Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501 Exercise 15

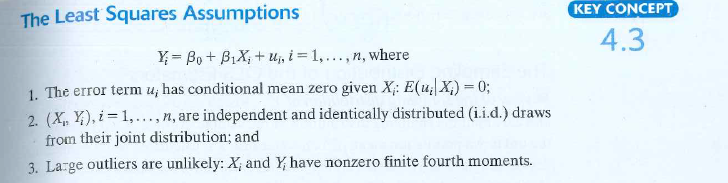

Suppose that ( Y i, X i ) satisfy the assumptions in Key Concept 4.3 and, in addition, u i , is N( 0, u 2 ,) and is independent of X t.

a. Is conditionally unbiased

conditionally unbiased

b. Is the best linear conditionally unbiased estimator of 1

the best linear conditionally unbiased estimator of 1

c. How would your answers to (a) and (b) change if you assumed only that ( Y i X i ,) satisfied the assumptions in Key Concept 4.3 and var is constant

is constant

d. How would your answers to (a) and (b) change if you assumed only that ( Y i X i ,) satisfied the assumptions in Key Concept 4.3

a. Is

conditionally unbiased b. Is

the best linear conditionally unbiased estimator of 1 c. How would your answers to (a) and (b) change if you assumed only that ( Y i X i ,) satisfied the assumptions in Key Concept 4.3 and var

is constant d. How would your answers to (a) and (b) change if you assumed only that ( Y i X i ,) satisfied the assumptions in Key Concept 4.3

Explanation Verified

Verified

The least squares assumption ![]() It is give...

It is give...

Introduction to Econometrics 3rd Edition by James Stock, James Stock

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255