Deck 18: Business Acquisitions and Divestituresassets Versus Shares

Full screen (f)

Question

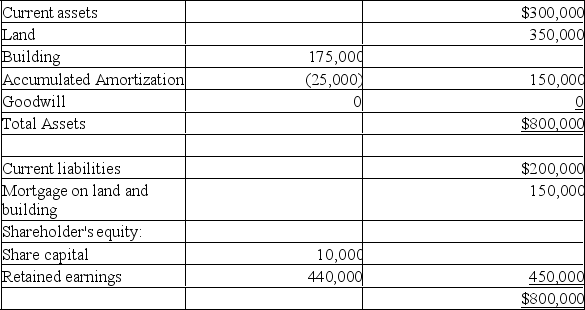

Mountain Wear Inc.(MWI)is a Canadian-controlled private corporation.Fred Martin is the sole shareholder.The PUC and ACB of Fred's shares is $10,000.The year-end balance sheet for MWI is as follows:

Additional information is available for MWI:

Additional information is available for MWI:

The current assets consist of accounts receivables and inventory,which have costs equal to their market values.

The UCC of the building is $160,000.

The land is currently valued at $450,000.

The building has a FMV of $205,000.

Goodwill has a FMV of $100,000.

Additional information:

Fred has used all of his capital gains deduction.

MWI is not associated with any other corporations for tax purposes.

Fred has recently been offered $450,000 for his shares by a local competitor.

Fred is in a 45% tax bracket on regular income,28% on eligible dividends,and 37% on non-eligible dividends.

Due to the timing of the sale,if assets are sold,the small business deduction will be available for all business income.

The tax rate on earnings subject to the small business deduction is 13%,and 27% on additional business income.

The combined (federal and provincial)tax rate on corporate investment income is 50 2/3% and the refundable rate is 30 2/3%.

The RDTOH balance prior to the sale was NIL.

Required:

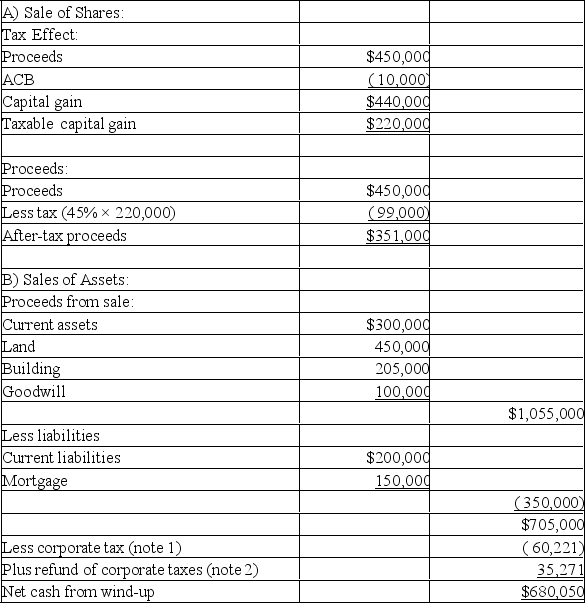

A)Calculate the after-tax proceeds of the sale if the shares of MWI are sold.

B)Calculate the net cash available for wind-up from MWI in an asset sale.(The proceeds will be distributed to Fred by way of a dividend.)

(Round all amounts to zero decimal places.)

Additional information is available for MWI:The current assets consist of accounts receivables and inventory,which have costs equal to their market values.

The UCC of the building is $160,000.

The land is currently valued at $450,000.

The building has a FMV of $205,000.

Goodwill has a FMV of $100,000.

Additional information:

Fred has used all of his capital gains deduction.

MWI is not associated with any other corporations for tax purposes.

Fred has recently been offered $450,000 for his shares by a local competitor.

Fred is in a 45% tax bracket on regular income,28% on eligible dividends,and 37% on non-eligible dividends.

Due to the timing of the sale,if assets are sold,the small business deduction will be available for all business income.

The tax rate on earnings subject to the small business deduction is 13%,and 27% on additional business income.

The combined (federal and provincial)tax rate on corporate investment income is 50 2/3% and the refundable rate is 30 2/3%.

The RDTOH balance prior to the sale was NIL.

Required:

A)Calculate the after-tax proceeds of the sale if the shares of MWI are sold.

B)Calculate the net cash available for wind-up from MWI in an asset sale.(The proceeds will be distributed to Fred by way of a dividend.)

(Round all amounts to zero decimal places.)

Question

Question

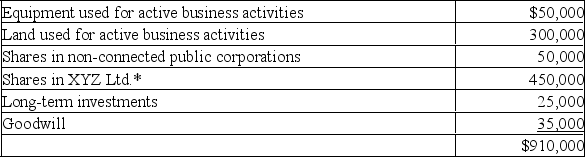

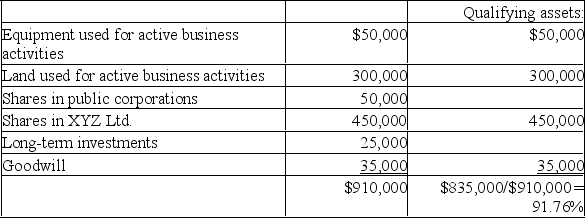

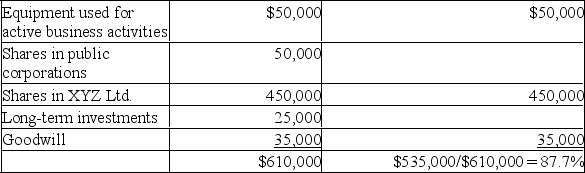

It is the end of 20x8,and ABC Inc.(a CCPC)is for sale.Jane,the sole shareholder would like to know if the company is currently a qualified small business corporation.Jane has provided you with the following information:

All of the business activities of ABC Inc.have taken place in Canada.

The following amounts represent fair market values of the company's assets:

*ABC owns 35% of the shares of XYZ,which is a small business corporation with 100% of the fair market value of its assets consistently used in active business in Canada.

*ABC owns 35% of the shares of XYZ,which is a small business corporation with 100% of the fair market value of its assets consistently used in active business in Canada.

Additional information:

The shares have not changed hands since the company began operations four years ago.

The land was acquired at the beginning of 20x8 with a five-year mortgage.

All of the other asset values have remained constant over the past three years.

Required:

Determine the following for ABC Inc.:

A)Is ABC Inc.a 'small business corporation' (SBC)? Show your calculations to support your answer.

B)Is ABC Inc.a 'qualified small business corporation' (QSBC)? Show calculations to support your answer.

All of the business activities of ABC Inc.have taken place in Canada.

The following amounts represent fair market values of the company's assets:

*ABC owns 35% of the shares of XYZ,which is a small business corporation with 100% of the fair market value of its assets consistently used in active business in Canada.Additional information:

The shares have not changed hands since the company began operations four years ago.

The land was acquired at the beginning of 20x8 with a five-year mortgage.

All of the other asset values have remained constant over the past three years.

Required:

Determine the following for ABC Inc.:

A)Is ABC Inc.a 'small business corporation' (SBC)? Show your calculations to support your answer.

B)Is ABC Inc.a 'qualified small business corporation' (QSBC)? Show calculations to support your answer.

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/8

Play

Full screen (f)

Deck 18: Business Acquisitions and Divestituresassets Versus Shares

1

Mountain Wear Inc.(MWI)is a Canadian-controlled private corporation.Fred Martin is the sole shareholder.The PUC and ACB of Fred's shares is $10,000.The year-end balance sheet for MWI is as follows:

Additional information is available for MWI:

The current assets consist of accounts receivables and inventory,which have costs equal to their market values.

The UCC of the building is $160,000.

The land is currently valued at $450,000.

The building has a FMV of $205,000.

Goodwill has a FMV of $100,000.

Additional information:

Fred has used all of his capital gains deduction.

MWI is not associated with any other corporations for tax purposes.

Fred has recently been offered $450,000 for his shares by a local competitor.

Fred is in a 45% tax bracket on regular income,28% on eligible dividends,and 37% on non-eligible dividends.

Due to the timing of the sale,if assets are sold,the small business deduction will be available for all business income.

The tax rate on earnings subject to the small business deduction is 13%,and 27% on additional business income.

The combined (federal and provincial)tax rate on corporate investment income is 50 2/3% and the refundable rate is 30 2/3%.

The RDTOH balance prior to the sale was NIL.

Required:

A)Calculate the after-tax proceeds of the sale if the shares of MWI are sold.

B)Calculate the net cash available for wind-up from MWI in an asset sale.(The proceeds will be distributed to Fred by way of a dividend.)

(Round all amounts to zero decimal places.)

Additional information is available for MWI:The current assets consist of accounts receivables and inventory,which have costs equal to their market values.

The UCC of the building is $160,000.

The land is currently valued at $450,000.

The building has a FMV of $205,000.

Goodwill has a FMV of $100,000.

Additional information:

Fred has used all of his capital gains deduction.

MWI is not associated with any other corporations for tax purposes.

Fred has recently been offered $450,000 for his shares by a local competitor.

Fred is in a 45% tax bracket on regular income,28% on eligible dividends,and 37% on non-eligible dividends.

Due to the timing of the sale,if assets are sold,the small business deduction will be available for all business income.

The tax rate on earnings subject to the small business deduction is 13%,and 27% on additional business income.

The combined (federal and provincial)tax rate on corporate investment income is 50 2/3% and the refundable rate is 30 2/3%.

The RDTOH balance prior to the sale was NIL.

Required:

A)Calculate the after-tax proceeds of the sale if the shares of MWI are sold.

B)Calculate the net cash available for wind-up from MWI in an asset sale.(The proceeds will be distributed to Fred by way of a dividend.)

(Round all amounts to zero decimal places.)

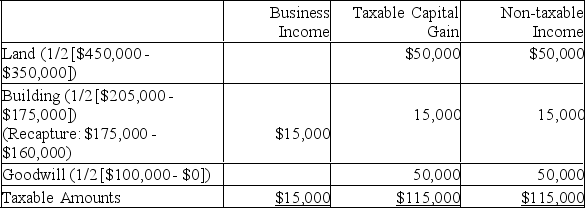

Note 1:

Note 1: Corporate tax (rounded):

Corporate tax (rounded): Note 2:

Note 2:Refund when income is distributed to Fred = $35,271 ($115,000 * 30 2/3%).

2

A purchaser has agreed to purchase all of the shares of Tee Co.,a CCPC.Tee Co.owns fifteen significant capital assets,all of which have appreciated in value.Which of the following is TRUE?

A)The purchaser will obtain a cost base of the assets equal to their fair market values.

B)Capital cost allowance will be based on higher asset values for the purchaser than was the case for the vendor.

C)The sale will result in business income for the vendor.

D)The purchaser will be responsible for the liabilities of Tee Co.

A)The purchaser will obtain a cost base of the assets equal to their fair market values.

B)Capital cost allowance will be based on higher asset values for the purchaser than was the case for the vendor.

C)The sale will result in business income for the vendor.

D)The purchaser will be responsible for the liabilities of Tee Co.

D

3

It is the end of 20x8,and ABC Inc.(a CCPC)is for sale.Jane,the sole shareholder would like to know if the company is currently a qualified small business corporation.Jane has provided you with the following information:

All of the business activities of ABC Inc.have taken place in Canada.

The following amounts represent fair market values of the company's assets:

*ABC owns 35% of the shares of XYZ,which is a small business corporation with 100% of the fair market value of its assets consistently used in active business in Canada.

Additional information:

The shares have not changed hands since the company began operations four years ago.

The land was acquired at the beginning of 20x8 with a five-year mortgage.

All of the other asset values have remained constant over the past three years.

Required:

Determine the following for ABC Inc.:

A)Is ABC Inc.a 'small business corporation' (SBC)? Show your calculations to support your answer.

B)Is ABC Inc.a 'qualified small business corporation' (QSBC)? Show calculations to support your answer.

All of the business activities of ABC Inc.have taken place in Canada.

The following amounts represent fair market values of the company's assets:

*ABC owns 35% of the shares of XYZ,which is a small business corporation with 100% of the fair market value of its assets consistently used in active business in Canada.Additional information:

The shares have not changed hands since the company began operations four years ago.

The land was acquired at the beginning of 20x8 with a five-year mortgage.

All of the other asset values have remained constant over the past three years.

Required:

Determine the following for ABC Inc.:

A)Is ABC Inc.a 'small business corporation' (SBC)? Show your calculations to support your answer.

B)Is ABC Inc.a 'qualified small business corporation' (QSBC)? Show calculations to support your answer.

ABC Inc.is both a small business corporation and a qualified small business corporation.

A)At the point of sale,>91% of ABC's assets were a combination of assets used in active business and shares in a connected small business corporation,thus meeting the 90% FMV of assets test required for a 'small business corporation'.

B)During the previous 24 months (prior to the purchase of the land),>87% of ABC's assets were a combination of assets used in active business and shares in a connected corporation.(While the active assets in ABC alone do not meet the 50% test,the combination of the active assets and the shares in XYZ Ltd.meets the 50% test since XYZ Ltd.has more than 90% of the fair market value of its assets used in active business in Canada.)

B)During the previous 24 months (prior to the purchase of the land),>87% of ABC's assets were a combination of assets used in active business and shares in a connected corporation.(While the active assets in ABC alone do not meet the 50% test,the combination of the active assets and the shares in XYZ Ltd.meets the 50% test since XYZ Ltd.has more than 90% of the fair market value of its assets used in active business in Canada.)

ABC is a qualified small business corporation (QSBC)since:

ABC is a qualified small business corporation (QSBC)since:

a)it is a small business corporation at the time of sale,

b)the shares have not been held by an unrelated person during the past 24 months,and

c)ABC meets the 24 month > 50% FMV of assets test since XYZ (which is required to meet the >50% test)meets the > 90% FMV test.

A)At the point of sale,>91% of ABC's assets were a combination of assets used in active business and shares in a connected small business corporation,thus meeting the 90% FMV of assets test required for a 'small business corporation'.

B)During the previous 24 months (prior to the purchase of the land),>87% of ABC's assets were a combination of assets used in active business and shares in a connected corporation.(While the active assets in ABC alone do not meet the 50% test,the combination of the active assets and the shares in XYZ Ltd.meets the 50% test since XYZ Ltd.has more than 90% of the fair market value of its assets used in active business in Canada.) ABC is a qualified small business corporation (QSBC)since:a)it is a small business corporation at the time of sale,

b)the shares have not been held by an unrelated person during the past 24 months,and

c)ABC meets the 24 month > 50% FMV of assets test since XYZ (which is required to meet the >50% test)meets the > 90% FMV test.

4

The Flower Company is for sale.The anticipated average profits for the next five years of the business have been calculated at $150,000.The business has been valued at $750,000 using the earnings method.The net tangible assets have been appraised at $625,000.Which of the following is TRUE for the Flower Company?

A)The company is expected to yield a 20% return for the purchaser, and is, therefore, a low risk investment.

B)The company is expected to yield a 20% return for the purchaser, and goodwill of $125,000 is present.

C)The company is expected to yield a 24% return for the purchaser, and goodwill of $125,000 is present.

D)The company is expected to yield a 24% return for the purchaser, and goodwill of $475,000 is present.

A)The company is expected to yield a 20% return for the purchaser, and is, therefore, a low risk investment.

B)The company is expected to yield a 20% return for the purchaser, and goodwill of $125,000 is present.

C)The company is expected to yield a 24% return for the purchaser, and goodwill of $125,000 is present.

D)The company is expected to yield a 24% return for the purchaser, and goodwill of $475,000 is present.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

5

Stick Co.owns land with a fair market value of $100,000,a building with a fair market value of $75,000,and equipment with a fair market value of $25,000.These assets are used for active business conducted in Canada.Which of the following would disqualify Stick Co.from being a small business corporation?

A)Stick Co.also owns 40% of the non-eligible shares of Rock Co.(a small business corporation), which have a fair market value of $20,000.

B)Stick Co.also owns portfolio shares in Leaf Co., (with less than 1% ownership), which have a fair market value of $5,000.

C)Stick Co.also has long-term investments valued at $30,000.

D)Stick Co.sold the equipment and used the funds to purchase 35% of the shares of Tree Co., a small business corporation.

A)Stick Co.also owns 40% of the non-eligible shares of Rock Co.(a small business corporation), which have a fair market value of $20,000.

B)Stick Co.also owns portfolio shares in Leaf Co., (with less than 1% ownership), which have a fair market value of $5,000.

C)Stick Co.also has long-term investments valued at $30,000.

D)Stick Co.sold the equipment and used the funds to purchase 35% of the shares of Tree Co., a small business corporation.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

6

A purchaser has agreed to purchase the shares of a qualified small business corporation.Which of the following is not applicable?

A)The seller may be eligible for the capital gains deduction.

B)The purchaser may try to discount the value of the shares if a future sale of the assets may result in a tax liability.

C)The sale will result in the immediate taxation of the corporation, and the after-tax proceeds will be paid to the seller.

D)The purchaser will assume the corporation's current UCC values.

A)The seller may be eligible for the capital gains deduction.

B)The purchaser may try to discount the value of the shares if a future sale of the assets may result in a tax liability.

C)The sale will result in the immediate taxation of the corporation, and the after-tax proceeds will be paid to the seller.

D)The purchaser will assume the corporation's current UCC values.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

7

Sam wishes to purchase Kitchen Cabinets,Inc.(KCI)Which of the following is TRUE if Sam purchases the assets of the corporation rather than the shares from the company's sole shareholder,Brent?

A)Payment of the purchase price will flow directly to Brent.

B)Sam will have no choice but to assume the liabilities of KCI.

C)Kitchen Cabinets Inc.may be subject to business income and capital gains.

D)Brent will be eligible to use for the capital gains deduction on the sale.

A)Payment of the purchase price will flow directly to Brent.

B)Sam will have no choice but to assume the liabilities of KCI.

C)Kitchen Cabinets Inc.may be subject to business income and capital gains.

D)Brent will be eligible to use for the capital gains deduction on the sale.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

8

There are a number of key tax effects that must be considered during a business divestiture and acquisition,from the perspectives of both the vendor and the purchaser.Match the following tax considerations with the most appropriate answer from the list below.Use each answer only once.

Tax consideration:

1.A change in control will restrict the use of losses._____

2.Capital gains and business income may occur in the business,reducing the after-tax proceeds._____

3.The capital gain deduction may apply._____

4.The cost base for assets is based on their market value._____

Answers:

a.A key tax consideration for the sale of shares from the vendor's perspective.

b.A key tax consideration for the sale of assets from the vendor's perspective.

c.A key tax consideration for the purchase of assets from the purchaser's perspective.

d.A key tax consideration for the purchase of shares from the purchaser's perspective.

Tax consideration:

1.A change in control will restrict the use of losses._____

2.Capital gains and business income may occur in the business,reducing the after-tax proceeds._____

3.The capital gain deduction may apply._____

4.The cost base for assets is based on their market value._____

Answers:

a.A key tax consideration for the sale of shares from the vendor's perspective.

b.A key tax consideration for the sale of assets from the vendor's perspective.

c.A key tax consideration for the purchase of assets from the purchaser's perspective.

d.A key tax consideration for the purchase of shares from the purchaser's perspective.

Unlock Deck

Unlock for access to all 8 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 8 flashcards in this deck.