Deck 12: Overview of Fixed-Income Portfolio Management

Full screen (f)

Question

The following information relates to Questions 1-6

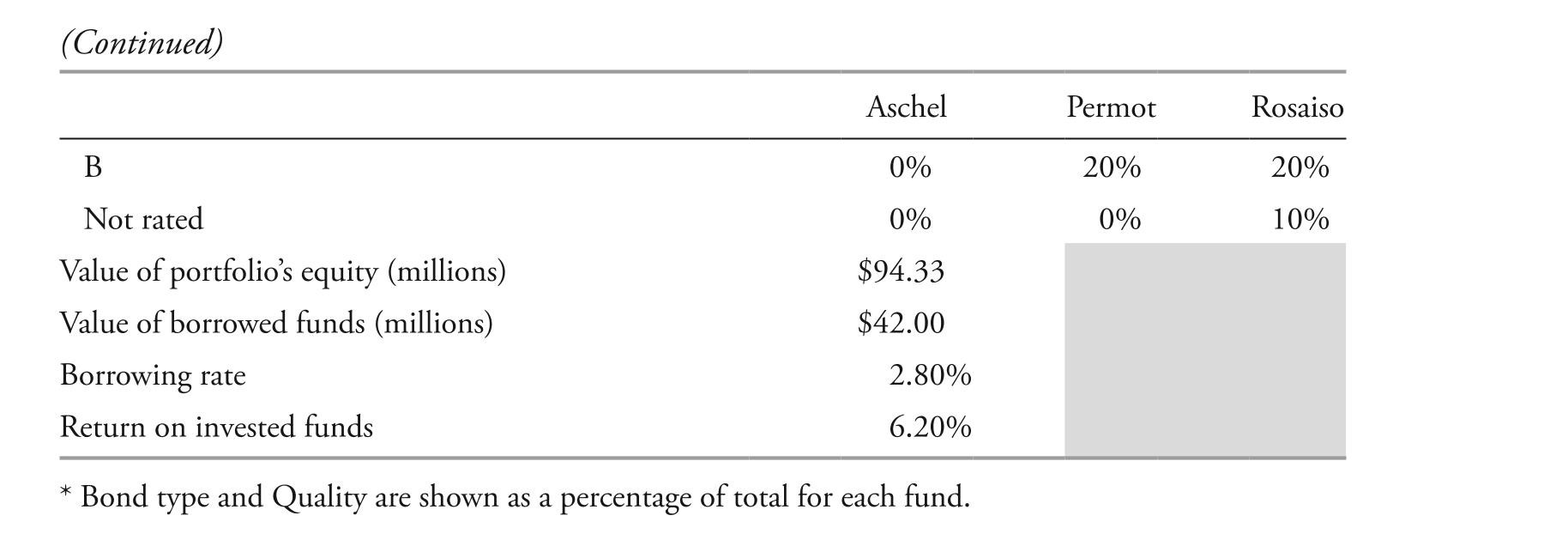

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on note 2, rosaiso is the only fund for which the expected change in price based on the investor's views of yields and yield spreads should be calculated using:

A) convexity.

B) modified duration.

C) effective duration.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on note 2, rosaiso is the only fund for which the expected change in price based on the investor's views of yields and yield spreads should be calculated using:

A) convexity.

B) modified duration.

C) effective duration.

Question

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-The levered portfolio return for aschel is closest to:

A) 7.25%.

B) 7.71%.

C) 8.96%.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-The levered portfolio return for aschel is closest to:

A) 7.25%.

B) 7.71%.

C) 8.96%.

Question

Question

Question

Question

Question

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 2, the optimal strategy to meet villash foundation's cash needs is the sale of:

A) 100% of bond 1.

B) 100% of bond 2.

C) 50% of bond 1 and 50% of bond 2.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 2, the optimal strategy to meet villash foundation's cash needs is the sale of:

A) 100% of bond 1.

B) 100% of bond 2.

C) 50% of bond 1 and 50% of bond 2.

Question

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-is Perreaux correct with respect to key features of cash flow matching?

A) Yes.

B) no, only feature 1 is correct.

C) no, only feature 2 is correct.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-is Perreaux correct with respect to key features of cash flow matching?

A) Yes.

B) no, only feature 1 is correct.

C) no, only feature 2 is correct.

Question

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, the rolling yield of aschel over a one-year investment horizon is closest to:

A) −2.56%.

B) 0.54%.

C) 5.66%.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, the rolling yield of aschel over a one-year investment horizon is closest to:

A) −2.56%.

B) 0.54%.

C) 5.66%.

Question

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, which fund provides the highest level of protection against inflation for coupon payments?

A) aschel

B) Permot

C) rosaiso

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, which fund provides the highest level of protection against inflation for coupon payments?

A) aschel

B) Permot

C) rosaiso

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/12

Play

Full screen (f)

Deck 12: Overview of Fixed-Income Portfolio Management

1

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on note 2, rosaiso is the only fund for which the expected change in price based on the investor's views of yields and yield spreads should be calculated using:

A) convexity.

B) modified duration.

C) effective duration.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on note 2, rosaiso is the only fund for which the expected change in price based on the investor's views of yields and yield spreads should be calculated using:

A) convexity.

B) modified duration.

C) effective duration.

effective duration.

2

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-The levered portfolio return for aschel is closest to:

A) 7.25%.

B) 7.71%.

C) 8.96%.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-The levered portfolio return for aschel is closest to:

A) 7.25%.

B) 7.71%.

C) 8.96%.

7.71%.

3

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 1, which bond most likely has the highest liquidity premium?

A) bond 1

B) bond 2

C) bond 3

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 1, which bond most likely has the highest liquidity premium?

A) bond 1

B) bond 2

C) bond 3

bond 3

4

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 2, the total expected return of the fund's global bond portfolio is closest to:

A) 0.90%.

B) 2.20%.

C) 3.76%.

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 2, the total expected return of the fund's global bond portfolio is closest to:

A) 0.90%.

B) 2.20%.

C) 3.76%.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

5

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-Strategy 2 is most likely preferred to Strategy 1 for meeting the objective of:

A) protecting inflation.

B) funding future liabilities.

C) minimizing the correlation of the fund's domestic bond portfolio and equity portfolio.

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-Strategy 2 is most likely preferred to Strategy 1 for meeting the objective of:

A) protecting inflation.

B) funding future liabilities.

C) minimizing the correlation of the fund's domestic bond portfolio and equity portfolio.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

6

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-which approach to its total return mandate is the fund's domestic bond portfolio most likely to use?

A) Pure indexing

B) enhanced indexing

C) active management

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-which approach to its total return mandate is the fund's domestic bond portfolio most likely to use?

A) Pure indexing

B) enhanced indexing

C) active management

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

7

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 2, the optimal strategy to meet villash foundation's cash needs is the sale of:

A) 100% of bond 1.

B) 100% of bond 2.

C) 50% of bond 1 and 50% of bond 2.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 2, the optimal strategy to meet villash foundation's cash needs is the sale of:

A) 100% of bond 1.

B) 100% of bond 2.

C) 50% of bond 1 and 50% of bond 2.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

8

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-is Perreaux correct with respect to key features of cash flow matching?

A) Yes.

B) no, only feature 1 is correct.

C) no, only feature 2 is correct.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-is Perreaux correct with respect to key features of cash flow matching?

A) Yes.

B) no, only feature 1 is correct.

C) no, only feature 2 is correct.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

9

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, the rolling yield of aschel over a one-year investment horizon is closest to:

A) −2.56%.

B) 0.54%.

C) 5.66%.

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, the rolling yield of aschel over a one-year investment horizon is closest to:

A) −2.56%.

B) 0.54%.

C) 5.66%.

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

10

The following information relates to Questions 1-6

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.

note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, which fund provides the highest level of protection against inflation for coupon payments?

A) aschel

B) Permot

C) rosaiso

Cécile Perreaux is a junior analyst for an international wealth management firm. her supervi-sor, Margit daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds aschel, Permot, and rosaiso are presented in exhibit 1. in Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged.

EXHIBIT 1 Selected Data on Fixed-Income Funds

after further review of the composition of each of the funds, Perreaux notes the following.note 1: aschel is the only fund of the three that uses leverage.note 2: rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with villash foundation. villash foundation is a tax-exempt client. Prior to the meeting, Perreaux identifies what she considers to be two key features of a cash flow-matching approach.

feature 1: it requires no yield curve assumptions.

feature 2: Cash flows come from coupons and liquidating bond portfolio positions.two years later, daasvand learns that villash foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation. Selected data

on the two bonds are presented in exhibit 2.

-based on exhibit 1, which fund provides the highest level of protection against inflation for coupon payments?

A) aschel

B) Permot

C) rosaiso

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

11

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 3, which manager is most likely to have an active management total return mandate?

A) Manager a

B) Manager b

C) Manager C

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-based on exhibit 3, which manager is most likely to have an active management total return mandate?

A) Manager a

B) Manager b

C) Manager C

Unlock Deck

Unlock for access to all 12 flashcards in this deck.

Unlock Deck

k this deck

12

The following information relates to Questions

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio

deveraux contemplates adding a new manager to the global bond portfolio. She reviews three proposals and determines that each manager uses the same index as its benchmark but pursues a different total return approach, as presented in exhibit 3.

-are foster's statements to deveraux supporting foster's choice of bonds to sell correct?

A) Only Statement 1 is correct.

B) Only Statement 2 is correct.

C) neither Statement 1 nor Statement 2 is correct.

Celia deveraux is chief investment officer for the topanga investors fund, which invests in equities and fixed income. The clients in the fund are all taxable investors. The fixed-income allocation includes a domestic (US) bond portfolio and an externally managed global bond portfolio.

The domestic bond portfolio has a total return mandate, which specifies a long-term re- turn objective of 25 basis points (bps) over the benchmark index. relative to the benchmark, small deviations in sector weightings are permitted, such risk factors as duration must closely match, and tracking error is expected to be less than 50 bps per year.

The objectives for the domestic bond portfolio include the ability to fund future liabili-ties, protect interest income from short-term inflation, and minimize the correlation with the fund's equity portfolio. The correlation between the fund's domestic bond portfolio and equity

portfolio is currently 0.14. deveraux plans to reduce the fund's equity allocation and increase

the allocation to the domestic bond portfolio. She reviews two possible investment strategies.

Strategy 1: Purchase aaa rated fixed-coupon corporate bonds with a modified duration

of two years and a correlation coefficient with the equity portfolio of −0.15.

Strategy 2: Purchase US government agency floating-coupon bonds with a modified du-

ration of one month and a correlation coefficient with the equity portfolioof −0.10.

deveraux realizes that the fund's return may decrease if the equity allocation of the fund is

reduced. deveraux decides to liquidate $20 million of US treasuries that are currently owned

and to invest the proceeds in the US corporate bond sector. to fulfill this strategy, deveraux

asks dan foster, a newly hired analyst for the fund, to recommend treasuries to sell and cor-porate bonds to purchase.

foster recommends treasuries from the existing portfolio that he believes are overvalued

and will generate capital gains. deveraux asks foster why he chose only overvalued bonds

with capital gains and did not include any bonds with capital losses. foster responds with two

statements.

Statement 1: taxable investors should prioritize selling overvalued bonds and always sell

them before selling bonds that are viewed as fairly valued or undervalued.

Statement 2: taxable investors should never intentionally realize capital losses.

regarding the purchase of corporate bonds, foster collects relevant data, which are pre-sented in exhibit 1.

deveraux and foster review the total expected 12-month return (assuming no reinvest-ment income) for the global bond portfolio. Selected financial data are presented in exhibit 2.exhibit 2 Selected data on global bond Portfolio