Intermediate Microeconomics and Its Application 12th Edition by Walter Nicholson,Christopher Snyder

Edition 12ISBN: 978-1133189022Intermediate Microeconomics and Its Application 12th Edition by Walter Nicholson,Christopher Snyder

Edition 12ISBN: 978-1133189022 Exercise 32

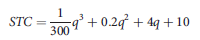

Suppose there are 100 identical firms in the perfectly competitive notecard industry. Each firm has a short-run total cost curve of the form:

and marginal cost is given by

a. Calculate the firm's short-run supply curve with q (the number of crates of notecards) as a function of market price (P).

b. Calculate the industry supply curve for the 100 firms in this industry.

c. Suppose market demand is given by Q =- 200P + 8,000. What will be the short run equilibrium price-quantity combination?

d. Suppose everyone starts writing more research papers and the new market demand is given by Q =- 200P + 11,200. What is the new short-run price-quantity equilibrium?

How much profit does each firm make?

and marginal cost is given by

a. Calculate the firm's short-run supply curve with q (the number of crates of notecards) as a function of market price (P).

b. Calculate the industry supply curve for the 100 firms in this industry.

c. Suppose market demand is given by Q =- 200P + 8,000. What will be the short run equilibrium price-quantity combination?

d. Suppose everyone starts writing more research papers and the new market demand is given by Q =- 200P + 11,200. What is the new short-run price-quantity equilibrium?

How much profit does each firm make?

Explanation Verified

Verified

a)For short run, supply curve condition ...

Intermediate Microeconomics and Its Application 12th Edition by Walter Nicholson,Christopher Snyder

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255