Deck 11: Worldwide Accounting Diversity and International Accounting Standards

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

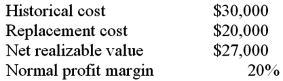

The following information pertains to inventory held by a company at December 31, 2011.  What is the amount of inventory loss shown on the income statement under IFRS?

What is the amount of inventory loss shown on the income statement under IFRS?

A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $6,000.

What is the amount of inventory loss shown on the income statement under IFRS?A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $6,000.

Question

The following information pertains to inventory held by a company at December 31, 2011.  What is the amount of inventory loss shown on the income statement under U.S. GAAP?

What is the amount of inventory loss shown on the income statement under U.S. GAAP?

A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $8,200.

What is the amount of inventory loss shown on the income statement under U.S. GAAP?A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $8,200.

Question

The following information pertains to inventory held by a company on December 31, 2011.  As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

A) U.S. GAAP income is $3,000 higher.

B) U.S. GAAP income is $10,000 lower.

C) IFRS income is $8,400 higher.

D) IFRS income is $3,000 lower.

E) IFRS income is $5,400 higher.

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?A) U.S. GAAP income is $3,000 higher.

B) U.S. GAAP income is $10,000 lower.

C) IFRS income is $8,400 higher.

D) IFRS income is $3,000 lower.

E) IFRS income is $5,400 higher.

Question

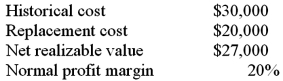

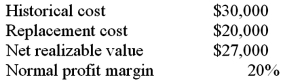

The following information pertains to inventory held by a company on December 31, 2011.  What amount of inventory should be reported under IFRS?

What amount of inventory should be reported under IFRS?

A) $25,000.

B) $27,000.

C) $30,000.

D) $5,000.

E) $2,000.

What amount of inventory should be reported under IFRS?A) $25,000.

B) $27,000.

C) $30,000.

D) $5,000.

E) $2,000.

Question

Question

Question

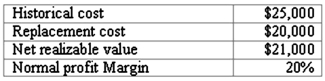

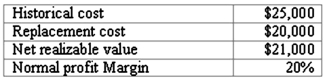

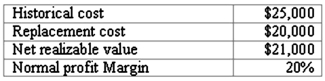

The following information pertains to inventory held by a company at December 31, 2011.  What amount of inventory should be reported under IFRS?

What amount of inventory should be reported under IFRS?

A) $25,000

B) $21,000

C) $20,000

D) $4,000

E) $5,000

What amount of inventory should be reported under IFRS?A) $25,000

B) $21,000

C) $20,000

D) $4,000

E) $5,000

Question

Question

The following information pertains to inventory held by a company on December 31, 2011.  What is the amount of inventory loss shown on the income statement under U.S. GAAP?

What is the amount of inventory loss shown on the income statement under U.S. GAAP?

A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

What is the amount of inventory loss shown on the income statement under U.S. GAAP?A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

Question

Question

Question

Question

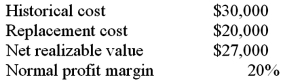

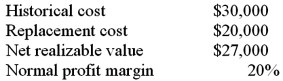

The following information pertains to inventory held by a company on December 31, 2011.  What amount of inventory should be reported under U.S. GAAP?

What amount of inventory should be reported under U.S. GAAP?

A) $16,000.

B) $27,000.

C) $30,000.

D) $21,600.

E) $20,000.

What amount of inventory should be reported under U.S. GAAP?A) $16,000.

B) $27,000.

C) $30,000.

D) $21,600.

E) $20,000.

Question

Question

Question

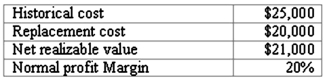

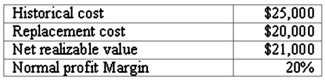

The following information pertains to inventory held by a company at December 31, 2011.  What amount of inventory should be reported under U.S. GAAP?

What amount of inventory should be reported under U.S. GAAP?

A) $25,000.

B) $21,000.

C) $20,000.

D) $16,800.

E) $16,000.

What amount of inventory should be reported under U.S. GAAP?A) $25,000.

B) $21,000.

C) $20,000.

D) $16,800.

E) $16,000.

Question

The following information pertains to inventory held by a company on December 31, 2011.  What is the amount of inventory loss shown on the income statement under IFRS?

What is the amount of inventory loss shown on the income statement under IFRS?

A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

What is the amount of inventory loss shown on the income statement under IFRS?A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

Question

Question

Question

The following information pertains to inventory held by a company at December 31, 2011.  As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

A) U.S. GAAP income is $1,000 higher.

B) U.S. GAAP income is $2,000 lower.

C) IFRS income is $1,000 higher.

D) IFRS income is $1,000 lower.

E) IFRS income is $5,000 higher.

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?A) U.S. GAAP income is $1,000 higher.

B) U.S. GAAP income is $2,000 lower.

C) IFRS income is $1,000 higher.

D) IFRS income is $1,000 lower.

E) IFRS income is $5,000 higher.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/60

Play

Full screen (f)

Deck 11: Worldwide Accounting Diversity and International Accounting Standards

1

Which of the following is not true about IFRS?

A) The IASB does not have the ability to enforce proper usage of IFRS.

B) IFRS is available to any organization or nation that wishes to use those standards.

C) IFRS is a comprehensive set of financial reporting standards.

D) IFRS includes only pronouncements issued by the IASB.

E) IFRS are considered as generally accepted accounting principles.

A) The IASB does not have the ability to enforce proper usage of IFRS.

B) IFRS is available to any organization or nation that wishes to use those standards.

C) IFRS is a comprehensive set of financial reporting standards.

D) IFRS includes only pronouncements issued by the IASB.

E) IFRS are considered as generally accepted accounting principles.

D

2

Which of the following is not a factor influencing a country's financial reporting practices?

A) Providers of financing.

B) Inflation.

C) Legal system.

D) Gross National Product.

E) Political and economic ties.

A) Providers of financing.

B) Inflation.

C) Legal system.

D) Gross National Product.

E) Political and economic ties.

D

3

In countries where there is less pressure for public accountability and information disclosure:

A) information needs can be satisfied by requesting information from internal company sources.

B) public offerings of stock shares are the primary source of financing for companies.

C) accounting information is prepared to meet the needs of taxing authorities.

D) accounting standards emphasize accounting for high inflation situations.

E) the accounting focus is on recent market economy reforms.

A) information needs can be satisfied by requesting information from internal company sources.

B) public offerings of stock shares are the primary source of financing for companies.

C) accounting information is prepared to meet the needs of taxing authorities.

D) accounting standards emphasize accounting for high inflation situations.

E) the accounting focus is on recent market economy reforms.

A

4

In the United States, foreign companies filing annual reports with the SEC that are not prepared in accordance with U.S. GAAP must:

A) present financial statements that comply with international GAAP.

B) conform with U.S. GAAP or present a reconciliation to U.S. GAAP.

C) have a demonstrated need for capital to be used for operations in the U.S.

D) use the U.S. dollar as their reporting currency.

E) use IFRS, or use foreign GAAP and provide a reconciliation to U.S. GAAP.

A) present financial statements that comply with international GAAP.

B) conform with U.S. GAAP or present a reconciliation to U.S. GAAP.

C) have a demonstrated need for capital to be used for operations in the U.S.

D) use the U.S. dollar as their reporting currency.

E) use IFRS, or use foreign GAAP and provide a reconciliation to U.S. GAAP.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

5

Foreign companies whose stock is listed on a U.S. stock exchange and using foreign GAAP other than IFRS must file their annual report with the SEC on:

A) Form 8-A.

B) Form 10-A.

C) Form 16-K.

D) Form 20-F.

E) Form 20-K.

A) Form 8-A.

B) Form 10-A.

C) Form 16-K.

D) Form 20-F.

E) Form 20-K.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is not a problem caused by diverse accounting practices across countries?

A) Preparation of consolidated financial statements.

B) Gaining access to foreign capital markets.

C) Lack of comparability of financial statements between companies in the same country.

D) Cost and expertise required of consolidations accounting staff.

E) Need for a company to maintain multiple sets of accounting records.

A) Preparation of consolidated financial statements.

B) Gaining access to foreign capital markets.

C) Lack of comparability of financial statements between companies in the same country.

D) Cost and expertise required of consolidations accounting staff.

E) Need for a company to maintain multiple sets of accounting records.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements is false regarding a country's legal system?

A) The two major types of legal systems are common law and codified Roman law.

B) Common law originated in the Roman jus civile.

C) Code law countries tend to have more statutes governing a wider range of human activity.

D) Accounting law is rather general in code law countries.

E) A nongovernmental organization is more likely to develop in a common law country than in a code law country.

A) The two major types of legal systems are common law and codified Roman law.

B) Common law originated in the Roman jus civile.

C) Code law countries tend to have more statutes governing a wider range of human activity.

D) Accounting law is rather general in code law countries.

E) A nongovernmental organization is more likely to develop in a common law country than in a code law country.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is not an IFRS pronouncement originally issued by the IASB?

A) Business Combinations.

B) First-Time Adoption of IFRS.

C) Financial Instruments: Disclosures.

D) Agriculture.

E) Operating Segments.

A) Business Combinations.

B) First-Time Adoption of IFRS.

C) Financial Instruments: Disclosures.

D) Agriculture.

E) Operating Segments.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

9

Convergence of accounting standards would not occur by:

A) FASB adopting an existing IASB standard.

B) IASB adopting an existing FASB standard.

C) IASB issuing a new standard.

D) IASB and FASB jointly developing a new standard.

E) IASB and FASB each issuing a similar but not identical standard.

A) FASB adopting an existing IASB standard.

B) IASB adopting an existing FASB standard.

C) IASB issuing a new standard.

D) IASB and FASB jointly developing a new standard.

E) IASB and FASB each issuing a similar but not identical standard.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

10

A U.S. company has many foreign subsidiaries and wants to convert its consolidated financial statements from U.S. GAAP to IFRS. Which of the following items is not one of the likely accounting issues to resolve for the opening IFRS balance sheet?

A) Measuring asset impairment.

B) Classifying extraordinary items.

C) Sale and leaseback gain recognition.

D) Measuring salaries expense.

E) Prior service cost recognition for pension amendments.

A) Measuring asset impairment.

B) Classifying extraordinary items.

C) Sale and leaseback gain recognition.

D) Measuring salaries expense.

E) Prior service cost recognition for pension amendments.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is not a way for a country to use IFRS?

A) Require foreign companies listed on that country's stock exchange to use IFRS for consolidated financial statements.

B) Allow foreign companies listed on that country's stock exchange to use IFRS.

C) Allow that country's companies listed on its stock exchange to use IFRS.

D) Adopt IFRS as that country's national GAAP.

E) All of the above are ways a country can use IFRS.

A) Require foreign companies listed on that country's stock exchange to use IFRS for consolidated financial statements.

B) Allow foreign companies listed on that country's stock exchange to use IFRS.

C) Allow that country's companies listed on its stock exchange to use IFRS.

D) Adopt IFRS as that country's national GAAP.

E) All of the above are ways a country can use IFRS.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

12

The types of differences that exist between IFRS and U.S. GAAP would not generally include:

A) Presentation differences.

B) Measurement differences.

C) Disclosure differences.

D) Comparability differences.

E) Recognition differences.

A) Presentation differences.

B) Measurement differences.

C) Disclosure differences.

D) Comparability differences.

E) Recognition differences.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

13

What international organization currently promulgates IFRS?

A) IASB.

B) IASC.

C) IOSCO.

D) FASB.

E) EU.

A) IASB.

B) IASC.

C) IOSCO.

D) FASB.

E) EU.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

14

The IASB and FASB are working on several joint projects. Which of the following is not a topic of the Revenue Recognition Project?

A) Eliminate inconsistencies in existing literature.

B) Cash flow presentation of revenue.

C) Business models issues for revenue recognition.

D) Conceptual basis as framework for future issues of revenue recognition.

E) Contract-based revenue recognition.

A) Eliminate inconsistencies in existing literature.

B) Cash flow presentation of revenue.

C) Business models issues for revenue recognition.

D) Conceptual basis as framework for future issues of revenue recognition.

E) Contract-based revenue recognition.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

15

In countries of Latin America:

A) accounting practice is designed to provide adequate information to investors and creditors.

B) accounting standards emphasize accounting for high inflation situations.

C) banks are the primary source of financing for companies.

D) accounting focuses are based recent market economy reforms.

E) accounting information is prepared to meet the needs of governmental planners.

A) accounting practice is designed to provide adequate information to investors and creditors.

B) accounting standards emphasize accounting for high inflation situations.

C) banks are the primary source of financing for companies.

D) accounting focuses are based recent market economy reforms.

E) accounting information is prepared to meet the needs of governmental planners.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements is false regarding providers of financing?

A) There is less pressure to provide accounting information in those countries in which financing is primarily by banks.

B) In countries where capital stock is the primary source of financing, accounting emphasizes the income statement.

C) Disclosures are less extensive in those countries financed primarily by stock.

D) Bankers tend to focus more on solvency and stockholders focus more on profitability.

E) As companies become more dependent on financing by stock, more information is demanded.

A) There is less pressure to provide accounting information in those countries in which financing is primarily by banks.

B) In countries where capital stock is the primary source of financing, accounting emphasizes the income statement.

C) Disclosures are less extensive in those countries financed primarily by stock.

D) Bankers tend to focus more on solvency and stockholders focus more on profitability.

E) As companies become more dependent on financing by stock, more information is demanded.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

17

A U.S. company has many foreign subsidiaries and wants to convert its consolidated financial statements from U.S. GAAP to IFRS. Which of the following items is not one of the likely accounting issues to resolve for the opening IFRS balance sheet?

A) Inventory valuation.

B) Capitalizing development costs.

C) Classifying deferred taxes as current or noncurrent.

D) Acquisition value for a subsidiary.

E) Liability for restructuring charges.

A) Inventory valuation.

B) Capitalizing development costs.

C) Classifying deferred taxes as current or noncurrent.

D) Acquisition value for a subsidiary.

E) Liability for restructuring charges.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following are not key FASB initiatives to further converge IFRS and U.S. GAAP?

A) Short-term convergence projects.

B) Joint projects sharing FASB and IASB staff resources.

C) Having the IASB Chairman in-residence at the FASB office.

D) Monitoring ongoing IASB projects.

E) Researching differences between U.S. GAAP and IFRS.

A) Short-term convergence projects.

B) Joint projects sharing FASB and IASB staff resources.

C) Having the IASB Chairman in-residence at the FASB office.

D) Monitoring ongoing IASB projects.

E) Researching differences between U.S. GAAP and IFRS.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

19

Which one of the following is not a background requirement for any IASB members?

A) Audit.

B) Tax.

C) Financial statement preparation.

D) Academia.

E) Financial statement user.

A) Audit.

B) Tax.

C) Financial statement preparation.

D) Academia.

E) Financial statement user.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following are not authoritative pronouncements of International Financial Reporting Standards (IFRSs)? 1) International Financial Reporting Standards issued by the IASB

2) International Accounting Standards issued by the IASC and adopted by the IASB

3) Interpretations originated by the International Financial Reporting Interpretations Committee (IFRIC)

4) U.S. Generally Accepted Accounting Principles

A) 4 only.

B) 3 and 4.

C) 1, 3, and 4.

D) 2, 3, and 4.

E) 1, 2, 3, and 4.

2) International Accounting Standards issued by the IASC and adopted by the IASB

3) Interpretations originated by the International Financial Reporting Interpretations Committee (IFRIC)

4) U.S. Generally Accepted Accounting Principles

A) 4 only.

B) 3 and 4.

C) 1, 3, and 4.

D) 2, 3, and 4.

E) 1, 2, 3, and 4.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

21

The following information pertains to inventory held by a company at December 31, 2011. What is the amount of inventory loss shown on the income statement under IFRS?

A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $6,000.

What is the amount of inventory loss shown on the income statement under IFRS?A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $6,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

22

The following information pertains to inventory held by a company at December 31, 2011. What is the amount of inventory loss shown on the income statement under U.S. GAAP?

A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $8,200.

What is the amount of inventory loss shown on the income statement under U.S. GAAP?A) $1,000.

B) $2,000.

C) $4,000.

D) $5,000.

E) $8,200.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

23

The following information pertains to inventory held by a company on December 31, 2011. As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

A) U.S. GAAP income is $3,000 higher.

B) U.S. GAAP income is $10,000 lower.

C) IFRS income is $8,400 higher.

D) IFRS income is $3,000 lower.

E) IFRS income is $5,400 higher.

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?A) U.S. GAAP income is $3,000 higher.

B) U.S. GAAP income is $10,000 lower.

C) IFRS income is $8,400 higher.

D) IFRS income is $3,000 lower.

E) IFRS income is $5,400 higher.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

24

The following information pertains to inventory held by a company on December 31, 2011. What amount of inventory should be reported under IFRS?

A) $25,000.

B) $27,000.

C) $30,000.

D) $5,000.

E) $2,000.

What amount of inventory should be reported under IFRS?A) $25,000.

B) $27,000.

C) $30,000.

D) $5,000.

E) $2,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

25

A company acquired a new piece of equipment on January 1, 2009 at a cost of $200,000. The equipment is expected to have a useful life of 10 years, a residual value of $20,000 and is depreciated on a straight-line basis. On January 1, 2011, the equipment was appraised and determined to have a fair value of $190,000 and a residual value of $25,000 and a remaining useful life of 10 years. At what amount should the equipment be reported on the December 31, 2011 balance sheet under U.S. GAAP?

A) $160,000

B) $150,000

C) $146,000

D) $140,000

E) $116,000

A) $160,000

B) $150,000

C) $146,000

D) $140,000

E) $116,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

26

The IASB and FASB are working on several joint projects. What is the purpose of the Revenue Recognition Project?

A) to provide guidance on the application of the acquisition method.

B) to enhance the usefulness of information in assessing the financial performance of the reporting enterprise

C) to develop a common comprehensive standard on revenue recognition.

D) to develop a common conceptual framework that both boards can use as a basis for future standard-setting.

E) to agree upon financial statement titles that will have no differentiation after translation to various languages.

A) to provide guidance on the application of the acquisition method.

B) to enhance the usefulness of information in assessing the financial performance of the reporting enterprise

C) to develop a common comprehensive standard on revenue recognition.

D) to develop a common conceptual framework that both boards can use as a basis for future standard-setting.

E) to agree upon financial statement titles that will have no differentiation after translation to various languages.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

27

The following information pertains to inventory held by a company at December 31, 2011. What amount of inventory should be reported under IFRS?

A) $25,000

B) $21,000

C) $20,000

D) $4,000

E) $5,000

What amount of inventory should be reported under IFRS?A) $25,000

B) $21,000

C) $20,000

D) $4,000

E) $5,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

28

A company sells a building to a bank in 2011 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally purchased for $200,000 and currently had a book value of $50,000 at the date of the sale. What amount should be recognized in 2011 as a gain on the sale using U.S. GAAP?

A) $20,000.

B) $50,000.

C) $100,000.

D) $150,000.

E) $200,000.

A) $20,000.

B) $50,000.

C) $100,000.

D) $150,000.

E) $200,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

29

The following information pertains to inventory held by a company on December 31, 2011. What is the amount of inventory loss shown on the income statement under U.S. GAAP?

A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

What is the amount of inventory loss shown on the income statement under U.S. GAAP?A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

30

A company incurs research and development costs of $200,000 in 2011 of which $50,000 of these costs relate to development activities because certain criteria have been met which suggest that an intangible asset has been created. What amount should be recognized as research and development expense in 2011 using U.S. GAAP?

A) $50,000.

B) $150,000.

C) $200,000.

D) $0.

E) $250,000.

A) $50,000.

B) $150,000.

C) $200,000.

D) $0.

E) $250,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

31

Which topic was not covered by FASB under the short-term convergence project?

A) Inventory costs.

B) Asset exchanges.

C) Liability transfers.

D) Accounting changes.

E) Earnings-per-share.

A) Inventory costs.

B) Asset exchanges.

C) Liability transfers.

D) Accounting changes.

E) Earnings-per-share.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

32

A company incurs research and development costs of $200,000 in 2011 of which $50,000 of these costs relate to development activities because certain criteria have been met which suggest that an intangible asset has been created. What amount should be recognized as research and development expense in 2011 using IFRS?

A) $50,000.

B) $150,000.

C) $200,000.

D) $0.

E) $250,000.

A) $50,000.

B) $150,000.

C) $200,000.

D) $0.

E) $250,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

33

The following information pertains to inventory held by a company on December 31, 2011. What amount of inventory should be reported under U.S. GAAP?

A) $16,000.

B) $27,000.

C) $30,000.

D) $21,600.

E) $20,000.

What amount of inventory should be reported under U.S. GAAP?A) $16,000.

B) $27,000.

C) $30,000.

D) $21,600.

E) $20,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

34

A company incurs research and development costs of $200,000 in 2011 of which $50,000 of these costs relate to development activities because certain criteria have been met which suggest that an intangible asset has been created. As a result of research and development costs, what is the difference in income between reporting using U.S. GAAP and IFRS in 2011?

A) U.S. GAAP income is $50,000 higher.

B) U.S. GAAP income is $50,000 lower.

C) IFRS income is $50,000 lower.

D) IFRS income is $150,000 lower.

E) IFRS income is $150,000 higher.

A) U.S. GAAP income is $50,000 higher.

B) U.S. GAAP income is $50,000 lower.

C) IFRS income is $50,000 lower.

D) IFRS income is $150,000 lower.

E) IFRS income is $150,000 higher.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

35

A company acquired a new piece of equipment on January 1, 2009 at a cost of $200,000. The equipment is expected to have a useful life of 10 years, a residual value of $20,000 and is depreciated on a straight-line basis. On January 1, 2011, the equipment was appraised and determined to have a fair value of $190,000 and a residual value of $25,000 and a remaining useful life of 10 years. At what amount should the equipment be reported on the December 31, 2011 balance sheet under the IFRS revaluation model?

A) $190,000

B) $173,500

C) $165,000

D) $136,000

E) $110,000

A) $190,000

B) $173,500

C) $165,000

D) $136,000

E) $110,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

36

The following information pertains to inventory held by a company at December 31, 2011. What amount of inventory should be reported under U.S. GAAP?

A) $25,000.

B) $21,000.

C) $20,000.

D) $16,800.

E) $16,000.

What amount of inventory should be reported under U.S. GAAP?A) $25,000.

B) $21,000.

C) $20,000.

D) $16,800.

E) $16,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

37

The following information pertains to inventory held by a company on December 31, 2011. What is the amount of inventory loss shown on the income statement under IFRS?

A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

What is the amount of inventory loss shown on the income statement under IFRS?A) $0.

B) $3,000.

C) $14,000.

D) $10,000.

E) $8,400.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

38

A company acquired a new piece of equipment on January 1, 2009 at a cost of $200,000. The equipment is expected to have a useful life of 10 years, a residual value of $20,000 and is depreciated on a straight-line basis. On January 1, 2011, the equipment was appraised and determined to have a fair value of $190,000 and a residual value of $25,000 and a remaining useful life of 10 years. At what amount should the equipment be reported on the December 31, 2011 balance sheet under the IFRS cost model?

A) $160,000

B) $150,000

C) $146,000

D) $140,000

E) $116,000

A) $160,000

B) $150,000

C) $146,000

D) $140,000

E) $116,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

39

The IASB and FASB are working on several joint projects. What is the purpose of the Financial Statement Presentation Project?

A) to provide guidance on the application of the acquisition method.

B) to enhance the usefulness of information in assessing the financial performance of the reporting enterprise.

C) to develop a common comprehensive standard on revenue recognition.

D) to develop a common conceptual framework that both boards can use as a basis for future standard-setting.

E) to agree upon financial statement titles that will have no differentiation after translation to various languages.

A) to provide guidance on the application of the acquisition method.

B) to enhance the usefulness of information in assessing the financial performance of the reporting enterprise.

C) to develop a common comprehensive standard on revenue recognition.

D) to develop a common conceptual framework that both boards can use as a basis for future standard-setting.

E) to agree upon financial statement titles that will have no differentiation after translation to various languages.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

40

The following information pertains to inventory held by a company at December 31, 2011. As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?

A) U.S. GAAP income is $1,000 higher.

B) U.S. GAAP income is $2,000 lower.

C) IFRS income is $1,000 higher.

D) IFRS income is $1,000 lower.

E) IFRS income is $5,000 higher.

As a result of inventory loss, what is the difference in income between reporting using U.S. GAAP and IFRS?A) U.S. GAAP income is $1,000 higher.

B) U.S. GAAP income is $2,000 lower.

C) IFRS income is $1,000 higher.

D) IFRS income is $1,000 lower.

E) IFRS income is $5,000 higher.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

41

Which two EU directives have helped harmonize accounting standards?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

42

What accounting topics were covered under the FASB short-term convergence project?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

43

A company sells a building to a bank in 2011 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally purchased for $200,000 and currently had a book value of $50,000 at the date of the sale. What amount should be recognized as a gain in 2011 using IFRS?

A) $20,000.

B) $50,000.

C) $100,000.

D) $150,000.

E) $200,000.

A) $20,000.

B) $50,000.

C) $100,000.

D) $150,000.

E) $200,000.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

44

What are the six key FASB initiatives to further convergence?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

45

Principal Company is a U.S.-based company that prepares its consolidated financial statements in accordance with U.S. GAAP. Principal reported net income of $2,600,000 in 2011 and stockholders' equity of $12,000,000 at December 31, 2011. Principal wants to determine the reporting impact of switching to IFRS. The following three items would create differences in financial reporting:

1) At December 31, 2011, inventory had a historical cost of $850,000, a replacement cost of $700,000, and a net realizable value of $800,000. The normal profit margin was 10%.

2) Principal acquired a building at the beginning of 2009 at a cost of $5,000,000. The building has an estimated useful life of 20 years, an estimated residual value of $1,000,000, and is being depreciated on a straight-line basis. On January 1, 2011, the building has a fair value of $5,500,000. There is no change in the estimated useful life or residual value. In a switch to IFRS, Principal would use the revaluation model in IAS 16 to determine the carrying value of property, plant, and equipment subsequent to acquisition.

3) In 2011, Principal incurred $800,000 of research and development for a new product, of which 35% relates to development activities subsequent to the point at which criteria indicating the creation of an intangible asset had been met. As of the end of 2011, development of the new product had not been completed.

Required:

1) Prepare a schedule reconciling net income under U.S. GAAP to net income under IFRS for the year ended December 31, 2011.

2) Prepare a schedule reconciling stockholders' equity under U.S. GAAP to

1) At December 31, 2011, inventory had a historical cost of $850,000, a replacement cost of $700,000, and a net realizable value of $800,000. The normal profit margin was 10%.

2) Principal acquired a building at the beginning of 2009 at a cost of $5,000,000. The building has an estimated useful life of 20 years, an estimated residual value of $1,000,000, and is being depreciated on a straight-line basis. On January 1, 2011, the building has a fair value of $5,500,000. There is no change in the estimated useful life or residual value. In a switch to IFRS, Principal would use the revaluation model in IAS 16 to determine the carrying value of property, plant, and equipment subsequent to acquisition.

3) In 2011, Principal incurred $800,000 of research and development for a new product, of which 35% relates to development activities subsequent to the point at which criteria indicating the creation of an intangible asset had been met. As of the end of 2011, development of the new product had not been completed.

Required:

1) Prepare a schedule reconciling net income under U.S. GAAP to net income under IFRS for the year ended December 31, 2011.

2) Prepare a schedule reconciling stockholders' equity under U.S. GAAP to

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

46

The major providers of financing in some countries are stockholders, while other countries predominantly use banks as the main financing source. What difference does it make to accounting disclosures in comparing a company from one of each of those countries?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

47

A company sells a building to a bank in 2011 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally purchased for $200,000 and currently had a book value of $50,000 at the date of the sale.

Assume the seller of the building is a U.S. company that is preparing to convert from U.S. GAAP to IFRS. At December 31, 2012, with regard to the sale and leaseback accounting, what amount would reconcile stockholders' equity from U.S. GAAP to IFRS at December 31, 2012?

A.

Increase $40,000.

B.

Decrease $40,000.

C.

Decrease $60,000.

D.

Increase $60,000.

E.

No amount would be necessary for reconciliation.

Assume the seller of the building is a U.S. company that is preparing to convert from U.S. GAAP to IFRS. At December 31, 2012, with regard to the sale and leaseback accounting, what amount would reconcile stockholders' equity from U.S. GAAP to IFRS at December 31, 2012?

A.

Increase $40,000.

B.

Decrease $40,000.

C.

Decrease $60,000.

D.

Increase $60,000.

E.

No amount would be necessary for reconciliation.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

48

What problems are caused by diverse accounting practices?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

49

Why does each country have its own unique set of financial reporting practices?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

50

What were the major objectives of the Treaty of Rome?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

51

What are the four different ways IFRS can be used by a country?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

52

A company sells a building to a bank in 2011 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally purchased for $200,000 and currently had a book value of $50,000 at the date of the sale. As a result of the sale and leaseback transaction in 2011, what is the difference between income using U.S. GAAP and IFRS in 2011?

A) U.S. GAAP income is $80,000 higher.

B) U.S. GAAP income is $100,000 higher.

C) IFRS income is $50,000 lower.

D) IFRS income is $100,000 lower.

E) IFRS income is $80,000 higher.

A) U.S. GAAP income is $80,000 higher.

B) U.S. GAAP income is $100,000 higher.

C) IFRS income is $50,000 lower.

D) IFRS income is $100,000 lower.

E) IFRS income is $80,000 higher.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

53

What are measurement differences in international reporting and what would be an example of a difference?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

54

How did the early International Accounting Standards (IAS) obtain support from a sufficient number of board members?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

55

What are the two major types of legal systems used around the world?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

56

What are the three authoritative pronouncements that make up the International Financial Reporting Standards (IFRS)?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

57

What is meant by harmonization of accounting standards?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

58

What are recognition differences in international reporting and what would be an example of a difference?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

59

A company sells a building to a bank in 2011 at a gain of $100,000 and immediately leases the building back for period of five years. The lease is accounted for as an operating lease. The building was originally purchased for $200,000 and currently had a book value of $50,000 at the date of the sale. As a result of the sale and leaseback transaction in 2011, what is the difference between income using U.S. GAAP and IFRS in 2012?

A) $0.

B) U.S. GAAP income is $20,000 higher.

C) IFRS income is $80,000 lower.

D) IFRS income is $60,000 lower.

E) IFRS income is $80,000 higher.

A) $0.

B) U.S. GAAP income is $20,000 higher.

C) IFRS income is $80,000 lower.

D) IFRS income is $60,000 lower.

E) IFRS income is $80,000 higher.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

60

What is the IOSCO?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 60 flashcards in this deck.