Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501Introduction to Econometrics 3rd Edition by James Stock, James Stock

Edition 3ISBN: 978-9352863501 Exercise 15

Consider the heterogeneous regression model  where 0i and 1i are random variables that differ from one observation to the next. Suppose that

where 0i and 1i are random variables that differ from one observation to the next. Suppose that  are distributed independently of X i.

are distributed independently of X i.

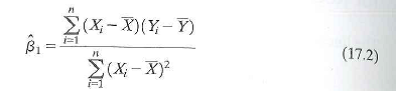

a. Let denote the OLS estimator of 1 given in Equation (17.2). Show that

denote the OLS estimator of 1 given in Equation (17.2). Show that  , where E ( 1 ) is the average value of 1 i in the population.

, where E ( 1 ) is the average value of 1 i in the population.

b. Suppose that , where 0 and 1 are known positive constants. Let

, where 0 and 1 are known positive constants. Let  denote the weighted least squares estimator. Does

denote the weighted least squares estimator. Does  Explain.

Explain.

where 0i and 1i are random variables that differ from one observation to the next. Suppose that are distributed independently of X i. a. Let

denote the OLS estimator of 1 given in Equation (17.2). Show that , where E ( 1 ) is the average value of 1 i in the population.b. Suppose that

, where 0 and 1 are known positive constants. Let denote the weighted least squares estimator. Does Explain. Explanation Verified

Verified

a) The heterogeneous regression is ![]() The ...

The ...

Introduction to Econometrics 3rd Edition by James Stock, James Stock

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255