Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726 Exercise 3

Houston Milling

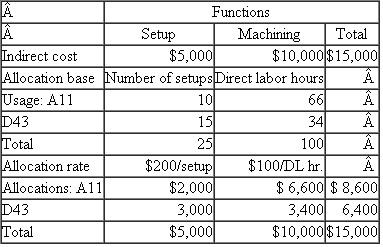

Houston Milling is a subcontractor to Pratt Whitney, which makes jet engines. Houston Milling makes two different fuel pump housings for two Pratt Whitney jet engines: the A11 housing and the D43. These pump housings are received from Pratt Whitney, which buys them from an outside (independent) foundry and ships them to Houston for precision machining. Houston performs two machining operations on the housings. These are performed in two separate machining departments (Department 1 and Department 2). Both housings, A11 and D43, require machining in both Departments 1 and 2. Before the parts are machined, the machines must first be set up, which includes cleaning the machine, checking the tools in the machine, adjusting the tolerances, and then finally machining some trial parts. Houston's current accounting system tracks the number of setups and direct labor hours used by each part. Table 1 summarizes the indirect costs of producing A11 and D43. (The direct costs such as direct labor and materials are ignored to simplify the computations.)

Setup and machine hours in the two departments are pooled into two cost pools: setup and machining. Table 1 allocates the costs in these two pools to the two products. Under this accounting system, A11 has indirect costs of $8,600 and D43 has indirect costs of $6,400. Management believes that the current accounting system is not producing accurate costs for the two products because the two cost pools are too aggregated. They decide to disaggregate the data and use four cost pools. They collect some additional data, which are summarized in Table 2.

Required:

a. Calculate revised cost allocations based on the disaggregated data in Table 2. Number of setups is used to allocate the indirect cost of setups in both Departments 1 and 2 and direct labor hours are used to allocate the machining costs in Departments 1 and 2.

b. Prepare a short memo describing the pros and cons of the revised allocated indirect costs in (a) compared to those in Table 1.

TABLE 1 Houston Milling Allocated Indirect Costs of Producing Parts A11 and D4 3 TABLE 2 Houston Milling Disaggregated Cost Pool Data

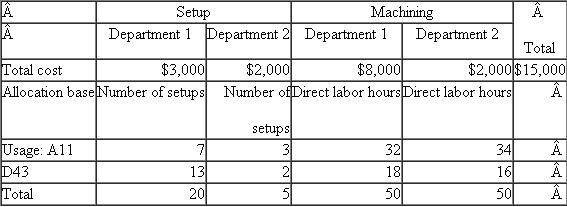

TABLE 2 Houston Milling Disaggregated Cost Pool Data  TABLE 3 Houston Milling Setup Hours and Machine Hours in Departments 1 an d 2

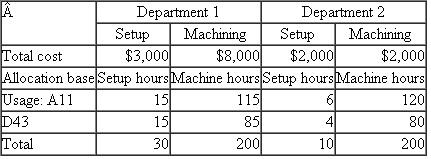

TABLE 3 Houston Milling Setup Hours and Machine Hours in Departments 1 an d 2  c. After completing the analysis in ( a ) and ( b ), some additional data are collected from a special study of setup hours and machine hours in the two departments. These data are presented in Table 3. In particular, setup hours and machine hours are collected in the two departments. Management now believes that setup hours and machine hours more accurately reflect the true cause-and-effect relations of setup costs and machining costs in Departments 1 and 2 than number of setups and direct labor hours, respectively.

c. After completing the analysis in ( a ) and ( b ), some additional data are collected from a special study of setup hours and machine hours in the two departments. These data are presented in Table 3. In particular, setup hours and machine hours are collected in the two departments. Management now believes that setup hours and machine hours more accurately reflect the true cause-and-effect relations of setup costs and machining costs in Departments 1 and 2 than number of setups and direct labor hours, respectively.

Based on the data presented in Table 3, calculate revised cost allocations for A11 and D43. Setup costs in Departments 1 and 2 are to be allocated based on setup hours, and machining costs in Departments 1 and 2 are to be allocated based on machine hours.

d. Compare the total product costs for A11 and D43 in Table 1 and parts (a) and (c). What conclusions can you draw?

P11-11: Sanchez Gadgets

Sanchez Gadgets purchases innovative home kitchen gadgets from around the world (such as a kitchen torch, a pasta maker, and an automatic salad spinner) and sells them to specialty cooking retail stores. Sanchez has a marketing department that locates and purchases the innovative gadgets and prepares price lists and catalogs for Sanchez's direct selling force. Sanchez's salespeople are assigned geographic sales territories and are responsible for all the specialty kitchen stores in their geographic territories.

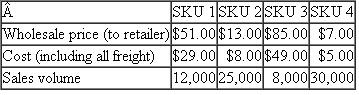

Management at Sanchez is concerned that with over 450 different items it is currently carrying too many different SKUs (SKUs are "stock keeping units"). Management is currently looking for a methodology to eliminate unprofitable SKUs. To focus on developing that methodology, assume that Sanchez has just four SKUs: SKU1, SKU2, SKU3, and SKU4. The following data summarize the current sales, selling prices, and cost (purchase price plus freight) for each SKU: Sanchez purchases items for sale and inventories them. The cost of inventorying each item (including the opportunity cost of financing the item) is 20 percent of the annual cost of the item. So if 100 units of a gadget are sold each year, and the cost of the item is $4, Sanchez's inventory holding cost is $80 (20% × 100 × $4).

Sanchez purchases items for sale and inventories them. The cost of inventorying each item (including the opportunity cost of financing the item) is 20 percent of the annual cost of the item. So if 100 units of a gadget are sold each year, and the cost of the item is $4, Sanchez's inventory holding cost is $80 (20% × 100 × $4).

The annual cost of the marketing department is $135,000. This amount consists of the salaries and fringe benefits of the employees who purchase the products and prepare the catalogs and price lists. Management determines that marketing department costs vary with the number of SKUs.

The annual cost of the direct sales force is $350,000. This amount consists of the salaries, fringe benefits, and travel expenses of the salespeople who call on the retail specialty kitchen stores to sell Sanchez gadgets. After extensive conversations with the salespeople, management believes that the salespeople spend their time in proportion to the sales volume of the gadgets. In other words, if a particular gadget accounts for 10 percent of Sanchez's total revenue, then the sales force spends about 10 percent of its time selling that item.

Required:

a. Design a reporting methodology that identifies possible SKUs that Sanchez should consider dropping from its product mix. Using your methodology, compute the profitability of each of the four SKUs.

b. Based on your analysis in part (a), which SKUs should Sanchez drop? Which ones should Sanchez retain?

c. Discuss the critical assumptions underlying your analysis in part (a).

Houston Milling is a subcontractor to Pratt Whitney, which makes jet engines. Houston Milling makes two different fuel pump housings for two Pratt Whitney jet engines: the A11 housing and the D43. These pump housings are received from Pratt Whitney, which buys them from an outside (independent) foundry and ships them to Houston for precision machining. Houston performs two machining operations on the housings. These are performed in two separate machining departments (Department 1 and Department 2). Both housings, A11 and D43, require machining in both Departments 1 and 2. Before the parts are machined, the machines must first be set up, which includes cleaning the machine, checking the tools in the machine, adjusting the tolerances, and then finally machining some trial parts. Houston's current accounting system tracks the number of setups and direct labor hours used by each part. Table 1 summarizes the indirect costs of producing A11 and D43. (The direct costs such as direct labor and materials are ignored to simplify the computations.)

Setup and machine hours in the two departments are pooled into two cost pools: setup and machining. Table 1 allocates the costs in these two pools to the two products. Under this accounting system, A11 has indirect costs of $8,600 and D43 has indirect costs of $6,400. Management believes that the current accounting system is not producing accurate costs for the two products because the two cost pools are too aggregated. They decide to disaggregate the data and use four cost pools. They collect some additional data, which are summarized in Table 2.

Required:

a. Calculate revised cost allocations based on the disaggregated data in Table 2. Number of setups is used to allocate the indirect cost of setups in both Departments 1 and 2 and direct labor hours are used to allocate the machining costs in Departments 1 and 2.

b. Prepare a short memo describing the pros and cons of the revised allocated indirect costs in (a) compared to those in Table 1.

TABLE 1 Houston Milling Allocated Indirect Costs of Producing Parts A11 and D4 3

TABLE 2 Houston Milling Disaggregated Cost Pool Data TABLE 3 Houston Milling Setup Hours and Machine Hours in Departments 1 an d 2 c. After completing the analysis in ( a ) and ( b ), some additional data are collected from a special study of setup hours and machine hours in the two departments. These data are presented in Table 3. In particular, setup hours and machine hours are collected in the two departments. Management now believes that setup hours and machine hours more accurately reflect the true cause-and-effect relations of setup costs and machining costs in Departments 1 and 2 than number of setups and direct labor hours, respectively.Based on the data presented in Table 3, calculate revised cost allocations for A11 and D43. Setup costs in Departments 1 and 2 are to be allocated based on setup hours, and machining costs in Departments 1 and 2 are to be allocated based on machine hours.

d. Compare the total product costs for A11 and D43 in Table 1 and parts (a) and (c). What conclusions can you draw?

P11-11: Sanchez Gadgets

Sanchez Gadgets purchases innovative home kitchen gadgets from around the world (such as a kitchen torch, a pasta maker, and an automatic salad spinner) and sells them to specialty cooking retail stores. Sanchez has a marketing department that locates and purchases the innovative gadgets and prepares price lists and catalogs for Sanchez's direct selling force. Sanchez's salespeople are assigned geographic sales territories and are responsible for all the specialty kitchen stores in their geographic territories.

Management at Sanchez is concerned that with over 450 different items it is currently carrying too many different SKUs (SKUs are "stock keeping units"). Management is currently looking for a methodology to eliminate unprofitable SKUs. To focus on developing that methodology, assume that Sanchez has just four SKUs: SKU1, SKU2, SKU3, and SKU4. The following data summarize the current sales, selling prices, and cost (purchase price plus freight) for each SKU:

Sanchez purchases items for sale and inventories them. The cost of inventorying each item (including the opportunity cost of financing the item) is 20 percent of the annual cost of the item. So if 100 units of a gadget are sold each year, and the cost of the item is $4, Sanchez's inventory holding cost is $80 (20% × 100 × $4).The annual cost of the marketing department is $135,000. This amount consists of the salaries and fringe benefits of the employees who purchase the products and prepare the catalogs and price lists. Management determines that marketing department costs vary with the number of SKUs.

The annual cost of the direct sales force is $350,000. This amount consists of the salaries, fringe benefits, and travel expenses of the salespeople who call on the retail specialty kitchen stores to sell Sanchez gadgets. After extensive conversations with the salespeople, management believes that the salespeople spend their time in proportion to the sales volume of the gadgets. In other words, if a particular gadget accounts for 10 percent of Sanchez's total revenue, then the sales force spends about 10 percent of its time selling that item.

Required:

a. Design a reporting methodology that identifies possible SKUs that Sanchez should consider dropping from its product mix. Using your methodology, compute the profitability of each of the four SKUs.

b. Based on your analysis in part (a), which SKUs should Sanchez drop? Which ones should Sanchez retain?

c. Discuss the critical assumptions underlying your analysis in part (a).

Explanation Verified

Verified

Activity-Based Costing (ABC)

Movement b...

Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255