Figure 8.23

(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

Question

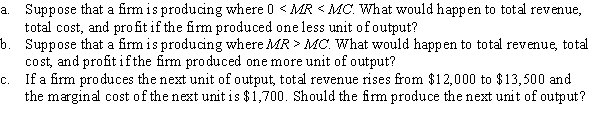

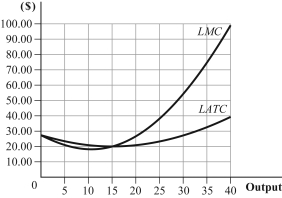

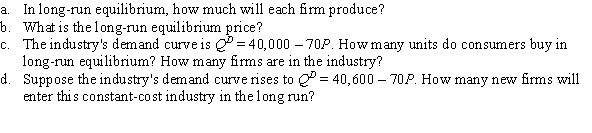

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2.

Question

Question

Use the following to answer question:

Figure 8.24

(Figure 8.24) Answer the following questions.

Figure 8.24

(Figure 8.24) Answer the following questions.

Question

Question

Question

Question

Use the following to answer question:

Figure 8.22

(Figure 8.22) Answer the following questions:

Figure 8.22

(Figure 8.22) Answer the following questions:

Question

Suppose that a perfectly competitive firm's AVC curve is given by AVC = WQ, and its marginal cost curve is given by MC = 2WQ, where W is the wage rate.

Question

Use the following to answer question:

Figure 8.25

(Figure 8.25) Answer the following questions.

Figure 8.25

(Figure 8.25) Answer the following questions.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/93

Play

Full screen (f)

Deck 8: Supply in a Competitive Market

1

Use the following to answer question:

Figure 8.5

(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

Figure 8.5

(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

B

2

Use the following to answer question:

Table 8.1

(Table 8.1) The level of output where marginal revenue equals marginal cost is:

A)3)

B)5)

C)2)

D) 4.

Table 8.1

(Table 8.1) The level of output where marginal revenue equals marginal cost is:

A)3)

B)5)

C)2)

D) 4.

D

3

Use the following to answer question:

Figure 8.7

(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

Figure 8.7

(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

A

4

To maximize profits, a firm should produce where:

A) MR = MC.

B) TR/Q = TC/Q.

C) P = AVC.

D) ATC < P < AVC.

A) MR = MC.

B) TR/Q = TC/Q.

C) P = AVC.

D) ATC < P < AVC.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

5

Use the following to answer question:

Figure 8.2

(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

Figure 8.2

(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

6

A firm should _____ output whenever MR exceeds MC because _____.

A) reduce; revenues will rise by more than costs, increasing the firm's profit

B) reduce; total revenues exceed total costs

C) expand; revenues will rise by more than costs, increasing the firm's profit

D) not change; selling more output will increase marginal revenue by less than marginal cost

A) reduce; revenues will rise by more than costs, increasing the firm's profit

B) reduce; total revenues exceed total costs

C) expand; revenues will rise by more than costs, increasing the firm's profit

D) not change; selling more output will increase marginal revenue by less than marginal cost

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

7

Use the following to answer question:

Table 8.2

(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

A) less; more

B) less; less

C) more; more

D) more; less

Table 8.2

(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

A) less; more

B) less; less

C) more; more

D) more; less

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

8

Why is the type of product sold in an industry an important characteristic?

A) A firm that can differentiate its product from that of rivals may be able to charge a higher price for a superior product.

B) A firm that sells intangible goods is usually considered a monopoly.

C) Expensive products are usually sold by perfectly competitive firms.

D) Service industries cannot differentiate their products, which makes it easy for new firms to enter the industry.

A) A firm that can differentiate its product from that of rivals may be able to charge a higher price for a superior product.

B) A firm that sells intangible goods is usually considered a monopoly.

C) Expensive products are usually sold by perfectly competitive firms.

D) Service industries cannot differentiate their products, which makes it easy for new firms to enter the industry.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

9

Economists assume that firms maximize:

A) the difference between marginal revenue and marginal cost.

B) TR = PQ.

C) = TR - TC.

D) P - ATC, the profit per unit of output.

A) the difference between marginal revenue and marginal cost.

B) TR = PQ.

C) = TR - TC.

D) P - ATC, the profit per unit of output.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following characteristics relate(s) to perfect competition?

A) I and II

B) II and III

C) II

D) III

A) I and II

B) II and III

C) II

D) III

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

11

Use the following to answer question:

Figure 8.6

(Figure 8.6) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

Figure 8.6

(Figure 8.6) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

12

Use the following to answer question:

Figure 8.10

(Figure 8.10) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Figure 8.10

(Figure 8.10) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

13

Use the following to answer question:

Figure 8.3

(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) II and III

D) I

Figure 8.3

(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) II and III

D) I

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

14

The idea that firms pursue actions to maximize profits is:

A) generally rejected by economists in favor of the idea that firms maximize revenues.

B) a reasonable assumption, because firms that do not maximize profits will see their market share drain away to their profit-maximizing rivals.

C) easier to accomplish when management has little oversight from shareholders and boards of directors.

D) refuted by evidence that firms engage in goodwill advertising and other charitable activities.

A) generally rejected by economists in favor of the idea that firms maximize revenues.

B) a reasonable assumption, because firms that do not maximize profits will see their market share drain away to their profit-maximizing rivals.

C) easier to accomplish when management has little oversight from shareholders and boards of directors.

D) refuted by evidence that firms engage in goodwill advertising and other charitable activities.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

15

Use the following to answer question:

Figure 8.4

(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

A) panel a.

B) panel b.

C) panel c.

D) panel d.

Figure 8.4

(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

A) panel a.

B) panel b.

C) panel c.

D) panel d.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

16

Use the following to answer question:

Figure 8.9

(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

A) -$60.

B) $48.

C) $60.

D) -$20.

Figure 8.9

(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

A) -$60.

B) $48.

C) $60.

D) -$20.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

17

Use the following to answer question:

Figure 8.8

(Figure 8.8) Which of the following statements is (are) TRUE?

A) I

B) II and III

C) II

D) I and III

Figure 8.8

(Figure 8.8) Which of the following statements is (are) TRUE?

A) I

B) II and III

C) II

D) I and III

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

18

In the market for lock washers, a perfectly competitive market, the current equilibrium price is $5 per box. Washer King, one of the many producers of washers, has a daily short-run total cost given by TC = 190 + 0.20Q + 0.0025Q2, where Q measures boxes of washers. Washer King's corresponding marginal cost is MC = 0.20 + 0.005Q. How many boxes of washers should Washer King produce per day to maximize profit?

A) 280

B) 960

C) 1,450

D) 2,125

A) 280

B) 960

C) 1,450

D) 2,125

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements is (are) TRUE of price-taking firms?

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

20

Use the following to answer question:

Figure 8.1

(Figure 8.1) Which of the following statements is (are) TRUE?

A) II and III

B) III

C) I

D) I and II

Figure 8.1

(Figure 8.1) Which of the following statements is (are) TRUE?

A) II and III

B) III

C) I

D) I and II

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

21

Suppose a perfectly competitive industry has 300 firms, and the short-run supply curve for each firm is given by Q = 2P. What is the short-run industry supply curve?

A) QS = 150P

B) QS = 600

C) QS = 600P

D) QS = 300 + 2P

A) QS = 150P

B) QS = 600

C) QS = 600P

D) QS = 300 + 2P

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is (are) TRUE?

A) I, II, and III

B) II and III

C) III

D) II

A) I, II, and III

B) II and III

C) III

D) II

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

23

In a perfectly competitive market with 50 firms, output is zero at prices less than $20. At prices of $20 to $29.99, each firm will produce 1 unit of output. At any price of $30 or more, each firm will produce 3 units of output. At a price of $27, the industry produces _____ units, and at a price of $35, the industry produces _____units.

A) 16.67; 50

B) 50; 150

C) 30; 75

D) 9; 45

A) 16.67; 50

B) 50; 150

C) 30; 75

D) 9; 45

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

24

Use the following to answer question:

Figure 8.16

(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

Figure 8.16

(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

25

In a perfectly competitive market with 2,000 firms, output is zero at prices less than $10. At prices of $10 to $19.99, each firm will produce 100 units of output. At any price of $20 or more, each firm will produce 300 units of output. As this industry expands output, however, prices of the key inputs to production increase substantially. The total industry output at a market price of $33 is:

A) between 200,000 and 800,000.

B) 600,000 or less.

C) greater than 600,000.

D) 800,000.

A) between 200,000 and 800,000.

B) 600,000 or less.

C) greater than 600,000.

D) 800,000.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

26

In a perfectly competitive industry, the equilibrium price is $56 and the minimum average total cost of the industry's firms is $40. If this is a constant-cost industry, we can expect that in the long run, firms will _____ the market, shifting the industry's short-run supply curve _____.

A) enter; outward until the minimum average total cost rises to $56.

B) enter; outward until the new equilibrium price is $40.

C) enter; inward until firms are making positive profit.

D) exit; inward until firms are breaking even.

A) enter; outward until the minimum average total cost rises to $56.

B) enter; outward until the new equilibrium price is $40.

C) enter; inward until firms are making positive profit.

D) exit; inward until firms are breaking even.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following to answer question:

Figure 8.15

(Figure 8.15) Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) I and III

D) III

Figure 8.15

(Figure 8.15) Which of the following statements is (are) TRUE?

A) I, II, and III

B) II

C) I and III

D) III

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

28

A firm's short-run total cost is TC = 10,100 + 7,700Q - 100Q2 + Q3/3, and its marginal cost is MC = 7,700 - 200Q + Q2. What is the firm's shutdown price?

A) $45

B) $200

C) $1,100

D) $18

A) $45

B) $200

C) $1,100

D) $18

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

29

The perfectly competitive firm's short-run supply curve is:

A) the portion of its marginal cost curve that lies above average variable cost.

B) the portion of its marginal cost curve that lies above average total cost.

C) its average variable cost curve, which lies above marginal revenue.

D) its average total cost curve, which lies above marginal revenue.

A) the portion of its marginal cost curve that lies above average variable cost.

B) the portion of its marginal cost curve that lies above average total cost.

C) its average variable cost curve, which lies above marginal revenue.

D) its average total cost curve, which lies above marginal revenue.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

30

Use the following to answer question:

Figure 8.12

(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

A) B, C, and D.

B) A, B, C, and D.

C) E, B, C, and D.

D) B, C, and H.

Figure 8.12

(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

A) B, C, and D.

B) A, B, C, and D.

C) E, B, C, and D.

D) B, C, and H.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

31

A street vendor's annual license fee was recently increased by the city. The street vendor's:

A) marginal cost curve will shift out, along with her average variable cost curve.

B) marginal cost curve will shift in, along with her average variable cost curve.

C) marginal and average variable cost curves will not be affected.

D) total variable cost curve will rotate upward.

A) marginal cost curve will shift out, along with her average variable cost curve.

B) marginal cost curve will shift in, along with her average variable cost curve.

C) marginal and average variable cost curves will not be affected.

D) total variable cost curve will rotate upward.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

32

With which of the following scenarios should a perfectly competitive firm shut down in the short run?

A) II

B) III

C) II and III

D) I and III

A) II

B) III

C) II and III

D) I and III

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

33

A perfectly competitive firm maximizes profit by producing 500 units of output, selling each unit for $10. The firm's average variable cost is $7 and average fixed cost is $2. What is the firm's producer surplus?

A) $500

B) $1,500

C) $1,000

D) $1

A) $500

B) $1,500

C) $1,000

D) $1

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

34

Use the following to answer question:

Figure 8.13

(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Figure 8.13

(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

35

Use the following to answer question:

Figure 8.11

(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Figure 8.11

(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

36

Pitch (a sticky black substance made from petroleum) is a key input in the production of clay targets. If the price of pitch falls, clay target manufacturers will encounter a(n) _____ shift of their marginal cost curve and a(n)_____ shift of their average variable cost.

A) inward; inward

B) outward; outward

C) inward; outward

D) outward; inward

A) inward; inward

B) outward; outward

C) inward; outward

D) outward; inward

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

37

A perfectly competitive industry has 100 high-cost producers, each with a short-run supply curve given by QH = 16P, and 100 low-cost producers, each with a short-run supply curve given by QL = 24P. The industry demand curve is given by Qd = 100,000 - 1,000P. At market equilibrium, industry producer surplus is:

A) $800,000.

B) $20,000.

C) $4,000.

D) $1.2 million.

A) $800,000.

B) $20,000.

C) $4,000.

D) $1.2 million.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

38

Use the following to answer question:

Figure 8.14

(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A)700.

B)250.

C) 1,050.

D) 500.

Figure 8.14

(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A)700.

B)250.

C) 1,050.

D) 500.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

39

Stu owns an ice cream parlor that is usually closed during the winter. This winter, however, Stu is considering opening his business in February instead of March. If Stu opens his store in February, he will earn total revenue of $4,000 for the month, incurring variable costs of $3,500 and fixed costs of $1,500. If the store remains closed during February, Stu will earn no revenues and incur fixed costs of $1,500. Stu should:

A) stay closed in February because he will lose $1,000 if he opens.

B) stay closed in February because the $500 of operating profit is insufficient to cover the $1,500 of fixed costs.

C) open in February because the $4,000 of total revenue exceeds the $1,500 of fixed costs.

D) open in February because the $4,000 of total revenue exceeds the $3,500 of variable costs.

A) stay closed in February because he will lose $1,000 if he opens.

B) stay closed in February because the $500 of operating profit is insufficient to cover the $1,500 of fixed costs.

C) open in February because the $4,000 of total revenue exceeds the $1,500 of fixed costs.

D) open in February because the $4,000 of total revenue exceeds the $3,500 of variable costs.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

40

Suppose the market for relay switches is considered perfectly competitive and is in equilibrium at a price of $5,000 per pallet of relay switches. Callahan Relay produces relay switches at an average total cost given by ATC = and marginal cost given by MC = 2Q, where Q measures pallets of relay switches. If Callahan Relay maximizes profit, how much profit will it earn?

A) $125,000

B) $88,000

C) $2.5 million

D) $4.75 million

A) $125,000

B) $88,000

C) $2.5 million

D) $4.75 million

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following statements is (are) TRUE?

A) I, II, and III

B) II and III

C) I and III

D) I

A) I, II, and III

B) II and III

C) I and III

D) I

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

42

(Graph) Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits. Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

43

Answer the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

44

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

45

Suppose that a firm is earning a 12% return on capital in a perfectly competitive industry, and the market return outside the industry is 9.5%. Which of the following statements is (are) TRUE?

A) In the short run, the firm is making a below-market return of 2.5%.

B) In the short run, the firm is making a negative return on capital of 2.5%.

C) In the long run, the firm's return on capital will be 0%.

D) In the long run, the firm's return on capital will be 9.5%.

A) In the short run, the firm is making a below-market return of 2.5%.

B) In the short run, the firm is making a negative return on capital of 2.5%.

C) In the long run, the firm's return on capital will be 0%.

D) In the long run, the firm's return on capital will be 9.5%.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

46

Use the following to answer question:

Figure 8.18

(Figure 8.18) Which of the following statements is (are) TRUE?

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Figure 8.18

(Figure 8.18) Which of the following statements is (are) TRUE?

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

47

Use the following to answer question:

Figure 8.20

(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

Figure 8.20

(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

48

Use the following to answer question:

Figure 8.19

(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

A) II

B) III

C) II and III

D) I

Figure 8.19

(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

A) II

B) III

C) II and III

D) I

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

49

In a perfectly competitive market, each firm has a long-run total cost given by LTC = 100Q - 10Q2 + 1/3Q3 and long-run marginal cost curve given by LMC = 100 - 20Q + Q2. What is the market's long-run equilibrium price?

A) $8.50

B) $33

C) $70

D) $25

A) $8.50

B) $33

C) $70

D) $25

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

50

Answer the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

51

Suppose the long-run equilibrium price in a perfectly competitive market is $100. When demand increases, if it is a(n) _____ industry, the long-run equilibrium price will _____ to reflect a _____ long-run average total cost.

A) decreasing-cost; rise; lower

B) increasing-cost; rise; lower

C) decreasing-cost; fall; lower

D) increasing-cost; fall; higher

A) decreasing-cost; rise; lower

B) increasing-cost; rise; lower

C) decreasing-cost; fall; lower

D) increasing-cost; fall; higher

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

52

In a perfectly competitive industry, the long-run equilibrium price is $12. If a technological innovation lowers production costs, the long-run equilibrium price will:

A) fall below $12.

B) initially fall but then return to $12.

C) initially rise but then return to $12.

D) rise above $12.

A) fall below $12.

B) initially fall but then return to $12.

C) initially rise but then return to $12.

D) rise above $12.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

53

Use the following to answer question:

Figure 8.17

(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Figure 8.17

(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

54

A March 25, 2010, article at SunSentinel.com reported, "Strawberry farmers in Florida are facing such a sharp collapse in prices for their berries that many are deciding to simply leave huge tracts of the berries to rot in the fields. . . . Wholesale prices that were $17 to $19 for a flat of eight containers have now fallen to $5 to $6 a flat."

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

55

In a perfectly competitive industry, there are two types of firms: low-cost producers and high-cost producers. The minimum average total cost of the high-cost producers is $150. The low-cost producers have a long-run total cost curve given by LTC = 150Q - 15Q2 + 0.4Q3, where LMC = 150 - 30Q + 1.2Q2. How much economic rent does the low-cost producer earn?

A) $3,125

B) $14,000

C) $710

D) $45,000

A) $3,125

B) $14,000

C) $710

D) $45,000

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

56

Use the following to answer question:

Figure 8.21

(Figure 8.21) Answer each of the following questions.

Figure 8.21

(Figure 8.21) Answer each of the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

57

Complete the following table and identify the quantity that maximizes profit.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

58

Suppose the market for sprouts is in long-run equilibrium. In the short run, what will happen if an E. coli outbreak reduces the demand for sprouts?

A) The marginal cost curve will shift downward for each producer, leaving prices unchanged.

B) The market price of sprouts will fall, causing each firm to produce fewer sprouts.

C) Existing firms will expand output to make up for the decrease in demand.

D) The marginal cost curve will shift upward for each producer, causing prices to rise and profits to fall.

A) The marginal cost curve will shift downward for each producer, leaving prices unchanged.

B) The market price of sprouts will fall, causing each firm to produce fewer sprouts.

C) Existing firms will expand output to make up for the decrease in demand.

D) The marginal cost curve will shift upward for each producer, causing prices to rise and profits to fall.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

59

Suppose that there are 1,000 firms in a perfectly competitive industry, each with a short-run total cost curve given by TC = 800 + 8Q + 0.1Q2 and marginal cost curve given by MC = 8 + 0.2Q.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

60

Complete the following table, choosing from this list: one, few, identical, some, unique, differentiated, identical or differentiated, many, none. Some words may be used more than once.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

61

Answer the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

62

A perfectly competitive industry consists of 50 East Coast firms and 80 West Coast firms. Each of the East Coast firms has a short-run supply curve of QE = 20P, and each of the West Coast firms has a short-run supply curve of QW = 30P.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

63

Use the following to answer question:

Figure 8.26

(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

Figure 8.26

(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

64

In the lemonade stand industry, Lucy is representative of a low-cost provider and Charlie is representative of a high-cost provider. The minimum average total cost of the high-cost producers is $5. The low-cost producers have a long-run total cost curve given by LTC = 5Q -1.5Q2 + 0.33Q3, where LMC = 5 - 3Q + Q2. How much economic rent does the low-cost producer, such as Lucy, earn?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

65

A perfectly competitive industry consists of 500 identical firms, each with a short-run supply curve given by Qs = -20 + 15P. What is the equation for the industry's short-run supply curve?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

66

Under free entry and exit, to find the quantity where ATC is minimized, the firm can:

A) set marginal cost equal to average total cost and solve for Q.

B) take the first-order condition of average total cost with respect to Q and solve for Q.

C) Either A or B.

D) Neither A nor B.

A) set marginal cost equal to average total cost and solve for Q.

B) take the first-order condition of average total cost with respect to Q and solve for Q.

C) Either A or B.

D) Neither A nor B.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

67

Marginal cost can be calculated as:

A) the derivative of total cost with respect to quantity.

B) the derivative of variable cost with respect to quantity.

C) Either A or B.

D) Neither A nor B.

A) the derivative of total cost with respect to quantity.

B) the derivative of variable cost with respect to quantity.

C) Either A or B.

D) Neither A nor B.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

68

A perfectly competitive industry in long-run equilibrium comprises 200 identical firms. In one of the firms, the workers unionize and receive a 20% wage increase. What happens to the unionized firm in the short run and the long run? Supplement your answer with a graph.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

69

Use the following to answer question:

Figure 8.23

(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

Figure 8.23

(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

70

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

71

If the long-run total cost curve for each firm is given by TC = 60Q - 70Q2 + 4Q3, in the long run, the marginal cost is:

A) 60 - 70Q + 4Q2.

B) 60 - 140Q + 12Q2.

C) 60Q - 70Q2 + 4Q3.

D) -70Q2 + 4Q3.

A) 60 - 70Q + 4Q2.

B) 60 - 140Q + 12Q2.

C) 60Q - 70Q2 + 4Q3.

D) -70Q2 + 4Q3.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

72

Use the following to answer question:

Figure 8.24

(Figure 8.24) Answer the following questions.

Figure 8.24

(Figure 8.24) Answer the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

73

If the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3, in the long run, the marginal cost is:

A) 1,000.

B) 100Q - 10Q2 + Q3.

C) 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2.

A) 1,000.

B) 100Q - 10Q2 + Q3.

C) 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

74

Suppose that the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3. Also suppose there is free entry and exit. To find the quantity where ATC is minimized, solve the following equation for Q:

A) 100 - 20Q + 3Q2 = 1,000 + 100Q - 10Q2 + Q3.

B) 100 - 20Q + 3Q2 = 100 - 10Q + Q2.

C) 100 - 20Q + 3Q2 = 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2 = 1,000(Q + 100 - 10Q + Q2).

A) 100 - 20Q + 3Q2 = 1,000 + 100Q - 10Q2 + Q3.

B) 100 - 20Q + 3Q2 = 100 - 10Q + Q2.

C) 100 - 20Q + 3Q2 = 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2 = 1,000(Q + 100 - 10Q + Q2).

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

75

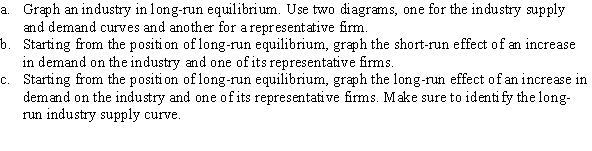

Explain what will happen in each of the following scenarios in a long run constant cost competitive industry.

a. The market price is $50 and firms are earning positive profits.

b. The market price is $25 and firms are earning zero profits.

c. The market price is $15 and firms are earning negative profits.

a. The market price is $50 and firms are earning positive profits.

b. The market price is $25 and firms are earning zero profits.

c. The market price is $15 and firms are earning negative profits.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

76

Use the following to answer question:

Figure 8.22

(Figure 8.22) Answer the following questions:

Figure 8.22

(Figure 8.22) Answer the following questions:

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

77

Suppose that a perfectly competitive firm's AVC curve is given by AVC = WQ, and its marginal cost curve is given by MC = 2WQ, where W is the wage rate.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

78

Use the following to answer question:

Figure 8.25

(Figure 8.25) Answer the following questions.

Figure 8.25

(Figure 8.25) Answer the following questions.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

79

If the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product, in the long run, the marginal cost is:

A) 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2.

C) 500 - 20Q + Q2.

D) -20Q2 + Q3.

A) 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2.

C) 500 - 20Q + Q2.

D) -20Q2 + Q3.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

80

Suppose that the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product. Also suppose there is free entry and exit. To find the quantity where ATC is minimized, the firm would need to solve the following equation for Q:

A) 500 - 40Q + 3Q2 = 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2 = 500 - 20Q + Q2.

C) 500Q - 20Q2 + Q3 = 500 - 20Q + Q2.

D) It would be impossible to do this without more information.

A) 500 - 40Q + 3Q2 = 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2 = 500 - 20Q + Q2.

C) 500Q - 20Q2 + Q3 = 500 - 20Q + Q2.

D) It would be impossible to do this without more information.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 93 flashcards in this deck.