Deck 12: Options

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

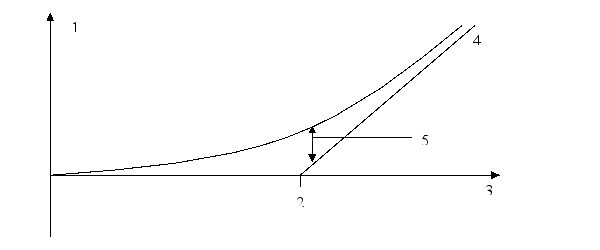

The following depicts the value of a call option.Match the descriptions in the Legend with the correct numbers on the graph.

Legend:

Time Value

Underlying asset price

Strike price

Intrinsic value of a call

Payoff/profit/option value

A)1, 2, 3, 4, 5 respectively

B)5, 3, 2, 4, 1 respectively

C)4, 1, 2, 5, 3 respectively

D)5, 1, 2, 4, 3 respectively

Legend:

Time Value

Underlying asset price

Strike price

Intrinsic value of a call

Payoff/profit/option value

A)1, 2, 3, 4, 5 respectively

B)5, 3, 2, 4, 1 respectively

C)4, 1, 2, 5, 3 respectively

D)5, 1, 2, 4, 3 respectively

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

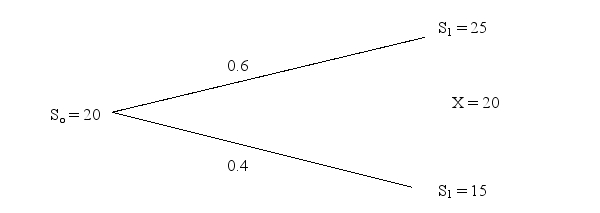

Francis has a long position on the underlying asset and has sold a number of call options with the following binomial tree:

Given the current asset price is $20 and r is 5%, what is the price of the this call option?

A)$2.86

B)$0.60

C)$21.43

D)−$21.43

Given the current asset price is $20 and r is 5%, what is the price of the this call option?

A)$2.86

B)$0.60

C)$21.43

D)−$21.43

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/55

Play

Full screen (f)

Deck 12: Options

1

The difference between the intrinsic value of an option and its actual value is:

A)the payoff

B)the premium

C)the time value

D)the underlying asset cost

A)the payoff

B)the premium

C)the time value

D)the underlying asset cost

the time value

2

Use the following statements to answer the following question:

I.A call option provides insurance against the decrease of the stock price below the strike price.

II.The buyer of a call option pays a premium regardless of the underlying asset price.

A)I and II are correct

B)I is correct and II is incorrect

C)I is incorrect and II is correct

D)I and II are incorrect

I.A call option provides insurance against the decrease of the stock price below the strike price.

II.The buyer of a call option pays a premium regardless of the underlying asset price.

A)I and II are correct

B)I is correct and II is incorrect

C)I is incorrect and II is correct

D)I and II are incorrect

I is incorrect and II is correct

3

Which of the following types of option is more valuable?

A)American put option

B)European put option

C)Need additional information

D)Neither one

A)American put option

B)European put option

C)Need additional information

D)Neither one

American put option

4

Which of the following investors would be happy to see a stock price sharply increase?

A)An investor who bought a call option.

B)An investor who bought a put option.

C)An investor who bought the stock and has sold a call option.

D)An investor who has sold a call option.

A)An investor who bought a call option.

B)An investor who bought a put option.

C)An investor who bought the stock and has sold a call option.

D)An investor who has sold a call option.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

5

What is a short position?

A)Position taken by the person who sells an option.

B)Position taken by the person who buys an option.

C)Buy a call and buy a put.

D)Sell a call and buy a put.

A)Position taken by the person who sells an option.

B)Position taken by the person who buys an option.

C)Buy a call and buy a put.

D)Sell a call and buy a put.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements is NOT true?

A)An increase in interest rates decreases the value of a call option.

B)An increase in volatility increases the value of a call option.

C)A decrease in volatility decreases the value of a put option.

D)An increase in the underlying asset's price decreases the value of a put.

A)An increase in interest rates decreases the value of a call option.

B)An increase in volatility increases the value of a call option.

C)A decrease in volatility decreases the value of a put option.

D)An increase in the underlying asset's price decreases the value of a put.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

7

The following depicts the value of a call option.Match the descriptions in the Legend with the correct numbers on the graph.

Legend:

Time Value

Underlying asset price

Strike price

Intrinsic value of a call

Payoff/profit/option value

A)1, 2, 3, 4, 5 respectively

B)5, 3, 2, 4, 1 respectively

C)4, 1, 2, 5, 3 respectively

D)5, 1, 2, 4, 3 respectively

Legend:

Time Value

Underlying asset price

Strike price

Intrinsic value of a call

Payoff/profit/option value

A)1, 2, 3, 4, 5 respectively

B)5, 3, 2, 4, 1 respectively

C)4, 1, 2, 5, 3 respectively

D)5, 1, 2, 4, 3 respectively

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

8

If an investor is trying to cancel their short position in a call option, they should:

A)buy the underlying asset.

B)sell the underlying asset.

C)buy the call option.

D)sell the call option.

A)buy the underlying asset.

B)sell the underlying asset.

C)buy the call option.

D)sell the call option.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

9

The time value on call option A is $5 and the option premium is $8.What is the intrinsic value of call option A?

A)$40

B)$13

C)−$3

D)$3

A)$40

B)$13

C)−$3

D)$3

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is true?

A)An increase in interest rates increases the value of a put option.

B)An increase in volatility increases the value of a put option.

C)A decrease in volatility increases the value of a put option.

D)A decrease in the underlying asset's price decreases the value of a put.

A)An increase in interest rates increases the value of a put option.

B)An increase in volatility increases the value of a put option.

C)A decrease in volatility increases the value of a put option.

D)A decrease in the underlying asset's price decreases the value of a put.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

11

The strike price on a call option is $8 and the price of the underlying stock is $10.What is the time value of money of the call option if the option premium is $3?

A)$4

B)$3

C)−$2

D)$1

A)$4

B)$3

C)−$2

D)$1

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following is the higher priced call option?

A)Higher ST, higher X, increased volatility

B)Higher ST, higher X, decreased volatility

C)Higher ST, lower X, increased volatility

D)Lower ST, higher X, decreased volatility

A)Higher ST, higher X, increased volatility

B)Higher ST, higher X, decreased volatility

C)Higher ST, lower X, increased volatility

D)Lower ST, higher X, decreased volatility

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

13

The strike price of an option is:

A)the value of the underlying asset at expiration.

B)the price of the option.

C)the proceeds generated if today was the expiration day.

D)the price at which an investor can buy or sell the underlying asset.

A)the value of the underlying asset at expiration.

B)the price of the option.

C)the proceeds generated if today was the expiration day.

D)the price at which an investor can buy or sell the underlying asset.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

14

A call option is:

A)the right to buy an underlying asset at a fixed price for a specified time.

B)the right to sell an underlying asset at a fixed price for a specified time.

C)a price established today for future delivery.

D)a standardized exchange-traded contract in which the seller agrees to deliver a commodity to the buyer at some point in the future.

A)the right to buy an underlying asset at a fixed price for a specified time.

B)the right to sell an underlying asset at a fixed price for a specified time.

C)a price established today for future delivery.

D)a standardized exchange-traded contract in which the seller agrees to deliver a commodity to the buyer at some point in the future.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

15

The intrinsic value of an in-the-money put option is:

A)X−ST

B)ST −X

C)X−ST+P

D)0

A)X−ST

B)ST −X

C)X−ST+P

D)0

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

16

Jay writes a call option with a strike price of $50.What will Jay's payoff be if the underlying asset price at expiration is $55?

A)$5

B)−$5

C)0

D)$105

A)$5

B)−$5

C)0

D)$105

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

17

Holding a put option and a call option on the same underlying asset, with the same strike price, and maturity has payoffs equivalent to:

A)holding a stock today

B)holding a stock in the future

C)holding a call option

D)none of the above

A)holding a stock today

B)holding a stock in the future

C)holding a call option

D)none of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following factors increases the price of a put option?

A)Higher asset price, higher strike price, increased volatility, increased dividends

B)Higher strike price, longer time to expiration, increased volatility, increased dividends

C)Higher strike price, longer time to expiration, increased volatility, increased interest rates

D)Longer time to expiration, increased volatility, decreasing interest rates, decreasing dividends

A)Higher asset price, higher strike price, increased volatility, increased dividends

B)Higher strike price, longer time to expiration, increased volatility, increased dividends

C)Higher strike price, longer time to expiration, increased volatility, increased interest rates

D)Longer time to expiration, increased volatility, decreasing interest rates, decreasing dividends

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

19

An option that can be exercised only at maturity is referred to as:

A)a European option

B)a call option

C)a protective put

D)an American option

A)a European option

B)a call option

C)a protective put

D)an American option

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

20

An option can be:

I.in the money

II.out of the money

III.at the money

IV.shallow

A)I, II, III, IV

B)I, II, III only

C)I, II only

D)I only

I.in the money

II.out of the money

III.at the money

IV.shallow

A)I, II, III, IV

B)I, II, III only

C)I, II only

D)I only

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

21

The standard Black-Scholes option pricing model applies to:

A)European call options on non-dividend paying stocks.

B)American call options on non-dividend paying stocks.

C)European call options on all stocks.

D)American call options on all stocks.

A)European call options on non-dividend paying stocks.

B)American call options on non-dividend paying stocks.

C)European call options on all stocks.

D)American call options on all stocks.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

22

Montreal Smoked Meat Ltd.(MSM)shares are currently selling for $55 per hsare.The 2-year put option on MSM shares has the following characteristics: strike price = $50, price = $0.25

Given that the risk-free rate is 2%, what is the price of a 2-year call option on MSM shares with an exercise price of $50?

A)$5.25

B)$7.19

C)$6.23

D)$0

Given that the risk-free rate is 2%, what is the price of a 2-year call option on MSM shares with an exercise price of $50?

A)$5.25

B)$7.19

C)$6.23

D)$0

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

23

Put-call parity is based on which one of the following principles?

A)Binomial tree

B)Time value of money

C)No arbitrage

D)Normality of returns

A)Binomial tree

B)Time value of money

C)No arbitrage

D)Normality of returns

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

24

When can put-call parity be applied?

I.Call and put have the same strike price

II.Call and put have the same time to expiration and are held until expiration

III.Call and put are created using the same underlying asset

IV.Call and put have the same premium

A)Only I is required

B)Only I and II are required

C)Only I, II, and III are required

D)I, II, III, and IV are required

I.Call and put have the same strike price

II.Call and put have the same time to expiration and are held until expiration

III.Call and put are created using the same underlying asset

IV.Call and put have the same premium

A)Only I is required

B)Only I and II are required

C)Only I, II, and III are required

D)I, II, III, and IV are required

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following best defines a covered call?

A)Purchasing a put option to protect a long position in an underlying asset.

B)Position between the floor and ceiling price.

C)The right, but not an obligation, to sell an underlying asset at a fixed price for a specified time.

D)Selling call options while owning the underlying asset

A)Purchasing a put option to protect a long position in an underlying asset.

B)Position between the floor and ceiling price.

C)The right, but not an obligation, to sell an underlying asset at a fixed price for a specified time.

D)Selling call options while owning the underlying asset

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

26

Using the following information, find the price of the put option:

Stock price St=$55, interest rate I=5%,

Strike price X=$53, Call premium=$3, Maturity: T=3 months

A)$0.47

B)$0.62

C)$3.47

D)$0.35

Stock price St=$55, interest rate I=5%,

Strike price X=$53, Call premium=$3, Maturity: T=3 months

A)$0.47

B)$0.62

C)$3.47

D)$0.35

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

27

Put-call parity has the following conditions:

I.both the call and the put have the same exercise price

II.both the call and the put are purchased at the same time

III.both the call and the put have the same expiration dates

IV.both are assumed to be European options

A)I, II, III only

B)I, III, IV only

C)I, II, IV only

D)II, III, IV only

I.both the call and the put have the same exercise price

II.both the call and the put are purchased at the same time

III.both the call and the put have the same expiration dates

IV.both are assumed to be European options

A)I, II, III only

B)I, III, IV only

C)I, II, IV only

D)II, III, IV only

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

28

Using the following information, find the price of the call option:

Stock price St=$ 55, Interest rate I=5%,

Strike price X=$ 52, Put premium=$ 1, Maturity: T=3 months

A)$6.47

B)$0.62

C)$8.47

D)$4.64

Stock price St=$ 55, Interest rate I=5%,

Strike price X=$ 52, Put premium=$ 1, Maturity: T=3 months

A)$6.47

B)$0.62

C)$8.47

D)$4.64

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following best defines implied volatility?

A)An estimate of the price volatility of an option.

B)The observed relationship of past and present option prices.

C)An estimate of the price volatility of the underlying asset based on observed option prices.

D)The observed relationship of past and present price volatility of the underlying asset.

A)An estimate of the price volatility of an option.

B)The observed relationship of past and present option prices.

C)An estimate of the price volatility of the underlying asset based on observed option prices.

D)The observed relationship of past and present price volatility of the underlying asset.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

30

Given the following information and based on the Black-Scholes option pricing model, calculate the price of the corresponding call option (round to 2 decimal places).

current stock price = $50

strike price = $50

risk-free rate = 10%

time to expiration of the option = 3 months

N(d1)= 0.5793

N(d2)= 0.4602

A)$0

B)$5.49

C)$5.96

D)$6.52

current stock price = $50

strike price = $50

risk-free rate = 10%

time to expiration of the option = 3 months

N(d1)= 0.5793

N(d2)= 0.4602

A)$0

B)$5.49

C)$5.96

D)$6.52

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the "Greeks" values measures the change in option value with a change in volatility of the underlying asset?

A)Delta

B)Theta

C)Gamma

D)Vega

A)Delta

B)Theta

C)Gamma

D)Vega

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

32

Min has created the following portfolio:

bought a share for $20

bought 3 puts, strike price $18

maturity 1year

Suppose at expiration ST is $17.What is the payoff of her strategy?

A)$0

B)$3

C)−$2

D)−$3

bought a share for $20

bought 3 puts, strike price $18

maturity 1year

Suppose at expiration ST is $17.What is the payoff of her strategy?

A)$0

B)$3

C)−$2

D)−$3

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

33

The Black-Scholes model includes the following components:

I.the standard deviation of the underlying asset

II.present value of the strike price

III.current value of the underlying asset

IV.cumulative standard normal density functions

A)I only

B)I, II only

C)I, II, III only

D)I, II, III, IV

I.the standard deviation of the underlying asset

II.present value of the strike price

III.current value of the underlying asset

IV.cumulative standard normal density functions

A)I only

B)I, II only

C)I, II, III only

D)I, II, III, IV

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

34

The standard Black-Scholes option pricing model assumes:

A)European call options.

B)continuous compounding.

C)non continuous volatility of the underlying stock price

D)all of the above.

E)a and b

A)European call options.

B)continuous compounding.

C)non continuous volatility of the underlying stock price

D)all of the above.

E)a and b

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following describes a covered call writing?

A)buying call options while owning the underlying asset.

B)buying put options while owning the underlying asset.

C)selling call options while owning the underlying asset.

D)selling put options while owning the underlying asset.

A)buying call options while owning the underlying asset.

B)buying put options while owning the underlying asset.

C)selling call options while owning the underlying asset.

D)selling put options while owning the underlying asset.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following statements to answer the question:

I.VIX is a measure of volatility in the financial markets

II.VIX is calculated as the aggregate volatility of option prices.

A)I and II are correct

B)I and II are incorrect

C)I is correct and II is incorrect

D)I is incorrect and II is correct

I.VIX is a measure of volatility in the financial markets

II.VIX is calculated as the aggregate volatility of option prices.

A)I and II are correct

B)I and II are incorrect

C)I is correct and II is incorrect

D)I is incorrect and II is correct

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

37

____________is the relationship between the price of a call option and a put option.

A)The binomial option pricing model

B)The Black-Scholes option pricing model

C)Put-call parity

D)A swap

A)The binomial option pricing model

B)The Black-Scholes option pricing model

C)Put-call parity

D)A swap

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

38

The basic put-call parity can be rearranged as:

A)P - S = C + PV(X)

B)C + P = S - PV(X)

C)C = P +S -PV(X)

D)P = C + S + PV(X)

A)P - S = C + PV(X)

B)C + P = S - PV(X)

C)C = P +S -PV(X)

D)P = C + S + PV(X)

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following strategies does NOT require the investor to long a put?

A)Collar

B)Covered call

C)Synthetic call and synthetic put

D)Protective put

A)Collar

B)Covered call

C)Synthetic call and synthetic put

D)Protective put

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

40

Given the following information and based on the Black-Scholes option pricing model, calculate the price of the corresponding call option (round to 2 decimal places).

current asset price = $50

strike price = $50

risk-free rate = 1%

time to expiration of the option = 2 years

N(d1)= 0.5793

N(d2)= 0.4602

A)$0

B)$5.49

C)$5.96

D)$6.41

current asset price = $50

strike price = $50

risk-free rate = 1%

time to expiration of the option = 2 years

N(d1)= 0.5793

N(d2)= 0.4602

A)$0

B)$5.49

C)$5.96

D)$6.41

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

41

Higher _________, higher ________

A)price volatility; estimated volatility

B)implied volatility; option price

C)estimated volatility; price volatility

D)implied volatility; price volatility

A)price volatility; estimated volatility

B)implied volatility; option price

C)estimated volatility; price volatility

D)implied volatility; price volatility

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

42

Francis has a long position on the underlying asset and has sold a number of call options with the following binomial tree:

Given the current asset price is $20 and r is 5%, what is the price of the this call option?

A)$2.86

B)$0.60

C)$21.43

D)−$21.43

Given the current asset price is $20 and r is 5%, what is the price of the this call option?

A)$2.86

B)$0.60

C)$21.43

D)−$21.43

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

43

The current value of an underlying asset is $80.The strike price of a call option with one month to expiration is $85.There is a 20% chance that in one month the value of the underlying asset will be $75 and an 80% chance that it will be $90.

a)What is the expected value of the underlying asset and the corresponding rate of return?

b)What is the hedge ratio and the corresponding value of the call given r = 0.02%?

a)What is the expected value of the underlying asset and the corresponding rate of return?

b)What is the hedge ratio and the corresponding value of the call given r = 0.02%?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

44

The current stock price is $568.36, a one-year call option with a strike price of $500 is $102, and the risk-free rate is 2%.What should be the price of a one-year put option with the same strike price?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

45

Create a table illustrating the range of payoffs of a protective put strategy for the following values of an underlying asset: 60, 70, 80, 90, 100.The strike price of all options in the strategy is $80 and the current value of the underlying asset is $80.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

46

Toronto Skaters' stock is now worth $100.In one month, it will either be $80 or $120.Given that the monthly risk-free rate is 2%, what is the corresponding value of the call? (Assume a strike price $105)

A)$13.28

B)$21.57

C)$10.78

D)$43.14

A)$13.28

B)$21.57

C)$10.78

D)$43.14

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

47

Toronto Skaters' stock is now worth $100.In one month, it will either be $80 or $120.Given that the monthly risk-free rate is 2%, how many calls does the investor need to sell to hedge a long position in Toronto Skaters' stock? (Assume a strike price of $105)

A)0.5

B)1.0

C)2.0

D)2.67

A)0.5

B)1.0

C)2.0

D)2.67

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

48

Assume the current value of the underlying asset is $20 and the value of the underlying asset tomorrow can either be $15 or $25.What is the risk-neutral probability of generating a 2% return on the asset?

A)0.54

B)−1.46

C)0.135

D)0.9

A)0.54

B)−1.46

C)0.135

D)0.9

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

49

Briefly explain how to replicate the payoff of a risk-free asset using put-call parity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

50

_________is an estimate of the ________ of the underlying asset based on observed option prices.

A)Price volatility; estimated volatility

B)Implied volatility; price volatility

C)Price volatility; implied volatility

D)Estimated volatility; price volatility

A)Price volatility; estimated volatility

B)Implied volatility; price volatility

C)Price volatility; implied volatility

D)Estimated volatility; price volatility

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

51

VIX can be used

A)to price interest rate volatility.

B)to measure the volatility of the underlying stock price based on the observed option prices.

C)to estimate the risk of default premium of the underlying debt.

D)none of the above.

A)to price interest rate volatility.

B)to measure the volatility of the underlying stock price based on the observed option prices.

C)to estimate the risk of default premium of the underlying debt.

D)none of the above.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

52

Marie wants to determine the fair value of a put option with a strike price of $20 due to expire in 2 years.A call with the same strike price and expiration is worth $5.The risk-free rate is 4%.What would you tell Marie is the fair value of the put option? Assume: continuous compounding and value of the underlying asset is $22

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

53

You have been provided with the following information:

S = $25

Exercise price = $20

Risk-free rate = 1%

Volatility is 20%

The option expires in one year.

Based on this information, what is the value of the corresponding call option?

(NOTE: if using the appendix A-1 to solve for the N(d1)and N(d2)values you should truncate d1 and d2 to two decimal places and round down.

S = $25

Exercise price = $20

Risk-free rate = 1%

Volatility is 20%

The option expires in one year.

Based on this information, what is the value of the corresponding call option?

(NOTE: if using the appendix A-1 to solve for the N(d1)and N(d2)values you should truncate d1 and d2 to two decimal places and round down.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

54

Create a table depicting the payoffs for a collar given Xput = $50, S = $55, and Xcall = $60.Assume the value of the asset in 2 months will be: $40, $50, $55, $60, $75, $80.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following statements is correct?

A)Risk neutral refers to the state of ignoring the risk involved in determining expected rates of return.

B)Risk neutral pricing uses the cost of capital to discount the future cash flows of the option.

C)Risk-neutral pricing ignores the probability of state in pricing the option.

D)b and c

A)Risk neutral refers to the state of ignoring the risk involved in determining expected rates of return.

B)Risk neutral pricing uses the cost of capital to discount the future cash flows of the option.

C)Risk-neutral pricing ignores the probability of state in pricing the option.

D)b and c

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 55 flashcards in this deck.