Deck 4: Income From Employment

Full screen (f)

Question

Question

Kate Bell was employed by The Tea Shop Ltd. (a Canadian controlled private corporation) from January to December of 20x4. She earned a gross salary of $72,000.

The following were deducted from her pay during the year:

The following amounts were paid by The Tea Shop Ltd. in 20x4 on Kate's behalf:

The following amounts were paid by The Tea Shop Ltd. in 20x4 on Kate's behalf:

Additional information:

Additional information:

On January 15, 20x2, Kate was given an option to purchase 500 shares of The Tea Shop for $5.00 per share. The market value of the shares on that date was $5.50. Kate exercised her option on June 1, 20x3 when the shares were valued at $7.00. She then sold the shares on March 17, 20x4 when the market value was $8.00 per share.

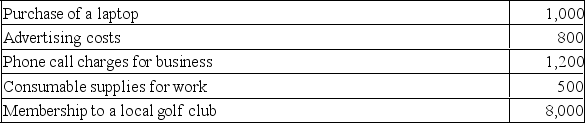

Kate pays $50 a month for her cell phone which she uses to keep in touch with friends and family. She also pays $80 a month to dry-clean her suits, and she purchases a new suit valued at $200 every three months. Kate purchased $300 worth of merchandise (at cost) from her employer during the year. The retail value of the merchandise was $500.

Kate contributed $1,000 to her RRSP during the year.

Required:

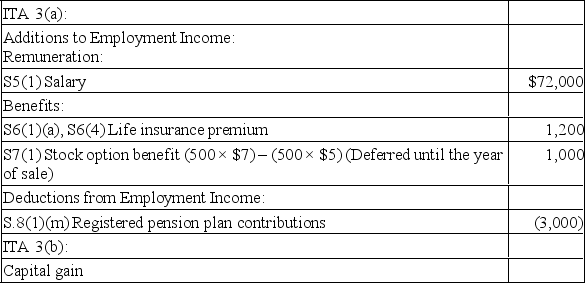

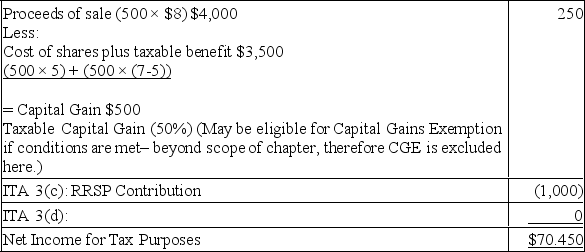

A) Calculate Kate's minimum net income for tax purposes for 20x4, in accordance with Section 3 of the Income Tax Act. Identify items that have been omitted in your calculations. (Kate minimizes her tax liability whenever possible.)

B) Will Kate be able to deduct the stock option deduction to arrive at her taxable income? Why or why not?

The following were deducted from her pay during the year:

The following amounts were paid by The Tea Shop Ltd. in 20x4 on Kate's behalf: Additional information:On January 15, 20x2, Kate was given an option to purchase 500 shares of The Tea Shop for $5.00 per share. The market value of the shares on that date was $5.50. Kate exercised her option on June 1, 20x3 when the shares were valued at $7.00. She then sold the shares on March 17, 20x4 when the market value was $8.00 per share.

Kate pays $50 a month for her cell phone which she uses to keep in touch with friends and family. She also pays $80 a month to dry-clean her suits, and she purchases a new suit valued at $200 every three months. Kate purchased $300 worth of merchandise (at cost) from her employer during the year. The retail value of the merchandise was $500.

Kate contributed $1,000 to her RRSP during the year.

Required:

A) Calculate Kate's minimum net income for tax purposes for 20x4, in accordance with Section 3 of the Income Tax Act. Identify items that have been omitted in your calculations. (Kate minimizes her tax liability whenever possible.)

B) Will Kate be able to deduct the stock option deduction to arrive at her taxable income? Why or why not?

Question

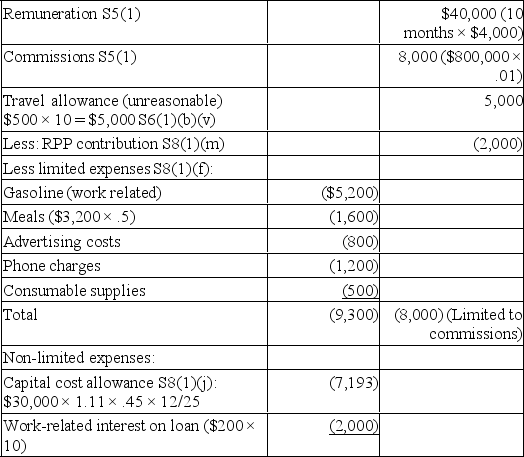

Andy worked for High Speed Bikes Inc. from March 1st to December 31st during 20x1. He earned a monthly base salary of $4,000, plus 1% commission on all of his sales. During 20x1, Andy's sales totaled $800,000. Andy was required by his employer to pay for his employment expenses. He traveled out of his city most days in order to sell to customers in surrounding towns. He received a monthly allowance of $500 to cover his traveling costs (which has been accurately recognized as 'unreasonable'). Andy and his employer each contributed $2,000 to the company's registered pension plan in 20x1.

Andy provided you with the following receipts for 20x1:

Andy purchased a new vehicle to use for his employment at High Speed Bikes Inc. 12,000 of the 25,000 kms driven in 20x1 were for business purposes. The vehicle cost Andy $32,000 plus HST of 11%. Work-related interest payments on the car loan totaled $200 per month.

Andy purchased a new vehicle to use for his employment at High Speed Bikes Inc. 12,000 of the 25,000 kms driven in 20x1 were for business purposes. The vehicle cost Andy $32,000 plus HST of 11%. Work-related interest payments on the car loan totaled $200 per month.

Required:

Calculate Andy's employment income for 20x1 in accordance with Section 3 of the Income Tax Act. (Use tax rules for 2019.)

Andy provided you with the following receipts for 20x1:

Andy purchased a new vehicle to use for his employment at High Speed Bikes Inc. 12,000 of the 25,000 kms driven in 20x1 were for business purposes. The vehicle cost Andy $32,000 plus HST of 11%. Work-related interest payments on the car loan totaled $200 per month.Required:

Calculate Andy's employment income for 20x1 in accordance with Section 3 of the Income Tax Act. (Use tax rules for 2019.)

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/8

Play

Full screen (f)

Deck 4: Income From Employment

1

Sarah borrowed $25,000 from her employer at a rate of 1% interest. At the time the loan was made, CRA's prescribed rate of interest was 3%. Sarah is in a 40% income tax bracket. What is the actual cost (rate) of Sarah's loan? (Assume there are no fluctuations in the prescribed rate of interest.)

A) 1%

B) 1.2%

C) 1.8%

D) 2%

A) 1%

B) 1.2%

C) 1.8%

D) 2%

C

2

Kate Bell was employed by The Tea Shop Ltd. (a Canadian controlled private corporation) from January to December of 20x4. She earned a gross salary of $72,000.

The following were deducted from her pay during the year:

The following amounts were paid by The Tea Shop Ltd. in 20x4 on Kate's behalf:

Additional information:

On January 15, 20x2, Kate was given an option to purchase 500 shares of The Tea Shop for $5.00 per share. The market value of the shares on that date was $5.50. Kate exercised her option on June 1, 20x3 when the shares were valued at $7.00. She then sold the shares on March 17, 20x4 when the market value was $8.00 per share.

Kate pays $50 a month for her cell phone which she uses to keep in touch with friends and family. She also pays $80 a month to dry-clean her suits, and she purchases a new suit valued at $200 every three months. Kate purchased $300 worth of merchandise (at cost) from her employer during the year. The retail value of the merchandise was $500.

Kate contributed $1,000 to her RRSP during the year.

Required:

A) Calculate Kate's minimum net income for tax purposes for 20x4, in accordance with Section 3 of the Income Tax Act. Identify items that have been omitted in your calculations. (Kate minimizes her tax liability whenever possible.)

B) Will Kate be able to deduct the stock option deduction to arrive at her taxable income? Why or why not?

The following were deducted from her pay during the year:

The following amounts were paid by The Tea Shop Ltd. in 20x4 on Kate's behalf: Additional information:On January 15, 20x2, Kate was given an option to purchase 500 shares of The Tea Shop for $5.00 per share. The market value of the shares on that date was $5.50. Kate exercised her option on June 1, 20x3 when the shares were valued at $7.00. She then sold the shares on March 17, 20x4 when the market value was $8.00 per share.

Kate pays $50 a month for her cell phone which she uses to keep in touch with friends and family. She also pays $80 a month to dry-clean her suits, and she purchases a new suit valued at $200 every three months. Kate purchased $300 worth of merchandise (at cost) from her employer during the year. The retail value of the merchandise was $500.

Kate contributed $1,000 to her RRSP during the year.

Required:

A) Calculate Kate's minimum net income for tax purposes for 20x4, in accordance with Section 3 of the Income Tax Act. Identify items that have been omitted in your calculations. (Kate minimizes her tax liability whenever possible.)

B) Will Kate be able to deduct the stock option deduction to arrive at her taxable income? Why or why not?

Omitted items:

Omitted items:Employer's portion of CPP, EI

Income tax deducted

Employer's contribution to RPP - specifically exempt

Kate's CPP, EI - deduction not allowed, eligible for non-refundable tax credit

Cell phone, dry-cleaning, suits - not deductible - personal expenses

Merchandise at cost-tax-exempt benefit

B) The shares are from a Canadian controlled private corporation. Therefore, Kate either has to hold the shares for two years after acquisition, or the option price must be equal to or greater than the fair market value at the option date. Neither of these requirements has been met. Therefore, Kate will not be able to deduct the stock option deduction in arriving at her taxable income.

3

Andy worked for High Speed Bikes Inc. from March 1st to December 31st during 20x1. He earned a monthly base salary of $4,000, plus 1% commission on all of his sales. During 20x1, Andy's sales totaled $800,000. Andy was required by his employer to pay for his employment expenses. He traveled out of his city most days in order to sell to customers in surrounding towns. He received a monthly allowance of $500 to cover his traveling costs (which has been accurately recognized as 'unreasonable'). Andy and his employer each contributed $2,000 to the company's registered pension plan in 20x1.

Andy provided you with the following receipts for 20x1:

Andy purchased a new vehicle to use for his employment at High Speed Bikes Inc. 12,000 of the 25,000 kms driven in 20x1 were for business purposes. The vehicle cost Andy $32,000 plus HST of 11%. Work-related interest payments on the car loan totaled $200 per month.

Required:

Calculate Andy's employment income for 20x1 in accordance with Section 3 of the Income Tax Act. (Use tax rules for 2019.)

Andy provided you with the following receipts for 20x1:

Andy purchased a new vehicle to use for his employment at High Speed Bikes Inc. 12,000 of the 25,000 kms driven in 20x1 were for business purposes. The vehicle cost Andy $32,000 plus HST of 11%. Work-related interest payments on the car loan totaled $200 per month.Required:

Calculate Andy's employment income for 20x1 in accordance with Section 3 of the Income Tax Act. (Use tax rules for 2019.)

4

Cindy works for Sky Manufacturers Ltd., which is a public corporation. In 20x1 she was offered an option to purchase shares at $15 per share from her employer. The fair market value on that day was $17 per share. Cindy exercised her option in 20x3 and purchased 500 shares. The fair market value at that time was $21 per share. What is Cindy's tax treatment of this option on her 20x3 tax return?

A) $1,000 taxable benefit and no security option deduction

B) $1,000 taxable benefit and a 50% security option deduction

C) $3,000 taxable benefit and no security option deduction

D) $3,000 taxable benefit and a 50% security option deduction

A) $1,000 taxable benefit and no security option deduction

B) $1,000 taxable benefit and a 50% security option deduction

C) $3,000 taxable benefit and no security option deduction

D) $3,000 taxable benefit and a 50% security option deduction

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

5

Susan was provided with a company car to drive from March 1st to December 31st of the current year. The car cost the company $22,000, plus GST (5%) and PST (6%). Susan drove the car a total of 15,000 kilometres during the year. 11,000 kilometres were for business purposes and the other 4,000 kilometres were for personal use. Susan's employer paid for all of the vehicle's operating costs which totaled $1,100. What is the minimum amount that Susan will report in total taxable benefits as a result of the above information? (Round your answer to the nearest dollar, and apply tax rules for 2019.)

A) $1,172

B) $1,758

C) $2,212

D) $6,901

A) $1,172

B) $1,758

C) $2,212

D) $6,901

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following factors are used by the courts in order to determine a taxpayer's status as an employee or a self-employed contractor?

A) control test, ownership of tools test, chance of lawsuit, integration test

B) control test, employer test, chance of lawsuit, integration test

C) control test, ownership of tools test, chance of profit and loss, integration test

D) control test, employer test, chance of profit and loss, integration test

A) control test, ownership of tools test, chance of lawsuit, integration test

B) control test, employer test, chance of lawsuit, integration test

C) control test, ownership of tools test, chance of profit and loss, integration test

D) control test, employer test, chance of profit and loss, integration test

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following, when provided by an employer, is NOT a tax-deferred or tax-free benefit for the employee?

A) Premiums for private health care plans providing extended health coverage beyond a public plan

B) Counselling services to prepare the employee for retirement

C) Contributions to the employee's registered pension plan

D) A near-cash gift for the employee's wedding

A) Premiums for private health care plans providing extended health coverage beyond a public plan

B) Counselling services to prepare the employee for retirement

C) Contributions to the employee's registered pension plan

D) A near-cash gift for the employee's wedding

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

8

An individual has the option to receive a $1000 annual bonus and invest the after-tax amount for 25 years, or receive $1000 per annum in a registered pension plan for the next 25 years. Assuming a constant rate of return of 8% and a tax rate of 40%, what will be the total after-tax difference between the two plans? Show all calculations.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 8 flashcards in this deck.