Deck 11: Systematic Risk and the Equity Risk Premium

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Suppose you have $10,000 in cash to invest.You decide to sell short $5000 worth of Kinston stock and invest the proceeds from your short sale plus your $10,000 into one-year Treasury bills earning 5%.At the end of the year,you decide to liquidate your portfolio.Kinston Industries has the following realized returns:

The return on your portfolio is closest to:

A) -0.5%

B) 13.5%

C) -2.5%

D) 14.5%

E) 5.0%

The return on your portfolio is closest to:

A) -0.5%

B) 13.5%

C) -2.5%

D) 14.5%

E) 5.0%

Question

Question

Question

Question

Question

Question

Question

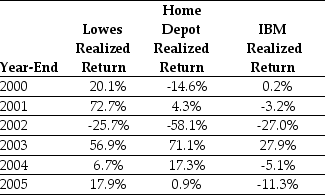

Use the table for the question(s) below.

Consider the following returns:

The volatility on Lowes' returns is closest to:

A) 35%

B) 10%

C) 13%

D) 42%

E) 22%

Consider the following returns:

The volatility on Lowes' returns is closest to:

A) 35%

B) 10%

C) 13%

D) 42%

E) 22%

Question

Question

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following returns:

The covariance between Lowes' and Home Depot's returns is closest to:

A) 0.10

B) 0.29

C) 0.12

D) 0.69

E) 0.41

Consider the following returns:

The covariance between Lowes' and Home Depot's returns is closest to:

A) 0.10

B) 0.29

C) 0.12

D) 0.69

E) 0.41

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

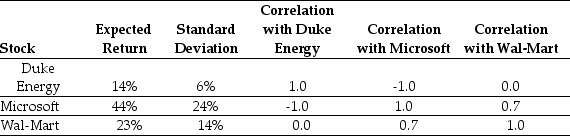

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 10.0%

B) 17.8%

C) 26.3%

D) 29.0%

E) 18.5%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 10.0%

B) 17.8%

C) 26.3%

D) 29.0%

E) 18.5%

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 5.0%

B) 0.6%

C) 7.6%

D) 22.4%

E) 10.1%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 5.0%

B) 0.6%

C) 7.6%

D) 22.4%

E) 10.1%

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 9%

B) 14%

C) 11%

D) 12%

E) 10%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 9%

B) 14%

C) 11%

D) 12%

E) 10%

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 8%

B) 9%

C) 11%

D) 6%

E) 7%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 8%

B) 9%

C) 11%

D) 6%

E) 7%

Question

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Microsoft is closest to:

A) 7.2%

B) 7.6%

C) 15.4%

D) 17.6%

E) 19.0%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Microsoft is closest to:

A) 7.2%

B) 7.6%

C) 15.4%

D) 17.6%

E) 19.0%

Question

Question

Question

Question

Use the table for the question(s) below.

Consider the following returns:

The volatility on Home Depot's returns is closest to:

A) 35%

B) 31%

C) 42%

D) 18%

E) 22%

Consider the following returns:

The volatility on Home Depot's returns is closest to:

A) 35%

B) 31%

C) 42%

D) 18%

E) 22%

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 15%

B) 14%

C) 29%

D) 44%

E) 22%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 15%

B) 14%

C) 29%

D) 44%

E) 22%

Question

Question

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 21%

B) 12%

C) 27%

D) 18%

E) 24%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 21%

B) 12%

C) 27%

D) 18%

E) 24%

Question

Question

Question

Question

Question

Question

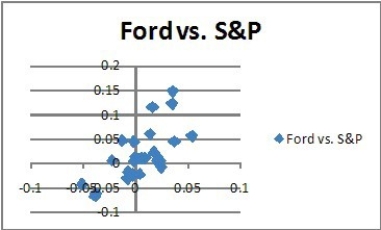

You observe the following scatterplot of Ford's weekly returns against the S&P 500.Which of the following statements is true about Ford's beta against the S&P 500?

A) Ford's beta appears to be positive.

B) Ford's beta appears to be negative.

C) Ford's beta appears to be zero- there is no apparent relation between its return and the S&P return.

D) Ford's beta appears to be highly negative.

E) Beta has nothing to do with the relationship seen in this scatterplot.

A) Ford's beta appears to be positive.

B) Ford's beta appears to be negative.

C) Ford's beta appears to be zero- there is no apparent relation between its return and the S&P return.

D) Ford's beta appears to be highly negative.

E) Beta has nothing to do with the relationship seen in this scatterplot.

Question

Question

Question

Question

Question

Question

Question

Question

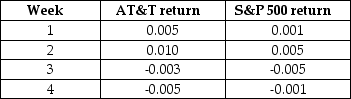

You observe that AT&T stock and the S&P 500 have the following weekly returns:

If this pattern of stock returns is typical of AT&T stock,and you calculated a beta against the S&P 500,which of the following is true?

A) AT&T's beta is negative.

B) AT&T's beta is zero.

C) AT&T's beta is positive.

D) AT&T's beta is highly negative.

E) Beta cannot be calculated from this data.

If this pattern of stock returns is typical of AT&T stock,and you calculated a beta against the S&P 500,which of the following is true?

A) AT&T's beta is negative.

B) AT&T's beta is zero.

C) AT&T's beta is positive.

D) AT&T's beta is highly negative.

E) Beta cannot be calculated from this data.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/102

Play

Full screen (f)

Deck 11: Systematic Risk and the Equity Risk Premium

1

You have invested $12,000 in RBC stock,$8,000 in TD stock,and $6,000 in WestJet stock.If you expect the return on RBC to be 5% in the next year,the return on TD to be 3%,and the return on WestJet to be 8%,what is the expected return for your portfolio?

A) 5.4%

B) 4.8%

C) 5.1%

D) 5.33%

E) 5.2%

A) 5.4%

B) 4.8%

C) 5.1%

D) 5.33%

E) 5.2%

5.1%

2

You have invested $25,000 in RBC stock and $18,000 in TD stock.If you expect the return on RBC to be 6% in the next year,and the return on TD to be 4%,what is the expected return for your portfolio?

A) 4%

B) 5%

C) 5.2%

D) 6%

E) 4.8%

A) 4%

B) 5%

C) 5.2%

D) 6%

E) 4.8%

5.2%

3

Your investment portfolio contains 200 shares of RBC and 450 shares of Air Canada.The price of RBC is currently $92 per share,and the price of Air Canada is currently $11 per share.If you expect the return on RBC to be 6% in the next year,and the return on Air Canada to be 8%,what is the expected return for your portfolio?

A) 6.4%

B) 7%

C) 6%

D) 8%

E) 6.8%

A) 6.4%

B) 7%

C) 6%

D) 8%

E) 6.8%

6.4%

4

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Lowes in your portfolio is:

A) 40%

B) 20%

C) 50%

D) 30%

E) 10%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Lowes in your portfolio is:

A) 40%

B) 20%

C) 50%

D) 30%

E) 10%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

5

What role does the standard deviations of two assets play in computation of the expected return of the two asset portfolio?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

6

Suppose you buy 100 shares of RBC at $85 per share,and 80 shares of TD at $75 per share.If RBC's stock goes up to $88.50 per share and TD's stock goes up to $77 per share,what is your portfolio return?

A) 2%

B) 0%

C) 3.5%

D) 3%

E) 4.5%

A) 2%

B) 0%

C) 3.5%

D) 3%

E) 4.5%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

7

A portfolio has three stocks - 300 shares of Yahoo (YHOO),300 Shares of General Motors (GM),and 100 shares of Standard and Poor's Index Fund (SPY).If the price of YHOO is $20,the price of GM is $30,and the price of SPY is $150,calculate the portfolio weight of YHOO and GM.

A) 10%, 20%

B) 15%, 25%

C) 20%, 30%

D) 20%, 40%

E) 43%, 43%

A) 10%, 20%

B) 15%, 25%

C) 20%, 30%

D) 20%, 40%

E) 43%, 43%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

8

Suppose over the next year Ball has a return of 12.5%,Lowes has a return of 20%,and Abbott Labs has a return of -10%.The value of your portfolio over the year is:

A) $21,000

B) $20,000

C) $20,700

D) $21,500

E) $22,000

A) $21,000

B) $20,000

C) $20,700

D) $21,500

E) $22,000

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

9

You have invested $5,000 in RBC stock,$12,000 in TD stock,and $18,000 in WestJet stock.If you expect the return on RBC to be 4% in the next year,the return on TD to be 5%,and the return on WestJet to be 6%,what is the expected return for your portfolio?

A) 5.4%

B) 5%

C) 4.8%

D) 6%

E) 5.2%

A) 5.4%

B) 5%

C) 4.8%

D) 6%

E) 5.2%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

10

Suppose over the next year Ball has a return of 12.5%,Lowes has a return of 20%,and Abbott Labs has a return of -10%.The return on your portfolio over the year is:

A) 0%

B) 7.5%

C) 3.5%

D) 5.0%

E) 2.5%

A) 0%

B) 7.5%

C) 3.5%

D) 5.0%

E) 2.5%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

11

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Abbott Labs in your portfolio is:

A) 50%

B) 40%

C) 30%

D) 20%

E) 10%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Abbott Labs in your portfolio is:

A) 50%

B) 40%

C) 30%

D) 20%

E) 10%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

12

A portfolio comprises two stocks,A and B,with equal amounts of money invested in each.If stock A's stock price increases and that of stock B decreases,the weight of stock A in the portfolio will increase.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

13

Your investment portfolio contains 100 shares of RBC,75 shares of TD,and 200 shares of WestJet.The price of RBC is currently $75 per share,the price of TD is $55 and the price of WestJet is currently $21 per share.If you expect the return on RBC to be 5% in the next year,the return on TD to be 6.5%,and the return on WestJet to be 10%,what is the expected return for your portfolio?

A) 6.4%

B) 6.7%

C) 7.2%

D) 6%

E) 6.5%

A) 6.4%

B) 6.7%

C) 7.2%

D) 6%

E) 6.5%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

14

A portfolio has three stocks - 100 shares of Yahoo (YHOO),200 Shares of General Motors (GM),and 50 shares of Standard and Poor's Index Fund (SPY).If the price of YHOO is $20,the price of GM is $20,and the price of SPY is $130,calculate the portfolio weight of YHOO and GM.

A) 12%, 17%

B) 11%, 31%

C) 15%, 29%

D) 16%, 32%

E) 29%, 57%

A) 12%, 17%

B) 11%, 31%

C) 15%, 29%

D) 16%, 32%

E) 29%, 57%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

15

Suppose you have $10,000 in cash to invest.You decide to sell short $5000 worth of Kinston stock and invest the proceeds from your short sale plus your $10,000 into one-year Treasury bills earning 5%.At the end of the year,you decide to liquidate your portfolio.Kinston Industries has the following realized returns:

The return on your portfolio is closest to:

A) -0.5%

B) 13.5%

C) -2.5%

D) 14.5%

E) 5.0%

The return on your portfolio is closest to:

A) -0.5%

B) 13.5%

C) -2.5%

D) 14.5%

E) 5.0%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

16

What role does the correlation of two assets play in computation of the expected return of the two asset portfolio?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

17

Suppose you buy 50 shares of RBC at $90 per share,and 70 shares of TD at $78 per share.If RBC's stock goes up to $94 per share and TD's stock falls to $72 per share,what is your portfolio return?

A) -2.2%

B) 0%

C) 6.4%

D) 4.4%

E) -7.7%

A) -2.2%

B) 0%

C) 6.4%

D) 4.4%

E) -7.7%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

18

You have invested $10,000 in RBC stock and $21,000 in TD stock.If you expect the return on RBC to be 5% in the next year,and the return on TD to be 6.5%,what is the expected return for your portfolio?

A) 5.75%

B) 5%

C) 6.5%

D) 6%

E) 5.5%

A) 5.75%

B) 5%

C) 6.5%

D) 6%

E) 5.5%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

19

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Ball Corporation in your portfolio is:

A) 50%

B) 40%

C) 20%

D) 30%

E) 10%

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

The weight of Ball Corporation in your portfolio is:

A) 50%

B) 40%

C) 20%

D) 30%

E) 10%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

20

A portfolio has three stocks - 200 shares of Yahoo (YHOO),100 Shares of General Motors (GM),and 50 shares of Standard and Poor's Index Fund (SPY).If the price of YHOO is $30,the price of GM is $30,and the price of SPY is $130,calculate the portfolio weight of YHOO and GM.

A) 38.7%, 19.4%

B) 21.3%, 35.2%

C) 11.7%, 12.7%

D) 36.2%, 21.6%

E) 57.1%, 28.6%

A) 38.7%, 19.4%

B) 21.3%, 35.2%

C) 11.7%, 12.7%

D) 36.2%, 21.6%

E) 57.1%, 28.6%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

21

We can reduce volatility by investing in less than perfectly correlated assets through diversification because the expected return of a portfolio is the weighted average of the expected returns of its stocks,but the volatility of a portfolio

A) is higher than the weighted average volatility.

B) is independent of weights in the stocks.

C) is less than the weighted average volatility.

D) depends on the expected return.

E) is the same as the weighted average volatility.

A) is higher than the weighted average volatility.

B) is independent of weights in the stocks.

C) is less than the weighted average volatility.

D) depends on the expected return.

E) is the same as the weighted average volatility.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

22

Use the table for the question(s) below.

Consider the following returns:

The volatility on Lowes' returns is closest to:

A) 35%

B) 10%

C) 13%

D) 42%

E) 22%

Consider the following returns:

The volatility on Lowes' returns is closest to:

A) 35%

B) 10%

C) 13%

D) 42%

E) 22%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

23

Your portfolio has 20% of its value invested in Bombardier and the remainder invested in Lululemon.Bombardier stock has a volatility of 15%,while Lululemon stock has a volatility of 12%.If the correlation between Bombardier and Lululemon is 0,what is the standard deviation of your portfolio?

A) 12.6%

B) 10%

C) 1%

D) 12.7%

E) 12%

A) 12.6%

B) 10%

C) 1%

D) 12.7%

E) 12%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

24

Diversification reduces the risk of a portfolio because ________ and some of the risks are averaged out of the portfolio.

A) stocks do not move identically

B) stocks have common risks

C) stocks are unpredictable

D) stocks are always affected by the market

E) some stocks have lower returns than others

A) stocks do not move identically

B) stocks have common risks

C) stocks are unpredictable

D) stocks are always affected by the market

E) some stocks have lower returns than others

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

25

The volatility of Home Depot share prices is 30% and that of General Motors shares is 30%.When I hold both stocks in my portfolio with an equal amount in each,and the stocks' returns have a correlation of minus 1,the overall volatility of returns of the portfolio is

A) more than 30%.

B) unchanged at 30%.

C) between 0 and 30%.

D) zero.

E) Cannot say for sure

A) more than 30%.

B) unchanged at 30%.

C) between 0 and 30%.

D) zero.

E) Cannot say for sure

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

26

The volatility of Home Depot Share prices is 30% and that of General Motors shares is 30%.When I hold both stocks in my portfolio and the stocks returns have zero correlation,the overall volatility of returns of the portfolio is

A) unchanged at 30%.

B) less than 30%.

C) more than 30%.

D) zero.

E) Cannot say for sure

A) unchanged at 30%.

B) less than 30%.

C) more than 30%.

D) zero.

E) Cannot say for sure

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

27

Stocks tend to move together if they are affected by

A) company-specific events.

B) common economic events.

C) events unrelated to the economy.

D) idiosyncratic shocks.

E) unforeseen events.

A) company-specific events.

B) common economic events.

C) events unrelated to the economy.

D) idiosyncratic shocks.

E) unforeseen events.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

28

Use the table for the question(s) below.

Consider the following returns:

The covariance between Lowes' and Home Depot's returns is closest to:

A) 0.10

B) 0.29

C) 0.12

D) 0.69

E) 0.41

Consider the following returns:

The covariance between Lowes' and Home Depot's returns is closest to:

A) 0.10

B) 0.29

C) 0.12

D) 0.69

E) 0.41

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

29

Your portfolio has 25% of its value invested in Bombardier and the remainder invested in Lululemon.Bombardier stock has a volatility of 30%,while Lululemon stock has a volatility of 18%.If the correlation between Bombardier and Lululemon is 0.2,what is the standard deviation of your portfolio?

A) 16.7%

B) 24%

C) 2.8%

D) 21%

E) 46.1%

A) 16.7%

B) 24%

C) 2.8%

D) 21%

E) 46.1%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

30

When the returns of two stocks are perfectly positively correlated,then

A) they always move oppositely.

B) they tend to move oppositely.

C) they have no tendency.

D) they tend to move together.

E) they always move together.

A) they always move oppositely.

B) they tend to move oppositely.

C) they have no tendency.

D) they tend to move together.

E) they always move together.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

31

Your portfolio has 50% of its value invested in Bombardier and the remainder invested in Lululemon.Bombardier stock has a volatility of 25%,while Lululemon stock has a volatility of 10%.If the correlation between Bombardier and Lululemon is -0.1,what is the standard deviation of your portfolio?

A) 16.7%

B) 17.5%

C) 13%

D) 17.4%

E) 1.7%

A) 16.7%

B) 17.5%

C) 13%

D) 17.4%

E) 1.7%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

32

If two stocks are perfectly negatively correlated,a portfolio with equal weighting in each stock will always have a volatility (standard deviation)of 0.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

33

When the returns of two stocks are negatively correlated,but not perfectly negatively correlated,then

A) they always move oppositely.

B) they tend to move oppositely.

C) they have no tendency.

D) they tend to move together.

E) they always move together.

A) they always move oppositely.

B) they tend to move oppositely.

C) they have no tendency.

D) they tend to move together.

E) they always move together.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

34

As we add more uncorrelated stocks to a portfolio where the stocks are held in equal weights,the benefit of diversification is most dramatic

A) after 20 stocks have been added.

B) when there are more than 500 stocks.

C) when there are more than 1000 stocks.

D) at the outset.

E) when there are more than 100 stocks.

A) after 20 stocks have been added.

B) when there are more than 500 stocks.

C) when there are more than 1000 stocks.

D) at the outset.

E) when there are more than 100 stocks.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

35

When we form an equally weighted portfolio of stocks and keep increasing the number of stocks in the portfolio,the volatility of the portfolio also increases.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

36

Correlation is the degree to which the returns of two stocks share common risks.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

37

The volatility of Home Depot share prices is 30% and that of General Motors shares is 30%.When I hold both stocks in my portfolio and the stocks' returns have a correlation of 1,the overall volatility of returns of the portfolio is

A) more than 30%.

B) less than 30%.

C) unchanged at 30%.

D) zero.

E) Cannot say for sure

A) more than 30%.

B) less than 30%.

C) unchanged at 30%.

D) zero.

E) Cannot say for sure

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

38

In a two-asset portfolio,what happens to the portfolio weight of the better performing asset?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

39

When we combine stocks in a portfolio,the amount of risk that is eliminated depends on the degree to which the stocks face common risks and move together.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

40

The volatility of Home Depot share prices is 30% and that of General Motors shares is 30%.When I hold both stocks in my portfolio,the overall volatility of the portfolio is:

A) 30%

B) 26%

C) 28%

D) 20%

E) More information needed.

A) 30%

B) 26%

C) 28%

D) 20%

E) More information needed.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

41

A stock market comprises 2000 shares of stock A and 2000 shares of stock B.The share prices for stocks A and B are $20 and $10,respectively.What proportion of the market portfolio is comprised of each stock?

A) Stock A is 66.7% and Stock B is 33.3%

B) Stock A is 33.3% and Stock B is 66.7%

C) Stock A is $40,000 and Stock B is $20,000

D) Stock A is 200% and Stock B is 100%

E) Stock A is 50% and Stock B is 50%

A) Stock A is 66.7% and Stock B is 33.3%

B) Stock A is 33.3% and Stock B is 66.7%

C) Stock A is $40,000 and Stock B is $20,000

D) Stock A is 200% and Stock B is 100%

E) Stock A is 50% and Stock B is 50%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

42

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 10.0%

B) 17.8%

C) 26.3%

D) 29.0%

E) 18.5%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 10.0%

B) 17.8%

C) 26.3%

D) 29.0%

E) 18.5%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

43

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 5.0%

B) 0.6%

C) 7.6%

D) 22.4%

E) 10.1%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest to:

A) 5.0%

B) 0.6%

C) 7.6%

D) 22.4%

E) 10.1%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

44

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 9%

B) 14%

C) 11%

D) 12%

E) 10%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 9%

B) 14%

C) 11%

D) 12%

E) 10%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

45

If you build a large enough portfolio,you can diversify away all the risks of a portfolio.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

46

Stocks that have a higher volatility will always have a higher beta.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

47

What diversification,if any,is achieved if two stocks in a portfolio are perfectly positively correlated?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

48

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 8%

B) 9%

C) 11%

D) 6%

E) 7%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 8%

B) 9%

C) 11%

D) 6%

E) 7%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

49

A stock market comprises 1000 shares of stock A and 3000 shares of stock B.The share prices for stocks A and B are $25 and $30,respectively.What is the capitalization of the market portfolio?

A) $115,000

B) $100,000

C) $98,000

D) $125,000

E) $90,000

A) $115,000

B) $100,000

C) $98,000

D) $125,000

E) $90,000

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

50

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Microsoft is closest to:

A) 7.2%

B) 7.6%

C) 15.4%

D) 17.6%

E) 19.0%

Consider the following expected returns, volatilities, and correlations:

The volatility of a portfolio that is equally invested in Wal-Mart and Microsoft is closest to:

A) 7.2%

B) 7.6%

C) 15.4%

D) 17.6%

E) 19.0%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

51

A stock market comprises 5000 shares of stock A and 2000 shares of stock B.Assume the share prices for stocks A and B are $20 and $35,respectively.If you have $15,000 to invest and you want to hold the market portfolio,how much of your money will you invest in Stock A?

A) $10,000

B) $8,823.53

C) $6,176.47

D) $5,000

E) $4,403.42

A) $10,000

B) $8,823.53

C) $6,176.47

D) $5,000

E) $4,403.42

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following combinations of stocks would give you the biggest reduction in risk?

A) Duke Energy and Wal-Mart

B) Wal-Mart and Microsoft

C) Microsoft and Duke Energy

D) Duke Energy by itself

E) Wal-Mart by itself

A) Duke Energy and Wal-Mart

B) Wal-Mart and Microsoft

C) Microsoft and Duke Energy

D) Duke Energy by itself

E) Wal-Mart by itself

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

53

Air Canada stock has a standard deviation of 18%,while the market index standard deviation is 8%.If the correlation between Air Canada and the market index is 0.45,what is the beta of Air Canada stock?

A) 1.01

B) 0.03

C) 0.2

D) 2.25

E) 2.5

A) 1.01

B) 0.03

C) 0.2

D) 2.25

E) 2.5

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

54

Use the table for the question(s) below.

Consider the following returns:

The volatility on Home Depot's returns is closest to:

A) 35%

B) 31%

C) 42%

D) 18%

E) 22%

Consider the following returns:

The volatility on Home Depot's returns is closest to:

A) 35%

B) 31%

C) 42%

D) 18%

E) 22%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

55

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 15%

B) 14%

C) 29%

D) 44%

E) 22%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

A) 15%

B) 14%

C) 29%

D) 44%

E) 22%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

56

What is the lowest risk possible by selecting two stocks that are perfectly negatively correlated?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

57

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 21%

B) 12%

C) 27%

D) 18%

E) 24%

Consider the following expected returns, volatilities, and correlations:

The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

A) 21%

B) 12%

C) 27%

D) 18%

E) 24%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

58

A stock market comprises 5000 shares of stock A and 2000 shares of stock B.Assume the share prices for stocks A and B are $20 and $35,respectively.What proportion of the market portfolio is comprised of stock A?

A) 58.8%

B) 41.2%

C) $100,000

D) $70,000

E) 100%

A) 58.8%

B) 41.2%

C) $100,000

D) $70,000

E) 100%

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

59

A stock market comprises 2000 shares of stock A and 2000 shares of stock B.The share prices for stocks A and B are $20 and $10,respectively.What is the capitalization of the market portfolio?

A) $55,000

B) $60,000

C) $70,000

D) $65,000

E) $50,000

A) $55,000

B) $60,000

C) $70,000

D) $65,000

E) $50,000

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

60

A stock market comprises 5000 shares of stock A and 2000 shares of stock B.Assume the share prices for stocks A and B are $20 and $35,respectively.What is the capitalization of the market portfolio?

A) $170,000

B) $150,000

C) $165,000

D) $185,000

E) $100,000

A) $170,000

B) $150,000

C) $165,000

D) $185,000

E) $100,000

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

61

A linear regression to estimate the relation between Research in Motion's stock returns and the market's return gives the best-fitting line that represents the relation between the stock and the market.The slope of this line is our estimate of

A) alpha.

B) beta.

C) risk-free rate.

D) volatility.

E) standard deviation.

A) alpha.

B) beta.

C) risk-free rate.

D) volatility.

E) standard deviation.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

62

Since total risk is greater than systematic risk,should standard deviation be always greater than beta?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

63

You observe the following scatterplot of Ford's weekly returns against the S&P 500.Which of the following statements is true about Ford's beta against the S&P 500?

A) Ford's beta appears to be positive.

B) Ford's beta appears to be negative.

C) Ford's beta appears to be zero- there is no apparent relation between its return and the S&P return.

D) Ford's beta appears to be highly negative.

E) Beta has nothing to do with the relationship seen in this scatterplot.

A) Ford's beta appears to be positive.

B) Ford's beta appears to be negative.

C) Ford's beta appears to be zero- there is no apparent relation between its return and the S&P return.

D) Ford's beta appears to be highly negative.

E) Beta has nothing to do with the relationship seen in this scatterplot.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

64

Air Canada stock has a standard deviation of 25%,while the market index standard deviation is 12%.If the correlation between Air Canada and the market index is 0.33,what is the beta of Air Canada stock?

A) 2.08

B) 0.16

C) 0.69

D) 2.75

E) 1.32

A) 2.08

B) 0.16

C) 0.69

D) 2.75

E) 1.32

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

65

You expect General Motors (GM)to have a beta of 1 over the next year and the beta of Exxon Mobil (XOM)to be 1.2 over the next year.Also,you expect the volatility of General Motors to be 30% and that of Exxon Mobil to be 40% over the next year.Which stock has more systematic risk? Which stock has more total risk?

A) GM, GM

B) GM, XOM

C) XOM, XOM

D) XOM, GM

E) They both have the same risks.

A) GM, GM

B) GM, XOM

C) XOM, XOM

D) XOM, GM

E) They both have the same risks.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

66

The market or equity risk premium can be estimated by computing the historical average excess return of the market portfolio.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

67

Is it possible for a stock to have high total risk but low systematic risk?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

68

The market portfolio is the portfolio of all risky investments held

A) in descending weights.

B) in ascending weights.

C) in proportion to their value.

D) based on previous year performance.

E) in equal weights.

A) in descending weights.

B) in ascending weights.

C) in proportion to their value.

D) based on previous year performance.

E) in equal weights.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

69

How does the S&P/TSX Composite index rank in terms of number and market capitalization of Canadian public firms?

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

70

You expect General Motors (GM)to have a beta of 1.3 over the next year and the beta of Exxon Mobil (XOM)to be 0.9 over the next year.Also,you expect the volatility of General Motors to be 40% and that of Exxon Mobil to be 30% over the next year.Which stock has more systematic risk? Which stock has more total risk?

A) XOM, GM

B) XOM, XOM

C) GM, XOM

D) GM, GM

E) They both have the same risks.

A) XOM, GM

B) XOM, XOM

C) GM, XOM

D) GM, GM

E) They both have the same risks.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

71

You observe that AT&T stock and the S&P 500 have the following weekly returns:

If this pattern of stock returns is typical of AT&T stock,and you calculated a beta against the S&P 500,which of the following is true?

A) AT&T's beta is negative.

B) AT&T's beta is zero.

C) AT&T's beta is positive.

D) AT&T's beta is highly negative.

E) Beta cannot be calculated from this data.

If this pattern of stock returns is typical of AT&T stock,and you calculated a beta against the S&P 500,which of the following is true?

A) AT&T's beta is negative.

B) AT&T's beta is zero.

C) AT&T's beta is positive.

D) AT&T's beta is highly negative.

E) Beta cannot be calculated from this data.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

72

If you build a large enough portfolio,you can diversify away all ________ risk,but you will be left with ________ risk.

A) diversifiable, unsystematic

B) unsystematic, systematic

C) systematic, undiversifiable

D) diversifiable, diversifiable

E) common, unsystematic

A) diversifiable, unsystematic

B) unsystematic, systematic

C) systematic, undiversifiable

D) diversifiable, diversifiable

E) common, unsystematic

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

73

Air Canada stock has a standard deviation of 10%,while the market index standard deviation is 7%.If the correlation between Air Canada and the market index is 0.85,what is the beta of Air Canada stock?

A) 0.60

B) 1.21

C) 1.43

D) 0.85

E) 1.0

A) 0.60

B) 1.21

C) 1.43

D) 0.85

E) 1.0

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

74

The amount of a stock's risk that is diversified away

A) is independent of the portfolio that you add it to.

B) depends on market risk premium.

C) depends on the risk-free rate of interest.

D) depends on the portfolio that you add it to.

E) depends on its market capitalization.

A) is independent of the portfolio that you add it to.

B) depends on market risk premium.

C) depends on the risk-free rate of interest.

D) depends on the portfolio that you add it to.

E) depends on its market capitalization.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

75

You expect General Motors (GM)to have a beta of 1.5 over the next year and the beta of Exxon Mobil (XOM)to be 1.9 over the next year.Also,you expect the volatility of General Motors to be 50% and that of Exxon Mobil to be 35% over the next year.Which stock has more systematic risk? Which stock has more total risk?

A) XOM, GM

B) GM, XOM

C) GM, GM

D) XOM, XOM

E) They both have the same risks.

A) XOM, GM

B) GM, XOM

C) GM, GM

D) XOM, XOM

E) They both have the same risks.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

76

A linear regression was done to estimate the relation between Sprint's stock returns and the market's return.The intercept of the line was found to be 0.23 and the slope was 1.47.Which of the following statements is true regarding Sprint's stock?

A) Sprint's beta is 0.23.

B) Sprint's beta is 1.47.

C) The risk-free rate is 1.47%.

D) The standard deviation of Sprint's excess returns is 23%.

E) Sprint's beta is between 0.23 and 1.47.

A) Sprint's beta is 0.23.

B) Sprint's beta is 1.47.

C) The risk-free rate is 1.47%.

D) The standard deviation of Sprint's excess returns is 23%.

E) Sprint's beta is between 0.23 and 1.47.

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

77

Companies that sell household products and food have very little relation to the state of the economy because such basic needs do not go away.These stocks tend to have ________ betas.

A) high

B) low

C) negative

D) zero

E) very high

A) high

B) low

C) negative

D) zero

E) very high

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

78

For each 1% change in the market portfolio's excess return,the investment's excess return is expected to change by ________ percent due to risks that it has in common with the market.

A) beta

B) alpha

C) zero

D) more than 1

E) less than 1

A) beta

B) alpha

C) zero

D) more than 1

E) less than 1

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

79

The beta of the market portfolio is:

A) 0

B) -1

C) 2

D) 1

E) 10

A) 0

B) -1

C) 2

D) 1

E) 10

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

80

The S&P 500 index traditionally is a ________ portfolio of the 500 largest U.S.stocks.

A) value weighted

B) equally weighted

C) chain weighted

D) price weighted

E) reputation weighted

A) value weighted

B) equally weighted

C) chain weighted

D) price weighted

E) reputation weighted

Unlock Deck

Unlock for access to all 102 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 102 flashcards in this deck.