Fundamentals of Oil & Gas Accounting 5th Edition by Rebecca Gallun, Charlotte Wright

Edition 5ISBN: 9781630181031Fundamentals of Oil & Gas Accounting 5th Edition by Rebecca Gallun, Charlotte Wright

Edition 5ISBN: 9781630181031 Exercise 12

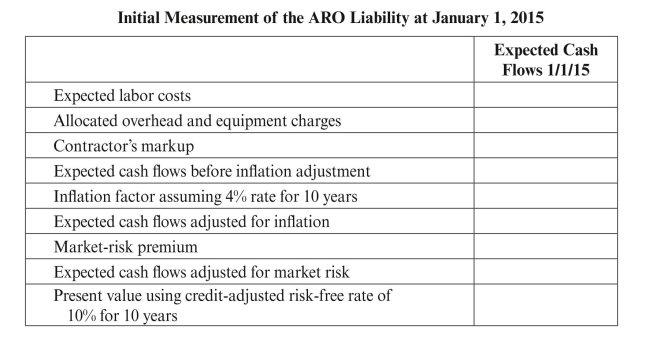

Ameritec Oil and Gas Company completes construction of an offshore oil platform

and places it into service on January 1, 2015. Ameritec is legally required to dismantle

and remove the platform at the end of its useful life, which is estimated to be 10 years.

On January 1, 2015, Ameritec recognized a liability for an asset retirement obligation

and capitalized an amount for an asset retirement cost. It estimated the initial fair value

of the liability using an expected present value technique. The significant assumptions

used in that estimate of fair value are as follows:

a. Labor costs are based on current marketplace wages required to hire contractors

to dismantle and remove offshore oil platforms. Ameritec assigns probability

assessments to a range of cash flow estimates as follows: b. Ameritec estimates allocated overhead and equipment charges using the rate it

b. Ameritec estimates allocated overhead and equipment charges using the rate it

applies to labor costs for transfer pricing (60%). The entity has no reason to believe

that its overhead and equipment rate differs from that used by contractors in the

industry.

c. A contractor typically adds a markup on labor, allocated internal costs, and

equipment to provide a profit margin on the job. The entity determines the profit

that contractors in the industry generally earn to dismantle and remove offshore oil

platforms is 15%.

d. A contractor would typically demand and receive a premium (market risk

premium) for bearing the uncertainty and unforeseeable circumstances inherent in

"locking in" today's price for a project that will not occur for 10 years. The entity

estimates the amount of that premium to be 5% of the estimated inflation-adjusted

cash flows.

e. The risk-free rate of interest on January 1, 2015 is 6%. The entity adjusts that rate

by 4% to reflect the effect of its credit standing. Therefore, the credit-adjusted risk-

free rate used to compute expected present value is 10%. (Round the present value

factor to four decimal places.)

f. Ameritec assumes a rate of inflation of 4% over the 10-year period. (Round the

factor to four decimal places.)

REqUIRED:

a. Complete the following tables:

b. Prepare the journal entry that would be made on January 1, 2015 to record the asset

b. Prepare the journal entry that would be made on January 1, 2015 to record the asset

retirement obligation.

c. Prepare the journal entries that would be made from December 31, 2015 to

December 31, 2024 to record the accretion expense and the amortization expense

related to the ARO.

d. On December 31, 2024, the entity settles its asset retirement obligation by using its

internal workforce at a cost of $432,000. Assume no changes during the 10-year

period in the cash flows used to estimate the obligation. Prepare the journal entry

that would be made on December 31, 2024 to record the settlement of the asset

retirement obligation.

and places it into service on January 1, 2015. Ameritec is legally required to dismantle

and remove the platform at the end of its useful life, which is estimated to be 10 years.

On January 1, 2015, Ameritec recognized a liability for an asset retirement obligation

and capitalized an amount for an asset retirement cost. It estimated the initial fair value

of the liability using an expected present value technique. The significant assumptions

used in that estimate of fair value are as follows:

a. Labor costs are based on current marketplace wages required to hire contractors

to dismantle and remove offshore oil platforms. Ameritec assigns probability

assessments to a range of cash flow estimates as follows:

b. Ameritec estimates allocated overhead and equipment charges using the rate itapplies to labor costs for transfer pricing (60%). The entity has no reason to believe

that its overhead and equipment rate differs from that used by contractors in the

industry.

c. A contractor typically adds a markup on labor, allocated internal costs, and

equipment to provide a profit margin on the job. The entity determines the profit

that contractors in the industry generally earn to dismantle and remove offshore oil

platforms is 15%.

d. A contractor would typically demand and receive a premium (market risk

premium) for bearing the uncertainty and unforeseeable circumstances inherent in

"locking in" today's price for a project that will not occur for 10 years. The entity

estimates the amount of that premium to be 5% of the estimated inflation-adjusted

cash flows.

e. The risk-free rate of interest on January 1, 2015 is 6%. The entity adjusts that rate

by 4% to reflect the effect of its credit standing. Therefore, the credit-adjusted risk-

free rate used to compute expected present value is 10%. (Round the present value

factor to four decimal places.)

f. Ameritec assumes a rate of inflation of 4% over the 10-year period. (Round the

factor to four decimal places.)

REqUIRED:

a. Complete the following tables:

b. Prepare the journal entry that would be made on January 1, 2015 to record the assetretirement obligation.

c. Prepare the journal entries that would be made from December 31, 2015 to

December 31, 2024 to record the accretion expense and the amortization expense

related to the ARO.

d. On December 31, 2024, the entity settles its asset retirement obligation by using its

internal workforce at a cost of $432,000. Assume no changes during the 10-year

period in the cash flows used to estimate the obligation. Prepare the journal entry

that would be made on December 31, 2024 to record the settlement of the asset

retirement obligation.

Explanation Verified

Verified

a. ![]() b.Initial measurement of the ARO lia...

b.Initial measurement of the ARO lia...

Fundamentals of Oil & Gas Accounting 5th Edition by Rebecca Gallun, Charlotte Wright

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255