Deck 20: Audit of the Inventory and Warehousing Cycle

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Auditor tests of physical controls over raw materials,work-in-process,and finished goods are performed by:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Given the following information about your audit client,perform analytical procedures and comment on your findings.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

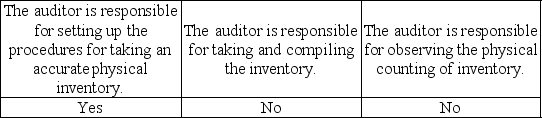

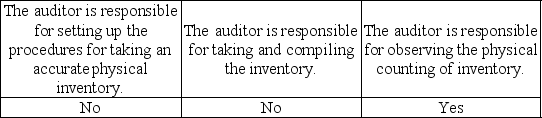

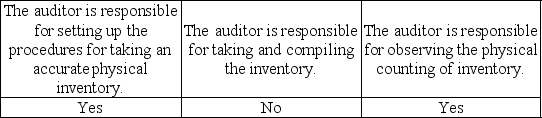

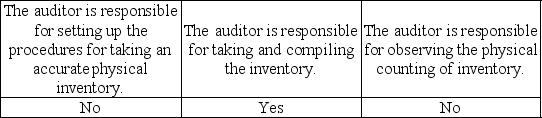

Which of the following statements is correct regarding the auditor's responsibility with respect to the year-end inventory procedures of an audit client?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The physical counting of inventory may be performed at which of the following times?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/116

Play

Full screen (f)

Deck 20: Audit of the Inventory and Warehousing Cycle

1

The main difference between job order and process costing systems is that:

A) one accumulates costs by materials issued and the other by labor incurred.

B) one accumulates costs by individual jobs and the other by particular processes.

C) one emphasizes costs accumulated in completed products and the other emphasizes costs associated with work-in-process.

D) one emphasizes costs adding value to the product and the other emphasizes costs incurred because of waste, scrap, and obsolescence.

A) one accumulates costs by materials issued and the other by labor incurred.

B) one accumulates costs by individual jobs and the other by particular processes.

C) one emphasizes costs accumulated in completed products and the other emphasizes costs associated with work-in-process.

D) one emphasizes costs adding value to the product and the other emphasizes costs incurred because of waste, scrap, and obsolescence.

B

2

The inventory and warehousing cycle can be thought of as having two separate but closely related systems,one involving the actual physical flow of goods,and the other the:

A) related costs.

B) storage of the goods.

C) internal control over those goods.

D) prevention of waste, obsolescence, and theft.

A) related costs.

B) storage of the goods.

C) internal control over those goods.

D) prevention of waste, obsolescence, and theft.

A

3

In most manufacturing companies,the inventory and warehousing cycle begins with the:

A) receipt of a customer's order.

B) completion of production of a customer's order.

C) initiation of production of a customer's order.

D) acquisition of raw materials for production of an order.

A) receipt of a customer's order.

B) completion of production of a customer's order.

C) initiation of production of a customer's order.

D) acquisition of raw materials for production of an order.

D

4

Inventory is a complex area to audit for all but which of the following reasons?

A) Inventory is often in different locations.

B) There are several acceptable valuation methods and some entities use different methods for different types of inventory.

C) Inventory is often the largest account on the balance sheet.

D) Inventory valuation includes few estimates.

A) Inventory is often in different locations.

B) There are several acceptable valuation methods and some entities use different methods for different types of inventory.

C) Inventory is often the largest account on the balance sheet.

D) Inventory valuation includes few estimates.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

5

Receipt of ordered materials by the receiving department will generate the completion of a form called the:

A) bill of lading.

B) receiving report.

C) materials requisition.

D) inventory acquisition summary.

A) bill of lading.

B) receiving report.

C) materials requisition.

D) inventory acquisition summary.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

6

State the six functions that make up the inventory and warehousing cycle and,for each function,identify the related documents and/or records that would be used by a manufacturing company.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

7

________ accumulate costs by individual jobs as material is issued into production and labor costs are incurred.

A) Just-in-time production systems

B) Job order cost systems

C) Process cost systems

D) Manufacturing systems

A) Just-in-time production systems

B) Job order cost systems

C) Process cost systems

D) Manufacturing systems

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

8

Inventory compilation tests are used to verify that the inventory is recorded at the lower of cost or market.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

9

What are two factors affecting the complexity of the audit of inventory?

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

10

In job cost systems,costs are accumulated by individual jobs.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

11

In process cost systems,costs are accumulated by individual jobs.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

12

Handling the receipt of ordered goods is a part of the ________ cycle.

A) purchasing

B) acquisition and payment

C) inventory

D) inventory and warehousing

A) purchasing

B) acquisition and payment

C) inventory

D) inventory and warehousing

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

13

Master files,spreadsheets,and reports that accumulate material,labor,and overhead as the costs are incurred are:

A) accounting systems.

B) storeroom documents.

C) cost accounting records.

D) finished goods inventory records.

A) accounting systems.

B) storeroom documents.

C) cost accounting records.

D) finished goods inventory records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

14

The audit of the inventory and warehousing cycle consists of five parts.State the five parts and,for each part,identify the cycle in which that part is tested by the auditor.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

15

Auditors test the quantity of materials charged to work-in-process by tracing these quantities to:

A) cost ledgers.

B) perpetual inventory records.

C) receiving reports.

D) material requisitions.

A) cost ledgers.

B) perpetual inventory records.

C) receiving reports.

D) material requisitions.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

16

________ is normally characterized as a difficult and complex account to audit.

A) Property, plant and equipment

B) Cash

C) Inventory

D) Prepaid insurance

A) Property, plant and equipment

B) Cash

C) Inventory

D) Prepaid insurance

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

17

The audit tests to verify that the client is using an inventory method which is generally accepted and to verify that physical counts were correctly summarized are performed during the audit of the:

A) acquisition and payments cycle.

B) payroll and personnel cycle.

C) inventory and warehousing cycle.

D) sales and collection cycle.

A) acquisition and payments cycle.

B) payroll and personnel cycle.

C) inventory and warehousing cycle.

D) sales and collection cycle.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

18

While separate perpetual inventory records are normally kept for raw materials and finished goods,most companies do not use perpetual records for work-in-process.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is not a function within the inventory and warehousing cycle?

A) Process the goods

B) Store raw materials

C) Ship finished goods

D) Process invoices for shipped goods

A) Process the goods

B) Store raw materials

C) Ship finished goods

D) Process invoices for shipped goods

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

20

The audit of the inventory and warehousing cycle will be affected by the results from other business processes.Identify the "other" business cycles and how they impact the audit of inventory.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

21

The receipt of raw materials is a part of the acquisition and payment cycle.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

22

When auditing inventory cost accounting,the auditor is concerned with all of the following except for:

A) net realizable value.

B) unit cost records.

C) physical controls over inventory.

D) documents and records for transferring inventory.

A) net realizable value.

B) unit cost records.

C) physical controls over inventory.

D) documents and records for transferring inventory.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

23

A major difficulty in the verification of inventory cost records for the purpose of inventory valuation is in determining the reasonableness of the:

A) direct labor hourly rate.

B) raw material per unit cost.

C) manufacturing overhead costs.

D) number of direct labor hours applied.

A) direct labor hourly rate.

B) raw material per unit cost.

C) manufacturing overhead costs.

D) number of direct labor hours applied.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

24

The physical observation of the inventory and the acquisition of raw materials are part of the inventory and warehousing cycle.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

25

Auditor tests of the physical controls over raw materials,work in process,and finished goods are generally limited to:

A) observation and confirmation.

B) observation and inquiry.

C) inquiry and reconciliation.

D) observation and reconciliation.

A) observation and confirmation.

B) observation and inquiry.

C) inquiry and reconciliation.

D) observation and reconciliation.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

26

In order to strengthen controls over cost accounting information,a company should consider implementing:

A) perpetual inventory master files.

B) a job order cost accounting system.

C) an accounting system that keeps separate the records of the accounting department from the records of the production department.

D) an economic quantity order system.

A) perpetual inventory master files.

B) a job order cost accounting system.

C) an accounting system that keeps separate the records of the accounting department from the records of the production department.

D) an economic quantity order system.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

27

An approved purchase requisition form authorizes shipment of goods to customers.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is correct regarding the audit of inventory cost accounting?

A) Cost accounting systems and controls are the same for all manufacturing companies.

B) All companies that have work-in-process must use a perpetual inventory system.

C) Auditors test perpetual inventory master files by examining documentation that supports additions and reductions of inventory amounts in the master files.

D) Manufacturing companies keep their cost accounting records separate from the production and other accounting records.

A) Cost accounting systems and controls are the same for all manufacturing companies.

B) All companies that have work-in-process must use a perpetual inventory system.

C) Auditors test perpetual inventory master files by examining documentation that supports additions and reductions of inventory amounts in the master files.

D) Manufacturing companies keep their cost accounting records separate from the production and other accounting records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

29

Almost all companies need physical controls over their assets to prevent loss.Which of the following is not an example of such a control?

A) Perpetual inventory master files

B) Segregated, limited-access storage areas

C) Custody of assets assigned to specific responsible individuals

D) Approved prenumbered documents for authorizing movement of inventory

A) Perpetual inventory master files

B) Segregated, limited-access storage areas

C) Custody of assets assigned to specific responsible individuals

D) Approved prenumbered documents for authorizing movement of inventory

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following is a significant audit concern related to the transfer of inventory from one location to another?

A) Recorded transfers occurred.

B) Transfers were properly transported.

C) Transfers were properly planned.

D) Transfers represent efficient movement of assets.

A) Recorded transfers occurred.

B) Transfers were properly transported.

C) Transfers were properly planned.

D) Transfers represent efficient movement of assets.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

31

To assure proper segregation of duties,who should maintain the perpetual inventory master files?

A) Production personnel

B) Inventory storeroom personnel

C) Inventory receiving personnel

D) Accounting department personnel

A) Production personnel

B) Inventory storeroom personnel

C) Inventory receiving personnel

D) Accounting department personnel

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

32

If the perpetual inventory master files show lower quantities of inventory than the physical count,an explanation of the difference might be unrecorded:

A) sales.

B) sales discounts.

C) purchases.

D) purchase discounts.

A) sales.

B) sales discounts.

C) purchases.

D) purchase discounts.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

33

Auditor tests of physical controls over raw materials,work-in-process,and finished goods are performed by:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

34

Cost accounting controls are those related to the physical inventory and the consequent costs from the point at which:

A) materials are ordered for purchase until the finished product is sold.

B) the customer's order is received until the finished product is shipped.

C) raw materials are requisitioned until the finished product is sent to storage.

D) raw materials are requisitioned until the finished product is completely manufactured.

A) materials are ordered for purchase until the finished product is sold.

B) the customer's order is received until the finished product is shipped.

C) raw materials are requisitioned until the finished product is sent to storage.

D) raw materials are requisitioned until the finished product is completely manufactured.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is an internal control weakness for a company whose inventory of supplies consists of a large number of individual items?

A) The cycle basis is used for physical counts.

B) Supplies of relatively little value are expensed when purchased.

C) Perpetual inventory records are maintained only for items of significant value.

D) The storekeeper is responsible for maintenance of perpetual inventory records.

A) The cycle basis is used for physical counts.

B) Supplies of relatively little value are expensed when purchased.

C) Perpetual inventory records are maintained only for items of significant value.

D) The storekeeper is responsible for maintenance of perpetual inventory records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

36

When auditing manufacturing overhead costs assigned to inventory,auditors should keep in mind that:

A) GAAP has strict procedures that must be followed when assigning overhead to work-in-process inventory.

B) overhead costs must be allocated to raw materials, work-in-process, and finished goods inventory.

C) management typically allocates overhead using total direct labor dollars as the basis for the allocation.

D) determining the reasonableness of the allocation method is relatively simple for work-in-process inventory.

A) GAAP has strict procedures that must be followed when assigning overhead to work-in-process inventory.

B) overhead costs must be allocated to raw materials, work-in-process, and finished goods inventory.

C) management typically allocates overhead using total direct labor dollars as the basis for the allocation.

D) determining the reasonableness of the allocation method is relatively simple for work-in-process inventory.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

37

One of the auditor's primary concerns in verifying the transfer of inventory from one location to another is that:

A) recorded transfers exist.

B) all actual transfers are recorded.

C) the quantity, date, and description of all recorded transfers are accurate.

D) all of the above.

A) recorded transfers exist.

B) all actual transfers are recorded.

C) the quantity, date, and description of all recorded transfers are accurate.

D) all of the above.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

38

A well-designed computerized system of perpetual inventory master files includes information about the:

A) units of inventory purchased, sold, and on hand.

B) unit costs of inventory purchased, sold, and on hand.

C) units of raw materials, work-in-process, and finished goods.

D) units and unit costs of inventory purchased, sold, and on hand.

A) units of inventory purchased, sold, and on hand.

B) unit costs of inventory purchased, sold, and on hand.

C) units of raw materials, work-in-process, and finished goods.

D) units and unit costs of inventory purchased, sold, and on hand.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

39

The reliability of perpetual inventory master files affects the timing and ________ of the auditor's physical examination of inventory.

A) cutoff

B) accuracy

C) nature

D) extent

A) cutoff

B) accuracy

C) nature

D) extent

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following controls would be appropriate regarding the release of materials from a stockroom?

A) Production employees request materials be delivered to their work areas as they need them.

B) Stockroom employees deliver materials to work areas throughout the day to maintain acceptable levels of safety stock - no written records are maintained.

C) Production employees submit approved requisition forms to the stockroom for materials needed.

D) Production employer in need of materials should personally pick up needed materials from the stockroom.

A) Production employees request materials be delivered to their work areas as they need them.

B) Stockroom employees deliver materials to work areas throughout the day to maintain acceptable levels of safety stock - no written records are maintained.

C) Production employees submit approved requisition forms to the stockroom for materials needed.

D) Production employer in need of materials should personally pick up needed materials from the stockroom.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

41

The audit of cost accounting begins with the internal transfer of assets from raw materials to work-in-process to:

A) manufacturing overhead.

B) finished goods inventory.

C) the perpetual inventory master files.

D) retail sales.

A) manufacturing overhead.

B) finished goods inventory.

C) the perpetual inventory master files.

D) retail sales.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

42

When determining the sample size for the number of items the auditor should count during the physical inventory:

A) it is easy to quantify the number of items based on a formula developed by the AICPA.

B) one of the key determinants that must be considered is internal control over the physical count.

C) one of the key determinants that must be considered is the time involved.

D) generally accepted auditing standards require that at least 80% of the dollar value of the inventory should be included in the sample.

A) it is easy to quantify the number of items based on a formula developed by the AICPA.

B) one of the key determinants that must be considered is internal control over the physical count.

C) one of the key determinants that must be considered is the time involved.

D) generally accepted auditing standards require that at least 80% of the dollar value of the inventory should be included in the sample.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

43

Comparing the physical counts with the perpetual inventory master files satisfies the balance-related audit objective of:

A) classification.

B) observation.

C) completeness.

D) accuracy.

A) classification.

B) observation.

C) completeness.

D) accuracy.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

44

From which of the following evidence-gathering audit procedures would an auditor obtain most assurance concerning the existence of inventories?

A) Observation of physical inventory counts

B) Written inventory representations from management

C) Confirmation of inventories in a public warehouse

D) Auditor's recomputation of inventory extensions

A) Observation of physical inventory counts

B) Written inventory representations from management

C) Confirmation of inventories in a public warehouse

D) Auditor's recomputation of inventory extensions

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

45

A comparison of the current year's inventory turnover ratio with previous years' may indicate the presence of obsolete inventory.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

46

Given the following information about your audit client,perform analytical procedures and comment on your findings.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

47

You are auditing the inventory account and are concerned about the possibility of an inventory overstatement.What is the best audit procedure to detect damaged inventory?

A) Observe the condition of inventory during the client's physical count.

B) Compare the condition of inventory from the previous year's count to the current year.

C) Compare inventory turnover from the previous year's inventory to the current year's inventory.

D) Reconcile the inventory counts to the cost accounting records.

A) Observe the condition of inventory during the client's physical count.

B) Compare the condition of inventory from the previous year's count to the current year.

C) Compare inventory turnover from the previous year's inventory to the current year's inventory.

D) Reconcile the inventory counts to the cost accounting records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

48

Production personnel should ordinarily be responsible for maintaining perpetual inventory records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

49

When auditors observe the client counting inventory,they should be careful to do all of the following except:

A) inquire about items that are likely to be obsolete or damaged.

B) calculate the unit cost of the inventory items.

C) discuss with management the reasons for excluding any material items.

D) observe the counting of the most significant items.

A) inquire about items that are likely to be obsolete or damaged.

B) calculate the unit cost of the inventory items.

C) discuss with management the reasons for excluding any material items.

D) observe the counting of the most significant items.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

50

What are the auditor's primary concerns in verifying the transfer of inventory from one location to another?

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

51

There must be a periodic physical count by the client of the inventory items on hand:

A) only if the client uses the LIFO method.

B) only if the client uses a lower-of-cost-or-market method.

C) regardless of the client's inventory valuation method.

D) only if the client uses either the LIFO or FIFO method.

A) only if the client uses the LIFO method.

B) only if the client uses a lower-of-cost-or-market method.

C) regardless of the client's inventory valuation method.

D) only if the client uses either the LIFO or FIFO method.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

52

If the auditor concludes that physical controls over inventory are so inadequate that the inventory will be difficult to count,the auditor should ordinarily:

A) withdraw from the engagement.

B) issue a qualified audit report.

C) conduct expanded observation tests of physical inventory.

D) hire a specialist to assist the auditor.

A) withdraw from the engagement.

B) issue a qualified audit report.

C) conduct expanded observation tests of physical inventory.

D) hire a specialist to assist the auditor.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

53

Discuss the four aspects of the audit of cost accounting with which the auditor is most concerned.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

54

When verifying the transfer of inventory from one location to another,the audit objectives with which the auditor is primarily concerned are occurrence of recorded transfers,completeness of recorded transfers,and accuracy of recorded transfers.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

55

The extent and timing of an auditor's physical examination of inventory is significantly influenced by the adequacy of the client's perpetual inventory records.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

56

Which one of the following analytical procedures would be most useful in alerting the auditor to the possibility of obsolete inventory?

A) Compare gross margin percentage with previous years'.

B) Compare unit costs of inventory with previous years'.

C) Compare inventory turnover ratio with previous years'.

D) Compare current year manufacturing costs with previous years'.

A) Compare gross margin percentage with previous years'.

B) Compare unit costs of inventory with previous years'.

C) Compare inventory turnover ratio with previous years'.

D) Compare current year manufacturing costs with previous years'.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

57

In addition to performing analytical procedures that examine the relationship of inventory account balances with related financial statement accounts,auditor's will often use non-financial measures in determining the reasonableness of inventory balances.List below at least two non-financial measures that may be useful to auditors.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

58

Management typically allocates overhead using total raw materials as the basis for the allocation.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following statements is correct regarding the auditor's responsibility with respect to the year-end inventory procedures of an audit client?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

60

It is frequently possible to test the physical inventory prior to the balance sheet date when:

A) there are accurate perpetual inventory master files.

B) year-end sales are small.

C) the internal control system is no better at year-end than at an earlier point in time.

D) the client counts inventory at interim dates.

A) there are accurate perpetual inventory master files.

B) year-end sales are small.

C) the internal control system is no better at year-end than at an earlier point in time.

D) the client counts inventory at interim dates.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

61

To best ascertain that a company has properly included merchandise that it owns in its ending inventory,the auditor should review and test the:

A) terms of the open purchase orders.

B) purchase cutoff procedures.

C) contractual commitments made by the purchasing department.

D) purchase invoices received on or around year-end.

A) terms of the open purchase orders.

B) purchase cutoff procedures.

C) contractual commitments made by the purchasing department.

D) purchase invoices received on or around year-end.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

62

When there are no perpetual inventory files and inventory is material:

A) an audit cannot be performed, so the auditor must issue a disclaimer.

B) a physical inventory should be taken by the client near year-end.

C) the auditor will have to perform the inventory count and determine valuation.

D) the auditor need not observe inventory counts but must do test counts.

A) an audit cannot be performed, so the auditor must issue a disclaimer.

B) a physical inventory should be taken by the client near year-end.

C) the auditor will have to perform the inventory count and determine valuation.

D) the auditor need not observe inventory counts but must do test counts.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

63

If a client intends to count inventory at an interim date,the auditor should expect there to be all of the following except:

A) controls over the preparation and maintenance of perpetual inventory records.

B) competent personnel assigned to count the inventory.

C) third-party inventory counting specialists.

D) an adequately designed plan to count the inventory.

A) controls over the preparation and maintenance of perpetual inventory records.

B) competent personnel assigned to count the inventory.

C) third-party inventory counting specialists.

D) an adequately designed plan to count the inventory.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

64

The auditor's tour of the client's inventory facilities should be led by:

A) a member of the audit committee.

B) the CFO.

C) a plant supervisor.

D) the company president.

A) a member of the audit committee.

B) the CFO.

C) a plant supervisor.

D) the company president.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

65

A common inventory observation procedure is to select a random sample of tag numbers and identify the tag with that number attached to the actual inventory item.The audit objective being achieved by this procedure is:

A) inventory as recorded on tags actually exists (existence).

B) existing inventory is counted and tagged (completeness).

C) inventory is counted accurately (accuracy).

D) inventory is classified correctly (classification).

A) inventory as recorded on tags actually exists (existence).

B) existing inventory is counted and tagged (completeness).

C) inventory is counted accurately (accuracy).

D) inventory is classified correctly (classification).

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

66

The auditor generally decides whether the inventory count can be taken before year-end primarily on the basis of:

A) audit efficiency.

B) accuracy of the perpetual inventory master files.

C) client convenience.

D) audit staff availability.

A) audit efficiency.

B) accuracy of the perpetual inventory master files.

C) client convenience.

D) audit staff availability.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

67

The most important part of the observation of inventory is to determine whether:

A) all counts are accurate.

B) the inventory-takers are qualified.

C) obsolete inventory has been identified.

D) the physical count is being taken in accordance with the client's instructions.

A) all counts are accurate.

B) the inventory-takers are qualified.

C) obsolete inventory has been identified.

D) the physical count is being taken in accordance with the client's instructions.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

68

Auditors need to understand the client's physical inventory count controls before the count of the inventory begins so that:

A) the auditors can accurately count and tag the inventory for the client.

B) the auditors can make constructive suggestions as to the adequacy of the procedures.

C) the client will be informed on exactly what items the auditor intends to test count.

D) the auditor can communicate any weaknesses directly to the audit committee.

A) the auditors can accurately count and tag the inventory for the client.

B) the auditors can make constructive suggestions as to the adequacy of the procedures.

C) the client will be informed on exactly what items the auditor intends to test count.

D) the auditor can communicate any weaknesses directly to the audit committee.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

69

An auditor must inquire about consigned or customer inventory included on the client's premises to satisfy the balance-related audit objective of:

A) cutoff.

B) classification.

C) rights.

D) completeness.

A) cutoff.

B) classification.

C) rights.

D) completeness.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

70

When a physical count of inventory is performed at an interim date,the auditor observes it at that time and tests the perpetual records for transactions:

A) throughout the year.

B) which are a representative sample of the period under audit.

C) from the date of the count to year-end.

D) from the date of the count to the end of the audit field work.

A) throughout the year.

B) which are a representative sample of the period under audit.

C) from the date of the count to year-end.

D) from the date of the count to the end of the audit field work.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

71

The physical counting of inventory may be performed at which of the following times?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

72

McKesson & Robbins Company is a well-known audit case involving auditor responsibility.What occurred at the McKesson & Robbins Company to change the way in which auditors audit inventory?

A) The company recorded nonexistent inventory.

B) The auditor did not perform any audit tests of the inventory.

C) The auditor and company colluded to overstate inventory balances.

D) The company counted inventory three months prior to year-end.

A) The company recorded nonexistent inventory.

B) The auditor did not perform any audit tests of the inventory.

C) The auditor and company colluded to overstate inventory balances.

D) The company counted inventory three months prior to year-end.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following is an accurate statement regarding inventory and risk?

A) Inventory with a high business risk includes products with potential obsolescence.

B) Auditors often have a greater concern for misstatements when inventory is stored in one warehouse.

C) Inherent risk is generally set at low for manufacturing companies.

D) Performance materiality for inventory is determined before assessing client business risk.

A) Inventory with a high business risk includes products with potential obsolescence.

B) Auditors often have a greater concern for misstatements when inventory is stored in one warehouse.

C) Inherent risk is generally set at low for manufacturing companies.

D) Performance materiality for inventory is determined before assessing client business risk.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

74

A useful starting point for becoming familiar with the client's inventory is for the auditor to:

A) read the AICPA's Industry Audit Guide.

B) review accounting theory covering special inventory problems.

C) read the client's accounting manual.

D) tour the client's facility.

A) read the AICPA's Industry Audit Guide.

B) review accounting theory covering special inventory problems.

C) read the client's accounting manual.

D) tour the client's facility.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

75

The audit of year-end physical inventories should include steps to verify that the client's purchases and sales cutoffs were adequate.The audit steps should be designed to detect whether merchandise included in the physical count at year-end was not recorded as a:

A) sale in the current period.

B) sale in the subsequent period.

C) purchase in the current period.

D) purchase return in the subsequent period.

A) sale in the current period.

B) sale in the subsequent period.

C) purchase in the current period.

D) purchase return in the subsequent period.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

76

Which one of the following procedures would not be appropriate for an auditor in discharging his responsibilities concerning the client's physical inventories?

A) Confirmation of goods in the hands of public warehouses

B) Supervising the taking of the annual physical inventory

C) Carrying out physical inventory procedures at an interim date

D) Obtaining written representation from the client as to the existence, quality, and dollar amount of the inventory

A) Confirmation of goods in the hands of public warehouses

B) Supervising the taking of the annual physical inventory

C) Carrying out physical inventory procedures at an interim date

D) Obtaining written representation from the client as to the existence, quality, and dollar amount of the inventory

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

77

The test of details of balance procedure which requires the auditor to account for unused inventory tag numbers to make sure none have been deleted is associated with the audit objective of:

A) accuracy.

B) existence.

C) detail tie-in.

D) completeness.

A) accuracy.

B) existence.

C) detail tie-in.

D) completeness.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

78

When an auditor observes that personnel who are responsible for physically counting inventory are not following the inventory instructions,the auditor should:

A) contact a client's supervisor to correct the problem.

B) modify the client's physical inventory instructions.

C) not discuss the problem with client's supervisor in order to maintain independence.

D) assign audit staff to the inventory count.

A) contact a client's supervisor to correct the problem.

B) modify the client's physical inventory instructions.

C) not discuss the problem with client's supervisor in order to maintain independence.

D) assign audit staff to the inventory count.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

79

A common inventory observation procedure is to be alert for items that are damaged,rust- or dust-covered,or located in inappropriate places.The balance-related audit objective being achieved by this procedure is:

A) classification.

B) cutoff.

C) realizable value.

D) rights.

A) classification.

B) cutoff.

C) realizable value.

D) rights.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

80

An auditor selects a random sampling of tag numbers and identifies the tag with that number attached to the actual inventory.The purpose of the procedure is to:

A) obtain proper cutoff information.

B) uncover the inclusion of nonexistent items as inventory.

C) to determine if the client has adequately priced the inventory item.

D) to verify that the client has not changed the recorded counts after the auditor left the premises.

A) obtain proper cutoff information.

B) uncover the inclusion of nonexistent items as inventory.

C) to determine if the client has adequately priced the inventory item.

D) to verify that the client has not changed the recorded counts after the auditor left the premises.

Unlock Deck

Unlock for access to all 116 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 116 flashcards in this deck.