Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Edition 3ISBN: 978-9352863501 Exercise 6

Consider TSLS estimation with a single included endogenous variable and a single instrument. Then the predicted value from the first-stage regression is

Use the definition of the sample variance and covariance to show that

Use the definition of the sample variance and covariance to show that

Use this result to fill in the steps of the derivation in Appendix of Equation (12.4).

Use this result to fill in the steps of the derivation in Appendix of Equation (12.4).

Appendix

Derivation of the Formula for the TSLS Estimator in Equation (12.4)

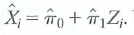

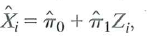

The first stage of TSLS is to regress X i on the instrument Z i by OLS and then compute the OLS predicted value

, and the second stage is to regress Y i on

, and the second stage is to regress Y i on

by OLS. Accordingly, the formula for the TSLS estimator, expressed in terms of the predicted value

by OLS. Accordingly, the formula for the TSLS estimator, expressed in terms of the predicted value

is the formula for the OLS estimator in Key Concept 4.2, with

is the formula for the OLS estimator in Key Concept 4.2, with

replacing X i. That is,

replacing X i. That is,

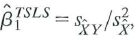

, where

, where

, is the sample variance of

, is the sample variance of

and

and

is the sample covariance between Y i and

is the sample covariance between Y i and

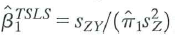

Because X i is the predicted value of X i from the first-stage regression,

, the definitions of sample variances and covariances imply that

, the definitions of sample variances and covariances imply that

(Exercise 12.4). Thus, the TSLS estimator can be written as

(Exercise 12.4). Thus, the TSLS estimator can be written as

. Finally,

. Finally,

is the OLS slope coefficient from the first stage of TSLS, so

is the OLS slope coefficient from the first stage of TSLS, so

Substitution of this formula for

Substitution of this formula for

into the formula

into the formula

yields the formula for the TSLS estimator in Equation (12.4).

yields the formula for the TSLS estimator in Equation (12.4).

Use the definition of the sample variance and covariance to show that Use this result to fill in the steps of the derivation in Appendix of Equation (12.4).Appendix

Derivation of the Formula for the TSLS Estimator in Equation (12.4)

The first stage of TSLS is to regress X i on the instrument Z i by OLS and then compute the OLS predicted value

, and the second stage is to regress Y i on by OLS. Accordingly, the formula for the TSLS estimator, expressed in terms of the predicted value is the formula for the OLS estimator in Key Concept 4.2, with replacing X i. That is, , where , is the sample variance of and is the sample covariance between Y i and Because X i is the predicted value of X i from the first-stage regression,

, the definitions of sample variances and covariances imply that (Exercise 12.4). Thus, the TSLS estimator can be written as . Finally, is the OLS slope coefficient from the first stage of TSLS, so Substitution of this formula for into the formula yields the formula for the TSLS estimator in Equation (12.4).Explanation Verified

Verified

For a TSLS regression, we have:

![]() Here, ...

Here, ...

Introduction to Econometrics 3rd Edition by James Stock, Mark Watson

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255