Deck 5: Accounting for Other Governmental Fund Types: Capital Projects, Debt Service, and Permanent

Full screen (f)

Question

Question

Question

Question

The citizens of Spencer County approved the issuance of $2,000,000 in 6 percent general obligation bonds to finance the construction of a courthouse annex. A capital projects fund was established for that purpose. The preclosing trial balance of the courthouse annex capital project fund follows:

a. Prepare any closing entries necessary at year-end.

a. Prepare any closing entries necessary at year-end.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the courthouse annex capital project fund.

c. Prepare a balance sheet for the Courthouse Annex Capital Project Fund, assuming all unexpended resources are restricted to construction of the courthouse annex.

a. Prepare any closing entries necessary at year-end.b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the courthouse annex capital project fund.

c. Prepare a balance sheet for the Courthouse Annex Capital Project Fund, assuming all unexpended resources are restricted to construction of the courthouse annex.

Question

A citizen group raised funds to establish an endowment for the Eastville City Library. Under the terms of the trust agreement, the principal must be maintained, but the earnings of the fund are to be used to purchase database and periodical subscriptions for the library. A preclosing trial balance of the library permanent fund follows:

a. Prepare any closing entries necessary at year-end.

a. Prepare any closing entries necessary at year-end.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the library permanent fund.

c. Prepare a balance sheet for the Library Permanent Fund (Use Assigned to Library for any spendable fund balance).

a. Prepare any closing entries necessary at year-end.b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the library permanent fund.

c. Prepare a balance sheet for the Library Permanent Fund (Use Assigned to Library for any spendable fund balance).

Question

Question

Question

Question

Question

Question

Question

Question

Jefferson County established a capital project fund in 2011 to build low- income housing with the transfer of $100,000 from the General Fund. The following transactions occurred during 2012:

1. April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. The bond premium was transferred to the debt service fund.

1. April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. The bond premium was transferred to the debt service fund.

2. The County received notice that it had met eligibility requirements for a federal government grant intended to support the capital project in the amount of $250,000. The grant (cash) will be received when the project is completed in February 2013.

3. The County issued a contract for the construction in the amount of $1,000,000.

4. The contractor periodically bills the County for construction completed to date. During the year, bills totaling $390,000 were received. By year-end, a total of $350,000 had been paid.

Jefferson County established a debt service fund in 2012 to make interest and principle payments on the bonds issued in item 1 above. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principle payments are $17,500 each. The following transactions occurred during 2012:

5. The bond premium was received through transfer from the capital project fund.

6. September 30, $38,500 was transferred from the General Fund for the October 1 bond payment.

7. The first debt service payment was made on October 1, 2012.

The Elwood Family Book Fund was established in December 2011, funded by a bequest with the legal restriction that only earnings, and not principal, can be used for the purchase of books for the James K. Polk Library in Jefferson County. The principal amount that must be maintained is $500,000. The following transactions occurred during 2012:

8. The Elwood family pledge of $500,000 was received in donated corporate bonds with a fair value of $370,000 and the balance in cash.

8. The Elwood family pledge of $500,000 was received in donated corporate bonds with a fair value of $370,000 and the balance in cash.

9. $130,000 was invested in U.S. Government Securities.

10. Interest in the amount of $17,000 was received in cash during the year.

11. During the year, books totaling $14,000 were ordered for the library.

12. During the year, the library reported receiving books with an invoice amount totaling $14,000. $13,900 of the amounts due for book purchases had been paid by year-end.

13. An additional $2,500 of interest had accrued on the investments at December 31 and will be received in January of next year.

14. The corporate bonds had a market value of $371,500 and the U.S. securities had a market value of $129,400 as of December 31.

Required:

Using the Excel template provided (a separate tab is provided for each of the requirements):

a. Prepare journal entries recording the events 1 to 14 for the capital projects, debt service, and permanent funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures and Changes in Fund Balance for the Governmental Funds (The General Fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Funds, assuming that unexpended spendable resources in the capital projects fund are classified as restricted and unexpended spendable resources in the debt service and permanent fund are classified as assigned.

1. April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. The bond premium was transferred to the debt service fund.2. The County received notice that it had met eligibility requirements for a federal government grant intended to support the capital project in the amount of $250,000. The grant (cash) will be received when the project is completed in February 2013.

3. The County issued a contract for the construction in the amount of $1,000,000.

4. The contractor periodically bills the County for construction completed to date. During the year, bills totaling $390,000 were received. By year-end, a total of $350,000 had been paid.

Jefferson County established a debt service fund in 2012 to make interest and principle payments on the bonds issued in item 1 above. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principle payments are $17,500 each. The following transactions occurred during 2012:

5. The bond premium was received through transfer from the capital project fund.

6. September 30, $38,500 was transferred from the General Fund for the October 1 bond payment.

7. The first debt service payment was made on October 1, 2012.

The Elwood Family Book Fund was established in December 2011, funded by a bequest with the legal restriction that only earnings, and not principal, can be used for the purchase of books for the James K. Polk Library in Jefferson County. The principal amount that must be maintained is $500,000. The following transactions occurred during 2012:

8. The Elwood family pledge of $500,000 was received in donated corporate bonds with a fair value of $370,000 and the balance in cash.9. $130,000 was invested in U.S. Government Securities.

10. Interest in the amount of $17,000 was received in cash during the year.

11. During the year, books totaling $14,000 were ordered for the library.

12. During the year, the library reported receiving books with an invoice amount totaling $14,000. $13,900 of the amounts due for book purchases had been paid by year-end.

13. An additional $2,500 of interest had accrued on the investments at December 31 and will be received in January of next year.

14. The corporate bonds had a market value of $371,500 and the U.S. securities had a market value of $129,400 as of December 31.

Required:

Using the Excel template provided (a separate tab is provided for each of the requirements):

a. Prepare journal entries recording the events 1 to 14 for the capital projects, debt service, and permanent funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures and Changes in Fund Balance for the Governmental Funds (The General Fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Funds, assuming that unexpended spendable resources in the capital projects fund are classified as restricted and unexpended spendable resources in the debt service and permanent fund are classified as assigned.

Question

The state government established a capital project fund in 2011 to build new highways. The fund is supported by a 5 percent tax on diesel fuel sales in the state. The tax is collected by private gas stations and remitted in the following month to the State. The following transactions occurred during 2012:

1. The encumbrances outstanding at December 31, 2011, were re-established.

1. The encumbrances outstanding at December 31, 2011, were re-established.

2. During the year, fuel taxes were remitted to the State totaling $26,250,000, including the amount due at the end of the previous year. In addition, $2,990,000 is expected to be remitted in January of next year for fuel sales in December 2012.

3. The State awarded new contracts for road construction totaling $29,000,000.

4. During the year, contractors submitted invoices for payment totaling $30,790,000. These were all under the terms of contracts (i.e., same $ amounts) issued by the State.

5. The State made payments on outstanding accounts of $31,500,000.

The state government operates a debt service fund to service outstanding general obligation bonds. The following transactions occurred during 2012:

6. The state general fund provided cash of $4,500,000 through transfer to the debt service fund.

6. The state general fund provided cash of $4,500,000 through transfer to the debt service fund.

7. Payments for matured interest totaled $3,200,000, and payments for matured principal totaled $1,600,000 during the year.

8. In December, the State refunded bonds to obtain a better interest rate. New bonds were issued providing proceeds of $20,000,000, which was immediately used to retire outstanding bonds in the same amount.

Required:

Use the Excel template provided. A separate tab is provided in Excel for each of the requirements:

a. Prepare journal entries recording the events 1 to 8 (above) for the capital projects, and debt service funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the Governmental Funds (the General Fund and special revenue fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Fund assuming all unexpended spendable net resources in the capital projects fund are classified as restricted and in the debt service fund are classified as assigned.

1. The encumbrances outstanding at December 31, 2011, were re-established.2. During the year, fuel taxes were remitted to the State totaling $26,250,000, including the amount due at the end of the previous year. In addition, $2,990,000 is expected to be remitted in January of next year for fuel sales in December 2012.

3. The State awarded new contracts for road construction totaling $29,000,000.

4. During the year, contractors submitted invoices for payment totaling $30,790,000. These were all under the terms of contracts (i.e., same $ amounts) issued by the State.

5. The State made payments on outstanding accounts of $31,500,000.

The state government operates a debt service fund to service outstanding general obligation bonds. The following transactions occurred during 2012:

6. The state general fund provided cash of $4,500,000 through transfer to the debt service fund.7. Payments for matured interest totaled $3,200,000, and payments for matured principal totaled $1,600,000 during the year.

8. In December, the State refunded bonds to obtain a better interest rate. New bonds were issued providing proceeds of $20,000,000, which was immediately used to retire outstanding bonds in the same amount.

Required:

Use the Excel template provided. A separate tab is provided in Excel for each of the requirements:

a. Prepare journal entries recording the events 1 to 8 (above) for the capital projects, and debt service funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the Governmental Funds (the General Fund and special revenue fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Fund assuming all unexpended spendable net resources in the capital projects fund are classified as restricted and in the debt service fund are classified as assigned.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/14

Play

Full screen (f)

Deck 5: Accounting for Other Governmental Fund Types: Capital Projects, Debt Service, and Permanent

1

Using the annual financial report obtained for Exercise 1-1, answer the following questions:

a. Examine the governmental fund financial statements. Are any major capital projects funds included If so, list them. Attempt to find out the nature and purpose of the projects from the letter of transmittal, the notes, or MD A. What are the major sources of funding, such as bond sales, intergovernmental grants, and transfers from other funds Were the projects completed during the year

b. Again looking at the governmental fund financial statements, are any major debt service funds included If so list them. What are the sources of funding for these debt service payments

c. Does your report include supplemental information including combining statements for nonmajor funds If so, are any capital projects and debt service funds included If so, list them. Indicate the major revenue and other financing source categories for these funds.

d. Look at the governmental fund Statement of Revenues, Expenditures, and Changes in Fund Balances, specifically the expenditure classification. Compute a ratio of capital outlay/total expenditures. Again, compute a ratio of debt service/total expenditures. Compare those with your classmates' ratios. Comment on the possible meaning of these ratios.

e. Look at the notes to the financial statements, specifically the note (in the summary of significant accounting policies) regarding the definition of modified accrual accounting. Does the note specifically indicate that modified accrual accounting is used for capital projects and debt service funds Does the note indicate that debt service payments, both principal and interest, are recorded as an expenditure when due

f. Does your government report capital leases payable in the government- wide Statement of Net Assets If so, can you determine if new capital leases were initiated during the year Can you trace the payments related to capital leases

g. Does your government report any permanent funds, either major or non- major If so, list them. What are the amounts of the permanent resources available for governmental purposes What is/are the governmental purpose(s)

a. Examine the governmental fund financial statements. Are any major capital projects funds included If so, list them. Attempt to find out the nature and purpose of the projects from the letter of transmittal, the notes, or MD A. What are the major sources of funding, such as bond sales, intergovernmental grants, and transfers from other funds Were the projects completed during the year

b. Again looking at the governmental fund financial statements, are any major debt service funds included If so list them. What are the sources of funding for these debt service payments

c. Does your report include supplemental information including combining statements for nonmajor funds If so, are any capital projects and debt service funds included If so, list them. Indicate the major revenue and other financing source categories for these funds.

d. Look at the governmental fund Statement of Revenues, Expenditures, and Changes in Fund Balances, specifically the expenditure classification. Compute a ratio of capital outlay/total expenditures. Again, compute a ratio of debt service/total expenditures. Compare those with your classmates' ratios. Comment on the possible meaning of these ratios.

e. Look at the notes to the financial statements, specifically the note (in the summary of significant accounting policies) regarding the definition of modified accrual accounting. Does the note specifically indicate that modified accrual accounting is used for capital projects and debt service funds Does the note indicate that debt service payments, both principal and interest, are recorded as an expenditure when due

f. Does your government report capital leases payable in the government- wide Statement of Net Assets If so, can you determine if new capital leases were initiated during the year Can you trace the payments related to capital leases

g. Does your government report any permanent funds, either major or non- major If so, list them. What are the amounts of the permanent resources available for governmental purposes What is/are the governmental purpose(s)

The solution to this and the first exercise of Chapters 1 through 8 will differ from student to student, assuming each has a different CAFR.

2

A concerned citizen provides resources and establishes a trust with the local government. What factors should be considered in determining which fund to report the trust activities

Like other governmental funds the capital projects, debt service funds and permanent funds also use an accrual basis of accounting and current financial resource measurement focus. These funds does not require to record the budgets.

The governmental funds are used for various purposes including revenue generation and investing in other financial sources as well as meeting the expenditures of the trust. These funds are thus classified as the general funds, debt service funds, permanent funds, and other special revenue funds.

Capital project funds report and accounts to the financial resources which are restricted or committed to a capital expenditure and are generally used to acquire major fixed assets. The funds that are restricted to meet the payments for expenditures of the principal and interest of debts are termed as debt service funds.

The permanent funds are the resources which are restricted such that the principal should not be expended, and the revenue is used for the benefit of the government and its citizen. If the revenues and capital could be used for the activities of the organization, they must be reported as special revenue funds.

The factors that are to be considered in determining the fund to be reported for the trust activities is if the resources of the trust are used for the benefit of the government or its citizenry or for the expenses related to the long-term debts or capital for the asset acquisition.

If the concerned citizen, is benefitted by the funds from the trust activities in any manner, these funds are to be reported as the capital funds or the debt service funds. If the resources benefit the government or the citizen, they are to be classified as permanent funds or special revenue funds based on the requirement to restrict the principal of these resources.

The governmental funds are used for various purposes including revenue generation and investing in other financial sources as well as meeting the expenditures of the trust. These funds are thus classified as the general funds, debt service funds, permanent funds, and other special revenue funds.

Capital project funds report and accounts to the financial resources which are restricted or committed to a capital expenditure and are generally used to acquire major fixed assets. The funds that are restricted to meet the payments for expenditures of the principal and interest of debts are termed as debt service funds.

The permanent funds are the resources which are restricted such that the principal should not be expended, and the revenue is used for the benefit of the government and its citizen. If the revenues and capital could be used for the activities of the organization, they must be reported as special revenue funds.

The factors that are to be considered in determining the fund to be reported for the trust activities is if the resources of the trust are used for the benefit of the government or its citizenry or for the expenses related to the long-term debts or capital for the asset acquisition.

If the concerned citizen, is benefitted by the funds from the trust activities in any manner, these funds are to be reported as the capital funds or the debt service funds. If the resources benefit the government or the citizen, they are to be classified as permanent funds or special revenue funds based on the requirement to restrict the principal of these resources.

3

Assume a government leases equipment to be used in governmental activities under a noncancelable lease, meeting the requirements for classification as a capital lease. Where would the capital lease be reported in the government's financial statements

Like other governmental funds the capital projects, debt service funds and permanent funds also use an accrual basis of accounting and current financial resource measurement focus. These funds does not require to record the budgets.

Capital project funds report and accounts to the financial resources which are restricted or committed to a capital expenditure and are generally used to acquire major fixed assets. The funds that are restricted to meet the payments for expenditures of the principal and interest of debts are termed as debt service funds.

The permanent funds are the resources which are restricted such that the principal should not be expended, and the revenue is used for the benefit of the government and its citizen. If the revenues and capital could be used for the activities of the organization, they must be reported as special revenue funds.

As per the FASB accounting and financial reporting standards, the noncancelable leases are classified as operating leases and capital leases.

As per the FASB standards, if a government acquires fixed assets through a capital lease agreement, these assets are to be recorded in the government-wide financial statements. Given that the government has acquired the equipment under noncancelable lease that qualifies to be classified as a capital lease. Therefore, the equipment will be reported in the government-wide financial statements.

Capital project funds report and accounts to the financial resources which are restricted or committed to a capital expenditure and are generally used to acquire major fixed assets. The funds that are restricted to meet the payments for expenditures of the principal and interest of debts are termed as debt service funds.

The permanent funds are the resources which are restricted such that the principal should not be expended, and the revenue is used for the benefit of the government and its citizen. If the revenues and capital could be used for the activities of the organization, they must be reported as special revenue funds.

As per the FASB accounting and financial reporting standards, the noncancelable leases are classified as operating leases and capital leases.

As per the FASB standards, if a government acquires fixed assets through a capital lease agreement, these assets are to be recorded in the government-wide financial statements. Given that the government has acquired the equipment under noncancelable lease that qualifies to be classified as a capital lease. Therefore, the equipment will be reported in the government-wide financial statements.

4

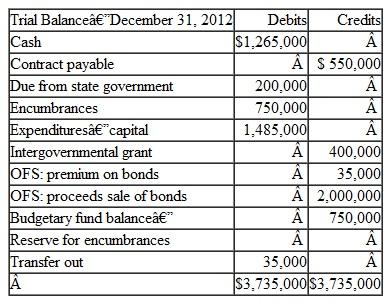

The citizens of Spencer County approved the issuance of $2,000,000 in 6 percent general obligation bonds to finance the construction of a courthouse annex. A capital projects fund was established for that purpose. The preclosing trial balance of the courthouse annex capital project fund follows:

a. Prepare any closing entries necessary at year-end.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the courthouse annex capital project fund.

c. Prepare a balance sheet for the Courthouse Annex Capital Project Fund, assuming all unexpended resources are restricted to construction of the courthouse annex.

a. Prepare any closing entries necessary at year-end.b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the courthouse annex capital project fund.

c. Prepare a balance sheet for the Courthouse Annex Capital Project Fund, assuming all unexpended resources are restricted to construction of the courthouse annex.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

5

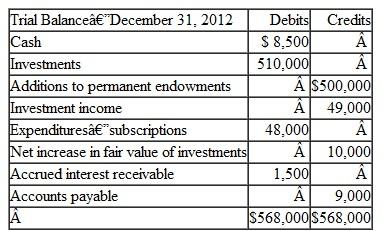

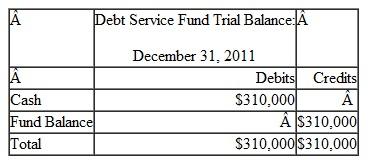

A citizen group raised funds to establish an endowment for the Eastville City Library. Under the terms of the trust agreement, the principal must be maintained, but the earnings of the fund are to be used to purchase database and periodical subscriptions for the library. A preclosing trial balance of the library permanent fund follows:

a. Prepare any closing entries necessary at year-end.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the library permanent fund.

c. Prepare a balance sheet for the Library Permanent Fund (Use Assigned to Library for any spendable fund balance).

a. Prepare any closing entries necessary at year-end.b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the library permanent fund.

c. Prepare a balance sheet for the Library Permanent Fund (Use Assigned to Library for any spendable fund balance).

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

6

a. Armstrong County established a County Office Building Construction Fund to account for a project that was expected to take less than one year to complete. The County's fiscal year ends on June 30.

(1) On July 1, 2011, bonds were sold at par in the amount of $8,750,000 for the project.

(2) On July 5, a contract was signed with the Sellers Construction Company in the amount of $8,650,000.

(3) On December 30, a progress bill was received from Sellers in the amount of $6,000,000. The bill was paid, except for a 5 percent retainage.

(4) On June 1, 2012, a final bill was received in the amount of $2,650,000 from Sellers, which was paid, except for the 5 percent retainage. An appointment was made between the County Engineer and Bill Sellers to inspect the building and to develop a list of items that needed to be corrected.

(5) On the day of the meeting, the County Engineer discovered that Sellers had filed for bankruptcy and moved to Florida. The City incurred a liability in the amount of $490,000 to have the defects corrected by the Baker Construction Company. (Charge the excess over the balance of Contracts Payable-Retained Percentage to Construction Expenditures.)

(6) All accounts (from 5 above) were paid; remaining cash was transferred to the Debt Service Fund.

(7) The accounts of the County Office Building Construction Fund were closed.

Record the transaction in the County Office Building Construction Fund.

b. Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund Balances for the County Office Building Construction Fund for the year ended June 30, 2012.

(1) On July 1, 2011, bonds were sold at par in the amount of $8,750,000 for the project.

(2) On July 5, a contract was signed with the Sellers Construction Company in the amount of $8,650,000.

(3) On December 30, a progress bill was received from Sellers in the amount of $6,000,000. The bill was paid, except for a 5 percent retainage.

(4) On June 1, 2012, a final bill was received in the amount of $2,650,000 from Sellers, which was paid, except for the 5 percent retainage. An appointment was made between the County Engineer and Bill Sellers to inspect the building and to develop a list of items that needed to be corrected.

(5) On the day of the meeting, the County Engineer discovered that Sellers had filed for bankruptcy and moved to Florida. The City incurred a liability in the amount of $490,000 to have the defects corrected by the Baker Construction Company. (Charge the excess over the balance of Contracts Payable-Retained Percentage to Construction Expenditures.)

(6) All accounts (from 5 above) were paid; remaining cash was transferred to the Debt Service Fund.

(7) The accounts of the County Office Building Construction Fund were closed.

Record the transaction in the County Office Building Construction Fund.

b. Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund Balances for the County Office Building Construction Fund for the year ended June 30, 2012.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

7

The Village of Harris issued $5,000,000 in 6 percent general obligation, tax- supported bonds on July 1, 2011, at 101. A fiscal agent is not used. Resources for principal and interest payments are to come from the General Fund. Interest payment dates are December 31 and June 30. The first of 20 annual principal payments is to be made June 30, 2012. Harris has a calendar fiscal year.

1. A capital projects fund transferred the premium ($50,000) to the debt service fund.

2. On December 31, 2011, funds in the amount of $150,000 were received from the General Fund and the first interest payment was made.

3. The books were closed for 2011.

4. On June 30, 2012, funds in the amount of $350,000 were received from the General Fund, and the second interest payment ($150,000) was made along with the first principal payment ($250,000).

5. On December 31, 2012, funds in the amount of $142,500 were received from the General Fund and the third interest payment was made ($142,500).

6. The books were closed for 2012.

a. Prepare journal entries to record the events above in the debt service fund.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the debt service fund for the year ended December 31, 2011.

c. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the debt service fund for the year ended December 31, 2012.

1. A capital projects fund transferred the premium ($50,000) to the debt service fund.

2. On December 31, 2011, funds in the amount of $150,000 were received from the General Fund and the first interest payment was made.

3. The books were closed for 2011.

4. On June 30, 2012, funds in the amount of $350,000 were received from the General Fund, and the second interest payment ($150,000) was made along with the first principal payment ($250,000).

5. On December 31, 2012, funds in the amount of $142,500 were received from the General Fund and the third interest payment was made ($142,500).

6. The books were closed for 2012.

a. Prepare journal entries to record the events above in the debt service fund.

b. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the debt service fund for the year ended December 31, 2011.

c. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the debt service fund for the year ended December 31, 2012.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

8

Beachfront property owners of the Village of Eden requested a seawall be constructed to protect their beach. The seawall was financed through a note payable, which was to be repaid from taxes raised through a special assessment on their properties. The Village guarantees the debt and accounts for the special assessment through a debt service fund. Assume the special assessments were levied in 2011, recording a special assessment receivable and deferred revenue in the amount of $600,000. One- third of the assessment is to be collected each year and used to pay the interest and principal on the note. Record the following transactions that occurred in 2012:

1. June 30, $200,000 of the assessments became due and currently receivable. ( Hint: The special assessment tax is recorded as revenue in the debt service fund when it becomes due.)

2. July 31, the $200,000 were collected.

3. September 30, interest of $40,000 and principal of $160,000 were paid.

4. December 31, the books were closed.

1. June 30, $200,000 of the assessments became due and currently receivable. ( Hint: The special assessment tax is recorded as revenue in the debt service fund when it becomes due.)

2. July 31, the $200,000 were collected.

3. September 30, interest of $40,000 and principal of $160,000 were paid.

4. December 31, the books were closed.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

9

The Village of Budekville, which has a fiscal year July 1 to June 30, sold $3,000,000 in 6 percent tax-supported bonds at par to construct an addition to its police station. The bonds were dated and issued on July 1, 2011. Interest is payable semiannually on January 1 and July 1, and the first of 10 equal annual principal payments will be made on July 1, 2012. The village used a capital projects fund to account for the project, and a debt service fund was created to make interest and principal payments.

1. The bonds were sold on July 1, 2011.

2. The General Fund transferred an amount equal to the first interest payment on December 31, 2011. The Debt Service Fund made the payment as of January 1, 2012.

3. The project was completed on June 15, 2012. Expenditures totaled $2,989,000. You may omit encumbrance entries.

4. The remaining balance was transferred to the Debt Service Fund from the Capital Projects Fund for the eventual payment of principal.

Required:

a. Prepare journal entries for the capital projects fund based on the aforementioned information. Include a closing entry.

b. Prepare journal entries for the debt service fund based on the information presented above. Include a closing entry.

c. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 2012, for the governmental funds (i.e., use separate columns for the General, capital projects, and debt service funds). Assume the General Fund reports the following: property tax revenues $500,000, other revenues $200,000, public safety expenditures $450,000, general government expenditures $150,000, other financing sources-transfers out $125,000, and beginning fund balance $120,000.

1. The bonds were sold on July 1, 2011.

2. The General Fund transferred an amount equal to the first interest payment on December 31, 2011. The Debt Service Fund made the payment as of January 1, 2012.

3. The project was completed on June 15, 2012. Expenditures totaled $2,989,000. You may omit encumbrance entries.

4. The remaining balance was transferred to the Debt Service Fund from the Capital Projects Fund for the eventual payment of principal.

Required:

a. Prepare journal entries for the capital projects fund based on the aforementioned information. Include a closing entry.

b. Prepare journal entries for the debt service fund based on the information presented above. Include a closing entry.

c. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the year ended June 30, 2012, for the governmental funds (i.e., use separate columns for the General, capital projects, and debt service funds). Assume the General Fund reports the following: property tax revenues $500,000, other revenues $200,000, public safety expenditures $450,000, general government expenditures $150,000, other financing sources-transfers out $125,000, and beginning fund balance $120,000.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

10

On July 1, 2011, a five-year agreement is signed between the City of Genoa and the Computer Leasing Corporation for the use of computer equipment not associated with proprietary funds activity. The cost of the lease, excluding executory costs, is $12,000 per year. The first payment is to be made by a capital projects fund at the inception of the lease. Subsequent payments, beginning July 1, 2012, are to be made by a debt service fund. The present value of the lease payments, including the first payment, is $54,552. The interest rate implicit in the lease is 5 percent.

a. Assuming the agreement meets the criteria for a capital lease under the provisions of SFAS No. 13, make the entries required in (1) the capital projects fund and (2) the debt service fund on July 1, 2011, and July 1, 2012.

b. Comment on where the fixed asset and long-term liability associated with this capital lease would be recorded and the impact of the journal entries recorded for a.

a. Assuming the agreement meets the criteria for a capital lease under the provisions of SFAS No. 13, make the entries required in (1) the capital projects fund and (2) the debt service fund on July 1, 2011, and July 1, 2012.

b. Comment on where the fixed asset and long-term liability associated with this capital lease would be recorded and the impact of the journal entries recorded for a.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

11

The Town of McHenry has $6,000,000 in general obligation bonds outstanding and maintains a single debt service fund for all debt service transactions. On July 1, 2012, a current refunding took place in which $6,000,000 in new general obligation bonds were issued. Record the transaction on the books of the debt service fund.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

12

The City of Sharpesburg received a gift of $950,000 from a local resident on June 1, 2012, and signed an agreement that the funds would be invested permanently and that the income would be used to purchase books for the city library. The following transactions took place during the year ended December 31, 2012:

1. The gift was recorded on June 1.

2. On June 1, ABC Company bonds were purchased as investments in the amount of $950,000 (par value). The bonds carry an annual interest rate of 6 percent, payable semiannually on December 1 and June 1.

3. On December 1, the semiannual interest payment was received.

4. From December 1 through December 31, $27,700 in book purchases were made; full payment was made in cash.

5. On December 31, an accrual was made for interest.

6. Also, on December 31, a reading of the financial press indicated that the ABC bonds had a fair value of $966,000, exclusive of accrued interest.

7. The books were closed.

Required:

a. Record the transactions on the books of the Library Book Permanent Fund.

b. Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund Balances for the Library Book Permanent Fund for the Year Ended December 31, 2012.

1. The gift was recorded on June 1.

2. On June 1, ABC Company bonds were purchased as investments in the amount of $950,000 (par value). The bonds carry an annual interest rate of 6 percent, payable semiannually on December 1 and June 1.

3. On December 1, the semiannual interest payment was received.

4. From December 1 through December 31, $27,700 in book purchases were made; full payment was made in cash.

5. On December 31, an accrual was made for interest.

6. Also, on December 31, a reading of the financial press indicated that the ABC bonds had a fair value of $966,000, exclusive of accrued interest.

7. The books were closed.

Required:

a. Record the transactions on the books of the Library Book Permanent Fund.

b. Prepare a separate Statement of Revenues, Expenditures, and Changes in Fund Balances for the Library Book Permanent Fund for the Year Ended December 31, 2012.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

13

Jefferson County established a capital project fund in 2011 to build low- income housing with the transfer of $100,000 from the General Fund. The following transactions occurred during 2012:

1. April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. The bond premium was transferred to the debt service fund.

2. The County received notice that it had met eligibility requirements for a federal government grant intended to support the capital project in the amount of $250,000. The grant (cash) will be received when the project is completed in February 2013.

3. The County issued a contract for the construction in the amount of $1,000,000.

4. The contractor periodically bills the County for construction completed to date. During the year, bills totaling $390,000 were received. By year-end, a total of $350,000 had been paid.

Jefferson County established a debt service fund in 2012 to make interest and principle payments on the bonds issued in item 1 above. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principle payments are $17,500 each. The following transactions occurred during 2012:

5. The bond premium was received through transfer from the capital project fund.

6. September 30, $38,500 was transferred from the General Fund for the October 1 bond payment.

7. The first debt service payment was made on October 1, 2012.

The Elwood Family Book Fund was established in December 2011, funded by a bequest with the legal restriction that only earnings, and not principal, can be used for the purchase of books for the James K. Polk Library in Jefferson County. The principal amount that must be maintained is $500,000. The following transactions occurred during 2012:

8. The Elwood family pledge of $500,000 was received in donated corporate bonds with a fair value of $370,000 and the balance in cash.

9. $130,000 was invested in U.S. Government Securities.

10. Interest in the amount of $17,000 was received in cash during the year.

11. During the year, books totaling $14,000 were ordered for the library.

12. During the year, the library reported receiving books with an invoice amount totaling $14,000. $13,900 of the amounts due for book purchases had been paid by year-end.

13. An additional $2,500 of interest had accrued on the investments at December 31 and will be received in January of next year.

14. The corporate bonds had a market value of $371,500 and the U.S. securities had a market value of $129,400 as of December 31.

Required:

Using the Excel template provided (a separate tab is provided for each of the requirements):

a. Prepare journal entries recording the events 1 to 14 for the capital projects, debt service, and permanent funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures and Changes in Fund Balance for the Governmental Funds (The General Fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Funds, assuming that unexpended spendable resources in the capital projects fund are classified as restricted and unexpended spendable resources in the debt service and permanent fund are classified as assigned.

1. April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. The bond premium was transferred to the debt service fund.2. The County received notice that it had met eligibility requirements for a federal government grant intended to support the capital project in the amount of $250,000. The grant (cash) will be received when the project is completed in February 2013.

3. The County issued a contract for the construction in the amount of $1,000,000.

4. The contractor periodically bills the County for construction completed to date. During the year, bills totaling $390,000 were received. By year-end, a total of $350,000 had been paid.

Jefferson County established a debt service fund in 2012 to make interest and principle payments on the bonds issued in item 1 above. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principle payments are $17,500 each. The following transactions occurred during 2012:

5. The bond premium was received through transfer from the capital project fund.

6. September 30, $38,500 was transferred from the General Fund for the October 1 bond payment.

7. The first debt service payment was made on October 1, 2012.

The Elwood Family Book Fund was established in December 2011, funded by a bequest with the legal restriction that only earnings, and not principal, can be used for the purchase of books for the James K. Polk Library in Jefferson County. The principal amount that must be maintained is $500,000. The following transactions occurred during 2012:

8. The Elwood family pledge of $500,000 was received in donated corporate bonds with a fair value of $370,000 and the balance in cash.9. $130,000 was invested in U.S. Government Securities.

10. Interest in the amount of $17,000 was received in cash during the year.

11. During the year, books totaling $14,000 were ordered for the library.

12. During the year, the library reported receiving books with an invoice amount totaling $14,000. $13,900 of the amounts due for book purchases had been paid by year-end.

13. An additional $2,500 of interest had accrued on the investments at December 31 and will be received in January of next year.

14. The corporate bonds had a market value of $371,500 and the U.S. securities had a market value of $129,400 as of December 31.

Required:

Using the Excel template provided (a separate tab is provided for each of the requirements):

a. Prepare journal entries recording the events 1 to 14 for the capital projects, debt service, and permanent funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures and Changes in Fund Balance for the Governmental Funds (The General Fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Funds, assuming that unexpended spendable resources in the capital projects fund are classified as restricted and unexpended spendable resources in the debt service and permanent fund are classified as assigned.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

14

The state government established a capital project fund in 2011 to build new highways. The fund is supported by a 5 percent tax on diesel fuel sales in the state. The tax is collected by private gas stations and remitted in the following month to the State. The following transactions occurred during 2012:

1. The encumbrances outstanding at December 31, 2011, were re-established.

2. During the year, fuel taxes were remitted to the State totaling $26,250,000, including the amount due at the end of the previous year. In addition, $2,990,000 is expected to be remitted in January of next year for fuel sales in December 2012.

3. The State awarded new contracts for road construction totaling $29,000,000.

4. During the year, contractors submitted invoices for payment totaling $30,790,000. These were all under the terms of contracts (i.e., same $ amounts) issued by the State.

5. The State made payments on outstanding accounts of $31,500,000.

The state government operates a debt service fund to service outstanding general obligation bonds. The following transactions occurred during 2012:

6. The state general fund provided cash of $4,500,000 through transfer to the debt service fund.

7. Payments for matured interest totaled $3,200,000, and payments for matured principal totaled $1,600,000 during the year.

8. In December, the State refunded bonds to obtain a better interest rate. New bonds were issued providing proceeds of $20,000,000, which was immediately used to retire outstanding bonds in the same amount.

Required:

Use the Excel template provided. A separate tab is provided in Excel for each of the requirements:

a. Prepare journal entries recording the events 1 to 8 (above) for the capital projects, and debt service funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the Governmental Funds (the General Fund and special revenue fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Fund assuming all unexpended spendable net resources in the capital projects fund are classified as restricted and in the debt service fund are classified as assigned.

1. The encumbrances outstanding at December 31, 2011, were re-established.2. During the year, fuel taxes were remitted to the State totaling $26,250,000, including the amount due at the end of the previous year. In addition, $2,990,000 is expected to be remitted in January of next year for fuel sales in December 2012.

3. The State awarded new contracts for road construction totaling $29,000,000.

4. During the year, contractors submitted invoices for payment totaling $30,790,000. These were all under the terms of contracts (i.e., same $ amounts) issued by the State.

5. The State made payments on outstanding accounts of $31,500,000.

The state government operates a debt service fund to service outstanding general obligation bonds. The following transactions occurred during 2012:

6. The state general fund provided cash of $4,500,000 through transfer to the debt service fund.7. Payments for matured interest totaled $3,200,000, and payments for matured principal totaled $1,600,000 during the year.

8. In December, the State refunded bonds to obtain a better interest rate. New bonds were issued providing proceeds of $20,000,000, which was immediately used to retire outstanding bonds in the same amount.

Required:

Use the Excel template provided. A separate tab is provided in Excel for each of the requirements:

a. Prepare journal entries recording the events 1 to 8 (above) for the capital projects, and debt service funds.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance for the Governmental Funds (the General Fund and special revenue fund financial statements have already been prepared).

e. Prepare a Balance Sheet for the Governmental Fund assuming all unexpended spendable net resources in the capital projects fund are classified as restricted and in the debt service fund are classified as assigned.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 14 flashcards in this deck.