Deck 3: Partnership Liquidation and Incorporation; Joint Ventures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The following balance sheet is for Arch, Bole & Cusp LLP, whose partners share net income and losses in a 2:2:1 ratio, respectively:

-Refer to the above information. If Arch, Bole & Cusp LLP is liquidated by the realization of other assets in installments, the first realization of other assets with a carrying amount of $90,000 realizes $50,000, and all cash available after settlement with creditors is distributed to the partners, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $13,333; Cusp, $6,667

B) Arch, $0; Bole, $3,000; Cusp, $17,000

C) Arch, $8,000; Bole, $8 000; Cusp, $4,000

D) Arch, $6,667; Bole, $6,667; Cusp, $6,666

E) Some other amounts

-Refer to the above information. If Arch, Bole & Cusp LLP is liquidated by the realization of other assets in installments, the first realization of other assets with a carrying amount of $90,000 realizes $50,000, and all cash available after settlement with creditors is distributed to the partners, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $13,333; Cusp, $6,667

B) Arch, $0; Bole, $3,000; Cusp, $17,000

C) Arch, $8,000; Bole, $8 000; Cusp, $4,000

D) Arch, $6,667; Bole, $6,667; Cusp, $6,666

E) Some other amounts

Question

The following balance sheet is for Arch, Bole & Cusp LLP, whose partners share net income and losses in a 2:2:1 ratio, respectively:

-Refer to the above information. If the facts are as in the previous question, except that $3,000 cash is to be withheld for potential liquidation costs, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $11,333; Cusp, $5,667

B) Arch, $0; Bole, $1,000; Cusp, $16,000

C) Arch, $6,800; Bole, $6,800; Cusp, $3,400

D) Arch, $5,667; Bole, $5,667; Cusp, $5,666

E) Some other amounts

-Refer to the above information. If the facts are as in the previous question, except that $3,000 cash is to be withheld for potential liquidation costs, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $11,333; Cusp, $5,667

B) Arch, $0; Bole, $1,000; Cusp, $16,000

C) Arch, $6,800; Bole, $6,800; Cusp, $3,400

D) Arch, $5,667; Bole, $5,667; Cusp, $5,666

E) Some other amounts

Question

Taylor, Ullman & Victor Limited Liability Partnership, whose partners share net income or loss equally, is in liquidation. Partner Taylor, whose capital account had a debit balance of $3,000, paid a $4,000 trade account payable of the partnership. The appropriate journal entry (explanation omitted) for the partnership is:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

The following condensed balance sheet is for Alexander, Bell & Corbin LLP, whose partners share net income and losses in a 3:1:1 ratio, respectively: The partners agreed to liquidate the partnership after realization of the other assets. The partners had no net personal assets. The amount of cash that Alexander receives if the other assets realize $160,000 is:

A) $25,000

B) $26,000

C) $28,000

D) $100,000

E) Some other amount

A) $25,000

B) $26,000

C) $28,000

D) $100,000

E) Some other amount

Question

Question

Question

The partners of Jensen, Smith & Hart LLP shared net income and losses in the ratio of 5:3:2, respectively. The partners decided to liquidate the partnership when its assets consisted of cash, $40,000, and other assets, $210,000; the liabilities and partners' capital were as follows:  If other assets with a carrying amount of $120,000 realized $90,000, the amount of cash that each partner may receive at that time is:

If other assets with a carrying amount of $120,000 realized $90,000, the amount of cash that each partner may receive at that time is:

A)

B)

C)

D)

If other assets with a carrying amount of $120,000 realized $90,000, the amount of cash that each partner may receive at that time is:A)

B)

C)

D)

Question

The balance sheet of Ames, Beard & Craig LLP on September 26, 2006, showed cash, $20,000; noncash assets, $262,000; liabilities, $50,000; total partners' capital, $232,000. On that date, the three partners decided to dissolve and liquidate the partnership. The income-sharing ratio, which was to be used for gains and losses from realization of noncash assets, and the partners' capital account balances on September 26, 2006, were as follows (there were no loans receivable from or payable to the partners):

Prepare a cash distribution program for Ames, Beard & Craig LLP on September 26, 2006. A supporting working paper is not required.

Prepare a cash distribution program for Ames, Beard & Craig LLP on September 26, 2006. A supporting working paper is not required.

Prepare a cash distribution program for Ames, Beard & Craig LLP on September 26, 2006. A supporting working paper is not required. Question

Question

The balance sheet of Quanto, Rollo & Simms LLP prior to liquidation included the following:

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash assets realized $60,000, resulting in a loss of $10,000. Creditors were paid in full, partners were paid $25,000, and cash of $5,000 was withheld pending future developments.

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash assets realized $60,000, resulting in a loss of $10,000. Creditors were paid in full, partners were paid $25,000, and cash of $5,000 was withheld pending future developments.

Prepare undated journal entries to record the foregoing transactions and events. Show supporting computations in the explanations for the journal entries.

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash assets realized $60,000, resulting in a loss of $10,000. Creditors were paid in full, partners were paid $25,000, and cash of $5,000 was withheld pending future developments.Prepare undated journal entries to record the foregoing transactions and events. Show supporting computations in the explanations for the journal entries.

Question

Question

The partners of Hendry & Kim LLP shared net income and losses in a 5:3 ratio. As a result of operating losses, the partners decided to liquidate the partnership. Noncash assets were realized and all available cash was paid to creditors, leaving creditors' claims of $20,500 unpaid. The partners' capital account balances and personal net assets before the realization of noncash assets were as follows:

Partnership creditors were paid $20,500 by Kim, and Hendry paid an appropriate amount of cash to Kim in final settlement.

Partnership creditors were paid $20,500 by Kim, and Hendry paid an appropriate amount of cash to Kim in final settlement.

a. Prepare a working paper to compute the liquidation loss incurred by the partnership.

b. Prepare a working paper to show how settlement is made by the partners after Kim paid $20,500 to partnership creditors.

Partnership creditors were paid $20,500 by Kim, and Hendry paid an appropriate amount of cash to Kim in final settlement.a. Prepare a working paper to compute the liquidation loss incurred by the partnership.

b. Prepare a working paper to show how settlement is made by the partners after Kim paid $20,500 to partnership creditors.

Question

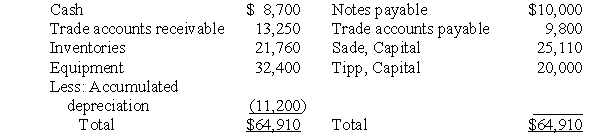

The balance sheet of Sade & Tipp LLP on April 30, 2006, was as follows:

The partnership was converted to S & T Corporation, with new accounting records. Sade and Tipp received a total of 10,000 shares of $1 par common stock in exchange for the net assets of the partnership. The accounting records of the partnership had been maintained in accordance with generally accepted accounting principles, except that an allowance for doubtful accounts of $800 had not been provided. The current fair values of the inventories and equipment were $28,000 and $35,000, respectively. Sade and Tipp shared net income and losses in a 3:2 ratio, respectively.

The partnership was converted to S & T Corporation, with new accounting records. Sade and Tipp received a total of 10,000 shares of $1 par common stock in exchange for the net assets of the partnership. The accounting records of the partnership had been maintained in accordance with generally accepted accounting principles, except that an allowance for doubtful accounts of $800 had not been provided. The current fair values of the inventories and equipment were $28,000 and $35,000, respectively. Sade and Tipp shared net income and losses in a 3:2 ratio, respectively.

Prepare journal entries for S & T Corporation on April 30, 2006, to record the transfer of net assets from the partnership and the issuance of common stock to the partners.

The partnership was converted to S & T Corporation, with new accounting records. Sade and Tipp received a total of 10,000 shares of $1 par common stock in exchange for the net assets of the partnership. The accounting records of the partnership had been maintained in accordance with generally accepted accounting principles, except that an allowance for doubtful accounts of $800 had not been provided. The current fair values of the inventories and equipment were $28,000 and $35,000, respectively. Sade and Tipp shared net income and losses in a 3:2 ratio, respectively.Prepare journal entries for S & T Corporation on April 30, 2006, to record the transfer of net assets from the partnership and the issuance of common stock to the partners.

Question

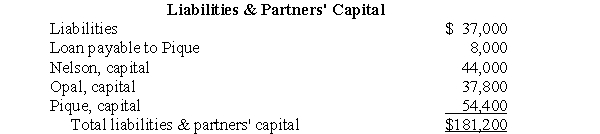

The liabilities and partners' capital section of the balance sheet for Nelson, Opal & Pique LLP was as follows on March 31, 2006, before liquidation:

The partners shared net income and losses in the ratio of 4:3:2, respectively.

The partners shared net income and losses in the ratio of 4:3:2, respectively.

Prepare a cash distribution program for Nelson, Opal & Pique LLP on March 31, 2006. A working paper is not required.

The partners shared net income and losses in the ratio of 4:3:2, respectively.Prepare a cash distribution program for Nelson, Opal & Pique LLP on March 31, 2006. A working paper is not required.

Question

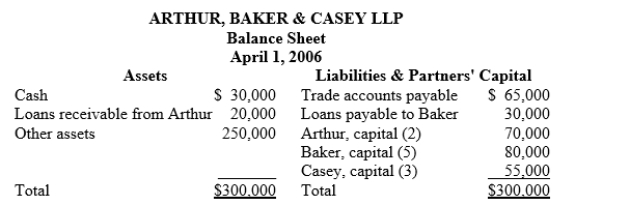

The partners of Arthur, Baker & Casey LLP decided to liquidate on April 1, 2006. The balance sheet of the partnership on April 1, 2006, follows, with the income-sharing ratio indicated parenthetically:

On April 1, 2006, the disposal of other assets with a carrying amount of $100,000 realized $70,000, and all available cash was distributed.

On April 1, 2006, the disposal of other assets with a carrying amount of $100,000 realized $70,000, and all available cash was distributed.

Prepare journal entries for Arthur, Baker & Casey LLP on April 1, 2006, to record the realization of the other assets and the distribution of available cash to creditors and to partners.

On April 1, 2006, the disposal of other assets with a carrying amount of $100,000 realized $70,000, and all available cash was distributed.Prepare journal entries for Arthur, Baker & Casey LLP on April 1, 2006, to record the realization of the other assets and the distribution of available cash to creditors and to partners.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 3: Partnership Liquidation and Incorporation; Joint Ventures

1

If a partner of a liquidating limited liability partnership is unable to pay a capital account deficit, the deficit is absorbed by the other partners in the income-sharing ratio of those partners.

True

2

After the realization of all noncash assets and the distribution of all available cash to the creditors, Kapp & Lodi LLP owed $15,000 to creditors. If at this point Kapp had a capital account balance of $18,000, Lodi had a capital account deficit of $3,000.

False

3

Gains and losses from the realization of noncash assets by limited liability partnership in a liquidation are divided in the ratio of the partners' capital account balances if there is no income-sharing plan in the partnership contract.

False

4

A loan receivable from a partner is added to the partner's capital account balance in the preparation of a cash distribution program to be used by the liquidator of the limited liability partnership.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

In the process of liquidation, partners may receive cash from a limited liability partnership before creditors receive cash if the noncash assets of the partnership are expected to realize a gain.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

If the partners' capital account balances have been reduced to the income-sharing ratio, subsequent cash payments to partners during liquidation of a limited liability partnership may be made in the ratio of their capital account balances.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

The marshaling of assets provisions of the Uniform Partnership Act deal with the order in which assets are realized during the liquidation of a limited liability partnership.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

All cash payments to partners during the liquidation of a limited liability partnership are made in the income-sharing ratio.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

In the computation of the amount of cash that may be paid to partners of a liquidating limited liability partnership on a specific date, accountants may assume that the maximum potential loss will be equal to the total of remaining noncash assets plus estimated liquidation costs.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

If a limited liability partnership is incorporated, the assets transferred to the corporation are entered in the accounting records of the corporation at current fair values.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

The investor enterprise must use the equity method of accounting for an investment in an unincorporated joint venture.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

If a limited liability partnership is incorporated, the corporation generally records the amount of the partnership's allowance for doubtful accounts, but does not record the accumulated depreciation of plant assets transferred to the corporation by the partnership.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

The fiscal year of a joint venture need not coincide with the fiscal years of the venturers.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

Two of the journal entries prepared by an investor in an unincorporated joint venture under the proportionate share method of accounting are identical to journal entries prepared under the equity method of accounting.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

The use of the equity method of accounting by investors in unincorporated joint ventures results in off-balance-sheet financing by the investors.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

If cash payments to partners of a limited liability partnership in liquidation are delayed until all noncash assets have been realized, any cash remaining after all partnership creditors have been paid is distributed:

A) According to the liquidator's best judgment

B) In the ratio for sharing net income and losses

C) In amounts equal to the partners' loan and capital account balances

D) In some other manner

A) According to the liquidator's best judgment

B) In the ratio for sharing net income and losses

C) In amounts equal to the partners' loan and capital account balances

D) In some other manner

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

In the liquidation of a limited liability partnership, a loan payable to a partner by the partnership is:

A) Paid immediately after all outside creditors have been paid in full

B) Considered to be the same as the partner's capital account

C) Used to absorb the partner's share of losses on realization of assets

D) Considered to be a liability of the partnership

A) Paid immediately after all outside creditors have been paid in full

B) Considered to be the same as the partner's capital account

C) Used to absorb the partner's share of losses on realization of assets

D) Considered to be a liability of the partnership

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

During the liquidation of Gym, Hob & Ing LLP, Partner Hob withdrew equipment with a cost to the partnership of $18,000, accumulated depreciation of $8,000, and a current fair value of $13,000. The partners shared net income and losses equally. The net debit to Hob's capital account (including any gain or loss on disposal of the equipment), assuming the noncash asset may be distributed safely to Hob, is:

A) $10,000

B) $12,000

C) $13,000

D) $18,000

E) Some other amount

A) $10,000

B) $12,000

C) $13,000

D) $18,000

E) Some other amount

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

In the preparation of an advance plan for installment payments of cash to partners of a liquidating limited liability partnership, each partner's capital per unit of income sharing is computed by:

A) Dividing each partner's capital account balance by the percentage of that partner's capital account balance of total partners' capital

B) Multiplying each partner's capital account balance by the percentage of that partner's capital account balance of total partners' capital

C) Dividing the total of each partner's capital account, plus any loan receivable from the partnership and minus any loan payable to the partnership, by the partner's income-sharing ratio

D) Some other method

A) Dividing each partner's capital account balance by the percentage of that partner's capital account balance of total partners' capital

B) Multiplying each partner's capital account balance by the percentage of that partner's capital account balance of total partners' capital

C) Dividing the total of each partner's capital account, plus any loan receivable from the partnership and minus any loan payable to the partnership, by the partner's income-sharing ratio

D) Some other method

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

In a marshaling of assets, the claims of limited liability partnership creditors rank:

A) Second in priority to partners' loans against partnership assets

B) Second in priority to partners' personal creditors against partners' personal assets

C) As part of the total owners' equity of the partnership

D) In none of the foregoing ways

A) Second in priority to partners' loans against partnership assets

B) Second in priority to partners' personal creditors against partners' personal assets

C) As part of the total owners' equity of the partnership

D) In none of the foregoing ways

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

In the installment liquidation of a limited liability partnership, the first partner to receive cash after all partnership liabilities have been paid is the partner who has the largest:

A) Capital per unit of income sharing

B) Capital account balance

C) Income-sharing ratio

D) Loan receivable from the partnership

A) Capital per unit of income sharing

B) Capital account balance

C) Income-sharing ratio

D) Loan receivable from the partnership

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

The following balance sheet is for Arch, Bole & Cusp LLP, whose partners share net income and losses in a 2:2:1 ratio, respectively:

-Refer to the above information. If Arch, Bole & Cusp LLP is liquidated by the realization of other assets in installments, the first realization of other assets with a carrying amount of $90,000 realizes $50,000, and all cash available after settlement with creditors is distributed to the partners, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $13,333; Cusp, $6,667

B) Arch, $0; Bole, $3,000; Cusp, $17,000

C) Arch, $8,000; Bole, $8 000; Cusp, $4,000

D) Arch, $6,667; Bole, $6,667; Cusp, $6,666

E) Some other amounts

-Refer to the above information. If Arch, Bole & Cusp LLP is liquidated by the realization of other assets in installments, the first realization of other assets with a carrying amount of $90,000 realizes $50,000, and all cash available after settlement with creditors is distributed to the partners, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $13,333; Cusp, $6,667

B) Arch, $0; Bole, $3,000; Cusp, $17,000

C) Arch, $8,000; Bole, $8 000; Cusp, $4,000

D) Arch, $6,667; Bole, $6,667; Cusp, $6,666

E) Some other amounts

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

The following balance sheet is for Arch, Bole & Cusp LLP, whose partners share net income and losses in a 2:2:1 ratio, respectively:

-Refer to the above information. If the facts are as in the previous question, except that $3,000 cash is to be withheld for potential liquidation costs, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $11,333; Cusp, $5,667

B) Arch, $0; Bole, $1,000; Cusp, $16,000

C) Arch, $6,800; Bole, $6,800; Cusp, $3,400

D) Arch, $5,667; Bole, $5,667; Cusp, $5,666

E) Some other amounts

-Refer to the above information. If the facts are as in the previous question, except that $3,000 cash is to be withheld for potential liquidation costs, the respective partners would receive (to the nearest dollar):

A) Arch, $0; Bole, $11,333; Cusp, $5,667

B) Arch, $0; Bole, $1,000; Cusp, $16,000

C) Arch, $6,800; Bole, $6,800; Cusp, $3,400

D) Arch, $5,667; Bole, $5,667; Cusp, $5,666

E) Some other amounts

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

24

Taylor, Ullman & Victor Limited Liability Partnership, whose partners share net income or loss equally, is in liquidation. Partner Taylor, whose capital account had a debit balance of $3,000, paid a $4,000 trade account payable of the partnership. The appropriate journal entry (explanation omitted) for the partnership is:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

In the installment liquidation of a limited liability partnership, each installment of cash is distributed:

A) In the partners' income-sharing ratio

B) In the ratio of the partners' capital account balances

C) As agreed to by the partners

D) As if no more cash would be forthcoming

A) In the partners' income-sharing ratio

B) In the ratio of the partners' capital account balances

C) As agreed to by the partners

D) As if no more cash would be forthcoming

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

If a liquidating limited liability partnership is insolvent:

A) The total of the debit-balance partners' capital accounts exceeds the total of the credit-balance capital accounts

B) Total liabilities exceeds total partners' capital

C) All noncash assets have been realized

D) Total cash is less than total liabilities

A) The total of the debit-balance partners' capital accounts exceeds the total of the credit-balance capital accounts

B) Total liabilities exceeds total partners' capital

C) All noncash assets have been realized

D) Total cash is less than total liabilities

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

The following condensed balance sheet is for Alexander, Bell & Corbin LLP, whose partners share net income and losses in a 3:1:1 ratio, respectively: The partners agreed to liquidate the partnership after realization of the other assets. The partners had no net personal assets. The amount of cash that Alexander receives if the other assets realize $160,000 is:

A) $25,000

B) $26,000

C) $28,000

D) $100,000

E) Some other amount

A) $25,000

B) $26,000

C) $28,000

D) $100,000

E) Some other amount

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

According to the Uniform Partnership Act, unpaid creditors of an insolvent partner of a liquidating general partnership have access to assets of the partnership:

A) On the same basis as creditors of the partnership

B) After partnership creditors have been paid in full, but only to the extent of the insolvent partner's equity in the partnership

C) After partnership creditors and loans payable to partners have been paid in full

D) Under no circumstances

A) On the same basis as creditors of the partnership

B) After partnership creditors have been paid in full, but only to the extent of the insolvent partner's equity in the partnership

C) After partnership creditors and loans payable to partners have been paid in full

D) Under no circumstances

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

Oliver, Patrick & Quincy LLP, is beginning liquidation. It has no cash, total liabilities of $60,000, including a $10,000 loan payable to Patrick, and equal partners' capital account balances of $40,000. The income-sharing ratio is 5:1:4, respectively. If a portion of the noncash assets with a carrying amount of $140,000 realizes $120,000, the cash payment that Patrick receives is:

A) $20,000

B) $44,000

C) $53,000

D) Some other amount

A) $20,000

B) $44,000

C) $53,000

D) Some other amount

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

The partners of Jensen, Smith & Hart LLP shared net income and losses in the ratio of 5:3:2, respectively. The partners decided to liquidate the partnership when its assets consisted of cash, $40,000, and other assets, $210,000; the liabilities and partners' capital were as follows: If other assets with a carrying amount of $120,000 realized $90,000, the amount of cash that each partner may receive at that time is:

A)

B)

C)

D)

If other assets with a carrying amount of $120,000 realized $90,000, the amount of cash that each partner may receive at that time is:A)

B)

C)

D)

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

The balance sheet of Ames, Beard & Craig LLP on September 26, 2006, showed cash, $20,000; noncash assets, $262,000; liabilities, $50,000; total partners' capital, $232,000. On that date, the three partners decided to dissolve and liquidate the partnership. The income-sharing ratio, which was to be used for gains and losses from realization of noncash assets, and the partners' capital account balances on September 26, 2006, were as follows (there were no loans receivable from or payable to the partners):

Prepare a cash distribution program for Ames, Beard & Craig LLP on September 26, 2006. A supporting working paper is not required.

Prepare a cash distribution program for Ames, Beard & Craig LLP on September 26, 2006. A supporting working paper is not required. Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

After realization of a portion of the noncash assets of Bemis, Coppo & Dipp LLP, which was being liquidated, the capital account balances were Bemis, $54,600; Coppo, $40,500; and Dipp, $17,000. Cash of $34,100 and other assets with a carrying amount of $98,000 were on hand. Creditors' claims totaled $20,000. Bemis, Coppo and Dipp shared net income and losses in a 2:1:1 ratio, respectively.

Prepare a working paper to compute the amount of cash that may be paid to creditors and to partners at this time, assuming that no partner is solvent.

Prepare a working paper to compute the amount of cash that may be paid to creditors and to partners at this time, assuming that no partner is solvent.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

The balance sheet of Quanto, Rollo & Simms LLP prior to liquidation included the following:

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash assets realized $60,000, resulting in a loss of $10,000. Creditors were paid in full, partners were paid $25,000, and cash of $5,000 was withheld pending future developments.

Prepare undated journal entries to record the foregoing transactions and events. Show supporting computations in the explanations for the journal entries.

The three partners shared net income and losses in a 5:3:2 ratio, respectively. Noncash assets realized $60,000, resulting in a loss of $10,000. Creditors were paid in full, partners were paid $25,000, and cash of $5,000 was withheld pending future developments.Prepare undated journal entries to record the foregoing transactions and events. Show supporting computations in the explanations for the journal entries.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

The partners of Dunn, Carson & Devlin LLP shared net income and losses in a 3:2:1 ratio, respectively. They decided to appoint a liquidator to liquidate the partnership. On May 31, 2006, the partnership's accounting records included cash, $42,500; other assets, $129,500; liabilities, $20,000; Dunn, capital, $75,000; Carson, capital, $55,000; and Devlin, capital, $22,000. The liquidator estimated that three months would be required to realize the other assets and that liquidation costs would amount to $4,500.

a. Prepare a cash distribution program showing how available cash should be paid to creditors and partners in the course of liquidation. A working paper is not required.

b. Prepare a journal entry to record cash payments to creditors and to partners on May 31, 2006, totaling $38,000.

a. Prepare a cash distribution program showing how available cash should be paid to creditors and partners in the course of liquidation. A working paper is not required.

b. Prepare a journal entry to record cash payments to creditors and to partners on May 31, 2006, totaling $38,000.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

The partners of Hendry & Kim LLP shared net income and losses in a 5:3 ratio. As a result of operating losses, the partners decided to liquidate the partnership. Noncash assets were realized and all available cash was paid to creditors, leaving creditors' claims of $20,500 unpaid. The partners' capital account balances and personal net assets before the realization of noncash assets were as follows:

Partnership creditors were paid $20,500 by Kim, and Hendry paid an appropriate amount of cash to Kim in final settlement.

a. Prepare a working paper to compute the liquidation loss incurred by the partnership.

b. Prepare a working paper to show how settlement is made by the partners after Kim paid $20,500 to partnership creditors.

Partnership creditors were paid $20,500 by Kim, and Hendry paid an appropriate amount of cash to Kim in final settlement.a. Prepare a working paper to compute the liquidation loss incurred by the partnership.

b. Prepare a working paper to show how settlement is made by the partners after Kim paid $20,500 to partnership creditors.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

The balance sheet of Sade & Tipp LLP on April 30, 2006, was as follows:

The partnership was converted to S & T Corporation, with new accounting records. Sade and Tipp received a total of 10,000 shares of $1 par common stock in exchange for the net assets of the partnership. The accounting records of the partnership had been maintained in accordance with generally accepted accounting principles, except that an allowance for doubtful accounts of $800 had not been provided. The current fair values of the inventories and equipment were $28,000 and $35,000, respectively. Sade and Tipp shared net income and losses in a 3:2 ratio, respectively.

Prepare journal entries for S & T Corporation on April 30, 2006, to record the transfer of net assets from the partnership and the issuance of common stock to the partners.

The partnership was converted to S & T Corporation, with new accounting records. Sade and Tipp received a total of 10,000 shares of $1 par common stock in exchange for the net assets of the partnership. The accounting records of the partnership had been maintained in accordance with generally accepted accounting principles, except that an allowance for doubtful accounts of $800 had not been provided. The current fair values of the inventories and equipment were $28,000 and $35,000, respectively. Sade and Tipp shared net income and losses in a 3:2 ratio, respectively.Prepare journal entries for S & T Corporation on April 30, 2006, to record the transfer of net assets from the partnership and the issuance of common stock to the partners.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

The liabilities and partners' capital section of the balance sheet for Nelson, Opal & Pique LLP was as follows on March 31, 2006, before liquidation:

The partners shared net income and losses in the ratio of 4:3:2, respectively.

Prepare a cash distribution program for Nelson, Opal & Pique LLP on March 31, 2006. A working paper is not required.

The partners shared net income and losses in the ratio of 4:3:2, respectively.Prepare a cash distribution program for Nelson, Opal & Pique LLP on March 31, 2006. A working paper is not required.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

The partners of Arthur, Baker & Casey LLP decided to liquidate on April 1, 2006. The balance sheet of the partnership on April 1, 2006, follows, with the income-sharing ratio indicated parenthetically:

On April 1, 2006, the disposal of other assets with a carrying amount of $100,000 realized $70,000, and all available cash was distributed.

Prepare journal entries for Arthur, Baker & Casey LLP on April 1, 2006, to record the realization of the other assets and the distribution of available cash to creditors and to partners.

On April 1, 2006, the disposal of other assets with a carrying amount of $100,000 realized $70,000, and all available cash was distributed.Prepare journal entries for Arthur, Baker & Casey LLP on April 1, 2006, to record the realization of the other assets and the distribution of available cash to creditors and to partners.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

On March 1, 2005, both Anson Company and Beale Company invested $50,000 for a 50% interest in AB Company, an unincorporated joint venture. For the fiscal year ended February 28, 2006, AB Company had a net income of $40,000 (revenue of $250,000 less expenses of $210,000), and its balance sheet on that date had total assets of $260,000 and total liabilities of $120,000.

a. Prepare journal entries for Anson Company on March 1, 2005, and February 28, 2006, to account for its investment in AB Company under the equity method of accounting.

b. Prepare an additional journal entry for Anson Company on February 28, 2006, to account for its investment in AB Company under the proportionate share method of accounting.

a. Prepare journal entries for Anson Company on March 1, 2005, and February 28, 2006, to account for its investment in AB Company under the equity method of accounting.

b. Prepare an additional journal entry for Anson Company on February 28, 2006, to account for its investment in AB Company under the proportionate share method of accounting.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

In a classroom discussion of accounting standards for unincorporated joint ventures, student Marcia was highly critical of the proportionate share method of accounting, under which each venturer recognizes in its accounting records its percentage share of the venture's revenue, expenses, assets, and liabilities. Marcia stated that she was unaware of any other situation in which legal form of a specific type of business enterprise resulted in acceptable alternative accounting standards of recognition and financial statement display.

What is your opinion of student Marcia's view? Explain.

What is your opinion of student Marcia's view? Explain.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.