Deck 15: Accounting for Income Taxes

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Smiley Corporation purchased a machine on January 2, 2007, for $2,000,000. The machine has an estimated 5-year life with no salvage value. The straight-line method of depreciation is being used for financial statement purposes and the following MACRS amounts will be deducted for tax purposes:

Assuming an income tax rate of 30% for all years, the net deferred tax liability that should be reflected on Smiley's balance sheet at December 31, 2008, should be

Assuming an income tax rate of 30% for all years, the net deferred tax liability that should be reflected on Smiley's balance sheet at December 31, 2008, should be

A)

B)

C)

D)

Assuming an income tax rate of 30% for all years, the net deferred tax liability that should be reflected on Smiley's balance sheet at December 31, 2008, should beA)

B)

C)

D)

Question

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The income tax expense is

A) $150,000.

B) $225,000.

C) $250,000.

D) $500,000.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The income tax expense is

A) $150,000.

B) $225,000.

C) $250,000.

D) $500,000.

Question

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The deferred tax asset to be recognized is

A) $0.

B) $75,000 current.

C) $375,000 current.

D) $375,000 noncurrent.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The deferred tax asset to be recognized is

A) $0.

B) $75,000 current.

C) $375,000 current.

D) $375,000 noncurrent.

Question

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The deferred tax liability-current to be recognized is

A) $75,000.

B) $225,000.

C) $150,000.

D) $300,000.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The deferred tax liability-current to be recognized is

A) $75,000.

B) $225,000.

C) $150,000.

D) $300,000.

Question

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-Income tax payable is

A) $0.

B) $75,000.

C) $150,000.

D) $225,000.

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-Income tax payable is

A) $0.

B) $75,000.

C) $150,000.

D) $225,000.

Question

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-The deferred tax asset to be recognized is

A) $75,000 current.

B) $150,000 current.

C) $225,000 current.

D) $300,000 current.

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-The deferred tax asset to be recognized is

A) $75,000 current.

B) $150,000 current.

C) $225,000 current.

D) $300,000 current.

Question

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-The deferred tax liability to be recognized is

A)

B)

C)

D)

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-The deferred tax liability to be recognized is

A)

B)

C)

D)

Question

Markes Corporation's partial income statement after its first year of operations is as follows:

Markes uses the straight -line method of depreciation for financial reporting purposes and accelerated depreciation for tax purposes. The amount charged to depreciation expense on its books this year was $1,500,000. No other differences existed between book income and taxable income except for the amount of depreciation. Assuming a 30% tax rate, what amount was deducted for depreciation on the corporation's tax return for the current year?

Markes uses the straight -line method of depreciation for financial reporting purposes and accelerated depreciation for tax purposes. The amount charged to depreciation expense on its books this year was $1,500,000. No other differences existed between book income and taxable income except for the amount of depreciation. Assuming a 30% tax rate, what amount was deducted for depreciation on the corporation's tax return for the current year?

A) $1,200,000

B) $1,425,000

C) $1,500,000

D) $1,800,000

Markes uses the straight -line method of depreciation for financial reporting purposes and accelerated depreciation for tax purposes. The amount charged to depreciation expense on its books this year was $1,500,000. No other differences existed between book income and taxable income except for the amount of depreciation. Assuming a 30% tax rate, what amount was deducted for depreciation on the corporation's tax return for the current year?A) $1,200,000

B) $1,425,000

C) $1,500,000

D) $1,800,000

Question

Dwyer Company reported the following results for the year ended December 31, 2008, its first year of operations:

The disparity between book income and taxable income is attributable to a temporary difference which will reverse in 2009. What should Dwyer record as a net deferred tax asset or liability for the year ended December 31, 2008, assuming that the enacted tax rates in effect are 40% in 2008 and 35% in 2009?

The disparity between book income and taxable income is attributable to a temporary difference which will reverse in 2009. What should Dwyer record as a net deferred tax asset or liability for the year ended December 31, 2008, assuming that the enacted tax rates in effect are 40% in 2008 and 35% in 2009?

A) $180,000 deferred tax liability

B) $157,500 deferred tax asset

C) $180,000 deferred tax asset

D) $157,500 deferred tax liability

The disparity between book income and taxable income is attributable to a temporary difference which will reverse in 2009. What should Dwyer record as a net deferred tax asset or liability for the year ended December 31, 2008, assuming that the enacted tax rates in effect are 40% in 2008 and 35% in 2009?A) $180,000 deferred tax liability

B) $157,500 deferred tax asset

C) $180,000 deferred tax asset

D) $157,500 deferred tax liability

Question

Question

Question

O'Malley Corporation prepared the following reconciliation for its first year of operations:

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.

-What amount should be reported in its 2008 income statement as the deferred portion of the provision for income taxes?

A) $90,000 debit

B) $120,000 debit

C) $90,000 credit

D) $105,000 credit

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.-What amount should be reported in its 2008 income statement as the deferred portion of the provision for income taxes?

A) $90,000 debit

B) $120,000 debit

C) $90,000 credit

D) $105,000 credit

Question

O'Malley Corporation prepared the following reconciliation for its first year of operations:

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.

-In O'Malley's 2008 income statement, what amount should be reported for total income tax expense?

A) $330,000

B) $315,000

C) $300,000

D) $210,000

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.-In O'Malley's 2008 income statement, what amount should be reported for total income tax expense?

A) $330,000

B) $315,000

C) $300,000

D) $210,000

Question

Question

Question

Question

Question

Tyler Company made the following journal entry in late 2008 for rent on property it leases to Danford Corporation.

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%

-What amount of income tax expense should Tyler Company report at the end of 2008?

A) $53,000

B) $71,000

C) $81,500

D) $113,000

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%-What amount of income tax expense should Tyler Company report at the end of 2008?

A) $53,000

B) $71,000

C) $81,500

D) $113,000

Question

Tyler Company made the following journal entry in late 2008 for rent on property it leases to Danford Corporation.

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%

-Assuming the taxes payable at the end of 2009 is $102,000, what amount of income tax expense would Tyler Company record for 2009?

A) $81,000

B) $91,500

C) $112,500

D) $123,000

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%-Assuming the taxes payable at the end of 2009 is $102,000, what amount of income tax expense would Tyler Company record for 2009?

A) $81,000

B) $91,500

C) $112,500

D) $123,000

Question

The following information is available for Nielsen Company after its first year of operations:

Nielsen estimates its annual warranty expense as a percentage of sales. The amount charged to warranty expense on its books was $95,000. Assuming a 40% income tax rate, what amount was actually paid this year for warranty claims?

Nielsen estimates its annual warranty expense as a percentage of sales. The amount charged to warranty expense on its books was $95,000. Assuming a 40% income tax rate, what amount was actually paid this year for warranty claims?

A) $105,000

B) $100,000

C) $95,000

D) $85,000

Nielsen estimates its annual warranty expense as a percentage of sales. The amount charged to warranty expense on its books was $95,000. Assuming a 40% income tax rate, what amount was actually paid this year for warranty claims?A) $105,000

B) $100,000

C) $95,000

D) $85,000

Question

Kubitz Company reported the following items on its income statement for the year ended December 31, 2008.

For Kubitz Company the amount of temporary differences used to measure deferred income taxes amount to

For Kubitz Company the amount of temporary differences used to measure deferred income taxes amount to

A) $0.

B) $11,000.

C) $16,000.

D) $27,000.

For Kubitz Company the amount of temporary differences used to measure deferred income taxes amount toA) $0.

B) $11,000.

C) $16,000.

D) $27,000.

Question

Question

Question

Question

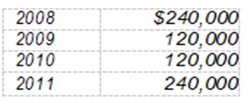

A reconciliation of Reaker Company's pretax accounting income with its taxable income for 2008, its first year of operations, is as follows:

The excess tax depreciation will result in equal net taxable amounts in each of the next three years. Enacted tax rates are 40% in 2008, 35% in 2009 and 2010, and 30% in 2011. The total deferred tax liability to be reported on Reaker's balance sheet at December 31, 2008, is

The excess tax depreciation will result in equal net taxable amounts in each of the next three years. Enacted tax rates are 40% in 2008, 35% in 2009 and 2010, and 30% in 2011. The total deferred tax liability to be reported on Reaker's balance sheet at December 31, 2008, is

A) $36,000.

B) $30,000.

C) $31,500.

D) $27,000.

The excess tax depreciation will result in equal net taxable amounts in each of the next three years. Enacted tax rates are 40% in 2008, 35% in 2009 and 2010, and 30% in 2011. The total deferred tax liability to be reported on Reaker's balance sheet at December 31, 2008, isA) $36,000.

B) $30,000.

C) $31,500.

D) $27,000.

Question

Mast, Inc. reports a taxable and financial loss of $650,000 for 2009. Its pretax financial income for the last two years was as follows:

The amount that Mast, Inc. reports as a net loss for financial reporting purposes in 2009, assuming that it uses the carryback provisions, and that the tax rate is 30% for all periods affected, is

The amount that Mast, Inc. reports as a net loss for financial reporting purposes in 2009, assuming that it uses the carryback provisions, and that the tax rate is 30% for all periods affected, is

A) $650,000 loss.

B) $0.

C) $195,000 loss.

D) $455,000 loss.

The amount that Mast, Inc. reports as a net loss for financial reporting purposes in 2009, assuming that it uses the carryback provisions, and that the tax rate is 30% for all periods affected, isA) $650,000 loss.

B) $0.

C) $195,000 loss.

D) $455,000 loss.

Question

Peck Co. reports a taxable and pretax financial loss of $400,000 for 2009. Peck's taxable and pretax financial income and tax rates for the last two years were:

The amount that Peck should report as an income tax refund receivable in 2009, assuming that it uses the carryback provisions and that the tax rate is 40% in 2009, is

The amount that Peck should report as an income tax refund receivable in 2009, assuming that it uses the carryback provisions and that the tax rate is 40% in 2009, is

A) $120,000.

B) $140,000.

C) $160,000.

D) $180,000.

The amount that Peck should report as an income tax refund receivable in 2009, assuming that it uses the carryback provisions and that the tax rate is 40% in 2009, isA) $120,000.

B) $140,000.

C) $160,000.

D) $180,000.

Question

Bennington Corporation began operations in 2004. There have been no permanent or temporary differences to account for since the inception of the business. The following data are available:

In 2008, Bennington had an operating loss of $930,000. What amount of income tax benefits should be reported on the 2008 income statement due to this loss?

In 2008, Bennington had an operating loss of $930,000. What amount of income tax benefits should be reported on the 2008 income statement due to this loss?

A) $409,500

B) $373,500

C) $372,000

D) $279,000

In 2008, Bennington had an operating loss of $930,000. What amount of income tax benefits should be reported on the 2008 income statement due to this loss?A) $409,500

B) $373,500

C) $372,000

D) $279,000

Question

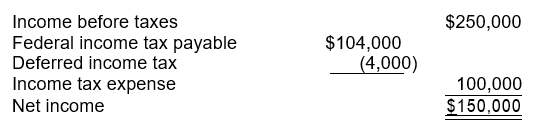

Ramos Corp.'s books showed pretax financial income of $1,500,000 for the year ended December 31, 2008. In the computation of federal income taxes, the following data were considered:  What amount should Ramos report as its current federal income tax liability on its December 31, 2008 balance sheet?

What amount should Ramos report as its current federal income tax liability on its December 31, 2008 balance sheet?

A) $100,000

B) $130,000

C) $225,000

D) $255,000

What amount should Ramos report as its current federal income tax liability on its December 31, 2008 balance sheet?A) $100,000

B) $130,000

C) $225,000

D) $255,000

Question

Eddy Corp.'s 2008 income statement showed pretax accounting income of $750,000. To compute the federal income tax liability, the following 2008 data are provided:  What amount of current federal income tax liability should be included in Eddy's December 31, 2008 balance sheet?

What amount of current federal income tax liability should be included in Eddy's December 31, 2008 balance sheet?

A) $48,000

B) $66,000

C) $75,000

D) $198,000

What amount of current federal income tax liability should be included in Eddy's December 31, 2008 balance sheet?A) $48,000

B) $66,000

C) $75,000

D) $198,000

Question

Question

Question

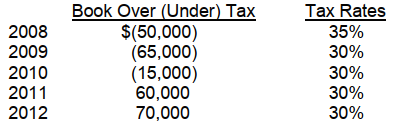

Brock Corp.'s 2008 income statement had pretax financial income of $250,000 in its first year of operations. Brock uses an accelerated cost recovery method on its tax return and straight-line depreciation for financial reporting. The differences between the book and tax deductions for depreciation over the five-year life of the assets acquired in 2008, and the enacted tax rates for 2008 to 2012 are as follows:  There are no other temporary differences. In Brock's December 31, 2008 balance sheet, the noncurrent deferred income tax liability and the income taxes currently payable should be

There are no other temporary differences. In Brock's December 31, 2008 balance sheet, the noncurrent deferred income tax liability and the income taxes currently payable should be

A)

B)

C)

D)

There are no other temporary differences. In Brock's December 31, 2008 balance sheet, the noncurrent deferred income tax liability and the income taxes currently payable should beA)

B)

C)

D)

Question

Question

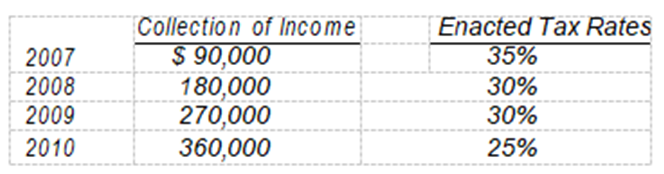

Karr, Inc. uses the accrual method of accounting for financial reporting purposes and appropriately uses the installment method of accounting for income tax purposes. Installment income of $900,000 will be collected in the following years when the enacted tax rates are:  The installment income is Karr's only temporary difference. What amount should be included in the deferred income tax liability in Karr's December 31, 2007 balance sheet?

The installment income is Karr's only temporary difference. What amount should be included in the deferred income tax liability in Karr's December 31, 2007 balance sheet?

A) $225,000

B) $256,500

C) $283,500

D) $315,000

The installment income is Karr's only temporary difference. What amount should be included in the deferred income tax liability in Karr's December 31, 2007 balance sheet?A) $225,000

B) $256,500

C) $283,500

D) $315,000

Question

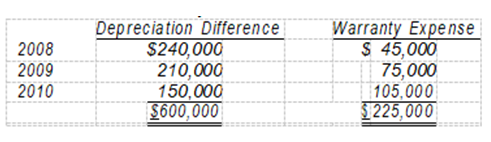

For calendar year 2007, Neer Corp. reported depreciation of $1,200,000 in its income statement. On its 2007 income tax return, Neer reported depreciation of $1,800,000. Neer's income statement also included $225,000 accrued warranty expense that will be deducted for tax purposes when paid. Neer's enacted tax rates are 30% for 2007 and 2008, and 24% for 2009 and 2010. The depreciation difference and warranty expense will reverse over the next three years as follows:  These were Neer's only temporary differences. In Neer's 2007 income statement, the deferred portion of its provision for income taxes should be

These were Neer's only temporary differences. In Neer's 2007 income statement, the deferred portion of its provision for income taxes should be

A) $200,700.

B) $112,500.

C) $101,700.

D) $109,800.

These were Neer's only temporary differences. In Neer's 2007 income statement, the deferred portion of its provision for income taxes should beA) $200,700.

B) $112,500.

C) $101,700.

D) $109,800.

Question

Nevitt Co., organized on January 2, 2007, had pretax accounting income of $880,000 and taxable income of $1,600,000 for the year ended December 31, 2007. The only temporary difference is accrued product warranty costs which are expected to be paid as follows:  The enacted income tax rates are 35% for 2007, 30% for 2008 through 2010, and 25% for 2011. If Nevitt expects taxable income in future years, the deferred tax asset in Nevitt's December 31, 2007 balance sheet should be

The enacted income tax rates are 35% for 2007, 30% for 2008 through 2010, and 25% for 2011. If Nevitt expects taxable income in future years, the deferred tax asset in Nevitt's December 31, 2007 balance sheet should be

A) $144,000.

B) $168,000.

C) $204,000.

D) $252,000.

The enacted income tax rates are 35% for 2007, 30% for 2008 through 2010, and 25% for 2011. If Nevitt expects taxable income in future years, the deferred tax asset in Nevitt's December 31, 2007 balance sheet should beA) $144,000.

B) $168,000.

C) $204,000.

D) $252,000.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/69

Play

Full screen (f)

Deck 15: Accounting for Income Taxes

1

When the book amount of an asset or liability differs from the tax basis as a result of a temporary difference, the future tax effects on taxable income must be reported solely in the future financial statement that the difference affects.

False

2

A deferred tax liability is the amount of deferred tax consequences attributable to existing temporary differences that will result in net taxable amounts in future years.

True

3

An objective of accounting for income taxes is to recognize deferred tax liabilities and assets for the future tax consequences of events that have already been recognized in the financial statements.

True

4

All positive and negative information should be considered in determining whether a valuation allowance is needed.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

5

An originating temporary difference is the initial difference that occurs when the book basis of an asset exceeds, but is not exceeded by, the tax basis of a liability.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

6

A reversing difference occurs when a temporary difference that originated in prior periods is eliminated and the related tax effect is removed from the deferred tax account.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

7

A permanent difference results when the tax laws cause an item reported on the income statement to be different from that same item reported on the balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

8

A corporation that has tax-free income has an effective tax rate that is less than the statutory (regular) tax rate.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

9

In computing deferred income taxes, a new tax rate should be used if (a) it is probable that a future tax rate change will occur, and (b) the rate is reasonably estimable.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

10

In general, the tax benefits of loss carryforwards should not be recognized in the loss year when the benefits arise, but rather in the year they are realized.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

11

The only way a tax loss carryforward can be recognized in the current year is when an entity has incurred net losses during the past three calendar years and has no ability to carry any of the loss back.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

12

In classifying deferred taxes on the balance sheet, an entity should net the current deferred tax asset and liability amount and net the noncurrent deferred tax asset and liability amount thus reporting only one current and one noncurrent deferred tax amount.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

13

The asset-liability approach to accounting for income taxes requires a journal entry at the end of each year which either increases an asset or decreases a liability.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

14

Interperiod income tax allocation causes

A) tax expense shown on the income statement to equal the amount of income taxes payable for the current year plus or minus the change in the deferred tax asset or liability balances for the year.

B) tax expense shown in the income statement to bear a normal relation to the tax liability.

C) tax liability shown in the balance sheet to bear a normal relation to the income before tax reported in the income statement.

D) tax expense in the income statement to be presented with the specific revenues causing the tax.

A) tax expense shown on the income statement to equal the amount of income taxes payable for the current year plus or minus the change in the deferred tax asset or liability balances for the year.

B) tax expense shown in the income statement to bear a normal relation to the tax liability.

C) tax liability shown in the balance sheet to bear a normal relation to the income before tax reported in the income statement.

D) tax expense in the income statement to be presented with the specific revenues causing the tax.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

15

The rationale for interperiod income tax allocation is to

A) recognize a tax asset or liability for the tax consequences of temporary differences that exist at the balance sheet date.

B) recognize a distribution of earnings to the taxing agency.

C) reconcile the tax consequences of permanent and temporary differences appearing on the current year's financial statements.

D) adjust income tax expense on the income statement to be in agreement with income taxes payable on the balance sheet.

A) recognize a tax asset or liability for the tax consequences of temporary differences that exist at the balance sheet date.

B) recognize a distribution of earnings to the taxing agency.

C) reconcile the tax consequences of permanent and temporary differences appearing on the current year's financial statements.

D) adjust income tax expense on the income statement to be in agreement with income taxes payable on the balance sheet.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

16

Interperiod tax allocation results in a deferred tax liability from

A) an income item partially recognized for financial purposes but fully recognized for tax purposes in any one year.

B) the amount of deferred tax consequences attributed to temporary differences that result in net deductible amounts in future years.

C) an income item fully recognized for tax and financial purposes in any one year.

D) the amount of deferred tax consequences attributed to temporary differences that result in net taxable amounts in future years.

A) an income item partially recognized for financial purposes but fully recognized for tax purposes in any one year.

B) the amount of deferred tax consequences attributed to temporary differences that result in net deductible amounts in future years.

C) an income item fully recognized for tax and financial purposes in any one year.

D) the amount of deferred tax consequences attributed to temporary differences that result in net taxable amounts in future years.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following situations would require interperiod income tax allocation procedures?

A) An excess of percentage depletion over cost depletion

B) Interest received on municipal bonds

C) A temporary difference exists at the balance sheet date because the tax basis of an asset or liability and its reported amount in the financial statements differ

D) Proceeds from a life insurance policy on an officer

A) An excess of percentage depletion over cost depletion

B) Interest received on municipal bonds

C) A temporary difference exists at the balance sheet date because the tax basis of an asset or liability and its reported amount in the financial statements differ

D) Proceeds from a life insurance policy on an officer

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

18

Interperiod income tax allocation procedures are appropriate when

A) an extraordinary loss will cause the amount of income tax expense to be less than the tax on ordinary net income.

B) an extraordinary gain will cause the amount of income tax expense to be greater than the tax on ordinary net income.

C) differences between net income for tax purposes and financial reporting occur because tax laws and financial accounting principles do not concur on the items to be recognized as revenue and expense.

D) differences between net income for tax purposes and financial reporting occur because, even though financial accounting principles and tax laws concur on the item to be recognized as revenues and expenses, they don't concur on the timing of the recognition.

A) an extraordinary loss will cause the amount of income tax expense to be less than the tax on ordinary net income.

B) an extraordinary gain will cause the amount of income tax expense to be greater than the tax on ordinary net income.

C) differences between net income for tax purposes and financial reporting occur because tax laws and financial accounting principles do not concur on the items to be recognized as revenue and expense.

D) differences between net income for tax purposes and financial reporting occur because, even though financial accounting principles and tax laws concur on the item to be recognized as revenues and expenses, they don't concur on the timing of the recognition.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

19

Interperiod tax allocation would not be required when

A) costs are written off in the year of the expenditure for tax purposes but capitalized for accounting purposes.

B) statutory (or percentage) depletion exceeds cost depletion for the period.

C) different methods of revenue recognition arise for tax purposes and accounting purposes.

D) different depreciable lives are used for machinery for tax and accounting purposes.

A) costs are written off in the year of the expenditure for tax purposes but capitalized for accounting purposes.

B) statutory (or percentage) depletion exceeds cost depletion for the period.

C) different methods of revenue recognition arise for tax purposes and accounting purposes.

D) different depreciable lives are used for machinery for tax and accounting purposes.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

20

In terms of FASB Statement of Financial Accounting Concepts No. 6, a deferred tax

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

21

At the December 31, 2007 balance sheet date, Garth Brooks Corporation reports an accrued receivable for financial reporting purposes but not for tax purposes. When this asset is recovered in 2008, a future taxable amount will occur and

A) pretax financial income will exceed taxable income in 2008.

B) Garth will record a decrease in a deferred tax liability in 2008.

C) total income tax expense for 2008 will exceed current tax expense for 2008.

D) Garth will record an increase in a deferred tax asset in 2008.

A) pretax financial income will exceed taxable income in 2008.

B) Garth will record a decrease in a deferred tax liability in 2008.

C) total income tax expense for 2008 will exceed current tax expense for 2008.

D) Garth will record an increase in a deferred tax asset in 2008.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

22

Assuming a 40% statutory tax rate applies to all years involved, which of the following situations will give rise to reporting a deferred tax liability on the balance sheet?

I. A revenue is deferred for financial reporting purposes but not for tax purposes.

II. A revenue is deferred for tax purposes but not for financial reporting purposes.

III. An expense is deferred for financial reporting purposes but not for tax purposes.

IV. An expense is deferred for tax purposes but not for financial reporting purposes.

A) item II only

B) items I and II only

C) items II and III only

D) items I and IV only

I. A revenue is deferred for financial reporting purposes but not for tax purposes.

II. A revenue is deferred for tax purposes but not for financial reporting purposes.

III. An expense is deferred for financial reporting purposes but not for tax purposes.

IV. An expense is deferred for tax purposes but not for financial reporting purposes.

A) item II only

B) items I and II only

C) items II and III only

D) items I and IV only

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

23

A major distinction between temporary and permanent differences is

A) permanent differences are not representative of acceptable accounting practice.

B) temporary differences occur frequently, whereas permanent differences occur only once.

C) once an item is determined to be a temporary difference, it maintains that status; however, a permanent difference can change in status with the passage of time.

D) temporary differences reverse themselves in subsequent accounting periods, whereas permanent differences do not reverse.

A) permanent differences are not representative of acceptable accounting practice.

B) temporary differences occur frequently, whereas permanent differences occur only once.

C) once an item is determined to be a temporary difference, it maintains that status; however, a permanent difference can change in status with the passage of time.

D) temporary differences reverse themselves in subsequent accounting periods, whereas permanent differences do not reverse.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

24

Renner Corporation's taxable income differed from its accounting income computed for this past year. An item that would create a permanent difference in accounting and taxable incomes for Renner would be

A) a balance in the Unearned Rent account at year end.

B) using accelerated depreciation for tax purposes and straight-line depreciation for book purposes.

C) a fine resulting from violations of OSHA regulations.

D) making installment sales during the year.

A) a balance in the Unearned Rent account at year end.

B) using accelerated depreciation for tax purposes and straight-line depreciation for book purposes.

C) a fine resulting from violations of OSHA regulations.

D) making installment sales during the year.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

25

The use of accelerated depreciation for tax purposes and straight-line depreciation for accounting purposes results in

A) a larger amount of depreciation expense shown on the tax return than on the income statement, over the asset's useful life.

B) the asset being fully depreciated for tax purposes in half the time it takes to become fully depreciated for accounting purposes.

C) a larger amount of depreciation expense shown on the income statement than on the tax return in the last year of the asset's useful life.

D) a loss on the sale of the asset in question if it is sold for its book value before its useful life expires.

A) a larger amount of depreciation expense shown on the tax return than on the income statement, over the asset's useful life.

B) the asset being fully depreciated for tax purposes in half the time it takes to become fully depreciated for accounting purposes.

C) a larger amount of depreciation expense shown on the income statement than on the tax return in the last year of the asset's useful life.

D) a loss on the sale of the asset in question if it is sold for its book value before its useful life expires.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is a permanent difference that is recognized for tax purposes but not for financial reporting purposes?

A) The deduction for dividends received from U.S. corporations.

B) Interest received on state and municipal bonds.

C) Compensation expense associated with certain employee stock options.

D) A litigation accrual.

A) The deduction for dividends received from U.S. corporations.

B) Interest received on state and municipal bonds.

C) Compensation expense associated with certain employee stock options.

D) A litigation accrual.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

27

When a change in the tax rate is enacted into law, its effect on existing deferred income tax accounts should be

A) handled retroactively in accordance with the guidance related to changes in accounting principles.

B) considered, but it should only be recorded in the accounts if it reduces a deferred tax liability or increases a deferred tax asset.

C) reported as an adjustment to tax expense in the period of change.

D) applied to all temporary or permanent differences that arise prior to the date of the enactment of the tax rate change, but not subsequent to the date of the change.

A) handled retroactively in accordance with the guidance related to changes in accounting principles.

B) considered, but it should only be recorded in the accounts if it reduces a deferred tax liability or increases a deferred tax asset.

C) reported as an adjustment to tax expense in the period of change.

D) applied to all temporary or permanent differences that arise prior to the date of the enactment of the tax rate change, but not subsequent to the date of the change.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

28

A net operating loss occurs for tax purposes in a year when tax-deductible expenses exceed taxable revenues. Under certain circumstances the federal tax laws permit taxpayers to use the losses of one year to offset the profits of other years. For what period of time can net operating losses be offset against prior or future years' profits?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

29

Tanner, Inc. incurred a financial and taxable loss for 2007. Tanner therefore decided to use the carryback provisions as it had been profitable up to this year. How should the amounts related to the carryback be reported in the 2007 financial statements?

A) The reduction of the loss should be reported as a prior period adjustment.

B) The refund claimed should be reported as a deferred charge and amortized over five years.

C) The refund claimed should be reported as revenue in the current year.

D) The refund claimed should be shown as a reduction of the loss in 2007.

A) The reduction of the loss should be reported as a prior period adjustment.

B) The refund claimed should be reported as a deferred charge and amortized over five years.

C) The refund claimed should be reported as revenue in the current year.

D) The refund claimed should be shown as a reduction of the loss in 2007.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

30

A deferred tax liability is classified on the balance sheet as either a current or a noncurrent liability. The current amount of a deferred tax liability should generally be

A) the net deferred tax consequences of temporary differences that will result in net taxable amounts during the next year.

B) totally eliminated from the financial statements if the amount is related to a noncurrent asset.

C) based on the classification of the related asset or liability for financial reporting purposes.

D) the total of all deferred tax consequences that are not expected to reverse in the operating period or one year, whichever is greater.

A) the net deferred tax consequences of temporary differences that will result in net taxable amounts during the next year.

B) totally eliminated from the financial statements if the amount is related to a noncurrent asset.

C) based on the classification of the related asset or liability for financial reporting purposes.

D) the total of all deferred tax consequences that are not expected to reverse in the operating period or one year, whichever is greater.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

31

In 2008, Delaney Company had revenues of $180,000 for book purposes and $150,000 for tax purposes. Delaney also had expenses of $100,000 for both book and tax purposes. If Delaney has a 35% tax rate, what is Delaney's income tax payable for 2008?

A) $10,500

B) $17,500

C) $28,000

D) $35,000

A) $10,500

B) $17,500

C) $28,000

D) $35,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

32

Maureen Corporation reports income before taxes of $500,000 in its income statement, but because of temporary differences taxable income is only $200,000. If the tax rate is 45%, what amount of net income should the corporation report?

A) $337,500

B) $275,000

C) $225,000

D) $90,000

A) $337,500

B) $275,000

C) $225,000

D) $90,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

33

Smiley Corporation purchased a machine on January 2, 2007, for $2,000,000. The machine has an estimated 5-year life with no salvage value. The straight-line method of depreciation is being used for financial statement purposes and the following MACRS amounts will be deducted for tax purposes:

Assuming an income tax rate of 30% for all years, the net deferred tax liability that should be reflected on Smiley's balance sheet at December 31, 2008, should be

A)

B)

C)

D)

Assuming an income tax rate of 30% for all years, the net deferred tax liability that should be reflected on Smiley's balance sheet at December 31, 2008, should beA)

B)

C)

D)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

34

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The income tax expense is

A) $150,000.

B) $225,000.

C) $250,000.

D) $500,000.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The income tax expense is

A) $150,000.

B) $225,000.

C) $250,000.

D) $500,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

35

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The deferred tax asset to be recognized is

A) $0.

B) $75,000 current.

C) $375,000 current.

D) $375,000 noncurrent.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The deferred tax asset to be recognized is

A) $0.

B) $75,000 current.

C) $375,000 current.

D) $375,000 noncurrent.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

36

Hefner Co. at the end of 2008, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.

-The deferred tax liability-current to be recognized is

A) $75,000.

B) $225,000.

C) $150,000.

D) $300,000.

The estimated litigation expense of $1,250,000 will be deductible in 2010 when it is expected to be paid. The gross profit from the installment sales will be realized in the amount of $500,000 in each of the next two years. The estimated liability for litigation is classified as noncurrent and the installment accounts receivable are classified as $500,000 current and $500,000 noncurrent. The income tax rate is 30% for all years.-The deferred tax liability-current to be recognized is

A) $75,000.

B) $225,000.

C) $150,000.

D) $300,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

37

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-Income tax payable is

A) $0.

B) $75,000.

C) $150,000.

D) $225,000.

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-Income tax payable is

A) $0.

B) $75,000.

C) $150,000.

D) $225,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

38

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-The deferred tax asset to be recognized is

A) $75,000 current.

B) $150,000 current.

C) $225,000 current.

D) $300,000 current.

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-The deferred tax asset to be recognized is

A) $75,000 current.

B) $150,000 current.

C) $225,000 current.

D) $300,000 current.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

39

Frizell Co. at the end of 2007, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows:

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.

-The deferred tax liability to be recognized is

A)

B)

C)

D)

The estimated litigation expense of $1,000,000 will be deductible in 2008 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years.-The deferred tax liability to be recognized is

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

40

Markes Corporation's partial income statement after its first year of operations is as follows:

Markes uses the straight -line method of depreciation for financial reporting purposes and accelerated depreciation for tax purposes. The amount charged to depreciation expense on its books this year was $1,500,000. No other differences existed between book income and taxable income except for the amount of depreciation. Assuming a 30% tax rate, what amount was deducted for depreciation on the corporation's tax return for the current year?

A) $1,200,000

B) $1,425,000

C) $1,500,000

D) $1,800,000

Markes uses the straight -line method of depreciation for financial reporting purposes and accelerated depreciation for tax purposes. The amount charged to depreciation expense on its books this year was $1,500,000. No other differences existed between book income and taxable income except for the amount of depreciation. Assuming a 30% tax rate, what amount was deducted for depreciation on the corporation's tax return for the current year?A) $1,200,000

B) $1,425,000

C) $1,500,000

D) $1,800,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

41

Dwyer Company reported the following results for the year ended December 31, 2008, its first year of operations:

The disparity between book income and taxable income is attributable to a temporary difference which will reverse in 2009. What should Dwyer record as a net deferred tax asset or liability for the year ended December 31, 2008, assuming that the enacted tax rates in effect are 40% in 2008 and 35% in 2009?

A) $180,000 deferred tax liability

B) $157,500 deferred tax asset

C) $180,000 deferred tax asset

D) $157,500 deferred tax liability

The disparity between book income and taxable income is attributable to a temporary difference which will reverse in 2009. What should Dwyer record as a net deferred tax asset or liability for the year ended December 31, 2008, assuming that the enacted tax rates in effect are 40% in 2008 and 35% in 2009?A) $180,000 deferred tax liability

B) $157,500 deferred tax asset

C) $180,000 deferred tax asset

D) $157,500 deferred tax liability

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

42

In 2008, Admire Company accrued, for financial statement reporting, estimated losses on disposal of unused plant facilities of $1,500,000. The facilities were sold in March 2009 and a $1,500,000 loss was recognized for tax purposes. Also in 2008, Admire paid $100,000 in premiums for a two-year life insurance policy in which the company was the beneficiary. Assuming that the enacted tax rate is 30% in both 2008 and 2009, and that Admire paid $780,000 in income taxes in 2008, the amount reported as net deferred income taxes on Admire's balance sheet at December 31, 2008, should be a

A) $420,000 asset.

B) $360,000 asset.

C) $360,000 liability.

D) $450,000 asset.

A) $420,000 asset.

B) $360,000 asset.

C) $360,000 liability.

D) $450,000 asset.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

43

Gleim Inc. has a deductible temporary difference of $100,000 at the end of its first year of operations. Its tax rate is 40%. Income taxes payable are $90,000. Gleim properly recorded a deferred tax asset. Later, after careful review of all available evidence, it is determined that it is more likely than not that $15,000 of the deferred tax asset will not be realized. What entry should Gleim make to record the reduction in asset value?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

44

O'Malley Corporation prepared the following reconciliation for its first year of operations:

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.

-What amount should be reported in its 2008 income statement as the deferred portion of the provision for income taxes?

A) $90,000 debit

B) $120,000 debit

C) $90,000 credit

D) $105,000 credit

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.-What amount should be reported in its 2008 income statement as the deferred portion of the provision for income taxes?

A) $90,000 debit

B) $120,000 debit

C) $90,000 credit

D) $105,000 credit

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

45

O'Malley Corporation prepared the following reconciliation for its first year of operations:

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.

-In O'Malley's 2008 income statement, what amount should be reported for total income tax expense?

A) $330,000

B) $315,000

C) $300,000

D) $210,000

The temporary difference will reverse evenly over the next two years at an enacted tax rate of 40%. The enacted tax rate for 2008 is 35%.-In O'Malley's 2008 income statement, what amount should be reported for total income tax expense?

A) $330,000

B) $315,000

C) $300,000

D) $210,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

46

Jesse Company sells household furniture. Customers who purchase furniture on the installment basis make payments in equal monthly installments over a two-year period, with no down payment required. Jesse's gross profit on installment sales equals 40% of the selling price of the furniture.

For financial accounting purposes, sales revenue is recognized at the time the sale is made. For income tax purposes, however, the installment method is used. There are no other book and income tax accounting differences, and Jesse's income tax rate is 30%.

If Jesse's December 31, 2008, balance sheet includes a deferred tax liability of $300,000 arising from the difference between book and tax treatment of the installment sales, it should also include installment accounts receivable of

A) $2,500,000.

B) $1,000,000.

C) $750,000.

D) $300,000.

For financial accounting purposes, sales revenue is recognized at the time the sale is made. For income tax purposes, however, the installment method is used. There are no other book and income tax accounting differences, and Jesse's income tax rate is 30%.

If Jesse's December 31, 2008, balance sheet includes a deferred tax liability of $300,000 arising from the difference between book and tax treatment of the installment sales, it should also include installment accounts receivable of

A) $2,500,000.

B) $1,000,000.

C) $750,000.

D) $300,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

47

McGee Company deducts insurance expense of $84,000 for tax purposes in 2008, but the expense is not yet recognized for accounting purposes. In 2009, 2010, and 2011, no insurance expense will be deducted for tax purposes, but $28,000 of insurance expense will be reported for accounting purposes in each of these years. McGee Company has a tax rate of 40% and income taxes payable of $72,000 at the end of 2008. There were no deferred taxes at the beginning of 2008.

-What is the amount of the deferred tax liability at the end of 2008?

A) $33,600

B) $28,800

C) $12,000

D) $0

-What is the amount of the deferred tax liability at the end of 2008?

A) $33,600

B) $28,800

C) $12,000

D) $0

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

48

McGee Company deducts insurance expense of $84,000 for tax purposes in 2008, but the expense is not yet recognized for accounting purposes. In 2009, 2010, and 2011, no insurance expense will be deducted for tax purposes, but $28,000 of insurance expense will be reported for accounting purposes in each of these years. McGee Company has a tax rate of 40% and income taxes payable of $72,000 at the end of 2008. There were no deferred taxes at the beginning of 2008.

-What is the amount of income tax expense for 2008?

A) $105,600

B) $100,800

C) $84,000

D) $72,000

-What is the amount of income tax expense for 2008?

A) $105,600

B) $100,800

C) $84,000

D) $72,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

49

McGee Company deducts insurance expense of $84,000 for tax purposes in 2008, but the expense is not yet recognized for accounting purposes. In 2009, 2010, and 2011, no insurance expense will be deducted for tax purposes, but $28,000 of insurance expense will be reported for accounting purposes in each of these years. McGee Company has a tax rate of 40% and income taxes payable of $72,000 at the end of 2008. There were no deferred taxes at the beginning of 2008.

-Assuming that income tax payable for 2009 is $96,000, the income tax expense for 2009 would be what amount?

A) $129,600

B) $107,200

C) $96,000

D) $84,800

-Assuming that income tax payable for 2009 is $96,000, the income tax expense for 2009 would be what amount?

A) $129,600

B) $107,200

C) $96,000

D) $84,800

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

50

Tyler Company made the following journal entry in late 2008 for rent on property it leases to Danford Corporation.

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%

-What amount of income tax expense should Tyler Company report at the end of 2008?

A) $53,000

B) $71,000

C) $81,500

D) $113,000

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%-What amount of income tax expense should Tyler Company report at the end of 2008?

A) $53,000

B) $71,000

C) $81,500

D) $113,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

51

Tyler Company made the following journal entry in late 2008 for rent on property it leases to Danford Corporation.

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%

-Assuming the taxes payable at the end of 2009 is $102,000, what amount of income tax expense would Tyler Company record for 2009?

A) $81,000

B) $91,500

C) $112,500

D) $123,000

The payment represents rent for the years 2009 and 2010, the period covered by the lease. Tyler Company is a cash basis taxpayer. Tyler has income tax payable of $92,000 at the end of 2008, and its tax rate is 35%-Assuming the taxes payable at the end of 2009 is $102,000, what amount of income tax expense would Tyler Company record for 2009?

A) $81,000

B) $91,500

C) $112,500

D) $123,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

52

The following information is available for Nielsen Company after its first year of operations:

Nielsen estimates its annual warranty expense as a percentage of sales. The amount charged to warranty expense on its books was $95,000. Assuming a 40% income tax rate, what amount was actually paid this year for warranty claims?

A) $105,000

B) $100,000

C) $95,000

D) $85,000

Nielsen estimates its annual warranty expense as a percentage of sales. The amount charged to warranty expense on its books was $95,000. Assuming a 40% income tax rate, what amount was actually paid this year for warranty claims?A) $105,000

B) $100,000

C) $95,000

D) $85,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

53

Kubitz Company reported the following items on its income statement for the year ended December 31, 2008.

For Kubitz Company the amount of temporary differences used to measure deferred income taxes amount to

A) $0.

B) $11,000.

C) $16,000.

D) $27,000.

For Kubitz Company the amount of temporary differences used to measure deferred income taxes amount toA) $0.

B) $11,000.

C) $16,000.

D) $27,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

54

Nolan Company sells its product on an installment basis, earning a $450 pretax gross profit on each installment sale. For accounting purposes the entire $450 is recognized in the year of sale, but for income tax purposes the installment method of accounting is used. Assume Nolan makes one sale in 2007, another sale in 2008, and a third sale in 2009. In each case, one-third of the gross sales price is collected in the year of sale, one-third in the next year, and the final installment in the third year. If the tax rate is 50%, what amount of deferred tax liability should Nolan Company show on its December 31, 2009 balance sheet?

A) $150

B) $225

C) $300

D) $450

A) $150

B) $225

C) $300

D) $450

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

55

Fesmire Co. had a deferred tax liability balance due to a temporary difference at the beginning of 2007 related to $200,000 of excess depreciation. In December of 2007, a new income tax act is signed into law that raises the corporate rate from 35% to 40%, effective January 1, 2009. If taxable amounts related to the temporary difference are scheduled to be reversed by $100,000 for both 2008 and 2009, Fesmire should increase or decrease deferred tax liability by what amount?

A) Decrease by $10,000

B) Decrease by $5,000

C) Increase by $5,000

D) Increase by $10,000

A) Decrease by $10,000

B) Decrease by $5,000

C) Increase by $5,000

D) Increase by $10,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

56

Meyers Co. had a deferred tax liability balance due to a temporary difference at the beginning of 2007 related to $600,000 of excess depreciation. In December of 2007, a new income tax act is signed into law that lowers the corporate rate from 40% to 35%, effective January 1, 2009. If taxable amounts related to the temporary difference are scheduled to be reversed by $300,000 for both 2008 and 2009, Meyers should increase or decrease deferred tax liability by what amount?

A) Decrease by $30,000

B) Decrease by $15,000

C) Increase by $15,000

D) Increase by $30,000

A) Decrease by $30,000

B) Decrease by $15,000

C) Increase by $15,000

D) Increase by $30,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

57

A reconciliation of Reaker Company's pretax accounting income with its taxable income for 2008, its first year of operations, is as follows:

The excess tax depreciation will result in equal net taxable amounts in each of the next three years. Enacted tax rates are 40% in 2008, 35% in 2009 and 2010, and 30% in 2011. The total deferred tax liability to be reported on Reaker's balance sheet at December 31, 2008, is

A) $36,000.

B) $30,000.

C) $31,500.

D) $27,000.

The excess tax depreciation will result in equal net taxable amounts in each of the next three years. Enacted tax rates are 40% in 2008, 35% in 2009 and 2010, and 30% in 2011. The total deferred tax liability to be reported on Reaker's balance sheet at December 31, 2008, isA) $36,000.

B) $30,000.

C) $31,500.

D) $27,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

58

Mast, Inc. reports a taxable and financial loss of $650,000 for 2009. Its pretax financial income for the last two years was as follows:

The amount that Mast, Inc. reports as a net loss for financial reporting purposes in 2009, assuming that it uses the carryback provisions, and that the tax rate is 30% for all periods affected, is

A) $650,000 loss.

B) $0.

C) $195,000 loss.

D) $455,000 loss.

The amount that Mast, Inc. reports as a net loss for financial reporting purposes in 2009, assuming that it uses the carryback provisions, and that the tax rate is 30% for all periods affected, isA) $650,000 loss.

B) $0.

C) $195,000 loss.

D) $455,000 loss.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

59

Peck Co. reports a taxable and pretax financial loss of $400,000 for 2009. Peck's taxable and pretax financial income and tax rates for the last two years were:

The amount that Peck should report as an income tax refund receivable in 2009, assuming that it uses the carryback provisions and that the tax rate is 40% in 2009, is

A) $120,000.

B) $140,000.

C) $160,000.

D) $180,000.

The amount that Peck should report as an income tax refund receivable in 2009, assuming that it uses the carryback provisions and that the tax rate is 40% in 2009, isA) $120,000.

B) $140,000.

C) $160,000.

D) $180,000.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

60

Bennington Corporation began operations in 2004. There have been no permanent or temporary differences to account for since the inception of the business. The following data are available:

In 2008, Bennington had an operating loss of $930,000. What amount of income tax benefits should be reported on the 2008 income statement due to this loss?

A) $409,500

B) $373,500

C) $372,000

D) $279,000

In 2008, Bennington had an operating loss of $930,000. What amount of income tax benefits should be reported on the 2008 income statement due to this loss?A) $409,500

B) $373,500

C) $372,000

D) $279,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

61

Ramos Corp.'s books showed pretax financial income of $1,500,000 for the year ended December 31, 2008. In the computation of federal income taxes, the following data were considered: What amount should Ramos report as its current federal income tax liability on its December 31, 2008 balance sheet?

A) $100,000

B) $130,000

C) $225,000

D) $255,000

What amount should Ramos report as its current federal income tax liability on its December 31, 2008 balance sheet?A) $100,000

B) $130,000

C) $225,000

D) $255,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

62

Eddy Corp.'s 2008 income statement showed pretax accounting income of $750,000. To compute the federal income tax liability, the following 2008 data are provided: What amount of current federal income tax liability should be included in Eddy's December 31, 2008 balance sheet?

A) $48,000

B) $66,000

C) $75,000

D) $198,000

What amount of current federal income tax liability should be included in Eddy's December 31, 2008 balance sheet?A) $48,000

B) $66,000

C) $75,000

D) $198,000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

63

On January 1, 2008, Lebo, Inc. purchased a machine for $720,000 which will be depreciated $72,000 per year for financial statement reporting purposes. For income tax reporting, Lebo elected to expense $80,000 and to use straight-line depreciation which will allow a cost recovery deduction of $64,000 for 2008. Assume a present and future enacted income tax rate of 30%. What amount should be added to Lebo's deferred income tax liability for this temporary difference at December 31, 2008?

A) $43,200

B) $24,000

C) $21,600

D) $19,200

A) $43,200

B) $24,000

C) $21,600

D) $19,200

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

64

On January 1, 2008, Magee Corp. purchased 40% of the voting common stock of Reed, Inc. and appropriately accounts for its investment by the equity method. During 2008, Reed reported earnings of $360,000 and paid dividends of $120,000. Magee assumes that all of Reed's undistributed earnings will be distributed as dividends in future periods when the enacted tax rate will be 30%. Ignore the dividend-received deduction. Magee's current enacted income tax rate is 25%. The increase in Magee's deferred income tax liability for this temporary difference is

A) $72,000.

B) $60,000.

C) $43,200.

D) $28,800.

A) $72,000.

B) $60,000.

C) $43,200.

D) $28,800.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

65