Deck 13: Personal Financial Statements and Accounting for Governments and Not-For-Profit Organizations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

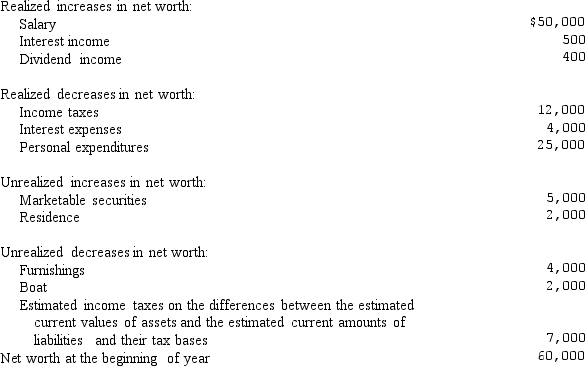

For Howard and Joyce,the changes in net worth for the year ended December 31,2012,are detailed as follows.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2010.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2010.

Question

Question

Question

Question

Question

Question

Question

Question

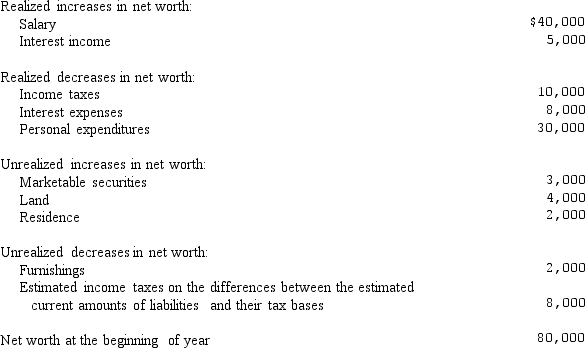

For Bill and Linda,the changes in net worth for the year ended December 31,2012,are detailed as follows.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2012.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2012.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 13: Personal Financial Statements and Accounting for Governments and Not-For-Profit Organizations

1

All cash receipts and disbursements,of governmental agencies,not required to be accounted for in another fund are accounted for in which of the following funds?

A)Fiduciary fund

B)Proprietary fund

C)General fund

D)Debt service fund

E)Special assessment fund

A)Fiduciary fund

B)Proprietary fund

C)General fund

D)Debt service fund

E)Special assessment fund

C

2

For a statement of changes in net worth,which of the following would be a realized decrease in net worth?

A)Dividend income

B)Change in value of land

C)Decrease in value of boat

D)Personal expenditures

E)Salary

A)Dividend income

B)Change in value of land

C)Decrease in value of boat

D)Personal expenditures

E)Salary

D

3

Personal financial statements predominately use historical cost information.

False

4

For a statement of financial condition,the figure that will usually be most important is the total asset amount.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following would not be a reasonable suggestion for reviewing the Statement of Financial Condition?

A)Determine unrealized increases in net worth.

B)Determine the personal net worth amount.

C)Determine the amounts of the assets that are very liquid.

D)Determine the due period of liabilities.

E)Compare specific assets and specific liabilities,indicating net investment in assets.

A)Determine unrealized increases in net worth.

B)Determine the personal net worth amount.

C)Determine the amounts of the assets that are very liquid.

D)Determine the due period of liabilities.

E)Compare specific assets and specific liabilities,indicating net investment in assets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

For personal financial statements,the statement of changes in net worth replaces the income statement.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following would not be a source of information for personal financial statements?

A)Broker's statements

B)Income tax returns

C)Safe deposit box

D)Checkbook

E)All of the answers would be a source of information.

A)Broker's statements

B)Income tax returns

C)Safe deposit box

D)Checkbook

E)All of the answers would be a source of information.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

Personal financial statements are financial statements of individuals,husband and wife,or a larger family group.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

The principal of fiduciary funds may be distributed.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is not an example of a not-for-profit institution?

A)University

B)Hospital

C)State government

D)Church

E)Nnone of the answers are correct.

A)University

B)Hospital

C)State government

D)Church

E)Nnone of the answers are correct.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

For personal financial statements,the statement of financial condition is similar to a balance sheet.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

Cash receipts and disbursements,of governmental agencies,related to the payment of interest and principal on long-term debt describe which of the following?

A)Appropriations

B)Debt service

C)Capital projects

D)General fund

E)Proprietary funds

A)Appropriations

B)Debt service

C)Capital projects

D)General fund

E)Proprietary funds

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

In accounting for governments,which of the following provides necessary resources and the authority for their disbursements?

A)General fund

B)Encumbrances

C)Internal services

D)Appropriations

E)Special assessments

A)General fund

B)Encumbrances

C)Internal services

D)Appropriations

E)Special assessments

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

The accounting for a nonprofit institution does not include a single entity concept or efficiency.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

Under GASB Statement No.34,which of the following is not a minimum requirement for general purpose external financial statements-state and local governments?

A)Management's Discussion and Analysis

B)government-wide financial statements

C)fund financial statements

D)notes to the financial statements

E)cash projected financial statements

A)Management's Discussion and Analysis

B)government-wide financial statements

C)fund financial statements

D)notes to the financial statements

E)cash projected financial statements

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following would not likely be a reason for preparing personal financial statements?

A)Obtaining personal credit

B)Determining the tax basis of marketable securities

C)Income tax planning

D)Retirement planning

E)Estate planning

A)Obtaining personal credit

B)Determining the tax basis of marketable securities

C)Income tax planning

D)Retirement planning

E)Estate planning

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

The statement of changes in net worth is presented in terms of realized increases (decreases)and unrealized increases (decreases).

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Government-wide financial statements help users do all but which of the following?

A)Relate cash receipts and disbursements to the acquisition of long-lived assets.

B)Assess the finances of the government in its entirety,including the year's operating results.

C)Determine whether the government's overall financial position improved or deteriorated.

D)Evaluate whether the government's current-year revenues were sufficient to pay for current-year services.

E)Make better comparisons between governments.

A)Relate cash receipts and disbursements to the acquisition of long-lived assets.

B)Assess the finances of the government in its entirety,including the year's operating results.

C)Determine whether the government's overall financial position improved or deteriorated.

D)Evaluate whether the government's current-year revenues were sufficient to pay for current-year services.

E)Make better comparisons between governments.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

The basic statement prepared for personal financial statements is the statement of changes in net worth.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

For a statement of changes in net worth,which of the following would be an unrealized decrease in net worth?

A)Decrease in value of furnishings

B)Salary

C)Income taxes

D)Increase in value of land

E)Interest income

A)Decrease in value of furnishings

B)Salary

C)Income taxes

D)Increase in value of land

E)Interest income

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Under GASB Statement No.34,a government entity will not continue to present fund statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

For Howard and Joyce,the changes in net worth for the year ended December 31,2012,are detailed as follows.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2010.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2010.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

The Governmental Accounting Standards Board is a branch of the Financial Accounting Foundation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

The financial data of the component units are included with the government entities reporting entity because of the significance of their operational or financial relationships with the government entity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

State and local governments serve as a steward over public funds.This stewardship responsibility dominates the accounting for state and local governments.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

Under GASB Statement No.34,the notes to the financial statements must include budgetary information that includes the original budget and revised budgets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

Under GASB Statement No.34,the basic financial statements are to be preceded by the management's discussion and analysis (MD&A).

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

Nonprofit institutions,other than governments,use forms of financial reporting that vary from the fund type of system to a commercial type of reporting.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

The budget for a state or local government is merely a plan of future revenues and expenses.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

For Bill and Linda,the changes in net worth for the year ended December 31,2012,are detailed as follows.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2012.

Required:

Prepare a statement of changes in net worth for the year ended December 31,2012.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

GASB Statement No.34 makes it clear that government-wide statements are considered superior to fund statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

For the government-wide statements,governmental activities are to be presented separately from the financial statements of business-type activities.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

GASB Statement No.34 calls for financial statements integrated with government-wide reporting and enhanced fund reporting.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

In general,SFAS No.116 directs that contributions received by not-for-profit organizations are recognized as revenues in the period received at their fair value.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

The rating for an industrial revenue bond represents the probability of default by the governmental unit.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

The statement of changes in net worth is required when presenting personal financial statements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Some government and not-for-profit organizations have added budgeting by objectives and/or measures of productivity to their financial reporting.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

The GASB has a seven-member board.A simple majority of four is needed to issue a pronouncement.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Under governmental accounting,a fund is defined as a fiscal and accounting entity with a self-balancing set of accounts.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

Personal financial statements present assets at their historical cost.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Intention is to maintain the fund's assets through cost reimbursement by users or partial cost recovery from users and periodic infusion of additional assets.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Intention is to maintain the fund's assets through cost reimbursement by users or partial cost recovery from users and periodic infusion of additional assets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Operations that are similar to private businesses where service users are charged fees.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Operations that are similar to private businesses where service users are charged fees.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Future commitments for expenditure.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Future commitments for expenditure.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

The principal of these funds must remain intact.Typically,revenues earned may be distributed.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

The principal of these funds must remain intact.Typically,revenues earned may be distributed.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

All cash receipts and disbursements not required to be accounted for in another fund.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

All cash receipts and disbursements not required to be accounted for in another fund.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Service centers that supply goods or services to other governmental units on a cost reimbursement basis.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Service centers that supply goods or services to other governmental units on a cost reimbursement basis.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to the acquisition of long-lived assets.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to the acquisition of long-lived assets.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to improvements or services for which special property assessments have been levied.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to improvements or services for which special property assessments have been levied.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to the payment of interest and principal on long-term debt.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Cash receipts and disbursements related to the payment of interest and principal on long-term debt.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Match the definitions to the terms.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Provide necessary resources and the authority for their disbursements.

a.Appropriations

b.Debt service

c.Capital projects

d.Special assessments

e.Internal services

f.Enterprises

g.Proprietary funds

h.General fund

i.Fiduciary funds

j.Encumbrances

Provide necessary resources and the authority for their disbursements.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.