Federal Tax Research 10th Edition by Roby Sawyers,William Raabe,Gerald Whittenburg,Steven Gill

Edition 10ISBN: 978-1285439396Federal Tax Research 10th Edition by Roby Sawyers,William Raabe,Gerald Whittenburg,Steven Gill

Edition 10ISBN: 978-1285439396 Exercise 30

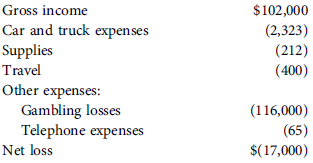

Charles Nobel works as a television talk show host for Broadcast Inc. In 2013, Charles generated substantial income from his employment. His wages from Broadcast were approximately $100,000 in 2013. The show is taped four days per week and taping lasts only a few hours each day. The crew of writers and Charles's ability to effortlessly read the teleprompter provide Charles with an extremely well-paid job for approximately 20 hours' work per week. This leaves Charles with time away from work that most U.S. employees would find enviable. In 2013, Charles found a way to use that extra time by becoming, in his words, a "professional slot machine gambler." On approximately 50 days in 2013, Charles played the slots in casinos in and around southern California. He managed to generate slot machine winnings of $102,000 in 2013; that is, his total winning payouts from slots were $102,000. However, during those same 50 days, Charles lost $116,000. Because of the level of play and money spent at the casinos, Charles was probably one of the top 1 percent or 2 percent of gamblers in all of southern California. In fact, he was frequently invited to slot machine tournaments based on his gambling and celebrity status. Charles also kept meticulous records of his gambling endeavors. He had detailed books and records that tracked the amounts played each day, the amounts won and lost, and various other expenses incurred. It seemed clear that Charles took his gambling very seriously. In previous years, Charles had played the slots less frequently but had managed to generate net gambling winnings (his wins exceeded his losses) and truly believed he could make money playing slots "professionally." On his 2013 tax return (Schedule C of Form 1040-Profit or Loss from Business), Charles reported the following:

Prepare a tax research memorandum to the files that provides your opinion on the proper treatment of Charles's gambling activities as it relates to calculating his taxable income (i.e., what is the taxable income or loss from Charles's gambling). For the purposes of this memo, you may assume that his gambling activities rise to the level of a trade or business. You may also assume that all Charles's expenses are ordinary and necessary business expenses that are fully supported and directly related to his gambling business.

Prepare a tax research memorandum to the files that provides your opinion on the proper treatment of Charles's gambling activities as it relates to calculating his taxable income (i.e., what is the taxable income or loss from Charles's gambling). For the purposes of this memo, you may assume that his gambling activities rise to the level of a trade or business. You may also assume that all Charles's expenses are ordinary and necessary business expenses that are fully supported and directly related to his gambling business.

Explanation Verified

Verified

US Federal Tax Laws: The very first step...

Federal Tax Research 10th Edition by Roby Sawyers,William Raabe,Gerald Whittenburg,Steven Gill

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255