Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Edition 1ISBN: 978-0538736787Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Edition 1ISBN: 978-0538736787 Exercise 18

SCORECARD MEASURES, STRATEGY TRANSLATION

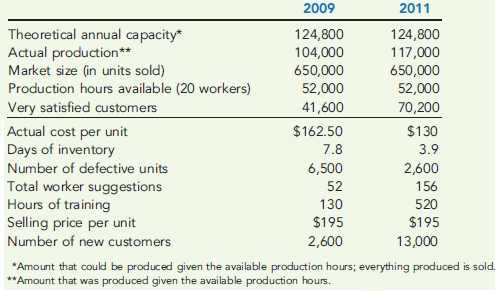

At the end of 2009, Activo Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Activo undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Activo wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered:

Required:

1. Compute the following measures for 2009 and 2011:

a. Actual velocity and cycle time

b. Percentage of total revenue from new customers (assume one unit per customer)

c. Percentage of very satisfied customers (assume each customer purchases one unit)

d. Market share

e. Percentage change in actual product cost (for 2011 only)

f. Percentage change in days of inventory (for 2011 only)

g. Defective units as a percentage of total units produced

h. Total hours of training

i. Suggestions per production worker

j. Total revenue

k. Number of new customers

2. For the measures listed in Requirement 1, list likely strategic objectives, classified according to the four Balance Scorecard perspectives. Assume there is one measure per objective.

At the end of 2009, Activo Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Activo undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Activo wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered:

Required:

1. Compute the following measures for 2009 and 2011:

a. Actual velocity and cycle time

b. Percentage of total revenue from new customers (assume one unit per customer)

c. Percentage of very satisfied customers (assume each customer purchases one unit)

d. Market share

e. Percentage change in actual product cost (for 2011 only)

f. Percentage change in days of inventory (for 2011 only)

g. Defective units as a percentage of total units produced

h. Total hours of training

i. Suggestions per production worker

j. Total revenue

k. Number of new customers

2. For the measures listed in Requirement 1, list likely strategic objectives, classified according to the four Balance Scorecard perspectives. Assume there is one measure per objective.

Explanation Verified

Verified

1. Calculation of the given measures for...

Cornerstones of Cost Accounting 1st Edition by Don Hansen,Maryanne Mowen

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255