Deck 10: Criticisms of Absorption Cost Systems:incentive to Overproduce

Full screen (f)

Question

Federal Mixing

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported Overhead is assigned to products using machine hours.

Overhead is assigned to products using machine hours.

?There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported

Overhead is assigned to products using machine hours.?There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Question

Navisky

Navisky designs, manufactures, and sells specialized GPS (Global Positioning System) devices for commercial applications. For example, Navisky currently sells a system for environmental studies and is planning systems for private aviation and fleet management. The firm has a design team that identifies potential commercial GPS applications, then designs and develops prototypes. Once a prototype is deemed successful and senior management determines that a market exists for the new application, the new design is put into production and the firm markets the new product through independent salespeople, direct marketing, trade shows, or whatever channel is most appropriate for that market.

?Currently, Navisky has one very successful system in production (for environmental studies) and several others in development. Navisky, located in Austria, is one of nine wholly owned subsidiaries of a large Swiss conglomerate. Andreas Hoffman, president of Navisky, expects to retire next year. He receives a fixed salary and a bonus based on reported accounting earnings. The bonus is 5 percent of earnings in excess of €850,000 for actual earnings between €850,000 and €1,400,000. If actual earnings exceed €1,400,000, the bonus is capped at €27,500 (5% × [€1,400,000 - €850,000]). (Earnings, both actual and target, are before taxes.)

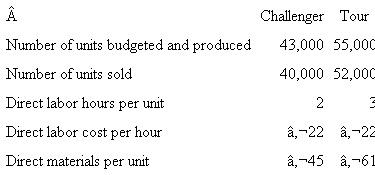

?The following data summarize Navisky's current operations (in euros).![Navisky Navisky designs, manufactures, and sells specialized GPS (Global Positioning System) devices for commercial applications. For example, Navisky currently sells a system for environmental studies and is planning systems for private aviation and fleet management. The firm has a design team that identifies potential commercial GPS applications, then designs and develops prototypes. Once a prototype is deemed successful and senior management determines that a market exists for the new application, the new design is put into production and the firm markets the new product through independent salespeople, direct marketing, trade shows, or whatever channel is most appropriate for that market. ?Currently, Navisky has one very successful system in production (for environmental studies) and several others in development. Navisky, located in Austria, is one of nine wholly owned subsidiaries of a large Swiss conglomerate. Andreas Hoffman, president of Navisky, expects to retire next year. He receives a fixed salary and a bonus based on reported accounting earnings. The bonus is 5 percent of earnings in excess of €850,000 for actual earnings between €850,000 and €1,400,000. If actual earnings exceed €1,400,000, the bonus is capped at €27,500 (5% × [€1,400,000 - €850,000]). (Earnings, both actual and target, are before taxes.) ?The following data summarize Navisky's current operations (in euros). ?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit. ?Navisky uses a traditional absorption costing system to absorb manufacturing overhead into product costs for inventory valuation and to calculate earnings for internal compensation purposes as well as external reporting. At the beginning of the current fiscal year, there was no beginning inventory of the environmental GPS devices. Required: a. How many units of the environmental GPS device would Mr. Hoffman like to see Navisky produce if he expects to sell 1,200 devices this year? b. Suppose Mr. Hoffman's bonus calculation was based on net income after including a charge for inventory holding costs at 20 percent of the ending inventory value. In other words, his bonus is 5 percent of net income in excess of €850,000 up to €1,400,000 where net income includes a 20 percent inventory holding cost. How many units of the environmental GPS device would Mr. Hoffman like to see produced if he expects to sell 1,200 devices this year? c. Explain why your answers in parts (b) and (c) differ, if they do. d. How many units of the environmental GPS device would Mr. Hoffman like to see produced assuming he expects to sell 1,200 devices this year if Navisky's net income is calculated using variable costing and net income includes a 20 percent inventory holding cost?<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_844b_050c_a8c8_93b54cb27f42_SM1503_00.jpg) ?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit.

?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit.

?Navisky uses a traditional absorption costing system to absorb manufacturing overhead into product costs for inventory valuation and to calculate earnings for internal compensation purposes as well as external reporting. At the beginning of the current fiscal year, there was no beginning inventory of the environmental GPS devices.

Required:

a. How many units of the environmental GPS device would Mr. Hoffman like to see Navisky produce if he expects to sell 1,200 devices this year?

b. Suppose Mr. Hoffman's bonus calculation was based on net income after including a charge for inventory holding costs at 20 percent of the ending inventory value. In other words, his bonus is 5 percent of net income in excess of €850,000 up to €1,400,000 where net income includes a 20 percent inventory holding cost. How many units of the environmental GPS device would Mr. Hoffman like to see produced if he expects to sell 1,200 devices this year?

c. Explain why your answers in parts (b) and (c) differ, if they do.

d. How many units of the environmental GPS device would Mr. Hoffman like to see produced assuming he expects to sell 1,200 devices this year if Navisky's net income is calculated using variable costing and net income includes a 20 percent inventory holding cost?

Navisky designs, manufactures, and sells specialized GPS (Global Positioning System) devices for commercial applications. For example, Navisky currently sells a system for environmental studies and is planning systems for private aviation and fleet management. The firm has a design team that identifies potential commercial GPS applications, then designs and develops prototypes. Once a prototype is deemed successful and senior management determines that a market exists for the new application, the new design is put into production and the firm markets the new product through independent salespeople, direct marketing, trade shows, or whatever channel is most appropriate for that market.

?Currently, Navisky has one very successful system in production (for environmental studies) and several others in development. Navisky, located in Austria, is one of nine wholly owned subsidiaries of a large Swiss conglomerate. Andreas Hoffman, president of Navisky, expects to retire next year. He receives a fixed salary and a bonus based on reported accounting earnings. The bonus is 5 percent of earnings in excess of €850,000 for actual earnings between €850,000 and €1,400,000. If actual earnings exceed €1,400,000, the bonus is capped at €27,500 (5% × [€1,400,000 - €850,000]). (Earnings, both actual and target, are before taxes.)

?The following data summarize Navisky's current operations (in euros).

?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit.?Navisky uses a traditional absorption costing system to absorb manufacturing overhead into product costs for inventory valuation and to calculate earnings for internal compensation purposes as well as external reporting. At the beginning of the current fiscal year, there was no beginning inventory of the environmental GPS devices.

Required:

a. How many units of the environmental GPS device would Mr. Hoffman like to see Navisky produce if he expects to sell 1,200 devices this year?

b. Suppose Mr. Hoffman's bonus calculation was based on net income after including a charge for inventory holding costs at 20 percent of the ending inventory value. In other words, his bonus is 5 percent of net income in excess of €850,000 up to €1,400,000 where net income includes a 20 percent inventory holding cost. How many units of the environmental GPS device would Mr. Hoffman like to see produced if he expects to sell 1,200 devices this year?

c. Explain why your answers in parts (b) and (c) differ, if they do.

d. How many units of the environmental GPS device would Mr. Hoffman like to see produced assuming he expects to sell 1,200 devices this year if Navisky's net income is calculated using variable costing and net income includes a 20 percent inventory holding cost?

Question

Joon

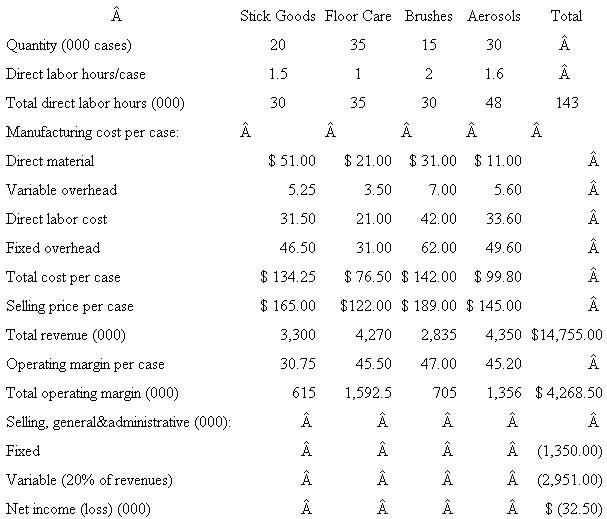

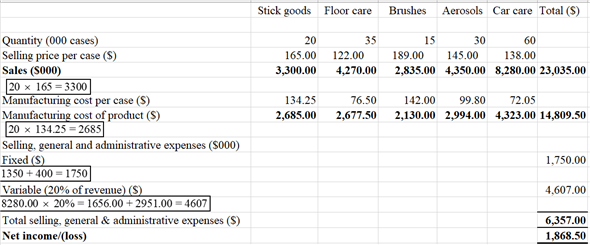

Joon manufactures and sells to retailers a variety of home care and personal care products. Joon has a single plant that produces all four of its product lines: Stick Goods (brooms and mops), Floor Care (strippers, soaps, and waxes), Brushes (hair brushes and shoe brushes), and Aerosols (room deodorizers, bug spray, furniture wax). The following statement summarizes Joon's financial performance for the most recent fiscal year. ?Direct labor costs $21 per hour. Fixed manufacturing overhead of $4.433 million is allocated to products based on direct labor hours. Last year, the fixed manufacturing overhead rate was $31 per direct labor hour ($4.433 million/143,000 direct labor hours). Variable manufacturing overhead is $3.50 per direct labor hour. Selling, general, and administrative (SG A) expenses consist of fixed costs ($1.35 million) and variable costs ($2,951 million). The variable SG A is 20 percent of revenues.

?Direct labor costs $21 per hour. Fixed manufacturing overhead of $4.433 million is allocated to products based on direct labor hours. Last year, the fixed manufacturing overhead rate was $31 per direct labor hour ($4.433 million/143,000 direct labor hours). Variable manufacturing overhead is $3.50 per direct labor hour. Selling, general, and administrative (SG A) expenses consist of fixed costs ($1.35 million) and variable costs ($2,951 million). The variable SG A is 20 percent of revenues.

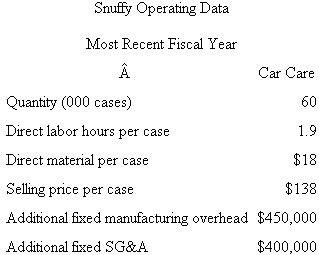

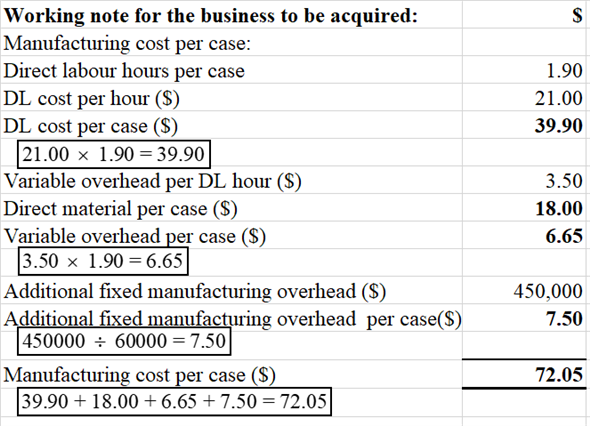

?The Joon plant has considerable excess capacity. Senior management has identified a potential acquisition target, Snuffy, that sells a line of automotive products (car waxes, soaps, brushes, and so forth) that are complementary to Joon's existing products and that can be manufactured in Joon's plant. Snuffy does not have any manufacturing facilities, but rather outsources the production of its products to contract manufacturers. Snuffy can be purchased for $38 million. The following table summarizes Snuffy's current operating data: Senior management argues that the reason Joon is currently losing money is that volumes have fallen in the plant and that the remaining products are having to carry an increasingly larger share of the overhead. This has caused some Joon product managers to raise prices. Senior managers realize that they must drive more volume into the plant if Joon is to return to profitability. Since organic growth (i.e., growth from existing products) is difficult due to a very competitive marketplace, management proposes to the board of directors the purchase of Snuffy as a way to drive additional volume into the plant. With volume of 60,000 cases and 1.9 direct labor hours per case, Snuffy's car care product line will add 114,000 direct labor hours to the plant and increase volume about 80 percent (114,000/143,000). This additional volume will significantly reduce the overhead the existing products must absorb and allow the product managers to lower prices. To incorporate Snuffy's manufacturing and distribution into Joon's current operations, Joon will have to incur additional fixed manufacturing overhead of $450,000 per year for new equipment, and $400,000 per year for additional SG A expenses.

Senior management argues that the reason Joon is currently losing money is that volumes have fallen in the plant and that the remaining products are having to carry an increasingly larger share of the overhead. This has caused some Joon product managers to raise prices. Senior managers realize that they must drive more volume into the plant if Joon is to return to profitability. Since organic growth (i.e., growth from existing products) is difficult due to a very competitive marketplace, management proposes to the board of directors the purchase of Snuffy as a way to drive additional volume into the plant. With volume of 60,000 cases and 1.9 direct labor hours per case, Snuffy's car care product line will add 114,000 direct labor hours to the plant and increase volume about 80 percent (114,000/143,000). This additional volume will significantly reduce the overhead the existing products must absorb and allow the product managers to lower prices. To incorporate Snuffy's manufacturing and distribution into Joon's current operations, Joon will have to incur additional fixed manufacturing overhead of $450,000 per year for new equipment, and $400,000 per year for additional SG A expenses.

Required:

a. Prepare a pro forma financial statement that shows Joon's financial performance (net income) for the most recent fiscal year assuming that Joon has already acquired Snuffy's car care products and has incorporated them into Joon's manufacturing and SG A processes. In preparing your analysis, make the following assumptions:

(i) Snuffy's products have the same fixed and variable cost structure as Joon's exisiting lines (i.e., variable overhead is $3.50 per direct labor hour and variable SG A is 20 percent of revenues).

(ii) The addition of Snuffy products does not change the demand for Joon's existing products.

(iii) There are no positive or negative externalities in manufacturing from having the additional Snuffy volume in the plant.

(iv) There is sufficient excess capacity in the plant and the local labor markets to absorb the additional Snuffy volume without causing labor rates or raw material prices to rise.

b. Based on your financial analysis in part ( a ), should Joon acquire Snuffy?

c. Evaluate management's arguments in favor of acquiring Snuffy.

d. What other advice would you offer Joon's management?

Joon manufactures and sells to retailers a variety of home care and personal care products. Joon has a single plant that produces all four of its product lines: Stick Goods (brooms and mops), Floor Care (strippers, soaps, and waxes), Brushes (hair brushes and shoe brushes), and Aerosols (room deodorizers, bug spray, furniture wax). The following statement summarizes Joon's financial performance for the most recent fiscal year.

?Direct labor costs $21 per hour. Fixed manufacturing overhead of $4.433 million is allocated to products based on direct labor hours. Last year, the fixed manufacturing overhead rate was $31 per direct labor hour ($4.433 million/143,000 direct labor hours). Variable manufacturing overhead is $3.50 per direct labor hour. Selling, general, and administrative (SG A) expenses consist of fixed costs ($1.35 million) and variable costs ($2,951 million). The variable SG A is 20 percent of revenues.?The Joon plant has considerable excess capacity. Senior management has identified a potential acquisition target, Snuffy, that sells a line of automotive products (car waxes, soaps, brushes, and so forth) that are complementary to Joon's existing products and that can be manufactured in Joon's plant. Snuffy does not have any manufacturing facilities, but rather outsources the production of its products to contract manufacturers. Snuffy can be purchased for $38 million. The following table summarizes Snuffy's current operating data:

Senior management argues that the reason Joon is currently losing money is that volumes have fallen in the plant and that the remaining products are having to carry an increasingly larger share of the overhead. This has caused some Joon product managers to raise prices. Senior managers realize that they must drive more volume into the plant if Joon is to return to profitability. Since organic growth (i.e., growth from existing products) is difficult due to a very competitive marketplace, management proposes to the board of directors the purchase of Snuffy as a way to drive additional volume into the plant. With volume of 60,000 cases and 1.9 direct labor hours per case, Snuffy's car care product line will add 114,000 direct labor hours to the plant and increase volume about 80 percent (114,000/143,000). This additional volume will significantly reduce the overhead the existing products must absorb and allow the product managers to lower prices. To incorporate Snuffy's manufacturing and distribution into Joon's current operations, Joon will have to incur additional fixed manufacturing overhead of $450,000 per year for new equipment, and $400,000 per year for additional SG A expenses.Required:

a. Prepare a pro forma financial statement that shows Joon's financial performance (net income) for the most recent fiscal year assuming that Joon has already acquired Snuffy's car care products and has incorporated them into Joon's manufacturing and SG A processes. In preparing your analysis, make the following assumptions:

(i) Snuffy's products have the same fixed and variable cost structure as Joon's exisiting lines (i.e., variable overhead is $3.50 per direct labor hour and variable SG A is 20 percent of revenues).

(ii) The addition of Snuffy products does not change the demand for Joon's existing products.

(iii) There are no positive or negative externalities in manufacturing from having the additional Snuffy volume in the plant.

(iv) There is sufficient excess capacity in the plant and the local labor markets to absorb the additional Snuffy volume without causing labor rates or raw material prices to rise.

b. Based on your financial analysis in part ( a ), should Joon acquire Snuffy?

c. Evaluate management's arguments in favor of acquiring Snuffy.

d. What other advice would you offer Joon's management?

Question

DIM

Diagnostic Imaging Medical (DIM) has introduced a revolutionary new magnetic resonance imaging (MRI) device that it sells to hospital radiology departments. Their new device has a much larger chamber that reduces patients' claustrophobic reactions compared to current machines. The following table displays how total cost per year varies with annual production. In other words, if DIM produces nine machines, the nine machines have a total manufacturing cost of $2.93 million.![DIM Diagnostic Imaging Medical (DIM) has introduced a revolutionary new magnetic resonance imaging (MRI) device that it sells to hospital radiology departments. Their new device has a much larger chamber that reduces patients' claustrophobic reactions compared to current machines. The following table displays how total cost per year varies with annual production. In other words, if DIM produces nine machines, the nine machines have a total manufacturing cost of $2.93 million. To simplify the analysis, assume DIM has no period costs, only the product costs in the above table. Management receives a bonus based on reported profits, where profits are calculated using absorption costing. Required: a. At a selling price of $500,000 per MRI, management expects to sell six units next year and plans to produce a few extra machines. The extra units are for training, marketing, and temporary spare parts in case an installed MRI fails and spare parts are needed. Management has financing and production capacity to vary production between 6 and 10 units. How many MRIs do you expect management to produce? Show your analysis that leads to this conclusion. b. Instead of expecting to sell six units at $500,000 each as in part ( a ), management expects to sell 11 units at $400,000 per unit. With expected sales at 11 units and a price of $400,000, DIM has the resources to produce between 11 and 15 MRIs. How many MRIs do you expect management to produce if expected sales are 11 units? Show your analysis that leads to this conclusion. c. Describe the differences and similarities in your answers to parts ( a ) and ( b ). Pay particular attention to the relation between units sold [6 in part ( a ) and 11 in part ( b )] and expected units produced, and how this relation differs or does not differ between parts ( a ) and ( b ). Also, explain what is causing your answers in parts ( a ) and ( b ) to differ or not differ. d. Provide some plausible explanations of why average costs may increase beyond a certain quantity of production.<div style=padding-top: 35px>](https://d2lvgg3v3hfg70.cloudfront.net/SM1503/11eb559c_8450_344b_a8c8_f9285f003a4e_SM1503_00.jpg) To simplify the analysis, assume DIM has no period costs, only the product costs in the above table. Management receives a bonus based on reported profits, where profits are calculated using absorption costing.

To simplify the analysis, assume DIM has no period costs, only the product costs in the above table. Management receives a bonus based on reported profits, where profits are calculated using absorption costing.

Required:

a. At a selling price of $500,000 per MRI, management expects to sell six units next year and plans to produce a few extra machines. The extra units are for training, marketing, and temporary spare parts in case an installed MRI fails and spare parts are needed. Management has financing and production capacity to vary production between 6 and 10 units. How many MRIs do you expect management to produce? Show your analysis that leads to this conclusion.

b. Instead of expecting to sell six units at $500,000 each as in part ( a ), management expects to sell 11 units at $400,000 per unit. With expected sales at 11 units and a price of $400,000, DIM has the resources to produce between 11 and 15 MRIs. How many MRIs do you expect management to produce if expected sales are 11 units? Show your analysis that leads to this conclusion.

c. Describe the differences and similarities in your answers to parts ( a ) and ( b ). Pay particular attention to the relation between units sold [6 in part ( a ) and 11 in part ( b )] and expected units produced, and how this relation differs or does not differ between parts ( a ) and ( b ). Also, explain what is causing your answers in parts ( a ) and ( b ) to differ or not differ.

d. Provide some plausible explanations of why average costs may increase beyond a certain quantity of production.

Diagnostic Imaging Medical (DIM) has introduced a revolutionary new magnetic resonance imaging (MRI) device that it sells to hospital radiology departments. Their new device has a much larger chamber that reduces patients' claustrophobic reactions compared to current machines. The following table displays how total cost per year varies with annual production. In other words, if DIM produces nine machines, the nine machines have a total manufacturing cost of $2.93 million.

To simplify the analysis, assume DIM has no period costs, only the product costs in the above table. Management receives a bonus based on reported profits, where profits are calculated using absorption costing.Required:

a. At a selling price of $500,000 per MRI, management expects to sell six units next year and plans to produce a few extra machines. The extra units are for training, marketing, and temporary spare parts in case an installed MRI fails and spare parts are needed. Management has financing and production capacity to vary production between 6 and 10 units. How many MRIs do you expect management to produce? Show your analysis that leads to this conclusion.

b. Instead of expecting to sell six units at $500,000 each as in part ( a ), management expects to sell 11 units at $400,000 per unit. With expected sales at 11 units and a price of $400,000, DIM has the resources to produce between 11 and 15 MRIs. How many MRIs do you expect management to produce if expected sales are 11 units? Show your analysis that leads to this conclusion.

c. Describe the differences and similarities in your answers to parts ( a ) and ( b ). Pay particular attention to the relation between units sold [6 in part ( a ) and 11 in part ( b )] and expected units produced, and how this relation differs or does not differ between parts ( a ) and ( b ). Also, explain what is causing your answers in parts ( a ) and ( b ) to differ or not differ.

d. Provide some plausible explanations of why average costs may increase beyond a certain quantity of production.

Question

Question

Easton Plant

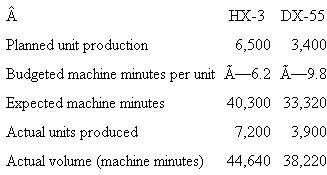

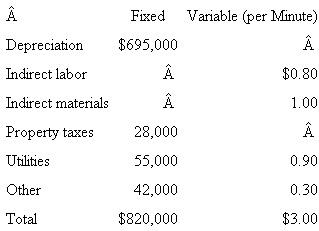

The Easton plant produces sheet metal chassis for television sets. Its customer is General Electric Appliances. The chassis are manufactured on a computerized, numerically controlled (NC) machine that cuts, drills, and bends the metal to form the chassis for the television set. Two different chassis are produced: HX?3 and DX?55.

?Easton has a single plant wide overhead account. Actual machine minutes on the NC machine are used to distribute overhead to the two products. There were no beginning inventories of work in process or finished goods. The following table summarizes the planned and actual production data for the year: The following data summarize the flexible overhead budget:

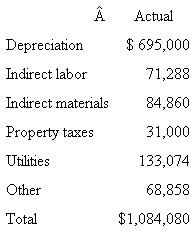

The following data summarize the flexible overhead budget:  At the end of the year, the following overhead amounts had been incurred:

At the end of the year, the following overhead amounts had been incurred:  Any over-or under absorbed overhead is written off to cost of goods sold. The ending finished goods inventory consists of 2,000 units of HX-3 and 1,000 units of DX-55, representing 13,400 minutes and 10,300 minutes of actual machine time, respectively.

Any over-or under absorbed overhead is written off to cost of goods sold. The ending finished goods inventory consists of 2,000 units of HX-3 and 1,000 units of DX-55, representing 13,400 minutes and 10,300 minutes of actual machine time, respectively.

Required: (Round all dollars, including overhead rates, to two decimal places.)

a. Calculate the overhead absorption rate set at the start of the year.

b. Calculate the over-or under absorbed overhead for the year.

c. The firm is considering switching to variable costing. What effect would this decision have on Easton's reported profit for this year? To implement variable costing at the end of the year, variable overhead is calculated as $3.00 per machine minute times the actual number of machine minutes. Fixed overhead is the difference between total actual overhead and variable overhead.

d. Instead of defining fixed overhead as all overhead in excess of variable overhead as in part ( c ) , assume the following: Fixed overhead is budgeted fixed overhead ($820,000), and variable overhead is the difference between total actual overhead and budgeted fixed overhead. What is the difference between absorption net income and variable costing income given these new assumptions?

The Easton plant produces sheet metal chassis for television sets. Its customer is General Electric Appliances. The chassis are manufactured on a computerized, numerically controlled (NC) machine that cuts, drills, and bends the metal to form the chassis for the television set. Two different chassis are produced: HX?3 and DX?55.

?Easton has a single plant wide overhead account. Actual machine minutes on the NC machine are used to distribute overhead to the two products. There were no beginning inventories of work in process or finished goods. The following table summarizes the planned and actual production data for the year:

The following data summarize the flexible overhead budget: At the end of the year, the following overhead amounts had been incurred: Any over-or under absorbed overhead is written off to cost of goods sold. The ending finished goods inventory consists of 2,000 units of HX-3 and 1,000 units of DX-55, representing 13,400 minutes and 10,300 minutes of actual machine time, respectively.Required: (Round all dollars, including overhead rates, to two decimal places.)

a. Calculate the overhead absorption rate set at the start of the year.

b. Calculate the over-or under absorbed overhead for the year.

c. The firm is considering switching to variable costing. What effect would this decision have on Easton's reported profit for this year? To implement variable costing at the end of the year, variable overhead is calculated as $3.00 per machine minute times the actual number of machine minutes. Fixed overhead is the difference between total actual overhead and variable overhead.

d. Instead of defining fixed overhead as all overhead in excess of variable overhead as in part ( c ) , assume the following: Fixed overhead is budgeted fixed overhead ($820,000), and variable overhead is the difference between total actual overhead and budgeted fixed overhead. What is the difference between absorption net income and variable costing income given these new assumptions?

Question

Question

Question

Question

Question

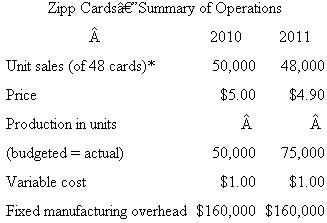

Zipp Cards

Zipp Cards buys baseball cards in bulk from the companies that produce them. Zipp buys sheets of 48 cards, then cuts the sheets into individual cards, and sorts and packages them, usually by team. Zipp then sells the packages to large discount stores. The accompanying table provides information regarding operations for 2010 and 2011. *One unit equals 48 cards.

*One unit equals 48 cards.

?Volume is measured in terms of 48-card sheets processed. Budgeted production and actual production in 2010 were both 50,000 units. There were no beginning inventories on January 1, 2010. In 2011, budgeted and actual production rose to 75,000 units.

?At the beginning of 2012, the president of Zipp was pleasantly surprised when the accountant showed her the income statement for the year 2011. The president remarked, "I'm surprised we made more money in 2011 than 2010. We had to cut prices and we didn't sell as many units, yet we still made more money. Well, you're the accountant and these numbers don't lie."

Required:

a. Prepare income statements for 2010 and 2011 using absorption costing.

b. Prepare a statement reconciling the change in net income from 2010 to 2011. Explain to the president why the firm made more money in 2011 than in 2010.

Zipp Cards buys baseball cards in bulk from the companies that produce them. Zipp buys sheets of 48 cards, then cuts the sheets into individual cards, and sorts and packages them, usually by team. Zipp then sells the packages to large discount stores. The accompanying table provides information regarding operations for 2010 and 2011.

*One unit equals 48 cards.?Volume is measured in terms of 48-card sheets processed. Budgeted production and actual production in 2010 were both 50,000 units. There were no beginning inventories on January 1, 2010. In 2011, budgeted and actual production rose to 75,000 units.

?At the beginning of 2012, the president of Zipp was pleasantly surprised when the accountant showed her the income statement for the year 2011. The president remarked, "I'm surprised we made more money in 2011 than 2010. We had to cut prices and we didn't sell as many units, yet we still made more money. Well, you're the accountant and these numbers don't lie."

Required:

a. Prepare income statements for 2010 and 2011 using absorption costing.

b. Prepare a statement reconciling the change in net income from 2010 to 2011. Explain to the president why the firm made more money in 2011 than in 2010.

Question

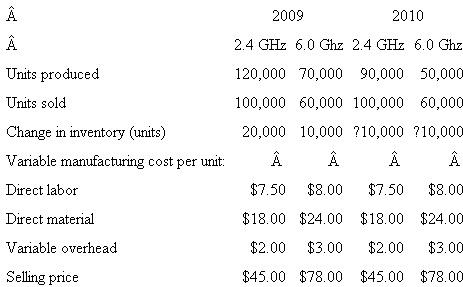

UniCom

UniCom produces a wide range of consumer electronics. UniCom's Newark, New York, plant produces two types of cordless phones: 2.4 GHz and 6.0 GHz. The following table summarizes operations at the Newark UniCom plant for the years 2009 and 2010. Fixed manufacturing overhead amounted to $4 million in each year. At the start of 2009, there were no beginning inventories of either 2.4-GHz or 6.0-GHz cordless phones. UniCom uses FIFO to value inventories.

Fixed manufacturing overhead amounted to $4 million in each year. At the start of 2009, there were no beginning inventories of either 2.4-GHz or 6.0-GHz cordless phones. UniCom uses FIFO to value inventories.

Required:

a. Prepare variable costing income statements for 2009 and 2010.

b. Prepare absorption costing income statements for 2009 and 2010. At the end of the year, fixed manufacturing overhead is absorbed to the two phone models using direct material as the allocation base.

c. Prepare a table that reconciles any differences in variable costing and absorption costing net incomes for 2009 and 2010.

UniCom produces a wide range of consumer electronics. UniCom's Newark, New York, plant produces two types of cordless phones: 2.4 GHz and 6.0 GHz. The following table summarizes operations at the Newark UniCom plant for the years 2009 and 2010.

Fixed manufacturing overhead amounted to $4 million in each year. At the start of 2009, there were no beginning inventories of either 2.4-GHz or 6.0-GHz cordless phones. UniCom uses FIFO to value inventories.Required:

a. Prepare variable costing income statements for 2009 and 2010.

b. Prepare absorption costing income statements for 2009 and 2010. At the end of the year, fixed manufacturing overhead is absorbed to the two phone models using direct material as the allocation base.

c. Prepare a table that reconciles any differences in variable costing and absorption costing net incomes for 2009 and 2010.

Question

Question

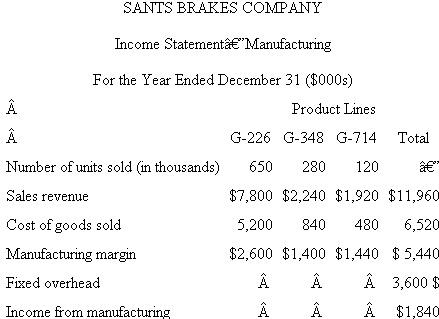

Sants Brakes Co.

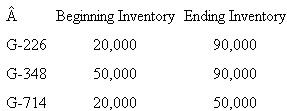

The current year's income statement for Sants Brakes Co. on a variable costing basis appears in the accompanying table. ?Inventories of finished stock were increased during the year in anticipation of increases in sales volume in the current year. Inventories in units of product for the beginning and end of the year follow.

?Inventories of finished stock were increased during the year in anticipation of increases in sales volume in the current year. Inventories in units of product for the beginning and end of the year follow.  ?The budgeted operating level for assigning fixed overhead to production is 1.8 million machine hours. One-half hour is required to produce a unit of G-226, two hours are required for a unit of G-348, and four hours are required for a unit of G-714.

?The budgeted operating level for assigning fixed overhead to production is 1.8 million machine hours. One-half hour is required to produce a unit of G-226, two hours are required for a unit of G-348, and four hours are required for a unit of G-714.

Required:

a. Recast the income statement on an absorption costing basis.

b. Explain why the income from manufacturing on the absorption costing statement differs from the income on the variable costing statement. Show your computations.

The current year's income statement for Sants Brakes Co. on a variable costing basis appears in the accompanying table.

?Inventories of finished stock were increased during the year in anticipation of increases in sales volume in the current year. Inventories in units of product for the beginning and end of the year follow. ?The budgeted operating level for assigning fixed overhead to production is 1.8 million machine hours. One-half hour is required to produce a unit of G-226, two hours are required for a unit of G-348, and four hours are required for a unit of G-714.Required:

a. Recast the income statement on an absorption costing basis.

b. Explain why the income from manufacturing on the absorption costing statement differs from the income on the variable costing statement. Show your computations.

Question

Question

Question

Aspen View

Aspen View produces a full line of sunglasses. This year it began producing a new model of sunglasses, the Peak 32. It produced 5,300 pairs and sold 4,900 pairs. The following table summarizes the fixed and variable costs of producing Peak 32 sunglasses. Aspen View uses variable costing to value its ending inventory. Required:

Required:

a. What is Aspen View's ending inventory value of Peak 32 sunglasses?

b. Aspen View is considering switching from variable costing to absorption costing. Would this year's net income from Peak 32 sunglasses be higher or lower using absorption costing? Explain why.

c. Suppose Aspen View uses absorption costing. If, instead of producing 5,300 pairs of Peak 32s it produced only 5,000, would net income from Peak 32 sunglasses be higher or lower from the smaller production compared to the larger production? Explain why.

d. Aspen View has an opportunity cost of capital of 20 percent. What is the cost of producing 5,300 pairs of Peak 32s instead of 4,900 pairs?

Aspen View produces a full line of sunglasses. This year it began producing a new model of sunglasses, the Peak 32. It produced 5,300 pairs and sold 4,900 pairs. The following table summarizes the fixed and variable costs of producing Peak 32 sunglasses. Aspen View uses variable costing to value its ending inventory.

Required: a. What is Aspen View's ending inventory value of Peak 32 sunglasses?

b. Aspen View is considering switching from variable costing to absorption costing. Would this year's net income from Peak 32 sunglasses be higher or lower using absorption costing? Explain why.

c. Suppose Aspen View uses absorption costing. If, instead of producing 5,300 pairs of Peak 32s it produced only 5,000, would net income from Peak 32 sunglasses be higher or lower from the smaller production compared to the larger production? Explain why.

d. Aspen View has an opportunity cost of capital of 20 percent. What is the cost of producing 5,300 pairs of Peak 32s instead of 4,900 pairs?

Question

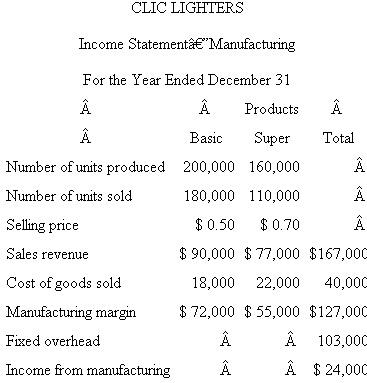

CLIC Lighters

CLIC manufactures two types of cigarette lighters: Basic and Super. A new plant began producing both lighter models this year. The following variable costing statement summarizes the first year of operations: ?For internal control purposes, variable costing is used. Management also wants income from manufacturing calculated using absorption costing. Fixed overhead is allocated to the two lighters using actual machine minutes. Each Basic lighter requires 1.1 machine minutes and each Super lighter requires 1.2 machine minutes.

?For internal control purposes, variable costing is used. Management also wants income from manufacturing calculated using absorption costing. Fixed overhead is allocated to the two lighters using actual machine minutes. Each Basic lighter requires 1.1 machine minutes and each Super lighter requires 1.2 machine minutes.

Required:

a. Calculate the fixed overhead rate per machine minute.

b. Calculate the plant's income from manufacturing for both Basic and Super lighters and for the entire plant using absorption costing.

c. Prepare a table that reconciles the difference in income from manufacturing reported using variable costing and absorption costing.

d. Explain in one or two sentences why income from manufacturing differs depending on whether variable costing or absorption costing is used.

CLIC manufactures two types of cigarette lighters: Basic and Super. A new plant began producing both lighter models this year. The following variable costing statement summarizes the first year of operations:

?For internal control purposes, variable costing is used. Management also wants income from manufacturing calculated using absorption costing. Fixed overhead is allocated to the two lighters using actual machine minutes. Each Basic lighter requires 1.1 machine minutes and each Super lighter requires 1.2 machine minutes.Required:

a. Calculate the fixed overhead rate per machine minute.

b. Calculate the plant's income from manufacturing for both Basic and Super lighters and for the entire plant using absorption costing.

c. Prepare a table that reconciles the difference in income from manufacturing reported using variable costing and absorption costing.

d. Explain in one or two sentences why income from manufacturing differs depending on whether variable costing or absorption costing is used.

Question

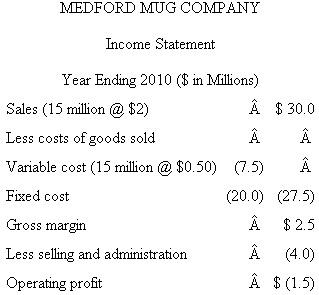

Medford Mug Company

The Medford Mug Company is an old-line maker of ceramic coffee mugs. It imprints company logos and other sayings on mugs for both commercial and wholesale markets. The firm has the capacity to produce 50 million mugs per year, but the recession has cut production and sales in the current year to 15 million mugs. The accompanying table shows the operating statement for 2010. At the end of 2010, there was no ending inventory of finished goods.

At the end of 2010, there was no ending inventory of finished goods.

?The board of directors is very concerned about the $1.5 million operating loss. It hires an outside consultant who reports back that the firm suffers from two problems. First, the president of the company receives a fixed salary, and since she owns no stock, she has very little incentive to worry about company profits. The second problem is that the company has not aggressively marketed its product and has not kept up with changing markets. The current president is 64 and the board of directors makes her an offer to retire one year early so that they can hire a new president to turn the firm around. The current president accepts the offer to retire and the board immediately hires a new president with a proven track record as a turnaround specialist.

?The new president is hired with an employment contract that pays a fixed wage of $50,000 a year plus 15 percent of the firm's operating profits (if any). Operating profits are calculated using absorption costing. In 2011, the new president doubles the selling and administration budget to $8 million (which includes the president's salary of $50,000). He designs a new line of "politically correct" sayings to imprint on the mugs and expands inventory and the number of distributors handling the mugs. Production is increased to 45 million mugs and sales climb to 18 million mugs at $2 each. Variable costs per mug remain at $.50 and fixed costs at $20 million in 2011.

?At the end of 2011, the president meets with the board of directors and announces he has accepted another job. He believes he has successfully gotten Medford Mug back on track and thanks the board for giving him the opportunity. His new job is helping to turn around another struggling company.

Required:

a. Calculate the president's bonus for 2011.

b. Evaluate the performance of the new president in 2011. Did he do as good a job as the numbers in ( a ) suggest?

The Medford Mug Company is an old-line maker of ceramic coffee mugs. It imprints company logos and other sayings on mugs for both commercial and wholesale markets. The firm has the capacity to produce 50 million mugs per year, but the recession has cut production and sales in the current year to 15 million mugs. The accompanying table shows the operating statement for 2010.

At the end of 2010, there was no ending inventory of finished goods.?The board of directors is very concerned about the $1.5 million operating loss. It hires an outside consultant who reports back that the firm suffers from two problems. First, the president of the company receives a fixed salary, and since she owns no stock, she has very little incentive to worry about company profits. The second problem is that the company has not aggressively marketed its product and has not kept up with changing markets. The current president is 64 and the board of directors makes her an offer to retire one year early so that they can hire a new president to turn the firm around. The current president accepts the offer to retire and the board immediately hires a new president with a proven track record as a turnaround specialist.

?The new president is hired with an employment contract that pays a fixed wage of $50,000 a year plus 15 percent of the firm's operating profits (if any). Operating profits are calculated using absorption costing. In 2011, the new president doubles the selling and administration budget to $8 million (which includes the president's salary of $50,000). He designs a new line of "politically correct" sayings to imprint on the mugs and expands inventory and the number of distributors handling the mugs. Production is increased to 45 million mugs and sales climb to 18 million mugs at $2 each. Variable costs per mug remain at $.50 and fixed costs at $20 million in 2011.

?At the end of 2011, the president meets with the board of directors and announces he has accepted another job. He believes he has successfully gotten Medford Mug back on track and thanks the board for giving him the opportunity. His new job is helping to turn around another struggling company.

Required:

a. Calculate the president's bonus for 2011.

b. Evaluate the performance of the new president in 2011. Did he do as good a job as the numbers in ( a ) suggest?

Question

Kothari Inc.

The telecom division of Kothari Inc. produces and sells 100,000 line modulators. Half of the modulators are sold externally at $150 per unit, and the other half are sold internally at variable manufacturing costs plus 10 percent. Kothari uses variable costing to evaluate the telecom division. The following summarizes the cost structure of the telecom division. Required:

Required:

a. Calculate the net income of the telecom division (before taxes) using variable costing.

b. Telecom can outsource the final assembly of all 100,000 modulators for $9.00 per modulator. If it does this, it can reduce variable manufacturing cost by $1.00 per unit and fixed manufacturing overhead by $700,000. If the managers of the telecom unit are compensated based on telecom's net income before taxes, do you expect them to outsource the final assembly of the modulators? Show calculations.

c. What happens to the net cash flows of Kothari Inc. if the final assembly of the modulators is outsourced?

The telecom division of Kothari Inc. produces and sells 100,000 line modulators. Half of the modulators are sold externally at $150 per unit, and the other half are sold internally at variable manufacturing costs plus 10 percent. Kothari uses variable costing to evaluate the telecom division. The following summarizes the cost structure of the telecom division.

Required: a. Calculate the net income of the telecom division (before taxes) using variable costing.

b. Telecom can outsource the final assembly of all 100,000 modulators for $9.00 per modulator. If it does this, it can reduce variable manufacturing cost by $1.00 per unit and fixed manufacturing overhead by $700,000. If the managers of the telecom unit are compensated based on telecom's net income before taxes, do you expect them to outsource the final assembly of the modulators? Show calculations.

c. What happens to the net cash flows of Kothari Inc. if the final assembly of the modulators is outsourced?

Question

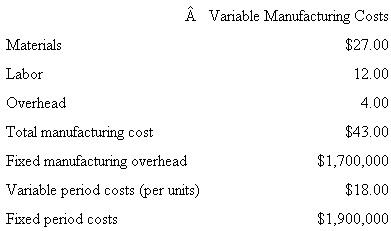

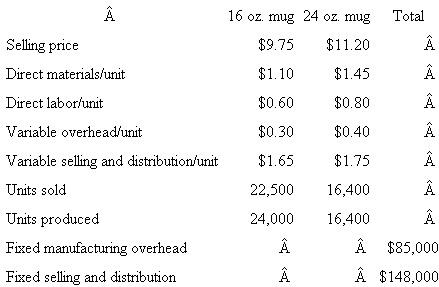

Mystic Mugs

Sanjog and Rajiv Gupta have started a business that manufactures and sells thermal mugs. Users personalize the mugs by plugging them into a laptop and downloading their favorite images from a digital camera. The company makes two mug sizes: 16 and 24 ounce mugs. This is its first year of business. The following data summarize operations for the first year. There were no beginning inventories. Overhead is assigned to products using direct labor dollars.

There were no beginning inventories. Overhead is assigned to products using direct labor dollars.

Required:

a. Calculate Mystic Mugs's net income before taxes using absorption costing.

b. Calculate Mystic Mugs's net income before taxes using variable costing.

c. Prepare a table that reconciles any difference between the two net income figures calculated in parts ( a ) and ( b ).

d. Write a short memo explaining in lay terms any difference between the two net income figures calculated in parts ( a ) and ( b ).

Sanjog and Rajiv Gupta have started a business that manufactures and sells thermal mugs. Users personalize the mugs by plugging them into a laptop and downloading their favorite images from a digital camera. The company makes two mug sizes: 16 and 24 ounce mugs. This is its first year of business. The following data summarize operations for the first year.

There were no beginning inventories. Overhead is assigned to products using direct labor dollars.Required:

a. Calculate Mystic Mugs's net income before taxes using absorption costing.

b. Calculate Mystic Mugs's net income before taxes using variable costing.

c. Prepare a table that reconciles any difference between the two net income figures calculated in parts ( a ) and ( b ).

d. Write a short memo explaining in lay terms any difference between the two net income figures calculated in parts ( a ) and ( b ).

Question

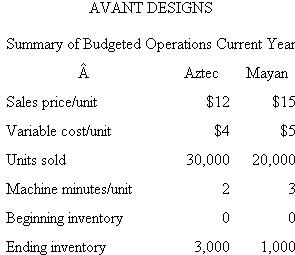

Avant Designs

Avant Designs designs and manufactures polished-nickel fashion bracelets. It offers two bracelets: Aztec and Mayan. The following data summarize budgeted operations for the current year: Budgeted fixed manufacturing overhead for the year was $258,000.

Budgeted fixed manufacturing overhead for the year was $258,000.

Required:

a. Prepare the budgeted income statement for the year using variable costing.

b. Prepare the budgeted income statement for the year using absorption costing. Budgeted fixed manufacturing overhead is allocated to the two bracelets using machine minutes.

c. Explain the difference in the two net income figures computed in parts ( a ) and ( b ). That is, reconcile any difference in earnings and explain why it occurs.

Avant Designs designs and manufactures polished-nickel fashion bracelets. It offers two bracelets: Aztec and Mayan. The following data summarize budgeted operations for the current year:

Budgeted fixed manufacturing overhead for the year was $258,000.Required:

a. Prepare the budgeted income statement for the year using variable costing.

b. Prepare the budgeted income statement for the year using absorption costing. Budgeted fixed manufacturing overhead is allocated to the two bracelets using machine minutes.

c. Explain the difference in the two net income figures computed in parts ( a ) and ( b ). That is, reconcile any difference in earnings and explain why it occurs.

Question

Taylor Chains

Taylor designs and manufactures high-performance bicycle chains for professional racers and serious amateurs. Two new titanium chain sets, the Challenger and the Tour, sell for €110 and €155, respectively. The following data summarize the cost structure for the two chain sets: ?Taylor uses an absorption costing system. Overhead is applied to these two products based on direct labor hours using a flexible budget to calculate the overhead rate before production begins for the year. Taylor budgeted (and produced) 43,000 Challenger chains and 55,000 Tour chains. Fixed manufacturing overhead was estimated to be €1.65 million and variable manufacturing overhead was estimated to be €1.75 per direct labor hour. Actual overhead incurred amounted to €2.1 million. Any over-or under absorbed overhead is written off to cost of goods sold.

?Taylor uses an absorption costing system. Overhead is applied to these two products based on direct labor hours using a flexible budget to calculate the overhead rate before production begins for the year. Taylor budgeted (and produced) 43,000 Challenger chains and 55,000 Tour chains. Fixed manufacturing overhead was estimated to be €1.65 million and variable manufacturing overhead was estimated to be €1.75 per direct labor hour. Actual overhead incurred amounted to €2.1 million. Any over-or under absorbed overhead is written off to cost of goods sold.

Required:

a. Calculate the overhead rate Taylor used to absorb overhead to the chains.

b. Using the predetermined overhead rate you calculated in ( a ), and assuming any over-or under absorbed overhead is written off to cost of goods sold, calculate Taylor Chains' net income before taxes for both the Challenger and Tour chains and for the entire firm.

c. Instead of using absorption costing, use variable costing to calculate Taylor Chains' net income before taxes for both the Challenger and Tour chains and for the entire firm. Assume that any over-or under absorbed overhead is treated as a fixed cost and is written off to cost of goods sold.

d. Explain why the net income numbers calculated in parts ( b ) and ( c ) differ and reconcile the difference numerically.

e. Suppose that next year Taylor incurs total manufacturing overhead of €2.3 million and sells all the chains it produces next year as well as the 6,000 chains it had in inventory from the first year of production. How much manufacturing overhead will appear on Taylor's income statement if the company uses (i) absorption costing or (ii) variable costing?

Taylor designs and manufactures high-performance bicycle chains for professional racers and serious amateurs. Two new titanium chain sets, the Challenger and the Tour, sell for €110 and €155, respectively. The following data summarize the cost structure for the two chain sets:

?Taylor uses an absorption costing system. Overhead is applied to these two products based on direct labor hours using a flexible budget to calculate the overhead rate before production begins for the year. Taylor budgeted (and produced) 43,000 Challenger chains and 55,000 Tour chains. Fixed manufacturing overhead was estimated to be €1.65 million and variable manufacturing overhead was estimated to be €1.75 per direct labor hour. Actual overhead incurred amounted to €2.1 million. Any over-or under absorbed overhead is written off to cost of goods sold.Required:

a. Calculate the overhead rate Taylor used to absorb overhead to the chains.

b. Using the predetermined overhead rate you calculated in ( a ), and assuming any over-or under absorbed overhead is written off to cost of goods sold, calculate Taylor Chains' net income before taxes for both the Challenger and Tour chains and for the entire firm.

c. Instead of using absorption costing, use variable costing to calculate Taylor Chains' net income before taxes for both the Challenger and Tour chains and for the entire firm. Assume that any over-or under absorbed overhead is treated as a fixed cost and is written off to cost of goods sold.

d. Explain why the net income numbers calculated in parts ( b ) and ( c ) differ and reconcile the difference numerically.

e. Suppose that next year Taylor incurs total manufacturing overhead of €2.3 million and sells all the chains it produces next year as well as the 6,000 chains it had in inventory from the first year of production. How much manufacturing overhead will appear on Taylor's income statement if the company uses (i) absorption costing or (ii) variable costing?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/23

Play

Full screen (f)

Deck 10: Criticisms of Absorption Cost Systems:incentive to Overproduce

1

Federal Mixing

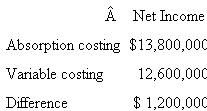

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported Overhead is assigned to products using machine hours.

?There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Federal Mixing (FM) is a division of Federal Chemicals, a large diversified chemical company. FM provides mixing services for both outside customers and other Federal divisions. FM buys or receives liquid chemicals and combines and packages them according to the customer's specifications. FM computes its divisional net income on both a fully absorbed and variable costing basis. For the year just ending, it reported

Overhead is assigned to products using machine hours.?There is no finished goods inventory at FM, only work-in-process (WIP) inventory. As soon as a product is completed, it is shipped to the customer. The beginning inventory was valued at $6.3 million and contained 70,000 machine hours. The ending WIP inventory was valued at $9.9 million and contained 90,000 machine hours.

Required:

Write a short nontechnical note to senior management explaining why variable costing and absorption costing net income amounts differ.

Absorption vs. Variable Costing

In the field of bookkeeping, variable costing (direct costing) and ingestion costing (full costing) are two distinct strategies for applying creation expenses to items or administrations. The distinction between the two techniques is in the treatment of settled assembling overhead expenses.

Under the immediate costing technique, settled assembling overhead expenses are expensed amid the period in which they are acquired. Under the full costing technique, settled assembling overhead expenses are expensed when the item is sold.

Variable costing discounts to pay all settled assembling costs acquired amid the year. Ingestion costing customizes the settled overheads between units in stock and units sold in view of machine hours.

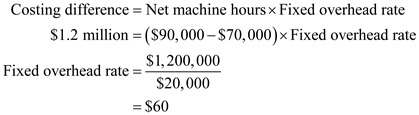

Ingestion costing net pay is higher than under factor costing of $1.2 million. This implies inventories under ingestion costing are higher by $1.2 million.

The closing work-in-process stock includes 20,000 more machine hours than the opening stock . From the information given, the settled overhead rate connected to items is $60 per machine hour.

. From the information given, the settled overhead rate connected to items is $60 per machine hour.

Compute the fixed overhead rate with the help of formula shown below: Thus, the overhead rate comes out to be

Thus, the overhead rate comes out to be  .

.

In the field of bookkeeping, variable costing (direct costing) and ingestion costing (full costing) are two distinct strategies for applying creation expenses to items or administrations. The distinction between the two techniques is in the treatment of settled assembling overhead expenses.

Under the immediate costing technique, settled assembling overhead expenses are expensed amid the period in which they are acquired. Under the full costing technique, settled assembling overhead expenses are expensed when the item is sold.

Variable costing discounts to pay all settled assembling costs acquired amid the year. Ingestion costing customizes the settled overheads between units in stock and units sold in view of machine hours.

Ingestion costing net pay is higher than under factor costing of $1.2 million. This implies inventories under ingestion costing are higher by $1.2 million.

The closing work-in-process stock includes 20,000 more machine hours than the opening stock

. From the information given, the settled overhead rate connected to items is $60 per machine hour. Compute the fixed overhead rate with the help of formula shown below:

Thus, the overhead rate comes out to be . 2

Navisky

Navisky designs, manufactures, and sells specialized GPS (Global Positioning System) devices for commercial applications. For example, Navisky currently sells a system for environmental studies and is planning systems for private aviation and fleet management. The firm has a design team that identifies potential commercial GPS applications, then designs and develops prototypes. Once a prototype is deemed successful and senior management determines that a market exists for the new application, the new design is put into production and the firm markets the new product through independent salespeople, direct marketing, trade shows, or whatever channel is most appropriate for that market.

?Currently, Navisky has one very successful system in production (for environmental studies) and several others in development. Navisky, located in Austria, is one of nine wholly owned subsidiaries of a large Swiss conglomerate. Andreas Hoffman, president of Navisky, expects to retire next year. He receives a fixed salary and a bonus based on reported accounting earnings. The bonus is 5 percent of earnings in excess of €850,000 for actual earnings between €850,000 and €1,400,000. If actual earnings exceed €1,400,000, the bonus is capped at €27,500 (5% × [€1,400,000 - €850,000]). (Earnings, both actual and target, are before taxes.)

?The following data summarize Navisky's current operations (in euros). ?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit.

?Navisky uses a traditional absorption costing system to absorb manufacturing overhead into product costs for inventory valuation and to calculate earnings for internal compensation purposes as well as external reporting. At the beginning of the current fiscal year, there was no beginning inventory of the environmental GPS devices.

Required:

a. How many units of the environmental GPS device would Mr. Hoffman like to see Navisky produce if he expects to sell 1,200 devices this year?

b. Suppose Mr. Hoffman's bonus calculation was based on net income after including a charge for inventory holding costs at 20 percent of the ending inventory value. In other words, his bonus is 5 percent of net income in excess of €850,000 up to €1,400,000 where net income includes a 20 percent inventory holding cost. How many units of the environmental GPS device would Mr. Hoffman like to see produced if he expects to sell 1,200 devices this year?

c. Explain why your answers in parts (b) and (c) differ, if they do.

d. How many units of the environmental GPS device would Mr. Hoffman like to see produced assuming he expects to sell 1,200 devices this year if Navisky's net income is calculated using variable costing and net income includes a 20 percent inventory holding cost?

Navisky designs, manufactures, and sells specialized GPS (Global Positioning System) devices for commercial applications. For example, Navisky currently sells a system for environmental studies and is planning systems for private aviation and fleet management. The firm has a design team that identifies potential commercial GPS applications, then designs and develops prototypes. Once a prototype is deemed successful and senior management determines that a market exists for the new application, the new design is put into production and the firm markets the new product through independent salespeople, direct marketing, trade shows, or whatever channel is most appropriate for that market.

?Currently, Navisky has one very successful system in production (for environmental studies) and several others in development. Navisky, located in Austria, is one of nine wholly owned subsidiaries of a large Swiss conglomerate. Andreas Hoffman, president of Navisky, expects to retire next year. He receives a fixed salary and a bonus based on reported accounting earnings. The bonus is 5 percent of earnings in excess of €850,000 for actual earnings between €850,000 and €1,400,000. If actual earnings exceed €1,400,000, the bonus is capped at €27,500 (5% × [€1,400,000 - €850,000]). (Earnings, both actual and target, are before taxes.)

?The following data summarize Navisky's current operations (in euros).

?Senior management at Navisky, including Mr. Hoffman, expects to sell about 1,200 units of the environmental GPS device this year. However, they have considerable discretion in setting production levels. Their plant has excess capacity and can produce up to 1,500 environmental devices without seeing any increase in the variable manufacturing costs per unit.?Navisky uses a traditional absorption costing system to absorb manufacturing overhead into product costs for inventory valuation and to calculate earnings for internal compensation purposes as well as external reporting. At the beginning of the current fiscal year, there was no beginning inventory of the environmental GPS devices.

Required:

a. How many units of the environmental GPS device would Mr. Hoffman like to see Navisky produce if he expects to sell 1,200 devices this year?

b. Suppose Mr. Hoffman's bonus calculation was based on net income after including a charge for inventory holding costs at 20 percent of the ending inventory value. In other words, his bonus is 5 percent of net income in excess of €850,000 up to €1,400,000 where net income includes a 20 percent inventory holding cost. How many units of the environmental GPS device would Mr. Hoffman like to see produced if he expects to sell 1,200 devices this year?

c. Explain why your answers in parts (b) and (c) differ, if they do.

d. How many units of the environmental GPS device would Mr. Hoffman like to see produced assuming he expects to sell 1,200 devices this year if Navisky's net income is calculated using variable costing and net income includes a 20 percent inventory holding cost?

Variable Costing

To take into account lacks in retention costing information, key fund experts will regularly create supplemental information in view of variable costing systems. As its name recommends, just factor generation costs are allotted to stock and cost of products sold. These expenses by and large comprised of direct materials, coordinate work, and variable assembling overhead.

Settled assembling costs are viewed as period costs alongside SG A costs. In some ways, this downplays the genuine cost of creation. The settled assembling overhead will be brought about regardless of what amount is delivered.

Over the long haul, a business must recoup those expenses to survive. In any case, on a case-by-case premise, incorporating settled assembling overhead in an item cost investigation can result in some wrong choices.

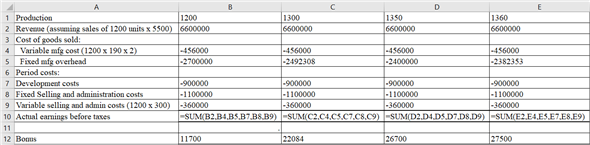

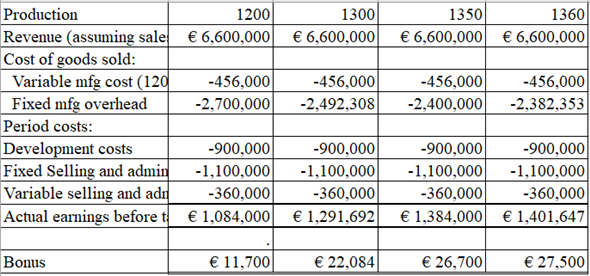

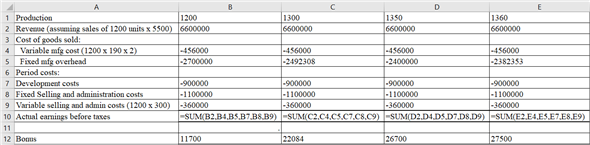

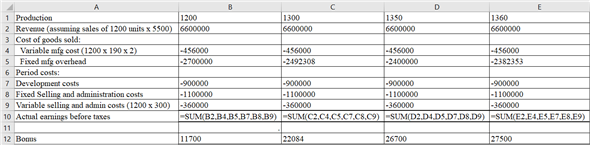

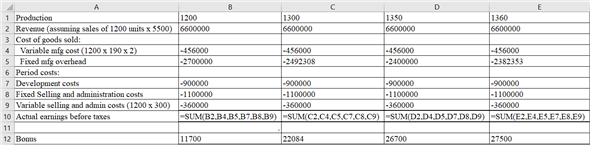

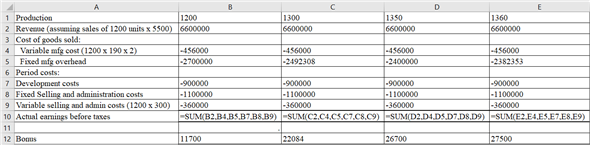

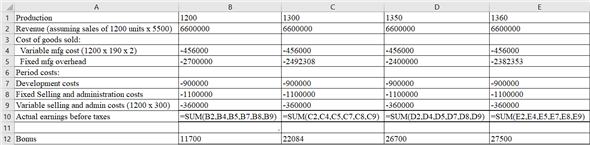

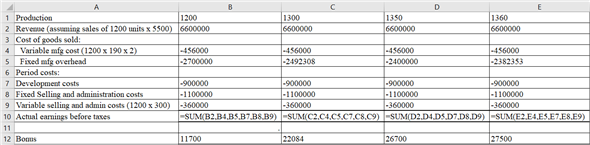

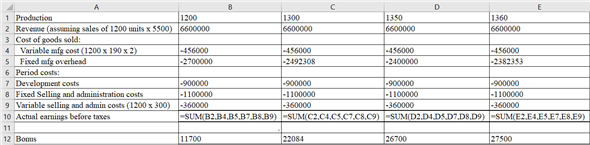

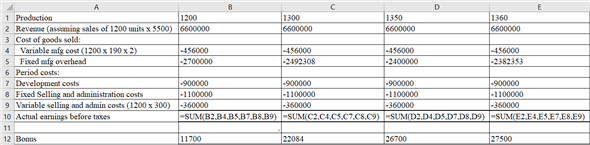

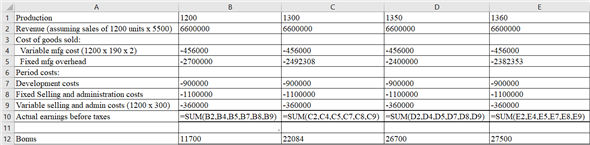

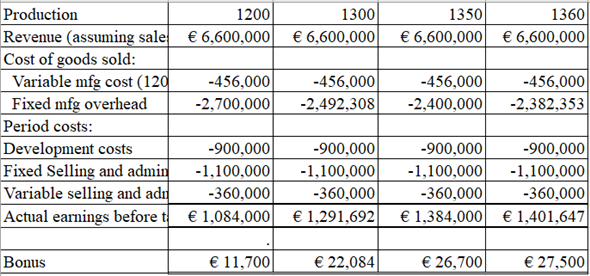

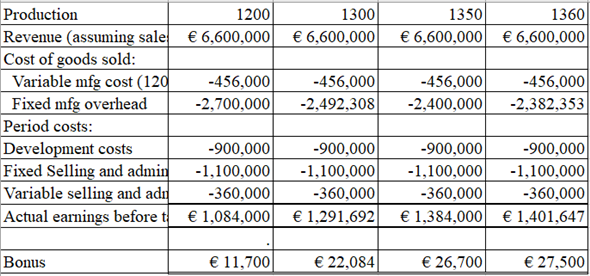

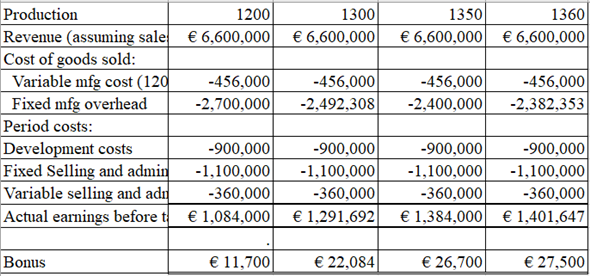

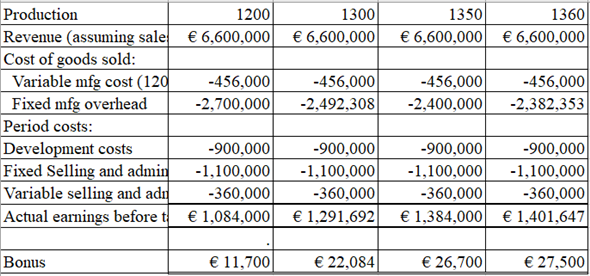

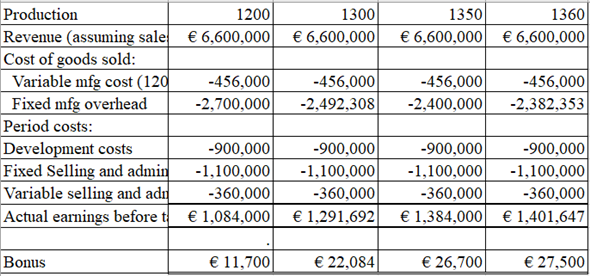

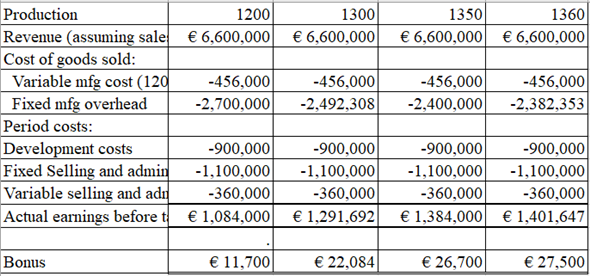

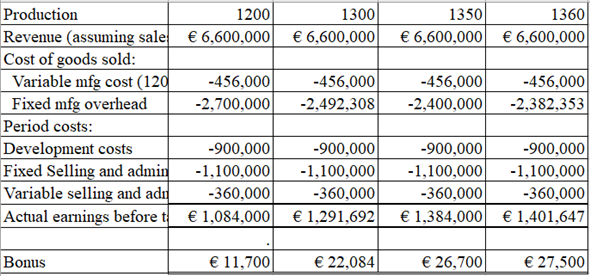

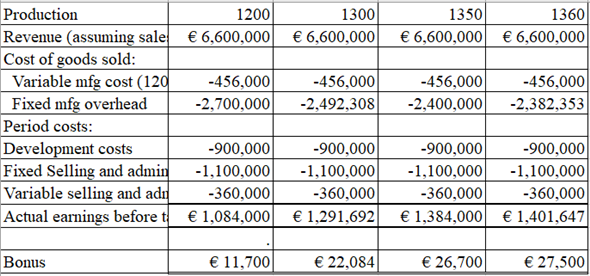

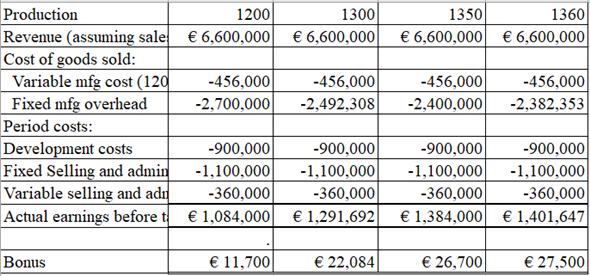

a.Mr. H, since he wants to leave one year from now and hereafter won't have to deal with any plenitude stock, has a propelling power to over convey. The table underneath demonstrates that given offers of 1200 units Mr. H should need to convey around 1,360 units.

At 1,360 units, expected benefit are about €1,401,647, or basically finished the reward best of €1,400,000. So to grow his reward, Mr. H should make 1,360 units or 160 more than he would like to offer. The result of the above MS-Excel has been shown below:

The result of the above MS-Excel has been shown below:  Working Note:

Working Note:

Compute the bonus for 1200 units using the equation as follows: Thus, the bonus for 1200 units to be

Thus, the bonus for 1200 units to be  .

.

Compute the bonus for 1300 units as follows: Thus, the bonus for 1300 units to be

Thus, the bonus for 1300 units to be  .

.

Compute the bonus for 1350 units as follows: Thus, the bonus for 1350 units to be

Thus, the bonus for 1350 units to be  .

.

Compute the bonus for 1360 units as follows: Thus, the bonus for 1360 units to be

Thus, the bonus for 1360 units to be  0

0

.

b.With a stock holding cost of 20 percent deducted from profit, Mr. H will want to create 1,420 units on the grounds that at this generation level (and given offers of 1,200 units) Mr. H will achieve the reward top of €27,500. 1

1

The result of the above MS-Excel has been shown below: 2

2

Working Note:

Compute the bonus for 1200 units as follows: 3

3

Thus, the bonus for 1200 units to be 4

4

.

Compute the bonus for 1350 units as follows: 5

5

Thus, the bonus for 1350 units to be 6

6

.

Compute the bonus for 1400 units as follows: 7

7

Thus, the bonus for 1400 units to be 8

8

.

Compute the bonus for 1420 units as follows: 9

9

Thus, the bonus for 1420 units to be 0

0

.

c.Strikingly, charging Mr. H a stock holding expense of 20 percent really makes him over deliver significantly more. Without the 20 percent stock charge Mr. H just needs to deliver around 1,360 units (or 160 more than he hopes to offer) to come to the €1.4 million income top. In any case, with the 20 percent stock charge,

Mr. H needs to deliver around 1,420 (or 220 more than he hopes to offer) to achieve the top. Henceforth, including the stock holding charge has the unreasonable motivator of really causing Mr. H to over to create significantly more. The explanation behind this is the presence of the reward top and the way that the 20 percent charge on the stock is not as much as the decrease in normal settled costs charged to cost of merchandise sold.

d.Under factor costing and a 20 percent stock holding cost, Mr. H won't over deliver. He will deliver precisely what he means to offer, 1,200 gadgets. In the event that he over produces under factor costing, income falls, and consequently, his reward is lower. 1

1

The result of the above MS-Excel has been shown below: 2

2

Working Note:

Compute the bonus for 1200 units as follows: 3

3

Thus, the bonus for 1200 units to be 4

4

.

Compute the bonus for 1350 units as follows: 5

5

Thus, the bonus for 1350 units to be 6

6

.

Compute the bonus for 1390 units as follows: 7

7

Thus, the bonus for 1390 units to be 8

8

.

Compute the bonus for 1400 units as follows: 9

9

Thus, the bonus for 1400 units to be 0

0

.

To take into account lacks in retention costing information, key fund experts will regularly create supplemental information in view of variable costing systems. As its name recommends, just factor generation costs are allotted to stock and cost of products sold. These expenses by and large comprised of direct materials, coordinate work, and variable assembling overhead.

Settled assembling costs are viewed as period costs alongside SG A costs. In some ways, this downplays the genuine cost of creation. The settled assembling overhead will be brought about regardless of what amount is delivered.

Over the long haul, a business must recoup those expenses to survive. In any case, on a case-by-case premise, incorporating settled assembling overhead in an item cost investigation can result in some wrong choices.

a.Mr. H, since he wants to leave one year from now and hereafter won't have to deal with any plenitude stock, has a propelling power to over convey. The table underneath demonstrates that given offers of 1200 units Mr. H should need to convey around 1,360 units.

At 1,360 units, expected benefit are about €1,401,647, or basically finished the reward best of €1,400,000. So to grow his reward, Mr. H should make 1,360 units or 160 more than he would like to offer.

The result of the above MS-Excel has been shown below: Working Note: Compute the bonus for 1200 units using the equation as follows:

Thus, the bonus for 1200 units to be .Compute the bonus for 1300 units as follows:

Thus, the bonus for 1300 units to be .Compute the bonus for 1350 units as follows:

Thus, the bonus for 1350 units to be .Compute the bonus for 1360 units as follows:

Thus, the bonus for 1360 units to be 0.

b.With a stock holding cost of 20 percent deducted from profit, Mr. H will want to create 1,420 units on the grounds that at this generation level (and given offers of 1,200 units) Mr. H will achieve the reward top of €27,500.

1The result of the above MS-Excel has been shown below:

2Working Note:

Compute the bonus for 1200 units as follows:

3Thus, the bonus for 1200 units to be

4.

Compute the bonus for 1350 units as follows:

5Thus, the bonus for 1350 units to be

6.

Compute the bonus for 1400 units as follows:

7Thus, the bonus for 1400 units to be

8.

Compute the bonus for 1420 units as follows:

9Thus, the bonus for 1420 units to be

0.

c.Strikingly, charging Mr. H a stock holding expense of 20 percent really makes him over deliver significantly more. Without the 20 percent stock charge Mr. H just needs to deliver around 1,360 units (or 160 more than he hopes to offer) to come to the €1.4 million income top. In any case, with the 20 percent stock charge,

Mr. H needs to deliver around 1,420 (or 220 more than he hopes to offer) to achieve the top. Henceforth, including the stock holding charge has the unreasonable motivator of really causing Mr. H to over to create significantly more. The explanation behind this is the presence of the reward top and the way that the 20 percent charge on the stock is not as much as the decrease in normal settled costs charged to cost of merchandise sold.

d.Under factor costing and a 20 percent stock holding cost, Mr. H won't over deliver. He will deliver precisely what he means to offer, 1,200 gadgets. In the event that he over produces under factor costing, income falls, and consequently, his reward is lower.

1The result of the above MS-Excel has been shown below:

2Working Note:

Compute the bonus for 1200 units as follows:

3Thus, the bonus for 1200 units to be

4.

Compute the bonus for 1350 units as follows:

5Thus, the bonus for 1350 units to be

6.

Compute the bonus for 1390 units as follows:

7Thus, the bonus for 1390 units to be

8.

Compute the bonus for 1400 units as follows:

9Thus, the bonus for 1400 units to be

0.

3

Joon

Joon manufactures and sells to retailers a variety of home care and personal care products. Joon has a single plant that produces all four of its product lines: Stick Goods (brooms and mops), Floor Care (strippers, soaps, and waxes), Brushes (hair brushes and shoe brushes), and Aerosols (room deodorizers, bug spray, furniture wax). The following statement summarizes Joon's financial performance for the most recent fiscal year. ?Direct labor costs $21 per hour. Fixed manufacturing overhead of $4.433 million is allocated to products based on direct labor hours. Last year, the fixed manufacturing overhead rate was $31 per direct labor hour ($4.433 million/143,000 direct labor hours). Variable manufacturing overhead is $3.50 per direct labor hour. Selling, general, and administrative (SG A) expenses consist of fixed costs ($1.35 million) and variable costs ($2,951 million). The variable SG A is 20 percent of revenues.