Deck 8: Inventory

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

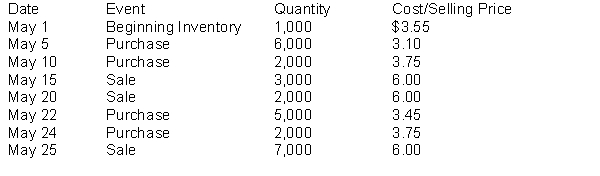

The following inventory transactions took place for NPR Corporation for the month of May:  The ending inventory balance for NPR Corporation, assuming the company uses a perpetual inventory system, and a first-in, first-out (FIFO)cost formula is

The ending inventory balance for NPR Corporation, assuming the company uses a perpetual inventory system, and a first-in, first-out (FIFO)cost formula is

A)$15,000.

B)$14,400.

C)$12,850.

D)$13,800.

The ending inventory balance for NPR Corporation, assuming the company uses a perpetual inventory system, and a first-in, first-out (FIFO)cost formula isA)$15,000.

B)$14,400.

C)$12,850.

D)$13,800.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Enviro Corporation had the following items as inventory as at December 31, 2017:  Assuming Enviro uses a perpetual inventory system, and that none of the inventory items can be grouped together for accounting purposes.The year-end adjusting entry should include a charge to cost of goods sold of

Assuming Enviro uses a perpetual inventory system, and that none of the inventory items can be grouped together for accounting purposes.The year-end adjusting entry should include a charge to cost of goods sold of

A)$223.

B)$188.

C)$35.

D)$0.

Assuming Enviro uses a perpetual inventory system, and that none of the inventory items can be grouped together for accounting purposes.The year-end adjusting entry should include a charge to cost of goods sold ofA)$223.

B)$188.

C)$35.

D)$0.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/127

Play

Full screen (f)

Deck 8: Inventory

1

Use the following information for questions.

During 2017 Ebert Corp.transferred inventory to Siskel Corp.and agreed to repurchase the merchandise early in 2018.Siskel then used the inventory as collateral to borrow from Southern Bank, remitting the proceeds to Ebert.In 2018 when Ebert repurchased the inventory, Siskel used the proceeds to repay its bank loan.

This transaction is known as a(n)

A)consignment.

B)instalment sale.

C)product financing arrangement.

D)sale with delayed payment terms.

During 2017 Ebert Corp.transferred inventory to Siskel Corp.and agreed to repurchase the merchandise early in 2018.Siskel then used the inventory as collateral to borrow from Southern Bank, remitting the proceeds to Ebert.In 2018 when Ebert repurchased the inventory, Siskel used the proceeds to repay its bank loan.

This transaction is known as a(n)

A)consignment.

B)instalment sale.

C)product financing arrangement.

D)sale with delayed payment terms.

C

2

An estimated loss on purchase commitments is reported

A)under other expenses and losses.

B)as a deduction from purchases.

C)as a current liability.

D)as an extraordinary item.

A)under other expenses and losses.

B)as a deduction from purchases.

C)as a current liability.

D)as an extraordinary item.

A

3

Which of the following is correct?

A)Goods on consignment are included in the consignee's inventory.

B)Goods on consignment are included in the consignor's inventory.

C)The consignee essentially has the risks and rewards of ovwnership.

D)Inventory on consignment is always shown in a separate account.

A)Goods on consignment are included in the consignee's inventory.

B)Goods on consignment are included in the consignor's inventory.

C)The consignee essentially has the risks and rewards of ovwnership.

D)Inventory on consignment is always shown in a separate account.

B

4

Goods in transit which are shipped FOB shipping point should be included

A)in the inventory of the buyer.

B)in the inventory of the seller.

C)in the inventory of the shipping company.

D)in no one's inventory until they arrive at their destination.

A)in the inventory of the buyer.

B)in the inventory of the seller.

C)in the inventory of the shipping company.

D)in no one's inventory until they arrive at their destination.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

5

Certain industries allow full or partial refunds for returned inventory.In such cases, which of the following is INCORRECT?

A)The vendor retains the risks and rewards for those items expected to be returned.

B)If returns can be reasonably predicted, then the goods may be considered sold by the vendor and removed from inventory.

C)If returns cannot be predicted, the sale is not recognized and the goods are not removed from inventory.

D)If returns cannot be predicted, the sale is still recognized but the goods are not removed from inventory.

A)The vendor retains the risks and rewards for those items expected to be returned.

B)If returns can be reasonably predicted, then the goods may be considered sold by the vendor and removed from inventory.

C)If returns cannot be predicted, the sale is not recognized and the goods are not removed from inventory.

D)If returns cannot be predicted, the sale is still recognized but the goods are not removed from inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following does NOT correctly describe the implications of an executory contract on the accounting entries and/or disclosures to be made by the purchaser and/or seller?

A)Assets and liabilities are usually recorded at inception of the contract.

B)Assets and liabilities are usually not recorded at inception of the contract.

C)Contract details should be disclosed if the amounts are abnormal in relation to the entity's normal business operations.

D)Assets and liabilities are recognized as performance has occurred.

A)Assets and liabilities are usually recorded at inception of the contract.

B)Assets and liabilities are usually not recorded at inception of the contract.

C)Contract details should be disclosed if the amounts are abnormal in relation to the entity's normal business operations.

D)Assets and liabilities are recognized as performance has occurred.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following items would be inventory for a company like Marriott Hotel Corporation?

A)hotel rooms

B)food and beverage stock

C)cleaning supplies

D)all of the above

A)hotel rooms

B)food and beverage stock

C)cleaning supplies

D)all of the above

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

8

Goods in transit which are shipped FOB destination should be included

A)in the inventory of the buyer.

B)in the inventory of the seller.

C)in the inventory of the shipping company.

D)in no one's inventory until they arrive at their destination.

A)in the inventory of the buyer.

B)in the inventory of the seller.

C)in the inventory of the shipping company.

D)in no one's inventory until they arrive at their destination.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

9

Use the following information for questions.

During 2017 Ebert Corp.transferred inventory to Siskel Corp.and agreed to repurchase the merchandise early in 2018.Siskel then used the inventory as collateral to borrow from Southern Bank, remitting the proceeds to Ebert.In 2018 when Ebert repurchased the inventory, Siskel used the proceeds to repay its bank loan.

On whose books should the cost of the inventory appear at the December 31, 2017 statement of financial position date?

A)Siskel Corp.

B)Ebert Corp.

C)Southern Bank

D)Siskel Corp., with Ebert Corp.making appropriate note disclosure of the transaction

During 2017 Ebert Corp.transferred inventory to Siskel Corp.and agreed to repurchase the merchandise early in 2018.Siskel then used the inventory as collateral to borrow from Southern Bank, remitting the proceeds to Ebert.In 2018 when Ebert repurchased the inventory, Siskel used the proceeds to repay its bank loan.

On whose books should the cost of the inventory appear at the December 31, 2017 statement of financial position date?

A)Siskel Corp.

B)Ebert Corp.

C)Southern Bank

D)Siskel Corp., with Ebert Corp.making appropriate note disclosure of the transaction

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

10

A manufacturer that carries very little inventory likely follows the

A)allowance method.

B)just-in-time method.

C)indirect method.

D)replacement method.

A)allowance method.

B)just-in-time method.

C)indirect method.

D)replacement method.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

11

A hardware retailer typically maintains the following inventory account(s):

A)Merchandise Inventory.

B)Raw Materials and Work in Process only.

C)Raw Materials, Work in Process and Finished Goods.

D)Work in Process and Merchandise Inventory.

A)Merchandise Inventory.

B)Raw Materials and Work in Process only.

C)Raw Materials, Work in Process and Finished Goods.

D)Work in Process and Merchandise Inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

12

Companies that carry inventories must carefully monitor inventory in order to

A)have the greatest selection available so customers can always find what they want.

B)minimize carrying costs and keep inventory levels high so stockouts never occur.

C)keep inventory levels high to maximize profits.

D)minimize carrying costs and meet customer demands.

A)have the greatest selection available so customers can always find what they want.

B)minimize carrying costs and keep inventory levels high so stockouts never occur.

C)keep inventory levels high to maximize profits.

D)minimize carrying costs and meet customer demands.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

13

Wilma received merchandise on consignment from Betty.As of March 31, Wilma had recorded the transaction as a purchase and included the goods in inventory.The effect of this on Wilma's financial statements for March 31 would be

A)net income was correct and current assets and current liabilities were overstated.

B)net income, current assets, and current liabilities were overstated.

C)net income and current liabilities were overstated.

D)no effect.

A)net income was correct and current assets and current liabilities were overstated.

B)net income, current assets, and current liabilities were overstated.

C)net income and current liabilities were overstated.

D)no effect.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

14

Under IFRs, liabilities related to non-cancellable purchase commitments are typically recognized

A)on the date the contract takes effect.

B)at the time of payment.

C)when the purchase is recorded in the accounting system.

D)in the period a decline in market price occurs.

A)on the date the contract takes effect.

B)at the time of payment.

C)when the purchase is recorded in the accounting system.

D)in the period a decline in market price occurs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

15

The cost of goods available for sale is calculated as

A)beginning inventory plus ending inventory.

B)beginning inventory minus ending inventory.

C)beginning inventory plus the cost of goods acquired during the period.

D)cost of goods acquired during the period minus ending inventory.

A)beginning inventory plus ending inventory.

B)beginning inventory minus ending inventory.

C)beginning inventory plus the cost of goods acquired during the period.

D)cost of goods acquired during the period minus ending inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

16

A manufacturing company typically maintains the following inventory account(s):

A)Merchandise Inventory.

B)Raw Materials and Work in Process only.

C)Raw Materials, Work in Process and Finished Goods.

D)Work in Process and Merchandise Inventory.

A)Merchandise Inventory.

B)Raw Materials and Work in Process only.

C)Raw Materials, Work in Process and Finished Goods.

D)Work in Process and Merchandise Inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

17

The cost of inventory is made up of

A)cost to purchase inventory only.

B)cost of purchase and allocated direct labour only.

C)cost of purchase, allocated direct labour, and allocated overhead.

D)cost of allocated direct labour and allocated overhead only.

A)cost to purchase inventory only.

B)cost of purchase and allocated direct labour only.

C)cost of purchase, allocated direct labour, and allocated overhead.

D)cost of allocated direct labour and allocated overhead only.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

18

Fred received merchandise on consignment from Dino.As of January 31, Fred included the goods in inventory, but did NOT record the transaction.The effect of this on Fred's financial statements for January 31 would be

A)net income, current assets, and retained earnings were understated.

B)net income was correct and current assets were understated.

C)net income, current assets, and retained earnings were overstated.

D)net income and current assets were overstated and current liabilities were understated.

A)net income, current assets, and retained earnings were understated.

B)net income was correct and current assets were understated.

C)net income, current assets, and retained earnings were overstated.

D)net income and current assets were overstated and current liabilities were understated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following items should be included in inventory at the balance sheet date?

A)goods in transit which were purchased FOB destination

B)goods received from another company for sale on consignment

C)goods sold to a customer, which are being held for the customer to call for at his or her convenience

D)goods in transit which were purchased FOB shipping point

A)goods in transit which were purchased FOB destination

B)goods received from another company for sale on consignment

C)goods sold to a customer, which are being held for the customer to call for at his or her convenience

D)goods in transit which were purchased FOB shipping point

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

20

When substantially all risks and rewards of ownership have passed to the purchaser, the purchaser then recognizes an asset.For this recognition, which of the following statements is correct?

A)The purchaser must have both legal title and possession of the goods.

B)Legal title and possession do not always pass to the purchaser at the same time.

C)In practice, recording inventory purchases often takes place when they leave the seller's place of business.

D)The purchaser must have possession of goods before it has legal title.

A)The purchaser must have both legal title and possession of the goods.

B)Legal title and possession do not always pass to the purchaser at the same time.

C)In practice, recording inventory purchases often takes place when they leave the seller's place of business.

D)The purchaser must have possession of goods before it has legal title.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following statements regarding borrowing costs is correct?

A)Neither ASPE nor IFRS usually require disclosure of these items.

B)They are usually amortized until the majority of the underlying products have been sold.

C)They are usually treated as period costs if they are incurred to bring inventories to a condition ready for sale.

D)If interest is capitalized, ASPE requires this policy and the amount capitalized to be disclosed.

A)Neither ASPE nor IFRS usually require disclosure of these items.

B)They are usually amortized until the majority of the underlying products have been sold.

C)They are usually treated as period costs if they are incurred to bring inventories to a condition ready for sale.

D)If interest is capitalized, ASPE requires this policy and the amount capitalized to be disclosed.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

22

Conversion costs include

A)all materials plus direct labour.

B)all materials plus variable overhead allocated.

C)direct labour plus variable and fixed overhead allocated.

D)direct labour plus fixed overhead allocated.

A)all materials plus direct labour.

B)all materials plus variable overhead allocated.

C)direct labour plus variable and fixed overhead allocated.

D)direct labour plus fixed overhead allocated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

23

On June 25, Veranda Corp.accepted delivery of merchandise which it purchased on account.As of June 30, Veranda had NOT recorded the transaction nor included the merchandise in its inventory.The effect of this on Veranda's June 30 balance sheet would be

A)assets and shareholders' equity were overstated but liabilities were not affected.

B)shareholders' equity was the only item affected by the omission.

C)assets, liabilities, and shareholders' equity were understated.

D)assets and liabilities were understated but shareholders' equity was not affected.

A)assets and shareholders' equity were overstated but liabilities were not affected.

B)shareholders' equity was the only item affected by the omission.

C)assets, liabilities, and shareholders' equity were understated.

D)assets and liabilities were understated but shareholders' equity was not affected.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following types of interest cost incurred in connection with the purchase or manufacture of inventory should be capitalized as a product cost?

A)purchase discounts lost

B)interest incurred during the production of discrete projects such as ships or real estate projects

C)interest incurred on notes payable to vendors for routine purchases made on a repetitive basis

D)interest on a building mortgage

A)purchase discounts lost

B)interest incurred during the production of discrete projects such as ships or real estate projects

C)interest incurred on notes payable to vendors for routine purchases made on a repetitive basis

D)interest on a building mortgage

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

25

On December 27, Cloud Corp.accepted delivery of merchandise which it purchased on account.As of December 31, Cloud had recorded the transaction, but did not include the merchandise in its year-end inventory.The effect of this on its December 31 financial statements would be

A)net income, current assets, and retained earnings were understated.

B)net income was correct and current assets were understated.

C)net income was understated and current liabilities were overstated.

D)net income was overstated and current assets were understated.

A)net income, current assets, and retained earnings were understated.

B)net income was correct and current assets were understated.

C)net income was understated and current liabilities were overstated.

D)net income was overstated and current assets were understated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

26

If the unavoidable costs of completing a purchase commitment are higher than the expected benefits from receiving the contracted goods or services, IFRS requires a loss provision to be recognized.This is known as a(n)

A)executory contract.

B)purchase commitment.

C)onerous contract.

D)impaired contract.

A)executory contract.

B)purchase commitment.

C)onerous contract.

D)impaired contract.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following best describes the concept of standard costs?

A)They are the costs that should be incurred per unit of finished goods inventory.

B)They are the costs that are actually incurred per unit of finished goods inventory.

C)When using standard costs, unallocated overhead is capitalized.

D)Standard costs are always acceptable for reporting purposes.

A)They are the costs that should be incurred per unit of finished goods inventory.

B)They are the costs that are actually incurred per unit of finished goods inventory.

C)When using standard costs, unallocated overhead is capitalized.

D)Standard costs are always acceptable for reporting purposes.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

28

All else being equal, which of the following statements with respect to the impact of inventory errors is NOT correct?

A)An overstatement of ending inventory will result in an understatement of income.

B)An overstatement of ending inventory will result in an overstatement of income.

C)An overstatement of beginning inventory will result in an understatement of income.

D)An understatement of beginning inventory will cause cost of goods sold to be understated.

A)An overstatement of ending inventory will result in an understatement of income.

B)An overstatement of ending inventory will result in an overstatement of income.

C)An overstatement of beginning inventory will result in an understatement of income.

D)An understatement of beginning inventory will cause cost of goods sold to be understated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is correct?

A)Selling costs are product costs.

B)Manufacturing overhead costs are product costs.

C)Interest costs for routine inventories are product costs.

D)Direct labour costs are usually period costs.

A)Selling costs are product costs.

B)Manufacturing overhead costs are product costs.

C)Interest costs for routine inventories are product costs.

D)Direct labour costs are usually period costs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

30

The use of a Purchase Discounts account implies that the recorded cost of a purchased inventory item is its

A)invoice price plus any purchase discount lost.

B)invoice price less the purchase discount taken.

C)invoice price less the purchase discount allowable whether taken or not.

D)invoice price.

A)invoice price plus any purchase discount lost.

B)invoice price less the purchase discount taken.

C)invoice price less the purchase discount allowable whether taken or not.

D)invoice price.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

31

In a periodic inventory system, if the beginning inventory is overstated

A)net income is understated.

B)working capital is understated.

C)the current ratio is overstated.

D)cost of goods sold is understated.

A)net income is understated.

B)working capital is understated.

C)the current ratio is overstated.

D)cost of goods sold is understated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following best describes the concept of product costs?

A)They are costs that are "attached" to inventory.

B)They are costs that are usually expenses.

C)They usually don't include freight charges.

D)They usually don't include conversion costs.

A)They are costs that are "attached" to inventory.

B)They are costs that are usually expenses.

C)They usually don't include freight charges.

D)They usually don't include conversion costs.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is correct regarding vendor rebates?

A)Vendor rebates are generally recorded as a reduction from sales.

B)The rebate is never recognized until it is actually received.

C)If the rebate meets asset recognition criteria, the receivable is allocated to goods sold.

D)Vendor rebates are generally recorded as a reduction in the purchase cost of inventory.

A)Vendor rebates are generally recorded as a reduction from sales.

B)The rebate is never recognized until it is actually received.

C)If the rebate meets asset recognition criteria, the receivable is allocated to goods sold.

D)Vendor rebates are generally recorded as a reduction in the purchase cost of inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

34

All of the following costs should be charged to expense in the period in which they are incurred EXCEPT for

A)manufacturing overhead costs for a product manufactured and sold in the same accounting period.

B)costs which will not benefit any future period.

C)costs from idle manufacturing capacity resulting from an unexpected plant shutdown.

D)costs of normal shrinkage and scrap incurred for the manufacture of a product in ending inventory.

A)manufacturing overhead costs for a product manufactured and sold in the same accounting period.

B)costs which will not benefit any future period.

C)costs from idle manufacturing capacity resulting from an unexpected plant shutdown.

D)costs of normal shrinkage and scrap incurred for the manufacture of a product in ending inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

35

If a material amount of inventory has been ordered through a formal purchase contract at the statement of financial position date, for future delivery, at firm prices,

A)this fact must be disclosed.

B)disclosure is required only if prices have declined since the date of the order.

C)disclosure is required only if prices have since risen substantially.

D)an appropriation of retained earnings is necessary.

A)this fact must be disclosed.

B)disclosure is required only if prices have declined since the date of the order.

C)disclosure is required only if prices have since risen substantially.

D)an appropriation of retained earnings is necessary.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

36

In a periodic inventory system, if ending inventory is understated,

A)net income is understated.

B)working capital is overstated.

C)the current ratio is overstated.

D)cost of goods sold is understated.

A)net income is understated.

B)working capital is overstated.

C)the current ratio is overstated.

D)cost of goods sold is understated.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

37

To record a "basket purchase" or to allocate a joint product cost, which method is the most rational?

A)average cost

B)relative sales value

C)fair value

D)amortized cost

A)average cost

B)relative sales value

C)fair value

D)amortized cost

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

38

An EXCEPTION to the general rule that costs should be charged to expense in the period incurred is

A)factory overhead costs incurred on a product manufactured but not sold during the current accounting period.

B)interest costs for financing of inventories that are routinely manufactured in large quantities on a repetitive basis.

C)general and administrative fixed costs incurred in connection with the purchase of inventory.

D)sales commission and salary costs incurred in connection with the sale of inventory.

A)factory overhead costs incurred on a product manufactured but not sold during the current accounting period.

B)interest costs for financing of inventories that are routinely manufactured in large quantities on a repetitive basis.

C)general and administrative fixed costs incurred in connection with the purchase of inventory.

D)sales commission and salary costs incurred in connection with the sale of inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

39

A "basket purchase" is a purchase of

A)a group of units with similar characteristics at a single lump-sum price.

B)individual units with similar characteristics priced individually.

C)a group of units with different characteristics at a single lump-sum price.

D)individual units with different characteristics priced individually.

A)a group of units with similar characteristics at a single lump-sum price.

B)individual units with similar characteristics priced individually.

C)a group of units with different characteristics at a single lump-sum price.

D)individual units with different characteristics priced individually.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

40

NOT using the net method because of difficulties that may arise is a good example of applying

A)relevance.

B)the cost/benefit constraint.

C)representational faithfulness.

D)the fair value principle.

A)relevance.

B)the cost/benefit constraint.

C)representational faithfulness.

D)the fair value principle.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

41

When using the moving-average cost formula with a perpetual system,

A)a weighted-average cost is calculated at year end.

B)a new unit cost is calculated each time a sale is made.

C)a new unit cost is calculated each time a purchase is made.

D)a new unit cost is calculated both when a sale is made and when a purchase is made.

A)a weighted-average cost is calculated at year end.

B)a new unit cost is calculated each time a sale is made.

C)a new unit cost is calculated each time a purchase is made.

D)a new unit cost is calculated both when a sale is made and when a purchase is made.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following is a characteristic of a perpetual inventory system?

A)Inventory purchases are debited to a Purchases account.

B)Inventory records arenot kept for every item.

C)Cost of goods sold is recorded with each sale.

D)Cost of goods sold is determined as the amount of purchases less the change in inventory.

A)Inventory purchases are debited to a Purchases account.

B)Inventory records arenot kept for every item.

C)Cost of goods sold is recorded with each sale.

D)Cost of goods sold is determined as the amount of purchases less the change in inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

43

Why are inventories included in the computation of net income?

A)to determine cost of goods sold

B)to determine sales revenue

C)to determine merchandise returns

D)Inventories are not included in the computation of net income.

A)to determine cost of goods sold

B)to determine sales revenue

C)to determine merchandise returns

D)Inventories are not included in the computation of net income.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

44

The inventory costing method that can be used only for goods that are NOT ordinarily interchangeable is the

A)LIFO method.

B)specific identification method.

C)weighted average cost method.

D)FIFO method.

A)LIFO method.

B)specific identification method.

C)weighted average cost method.

D)FIFO method.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following does NOT correctly describe the specific identification cost formula?

A)This method is most appropriate when goods are not interchangeable.

B)This method is most appropriate when goods are interchangeable.

C)This method is generally used for expensive, one-of-a-kind merchandise.

D)This method is often used for merchandise with serial numbers such as televisions.

A)This method is most appropriate when goods are not interchangeable.

B)This method is most appropriate when goods are interchangeable.

C)This method is generally used for expensive, one-of-a-kind merchandise.

D)This method is often used for merchandise with serial numbers such as televisions.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

46

The use of a "replacement cost" definition of "market" is based on the assumption that

A)a decline in an item's replacement cost results in a decline in its selling price.

B)prices will fall in the same proportion as input costs fall.

C)replacement cost is appropriate for all situations.

D)using "net realizable value less a normal profit margin" will arbitrarily shift profits from one period to another.

A)a decline in an item's replacement cost results in a decline in its selling price.

B)prices will fall in the same proportion as input costs fall.

C)replacement cost is appropriate for all situations.

D)using "net realizable value less a normal profit margin" will arbitrarily shift profits from one period to another.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

47

The following inventory transactions took place for NPR Corporation for the month of May: The ending inventory balance for NPR Corporation, assuming the company uses a perpetual inventory system, and a first-in, first-out (FIFO)cost formula is

A)$15,000.

B)$14,400.

C)$12,850.

D)$13,800.

The ending inventory balance for NPR Corporation, assuming the company uses a perpetual inventory system, and a first-in, first-out (FIFO)cost formula isA)$15,000.

B)$14,400.

C)$12,850.

D)$13,800.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following does NOT correctly describe the FIFO cost formula?

A)This method assumes that the oldest inventory costs are the first costs recorded for cost of goods sold.

B)This method assumes that most current inventory costs are the first costs recorded for cost of goods sold.

C)This method approximates the physical flow of most types of goods.

D)This method is permitted under both ASPE and IFRS.

A)This method assumes that the oldest inventory costs are the first costs recorded for cost of goods sold.

B)This method assumes that most current inventory costs are the first costs recorded for cost of goods sold.

C)This method approximates the physical flow of most types of goods.

D)This method is permitted under both ASPE and IFRS.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

49

All else being equal, which of the following statements is correct for a company that uses the FIFO costing formula with a perpetual inventory system (compared to a periodic system)?

A)The value of the ending inventory would be higher under a periodic system.

B)The value of the ending inventory would be lower under a periodic system.

C)The value of the ending inventory would be the same under both systems.

D)The periodic system would not require any additional entries at the end of the period.

A)The value of the ending inventory would be higher under a periodic system.

B)The value of the ending inventory would be lower under a periodic system.

C)The value of the ending inventory would be the same under both systems.

D)The periodic system would not require any additional entries at the end of the period.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

50

When inventory declines in value below original (historical)cost, and this decline is considered other than temporary, what is the maximum amount that the inventory can be valued at?

A)net realizable value

B)selling price

C)historical cost

D)net realizable value reduced by a normal profit margin

A)net realizable value

B)selling price

C)historical cost

D)net realizable value reduced by a normal profit margin

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

51

When using a periodic inventory system,

A)a Purchases account is not used.

B)a Cost of Goods Sold account is used.

C)two entries are required to record a sale.

D)a Cost of Goods Sold account is not used.

A)a Purchases account is not used.

B)a Cost of Goods Sold account is used.

C)two entries are required to record a sale.

D)a Cost of Goods Sold account is not used.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

52

In no case can "net realizable value" (in the lower of cost and net realizable value rule)be more than

A)estimated selling price in the ordinary course of business.

B)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal.

C)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal and an allowance for a normal profit margin.

D)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal, an allowance for a normal profit margin, and an adequate reserve for possible future losses.

A)estimated selling price in the ordinary course of business.

B)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal.

C)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal and an allowance for a normal profit margin.

D)estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal, an allowance for a normal profit margin, and an adequate reserve for possible future losses.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

53

If two factories produce the exact same product having the same costs, and factory costs are completely allocated to the individual products, the factory operating at 80% capacity (while the other operates at 100% capacity)

A)would have a lower rate of cost allocation to each unit of production.

B)would have a higher rate of cost allocation to each unit of production.

C)would have the same rate of cost allocation to each unit of production as the 100% capacity operation.

D)would be operating at a loss, because of unused capacity.

A)would have a lower rate of cost allocation to each unit of production.

B)would have a higher rate of cost allocation to each unit of production.

C)would have the same rate of cost allocation to each unit of production as the 100% capacity operation.

D)would be operating at a loss, because of unused capacity.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following does NOT correctly describe a periodic inventory system?

A)Cost of goods sold is calculated every time a sale is made.

B)Cost of goods sold is a residual amount.

C)Assuming a FIFO cost flow, cost of goods sold would equal those that calculated by the perpetual system.

D)Inventory and cost of goods sold must be updated at the end of the period.

A)Cost of goods sold is calculated every time a sale is made.

B)Cost of goods sold is a residual amount.

C)Assuming a FIFO cost flow, cost of goods sold would equal those that calculated by the perpetual system.

D)Inventory and cost of goods sold must be updated at the end of the period.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

55

The primary basis of accounting for inventories is cost.A departure from the cost basis of pricing inventory is required where there is evidence that when the goods are sold in the ordinary course of business, their

A)selling price will be less than their replacement cost.

B)replacement cost will be more than their net realizable value.

C)future utility will be less than their cost.

D)cost will be less than their replacement cost.

A)selling price will be less than their replacement cost.

B)replacement cost will be more than their net realizable value.

C)future utility will be less than their cost.

D)cost will be less than their replacement cost.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

56

Borrowing costs

A)are never included in the costs of inventories.

B)must only be included in inventory cost if they relate to inventories produced in large quantities and on a repetitive basis.

C)are capitalized if incurred to finance activities that help bring inventories to a condition available for sale.

D)none of the above

A)are never included in the costs of inventories.

B)must only be included in inventory cost if they relate to inventories produced in large quantities and on a repetitive basis.

C)are capitalized if incurred to finance activities that help bring inventories to a condition available for sale.

D)none of the above

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following statements is INCORRECT regarding the overriding objectives underlying inventory standards and guide management?

A)Report an inventory cost on the statement of financial position that is representative of the inventory's recent cost.

B)Choose an approach that corresponds as closely as possible to the physical flow of goods.

C)Use the same method for all inventory assets that have similar economic characteristics.

D)It is permissible under ASPE to use any inventory method, including LIFO.

A)Report an inventory cost on the statement of financial position that is representative of the inventory's recent cost.

B)Choose an approach that corresponds as closely as possible to the physical flow of goods.

C)Use the same method for all inventory assets that have similar economic characteristics.

D)It is permissible under ASPE to use any inventory method, including LIFO.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following does NOT correctly describe a perpetual inventory system?

A)Cost of goods sold is calculated every time a sale is made.

B)Assuming shrinkage of zero, inventory and cost of goods sold do not have to be updated at the end of the period.

C)The use of this system eliminates the requirement for an annual physical inventory count.

D)Assuming a FIFO cost flow, cost of goods sold would equal that calculated by the periodic system.

A)Cost of goods sold is calculated every time a sale is made.

B)Assuming shrinkage of zero, inventory and cost of goods sold do not have to be updated at the end of the period.

C)The use of this system eliminates the requirement for an annual physical inventory count.

D)Assuming a FIFO cost flow, cost of goods sold would equal that calculated by the periodic system.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

59

An inventory cost formula in which the oldest costs incurred rarely have an effect on the ending inventory valuation is

A)FIFO.

B)moving-average cost.

C)LIFO.

D)weighted average.

A)FIFO.

B)moving-average cost.

C)LIFO.

D)weighted average.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following does NOT correctly describe the weighted average cost formula?

A)It prices inventory on the basis of the average cost of beginning inventory.

B)It prices inventory on the basis of the average cost of goods available for sale during the period.

C)It takes into account that the volume of goods acquired at each price is different.

D)It includes the cost of beginning inventory in the calculations.

A)It prices inventory on the basis of the average cost of beginning inventory.

B)It prices inventory on the basis of the average cost of goods available for sale during the period.

C)It takes into account that the volume of goods acquired at each price is different.

D)It includes the cost of beginning inventory in the calculations.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

61

The lower of cost and NRV standard specific that the comparison is usually applied on

A)total inventory.

B)individual categories of inventory.

C)an item-by-item basis.

D)major categories of inventory.

A)total inventory.

B)individual categories of inventory.

C)an item-by-item basis.

D)major categories of inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

62

If a unit of inventory has declined in value below original cost, but the market value exceeds net realizable value, the amount to be used for purposes of inventory valuation is

A)net realizable value.

B)original cost.

C)market value.

D)net realizable value less a normal profit margin.

A)net realizable value.

B)original cost.

C)market value.

D)net realizable value less a normal profit margin.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following is NOT a premise upon which the gross profit method of estimating inventory is based?

A)Beginning inventory plus purchases equals cost of goods available for sale.

B)The gross profit must be equal to the contribution margin on goods sold.

C)Goods not included in cost of goods sold must be on hand in ending inventory.

D)When an estimate of cost of goods sold is deducted from cost of goods available for sale, the result is an estimate of ending inventory.

A)Beginning inventory plus purchases equals cost of goods available for sale.

B)The gross profit must be equal to the contribution margin on goods sold.

C)Goods not included in cost of goods sold must be on hand in ending inventory.

D)When an estimate of cost of goods sold is deducted from cost of goods available for sale, the result is an estimate of ending inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following statements with respect to the gross profit method of estimating inventory is NOT correct?

A)It may be used for interim reporting.

B)It may be used to estimate ending inventory when inventory has been destroyed.

C)It uses the interrelationship between the accounts used in the cost of goods sold calculation.

D)The use of this method eliminates the need for performing an actual inventory count.

A)It may be used for interim reporting.

B)It may be used to estimate ending inventory when inventory has been destroyed.

C)It uses the interrelationship between the accounts used in the cost of goods sold calculation.

D)The use of this method eliminates the need for performing an actual inventory count.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

65

Under IFRS, bearer plants used to grow produce including tea bushes, grape vines, and rubber trees are accounted for

A)as agricultural assets, in accordance with IAS41.

B)using the cost or revaluation method.

C)as inventory, at cost, in accordance with IAS2.

D)as inventory, at fair value less costs to sell, in accordance with IAS2.

A)as agricultural assets, in accordance with IAS41.

B)using the cost or revaluation method.

C)as inventory, at cost, in accordance with IAS2.

D)as inventory, at fair value less costs to sell, in accordance with IAS2.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

66

Enviro Corporation had the following items as inventory as at December 31, 2017: Assuming Enviro uses a perpetual inventory system, and that none of the inventory items can be grouped together for accounting purposes.The year-end adjusting entry should include a charge to cost of goods sold of

A)$223.

B)$188.

C)$35.

D)$0.

Assuming Enviro uses a perpetual inventory system, and that none of the inventory items can be grouped together for accounting purposes.The year-end adjusting entry should include a charge to cost of goods sold ofA)$223.

B)$188.

C)$35.

D)$0.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following statements regarding presentation and disclosure of inventories is.INCORRECT?

A)Major spare parts and standby equipment may be recognized as inventory if they are not expected to provide benefits beyond the current accounting period.

B)Inventories are one of the most significant assest of manufacturing and merchandising companies.

C)The classification of inventory seldom requires the exercise of professional judgement.

D)Minor spare parts and servicing equipment are usually classified as inventory.

A)Major spare parts and standby equipment may be recognized as inventory if they are not expected to provide benefits beyond the current accounting period.

B)Inventories are one of the most significant assest of manufacturing and merchandising companies.

C)The classification of inventory seldom requires the exercise of professional judgement.

D)Minor spare parts and servicing equipment are usually classified as inventory.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following does NOT correctly describe the concept of net realizable value (NRV)?

A)Estimates of NRV are based on the best evidence available at and shortly after the balance sheet date.

B)NRV generally does not change over time.

C)NRV generally changes over time.

D)A new estimate of NRV is required at each balance sheet date.

A)Estimates of NRV are based on the best evidence available at and shortly after the balance sheet date.

B)NRV generally does not change over time.

C)NRV generally changes over time.

D)A new estimate of NRV is required at each balance sheet date.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

69

Lower of cost and net realizable value

A)is most conservative if applied to the total inventory.

B)is most conservative if applied to major categories of inventory.

C)is most conservative if applied to individual items of inventory.

D)must be applied to major categories for income tax purposes.

A)is most conservative if applied to the total inventory.

B)is most conservative if applied to major categories of inventory.

C)is most conservative if applied to individual items of inventory.

D)must be applied to major categories for income tax purposes.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

70

The inventory turnover ratio is calculated by dividing the cost of goods sold by

A)beginning inventory.

B)ending inventory.

C)average inventory.

D)number of days in the year.

A)beginning inventory.

B)ending inventory.

C)average inventory.

D)number of days in the year.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following inventories may NOT be valued at fair value less costs to sell?

A)grain and livestock futures

B)biological assets

C)farm equipment

D)agricultural produce

A)grain and livestock futures

B)biological assets

C)farm equipment

D)agricultural produce

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

72

The gross profit method of inventory valuation

A)can be used as a substitute for the annual physical count of inventory.

B)assumes past percentages are appropriate for the current period.

C)uses markups but not markdowns.

D)is designed to approximate inventory valuation at the lower of cost and net realizable value.

A)can be used as a substitute for the annual physical count of inventory.

B)assumes past percentages are appropriate for the current period.

C)uses markups but not markdowns.

D)is designed to approximate inventory valuation at the lower of cost and net realizable value.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

73

Which statement is NOT true about the gross profit method of inventory valuation?

A)It may be used to estimate inventories for interim statements.

B)It may be used to estimate inventories for annual statements.

C)It may be used by auditors.

D)It may be used to provide a rough check on the accuracy of the physical inventory count.

A)It may be used to estimate inventories for interim statements.

B)It may be used to estimate inventories for annual statements.

C)It may be used by auditors.

D)It may be used to provide a rough check on the accuracy of the physical inventory count.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following is NOT a required inventory disclosure under ASPE?

A)any portion of foreign exchange gain/loss specifically attributable to inventory items

B)choice of accounting policies adopted to measure the inventory

C)carrying amount of inventory pledged as collateral for liabilities

D)amount of inventory recognized as an expense in the period

A)any portion of foreign exchange gain/loss specifically attributable to inventory items

B)choice of accounting policies adopted to measure the inventory

C)carrying amount of inventory pledged as collateral for liabilities

D)amount of inventory recognized as an expense in the period

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

75

The gross profit method is normally used

A)for insurance purposes, in cases where inventory has been destroyed.

B)for all of these (all of these are exmaples of how the gross profit method is used).

C)to provide a rough check on the accuracy of a physical inventory count.

D)by auditors to estimate a company's inventory for quarterly reporting.

A)for insurance purposes, in cases where inventory has been destroyed.

B)for all of these (all of these are exmaples of how the gross profit method is used).

C)to provide a rough check on the accuracy of a physical inventory count.

D)by auditors to estimate a company's inventory for quarterly reporting.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following criteria does NOT have to be met in order to be able to value inventory above cost?

A)The cost of disposal can be estimated.

B)The sale is assured.

C)There is an active market for the product.

D)The sale must already have occurred.

A)The cost of disposal can be estimated.

B)The sale is assured.

C)There is an active market for the product.

D)The sale must already have occurred.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

77

Under ASPE, agricultural produce, forest products, and mineral products inventories may be accounted for at net realizable value if

A)there is a well-established industry practice of doing so.

B)arbitrary cost allocation would be too costly.

C)costs to bring them to market are expected to be minimal.

D)the company's financial results appear more favourable by doing so.

A)there is a well-established industry practice of doing so.

B)arbitrary cost allocation would be too costly.

C)costs to bring them to market are expected to be minimal.

D)the company's financial results appear more favourable by doing so.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

78

The inventory turnover ratio is calculated as

A)cost of goods sold divided by average inventory.

B)average inventory divided by cost of goods sold.

C)cost of goods sold times average inventory.

D)average assets divided by cost of goods sold.

A)cost of goods sold divided by average inventory.

B)average inventory divided by cost of goods sold.

C)cost of goods sold times average inventory.

D)average assets divided by cost of goods sold.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

79

The gross profit percentage is calculated by

A)dividing cost of goods sold by net sales.

B)dividing gross profit on sales by cost of goods sold.

C)dividing gross profit on sales by net sales.

D)dividing gross profit on sales by goods available for sale.

A)dividing cost of goods sold by net sales.

B)dividing gross profit on sales by cost of goods sold.

C)dividing gross profit on sales by net sales.

D)dividing gross profit on sales by goods available for sale.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

80

The gross profit method of inventory valuation is NOT suitable when

A)a portion of the inventory is destroyed.

B)there is a substantial increase in inventory during the year.

C)there is no beginning inventory because it is the first year of operation.

D)the gross profit percentage applicable to the goods in ending inventory is different from the percentage applicable to the goods sold during the period.

A)a portion of the inventory is destroyed.

B)there is a substantial increase in inventory during the year.

C)there is no beginning inventory because it is the first year of operation.

D)the gross profit percentage applicable to the goods in ending inventory is different from the percentage applicable to the goods sold during the period.

Unlock Deck

Unlock for access to all 127 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 127 flashcards in this deck.