Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Edition 1ISBN: 978-0538736787Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Edition 1ISBN: 978-0538736787 Exercise 26

EXTERNAL LINKAGES, CUSTOMER COSTING, CUSTOMER PROFITABILITY

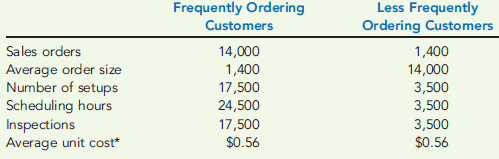

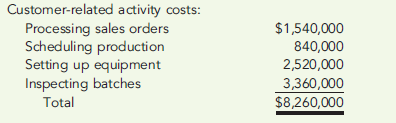

Carbon Company sells electrical components to medical equipment manufacturers for an average price of $1.05 per part. There are two types of customers: those who place small, frequent orders and those who place larger, less frequent orders. Each time an order is placed and processed, a setup is required. Scheduling is also needed to coordinate the many different orders that come in and place demands on the plant's manufacturing resources. Carbon also inspects a sample of the products each time a batch is produced to ensure that the customer's specifications have been met. Inspection takes essentially the same time regardless of the type of part being produced. Carbon's Cost Accounting Department has provided the following budgeted data for customer-related activities and costs (the amounts expected for the coming year):

Required:

1. Assign the customer-related activity costs to each category of customers in proportion to the sales revenue earned by each customer type. Calculate the profitability of each customer type. Discuss the problems with this measure of customer profitability.

2. Assign the customer-related activity costs to each customer type using activity rates. Now calculate the profitability of each customer category. As a manager, how would you use this information?

Carbon Company sells electrical components to medical equipment manufacturers for an average price of $1.05 per part. There are two types of customers: those who place small, frequent orders and those who place larger, less frequent orders. Each time an order is placed and processed, a setup is required. Scheduling is also needed to coordinate the many different orders that come in and place demands on the plant's manufacturing resources. Carbon also inspects a sample of the products each time a batch is produced to ensure that the customer's specifications have been met. Inspection takes essentially the same time regardless of the type of part being produced. Carbon's Cost Accounting Department has provided the following budgeted data for customer-related activities and costs (the amounts expected for the coming year):

Required:

1. Assign the customer-related activity costs to each category of customers in proportion to the sales revenue earned by each customer type. Calculate the profitability of each customer type. Discuss the problems with this measure of customer profitability.

2. Assign the customer-related activity costs to each customer type using activity rates. Now calculate the profitability of each customer category. As a manager, how would you use this information?

Explanation Verified

Verified

1.

Assigning the customer related activ...

Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255