Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501 Exercise 11

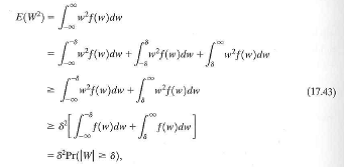

Let  be an estimator of the parameter , where

be an estimator of the parameter , where  might be biased. Show that if

might be biased. Show that if  (that is, the mean squared error of

(that is, the mean squared error of  tends to zero), then

tends to zero), then  .

.

be an estimator of the parameter , where might be biased. Show that if (that is, the mean squared error of tends to zero), then . Explanation Verified

Verified

The proof of Chebychev's inequality give...

Introduction to Econometrics 3rd Edition by James Stock, James Stock

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255