Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501 Exercise 16

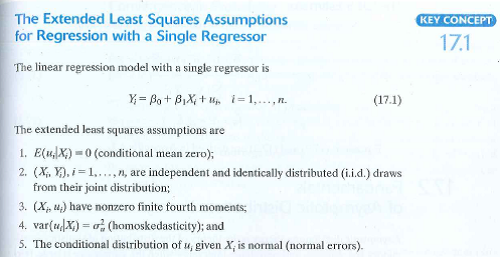

Suppose that Assumption #4 in Key Concept 17.1 is true, but you construct a 95% confidence interval for 1 using the heteroskedastic-robust standard error in a large sample. Would this confidence interval be valid asymptotically in the sense that it contained the true value of 1 in 95% of all repeated samples for large n Suppose instead that Assumption #4 in Key Concept 17.1 is false, but you construct a 95% confidence interval for 1 using the homoskedasticity-only standard error formula in a large sample. Would this confidence interval be valid asymptotically

Explanation Verified

Verified

If heteroskedastic standard errors are a...

Introduction to Econometrics 3rd Edition by James Stock, James Stock

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255