Deck 5: Unemployment Compensation Taxes

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Michael Mirer worked for Dawson Company for six months this year and earned $11,200. The other six months he earned $6,900 working for McBride Company (a separate company). The amount of FUTA taxes to be paid on Mirer's wages by the two companies is:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Michael Mirer worked for Dawson Company for six months this year and earned $11,200. The other six months he earned $6,900 working for McBride Company (a separate company). The amount of FUTA taxes to be paid on Mirer's wages by the two companies is:

Question

Question

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Stys Company's payroll for the year is $1,210,930. Of this amount, $510,710 is for wages paid in excess of $7,000 to each individual employee. The SUTA tax rate for the company is 3.2% on the first $7,000 of each employee's earnings.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Stys Company's payroll for the year is $1,210,930. Of this amount, $510,710 is for wages paid in excess of $7,000 to each individual employee. The SUTA tax rate for the company is 3.2% on the first $7,000 of each employee's earnings.

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . John Gercke is an employee of The Woolson Company. During the first part of the year, he earned $6,800 while working in State A. For the remainder of the year, the company transferred him to State B where he earned $16,500. The Woolson Company's tax rate in State A is 4.2%, and in State B it is 3.15% on the first $7,000. Assuming that reciprocal arrangements exist between the two states, determine the SUTA tax that the company paid to:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . John Gercke is an employee of The Woolson Company. During the first part of the year, he earned $6,800 while working in State A. For the remainder of the year, the company transferred him to State B where he earned $16,500. The Woolson Company's tax rate in State A is 4.2%, and in State B it is 3.15% on the first $7,000. Assuming that reciprocal arrangements exist between the two states, determine the SUTA tax that the company paid to:

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Niemann Company has a SUTA tax rate of 7.1%. The taxable payroll for the year for FUTA and SUTA is $82,600.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Niemann Company has a SUTA tax rate of 7.1%. The taxable payroll for the year for FUTA and SUTA is $82,600.

Question

Question

Question

Question

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Aaron Norman earned $24,900 for the year from Marcus Company. The company is subject to a SUTA tax of 4.7% on the first $9,900 of earnings. Determine:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Aaron Norman earned $24,900 for the year from Marcus Company. The company is subject to a SUTA tax of 4.7% on the first $9,900 of earnings. Determine:

Question

Question

Question

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Queno Company had FUTA taxable wages of $510,900 during the year. Determine its:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Queno Company had FUTA taxable wages of $510,900 during the year. Determine its:

Question

Question

Question

Question

Question

Question

Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

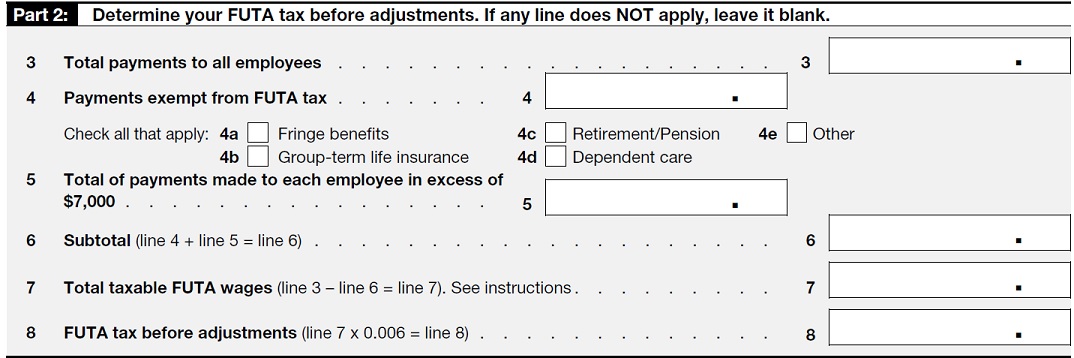

a. Complete Part 2 of Form 940 based on the following information:

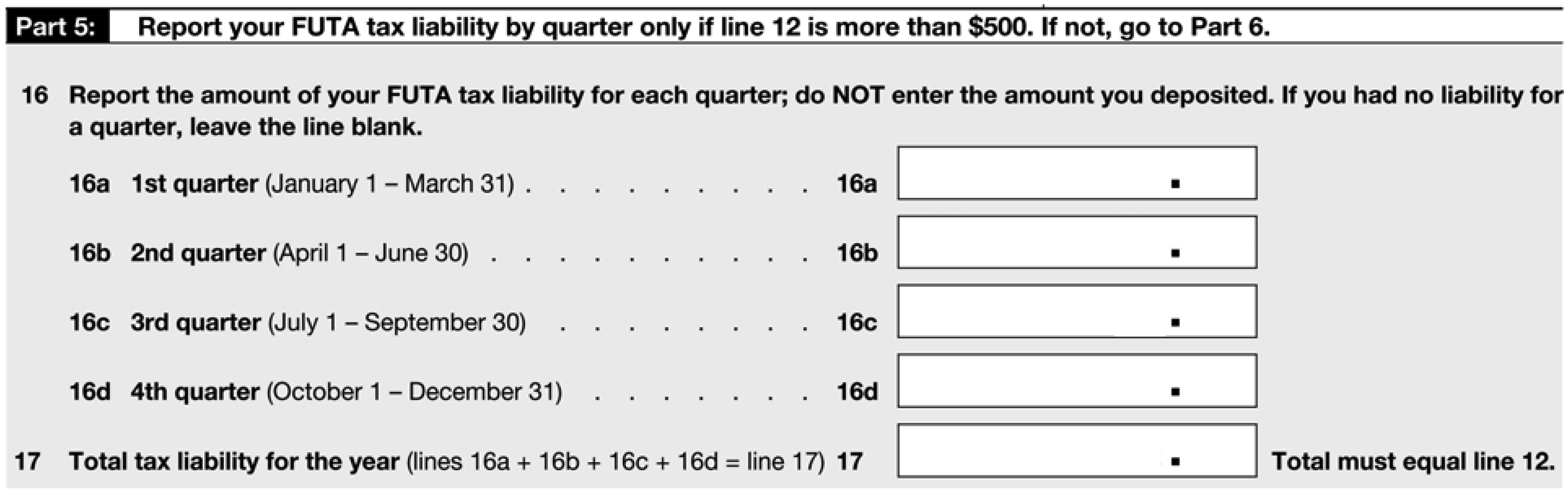

b. Complete Part 5 of Form 940 for the employer given the breakdown of FUTA taxable

b. Complete Part 5 of Form 940 for the employer given the breakdown of FUTA taxable

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

a. Complete Part 2 of Form 940 based on the following information:

b. Complete Part 5 of Form 940 for the employer given the breakdown of FUTA taxable Question

Question

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Ted Carman worked for Rivertide Country Club and earned $28,500 during the year. He also worked part time for Harrison Furniture Company and earned $12,400 during the year. The SUTA tax rate for Rivertide Country Club is 4.2% on the first $8,000, and the rate for Harrison Furniture Company is 5.1% on the first $8,000. Calculate the FUTA and SUTA taxes paid by the employers on Carman's earnings.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Ted Carman worked for Rivertide Country Club and earned $28,500 during the year. He also worked part time for Harrison Furniture Company and earned $12,400 during the year. The SUTA tax rate for Rivertide Country Club is 4.2% on the first $8,000, and the rate for Harrison Furniture Company is 5.1% on the first $8,000. Calculate the FUTA and SUTA taxes paid by the employers on Carman's earnings.

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/93

Play

Full screen (f)

Deck 5: Unemployment Compensation Taxes

1

Advance payments for work done in the future are not taxable wages for FUTA purposes.

False

2

Retirement pay is taxable wages for FUTA purposes.

False

3

Partnerships do not have to pay unemployment taxes on the wages of their employees.

False

4

For FUTA purposes, an employer must pay a higher FUTA tax rate on executives than on nonsupervisory personnel.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

5

The Social Security Act ordered every state to set up an unemployment compensation program.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

6

If an employee works in more than one state, the employer must pay a separate SUTA tax to each of those states in which the employee earns wages.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

7

If an employee has more than one employer during the current year, the taxable wage base applies separately to each of those employers, unless one employer has transferred the business to the second.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

8

Services performed by a child under the age of 21 for a parent-employer are excluded from FUTA coverage.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

9

Every employer is entitled to a 5.4 percent credit against the gross FUTA tax of 6.0 percent.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

10

Services performed in the employ of a religious organization that is exempt from federal income tax are also exempt from FUTA coverage.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

11

Insurance agents paid solely on a commission basis are not considered employees under FUTA.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

12

In the case of a part-time employee, the employer is not liable to pay any of the employee's earnings.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

13

Unemployment taxes (FUTA and SUTA) do not have to be paid by an employer who has only part-time employees.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

14

Educational assistance payments made to workers to improve skills required of their jobs are nontaxable for unemployment purposes.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

15

FUTA and SUTA coverages extend to U.S. citizens working abroad for American employers.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

16

A traveling salesperson who solicits and transmits to the principal orders for merchandise for resale is considered an employee under FUTA.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

17

Christmas gifts, excluding noncash gifts of nominal value, are taxable wages for unemployment purposes.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

18

Once a company attains the status of employer for FUTA purposes, that status continues for four calendar years.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

19

Directors of corporations who only attend and participate in board of directors' meetings are not covered as employees under FUTA.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

20

For FUTA purposes, the cash value of remuneration paid in any medium other than cash is not considered taxable wages.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

21

Even if a state repays its Title XII advances, all employers in that state are subject to a credit reduction in the year of the advance.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

22

If a company is liable for a credit reduction (due to Title XII advance), this extra tax must be paid along with each of the required deposits made during the year.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

23

Currently, none of the states imposes an unemployment tax on employees.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

24

If an employer's quarterly tax liability is $525, it must be paid on or before the last day of the month following the end of the quarter.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

25

FUTA tax deposits cannot be paid electronically.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

26

On Form 940, even if the total FUTA tax is more than $500, there is no listing of quarterly federal unemployment tax liabilities.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

27

An employer can use a credit card to pay the balance with Form 940 (under $500.)

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

28

In most states, the contribution reports and the wage information reports are filed quarterly.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

29

An employer can use a credit card to pay the quarterly deposit of FUTA taxes during the year.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

30

If an employer pays unemployment taxes to two states, it will have the same SUTA tax rate in both states.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

31

Form 940 must be mailed to the IRS by January 15.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

32

There is a uniform rate of unemployment benefits payable by all states.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

33

Schedule A of Form 940 only has to be completed by employers who are subject to the Title XII credit reduction.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

34

Even if the duties of depositing the FUTA taxes and filing Form 940 have been outsourced, the employer is still the responsible party.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

35

In order to obtain the maximum credit allowed against the federal unemployment tax, the employer must have paid its SUTA contributions by the due date of Form 940.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

36

In some states, employers may obtain reduced unemployment compensation rates by making voluntary contributions to the state fund.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

37

If an employer is subject to a credit reduction because of Title XII advances, the penalty for the entire year will be paid only with the deposit for the last quarter of the year.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

38

Unlike Form 941, there is no penalty for the late filing of Form 940.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

39

The mailing of Form 940 is considered timely if it is postmarked on or before the due date.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

40

"Dumping" is legal in all but a few states.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

41

Voluntary contributions to a state's unemployment department are:

A) allowed in all states.

B) designed to increase an employer's reserve account in order to lower the employer's contribution rate.

C) capable of being paid at any time with no time limit.

D) returned to the employer at the end of the following year.

E) sent directly to the IRS.

A) allowed in all states.

B) designed to increase an employer's reserve account in order to lower the employer's contribution rate.

C) capable of being paid at any time with no time limit.

D) returned to the employer at the end of the following year.

E) sent directly to the IRS.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

42

Included under the definition of employees for FUTA purposes are:

A) independent contractors.

B) insurance agents paid solely on commission.

C) student nurses.

D) officers of a corporation.

E) members of partnerships.

A) independent contractors.

B) insurance agents paid solely on commission.

C) student nurses.

D) officers of a corporation.

E) members of partnerships.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

43

When making a payment of FUTA taxes, the employer must make the payment by the:

A) end of the month after the quarter.

B) 15th of the month after the quarter.

C) 10th of the month after the quarter.

D) end of the following quarter.

E) same day of the FICA and FIT deposits.

A) end of the month after the quarter.

B) 15th of the month after the quarter.

C) 10th of the month after the quarter.

D) end of the following quarter.

E) same day of the FICA and FIT deposits.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

44

An employer must pay the quarterly FUTA tax liability if the liability is more than:

A) $3,000.

B) $500.

C) $1,000.

D) $1.

E) $100.

A) $3,000.

B) $500.

C) $1,000.

D) $1.

E) $100.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

45

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Michael Mirer worked for Dawson Company for six months this year and earned $11,200. The other six months he earned $6,900 working for McBride Company (a separate company). The amount of FUTA taxes to be paid on Mirer's wages by the two companies is:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Michael Mirer worked for Dawson Company for six months this year and earned $11,200. The other six months he earned $6,900 working for McBride Company (a separate company). The amount of FUTA taxes to be paid on Mirer's wages by the two companies is:

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

46

In order to avoid a credit reduction for Title XII advances, a state must repay the loans by:

A) the end of the year of the loans.

B) the end of the year the credit reduction is scheduled to take effect.

C) the end of the third year after the year of the loans.

D) November 10 of the year the credit reduction is scheduled to take effect.

E) June 30 of the year after the loans.

A) the end of the year of the loans.

B) the end of the year the credit reduction is scheduled to take effect.

C) the end of the third year after the year of the loans.

D) November 10 of the year the credit reduction is scheduled to take effect.

E) June 30 of the year after the loans.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

47

An aspect of the interstate reciprocal arrangement concerns:

A) the status of Americans working overseas.

B) the taxability of dismissal payments.

C) the determination of an employer's experience rating.

D) the transfer of an employee from one state to another during the year.

E) none of the above.

A) the status of Americans working overseas.

B) the taxability of dismissal payments.

C) the determination of an employer's experience rating.

D) the transfer of an employee from one state to another during the year.

E) none of the above.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

48

A federal unemployment tax is levied on:

A) employees only.

B) both employers and employees.

C) employers only.

D) government employers only.

E) no one.

A) employees only.

B) both employers and employees.

C) employers only.

D) government employers only.

E) no one.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

49

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Stys Company's payroll for the year is $1,210,930. Of this amount, $510,710 is for wages paid in excess of $7,000 to each individual employee. The SUTA tax rate for the company is 3.2% on the first $7,000 of each employee's earnings.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Stys Company's payroll for the year is $1,210,930. Of this amount, $510,710 is for wages paid in excess of $7,000 to each individual employee. The SUTA tax rate for the company is 3.2% on the first $7,000 of each employee's earnings.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

50

For FUTA purposes, an employer can be any one of the following except :

A) an individual.

B) a partnership.

C) a trust.

D) a corporation.

E) All of the above can be employers.

A) an individual.

B) a partnership.

C) a trust.

D) a corporation.

E) All of the above can be employers.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

51

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . John Gercke is an employee of The Woolson Company. During the first part of the year, he earned $6,800 while working in State A. For the remainder of the year, the company transferred him to State B where he earned $16,500. The Woolson Company's tax rate in State A is 4.2%, and in State B it is 3.15% on the first $7,000. Assuming that reciprocal arrangements exist between the two states, determine the SUTA tax that the company paid to:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . John Gercke is an employee of The Woolson Company. During the first part of the year, he earned $6,800 while working in State A. For the remainder of the year, the company transferred him to State B where he earned $16,500. The Woolson Company's tax rate in State A is 4.2%, and in State B it is 3.15% on the first $7,000. Assuming that reciprocal arrangements exist between the two states, determine the SUTA tax that the company paid to:

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

52

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Niemann Company has a SUTA tax rate of 7.1%. The taxable payroll for the year for FUTA and SUTA is $82,600.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Niemann Company has a SUTA tax rate of 7.1%. The taxable payroll for the year for FUTA and SUTA is $82,600.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

53

If the employer is tardy in paying the state contributions, the credit against the federal tax is limited to what percent of the late payments that would have been allowed as a credit if the contributions had been paid on time?

A) 6.2%

B) 90%

C) 5.13%

D) 20%

E) 0%

A) 6.2%

B) 90%

C) 5.13%

D) 20%

E) 0%

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following payments are taxable payments for federal unemployment tax?

A) Christmas gifts, excluding noncash gifts of nominal value

B) Caddy fees

C) Courtesy discounts to employees and their families

D) Workers' compensation payments

E) Value of meals and lodging furnished employees for the convenience of the employer

A) Christmas gifts, excluding noncash gifts of nominal value

B) Caddy fees

C) Courtesy discounts to employees and their families

D) Workers' compensation payments

E) Value of meals and lodging furnished employees for the convenience of the employer

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is not a factor considered in determining coverage of interstate employees?

A) Location of base of operations

B) Place where work is localized

C) Location of company's payroll department

D) Location of employee's residence

E) Location of place from which operations are controlled

A) Location of base of operations

B) Place where work is localized

C) Location of company's payroll department

D) Location of employee's residence

E) Location of place from which operations are controlled

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following provides for a reduction in the employer's state unemployment tax rate based on the employer's experience with the risk of unemployment?

A) Voluntary contribution

B) Title XII advances

C) Pooled-fund laws

D) Experience-rating plan

E) None of the above

A) Voluntary contribution

B) Title XII advances

C) Pooled-fund laws

D) Experience-rating plan

E) None of the above

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following types of payments are not taxable wages for federal unemployment tax?

A) Retirement pay

B) Cash prizes and awards for doing outstanding work

C) Dismissal pay

D) Bonuses as remuneration for services

E) Payment under a guaranteed annual wage plan

A) Retirement pay

B) Cash prizes and awards for doing outstanding work

C) Dismissal pay

D) Bonuses as remuneration for services

E) Payment under a guaranteed annual wage plan

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

58

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Aaron Norman earned $24,900 for the year from Marcus Company. The company is subject to a SUTA tax of 4.7% on the first $9,900 of earnings. Determine:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Aaron Norman earned $24,900 for the year from Marcus Company. The company is subject to a SUTA tax of 4.7% on the first $9,900 of earnings. Determine:

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

59

If the employer has made timely deposits that pay the FUTA tax liability in full, the filing of Form 940 can be delayed until:

A) December 31.

B) February 15.

C) February 10.

D) February 1.

E) March 31.

A) December 31.

B) February 15.

C) February 10.

D) February 1.

E) March 31.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

60

The person who is not an authorized signer of Form 940 is:

A) the individual, if a sole proprietorship.

B) the accountant from the company's independent auditing firm.

C) the president, if a corporation.

D) a fiduciary, if a trust.

E) All of the above are authorized signers.

A) the individual, if a sole proprietorship.

B) the accountant from the company's independent auditing firm.

C) the president, if a corporation.

D) a fiduciary, if a trust.

E) All of the above are authorized signers.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

61

The payments of FUTA taxes are included with the payments of FICA and FIT taxes and are paid as one lump sum.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

62

The maximum credit that can be applied to the FUTA tax because of SUTA contributions is 5.4%.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

63

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Queno Company had FUTA taxable wages of $510,900 during the year. Determine its:

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Queno Company had FUTA taxable wages of $510,900 during the year. Determine its:

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

64

If an employer pays a SUTA tax of 2.0%, the total credit that can be claimed against the FUTA tax is 2.0%.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

65

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Faruga Company had FUTA taxable payrolls for the four quarters of $38,400; $29,600; $16,500; and $8,900, respectively. What was the amount of Faruga's first required deposit of FUTA taxes?

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Faruga Company had FUTA taxable payrolls for the four quarters of $38,400; $29,600; $16,500; and $8,900, respectively. What was the amount of Faruga's first required deposit of FUTA taxes?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

66

For the purpose of the FUTA tax, members of partnerships are considered employees.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

67

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Sparks Company's SUTA rate for next year is 3.25% because its reserve ratio falls into the state's 10% to less than 12% category [(contributions - benefits paid) ÷ average payroll = $414,867 ÷ $3,521,790 = 11.78%]. If the next bracket (12% to less than 14%) would give the company a lower tax rate of 3.05%, what would be the least amount of the voluntary contribution needed to qualify the company for the 3.05% SUTA tax rate?

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Sparks Company's SUTA rate for next year is 3.25% because its reserve ratio falls into the state's 10% to less than 12% category [(contributions - benefits paid) ÷ average payroll = $414,867 ÷ $3,521,790 = 11.78%]. If the next bracket (12% to less than 14%) would give the company a lower tax rate of 3.05%, what would be the least amount of the voluntary contribution needed to qualify the company for the 3.05% SUTA tax rate?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

68

In the case of an employee who changes jobs during the year, only the first employer must pay FUTA tax on that employee's earnings.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

69

FUTA coverage does not include service of any nature performed outside the United States by a citizen of the United States for an American employer.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

70

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . In the first quarter of the year, Henry Gibson earned $3,000 in wages and reported $2,400 in tips to his employer. How much would the employer's FUTA tax be for the first quarter on Gibson?

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . In the first quarter of the year, Henry Gibson earned $3,000 in wages and reported $2,400 in tips to his employer. How much would the employer's FUTA tax be for the first quarter on Gibson?

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

71

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

a. Complete Part 2 of Form 940 based on the following information: b. Complete Part 5 of Form 940 for the employer given the breakdown of FUTA taxable

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

a. Complete Part 2 of Form 940 based on the following information:

b. Complete Part 5 of Form 940 for the employer given the breakdown of FUTA taxable Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

72

A bonus paid as remuneration for services is not considered taxable wages for unemployment tax purposes even if the employee has not exceeded the taxable wage base.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

73

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Ted Carman worked for Rivertide Country Club and earned $28,500 during the year. He also worked part time for Harrison Furniture Company and earned $12,400 during the year. The SUTA tax rate for Rivertide Country Club is 4.2% on the first $8,000, and the rate for Harrison Furniture Company is 5.1% on the first $8,000. Calculate the FUTA and SUTA taxes paid by the employers on Carman's earnings.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Ted Carman worked for Rivertide Country Club and earned $28,500 during the year. He also worked part time for Harrison Furniture Company and earned $12,400 during the year. The SUTA tax rate for Rivertide Country Club is 4.2% on the first $8,000, and the rate for Harrison Furniture Company is 5.1% on the first $8,000. Calculate the FUTA and SUTA taxes paid by the employers on Carman's earnings.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

74

The federal unemployment tax is imposed on employers, and thus, is not deducted from employees' wages.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

75

If an employer's FUTA tax liability for the 1st quarter is $935, no payment is required for the 1st quarter.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

76

Employer contributions made to employees' 401(k) plans that are included in total payments on Form 940 are also then deducted as exempt payments.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

77

The location of the employee's residence is the primary factor to be considered in determining coverage of an employee who works in more than one state.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

78

Educational assistance payments to workers are considered nontaxable wages for unemployment purposes.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

79

E-pay or a major debit or credit card can be used to pay the required FUTA deposits during the year.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

80

Instruction 5-1

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Hunter Company had a FUTA taxable payroll of $192,700 for the year. Since the company is located in a state that has 1.5% FUTA credit reduction due to unpaid loans, determine Hunter's FUTA tax liability for the year.

Use the net FUTA tax rate of 0.6% on the first $7,000 of taxable wages.

Refer to Instruction 5-1 . Hunter Company had a FUTA taxable payroll of $192,700 for the year. Since the company is located in a state that has 1.5% FUTA credit reduction due to unpaid loans, determine Hunter's FUTA tax liability for the year.

Unlock Deck

Unlock for access to all 93 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 93 flashcards in this deck.