Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726 Exercise 5

Rose Hospital

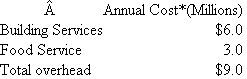

Rose Hospital has two service departments (building services and food service), and three patient care units (intensive care, surgery, and general medicine). Building Services provides janitorial, maintenance, and engineering services as well as space (utilities, depreciation, insurance, and taxes) to all departments and patient care units. Food Service provides meals to both patients and staff members. It operates a cafeteria and serves meals to patients in their rooms. Building services costs of $6 million are allocated based on square footage, and food service costs of $3 million are allocated based on number of meals served. The following two tables summarize the annual costs of the two service departments and the utilization of each service department by the other departments. *Before allocated service department costs

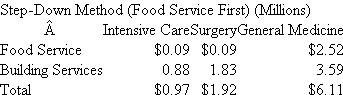

*Before allocated service department costs  The following table summarizes the allocation of service department costs using the step-down method with Food Service as the first service department to be allocated:

The following table summarizes the allocation of service department costs using the step-down method with Food Service as the first service department to be allocated:  Required:

Required:

(Round all allocation rates and all dollar amounts to two decimal places.)

a. Allocate the two service department costs to the three patient care units using the direct method of allocating service department costs.

b. Same as ( a ) except use the step-down allocation method with Building Services as the first service department allocated.

c. Write a short, nontechnical memo to management explaining why the sum of the two service department costs allocated to each patient care unit in ( b ) differs from the sum of the costs computed using the step-down method starting with Food Service.

Rose Hospital has two service departments (building services and food service), and three patient care units (intensive care, surgery, and general medicine). Building Services provides janitorial, maintenance, and engineering services as well as space (utilities, depreciation, insurance, and taxes) to all departments and patient care units. Food Service provides meals to both patients and staff members. It operates a cafeteria and serves meals to patients in their rooms. Building services costs of $6 million are allocated based on square footage, and food service costs of $3 million are allocated based on number of meals served. The following two tables summarize the annual costs of the two service departments and the utilization of each service department by the other departments.

*Before allocated service department costs The following table summarizes the allocation of service department costs using the step-down method with Food Service as the first service department to be allocated: Required: (Round all allocation rates and all dollar amounts to two decimal places.)

a. Allocate the two service department costs to the three patient care units using the direct method of allocating service department costs.

b. Same as ( a ) except use the step-down allocation method with Building Services as the first service department allocated.

c. Write a short, nontechnical memo to management explaining why the sum of the two service department costs allocated to each patient care unit in ( b ) differs from the sum of the costs computed using the step-down method starting with Food Service.

Explanation Verified

Verified

Direct Allocation Method:

Direct alloca...

Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255