Deck 8: Consolidated Tax Returns

Full screen (f)

Question

Question

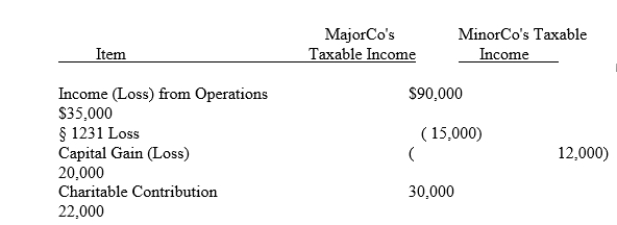

MajorCo and MinorCo had the following items of income and deduction for the current year:  Compute MajorCo and MinorCo's taxable income or loss computed on a separate basis.

Compute MajorCo and MinorCo's taxable income or loss computed on a separate basis.

Compute MajorCo and MinorCo's taxable income or loss computed on a separate basis. Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/10

Play

Full screen (f)

Deck 8: Consolidated Tax Returns

1

ParentCo and SubCo had the following items of income and deduction for the current year: Compute ParentCo and SubCo's consolidated taxable income or loss.

A)$215,000

B)$210,000.

C)$189,000.

D)$170,000.

E)None of the above.

A)$215,000

B)$210,000.

C)$189,000.

D)$170,000.

E)None of the above.

$189,000.

2

MajorCo and MinorCo had the following items of income and deduction for the current year: Compute MajorCo and MinorCo's taxable income or loss computed on a separate basis.

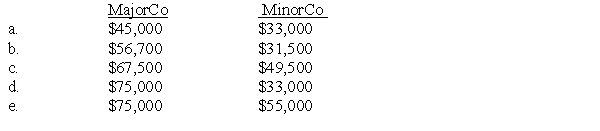

Compute MajorCo and MinorCo's taxable income or loss computed on a separate basis. C

3

Blue, Red, and White Corporations file Federal tax returns on a consolidated basis.The group's tax return has been under audit.Under a valid tax-sharing agreement, each corporation is liable for one-third of the group's consolidated tax liability.The parties have agreed that the group's unpaid liability for the year is $350,000.Because of an incorrect tax return position, $120,000 interest and a $90,000 penalty is attributable to Blue.At present, only Red is solvent and has the cash with which to make such a substantial tax payment.What is the maximum amount for which the IRS could be successful in forcing Red to satisfy the outstanding liabilities of the consolidated group?

A)$560,000.

B)$350,000.

C)$116,667.

D)$186,667.

E)Some other amount.

A)$560,000.

B)$350,000.

C)$116,667.

D)$186,667.

E)Some other amount.

A

4

Cardinal owned 100% of Bluejay for the entire year, and both companies use the accrual method of tax accounting.During the year, Bluejay purchased $30,000 of supplies from Cardinal.In addition, Bluejay provided certain accounting services to Cardinal for $10,000.Including these transactions, Cardinal's separate taxable income was $80,000, and Bluejay's separate taxable income was $50,000.What is the group's consolidated taxable income for the year?

A)$130,000.

B)$120,000.

C)$100,000.

D)$90,000.

E)None of the above.

A)$130,000.

B)$120,000.

C)$100,000.

D)$90,000.

E)None of the above.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

5

Loon's separate taxable income was $250,000, and Goose's was $140,000.Consolidated taxable income before contributions was $350,000.Charitable contributions made by the affiliated group included $11,000 by Loon and $12,000 by Goose.Compute the group's charitable contribution deduction.

A)$39,000.

B)$35,000.

C)$23,000.

D)$0.

E)Some other amount.

A)$39,000.

B)$35,000.

C)$23,000.

D)$0.

E)Some other amount.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

6

Raven purchased all of the stock of Dove on January 1, 2007, for $200,000.Dove produced a loss for 2007 of $280,000 and paid a dividend of $30,000 to Raven.In 2008, Dove generated a loss of $140,000; in 2009, it recognized net income of $100,000.What is Raven's capital gain or loss if it sells all of its Dove stock to a nongroup member on January 1, 2010, for $40,000?

A)($110,000).

B)$-0-.

C)$110,000.

D)$190,000.

E)Some other amount.

A)($110,000).

B)$-0-.

C)$110,000.

D)$190,000.

E)Some other amount.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

7

Finch acquired all of the stock of Gull on January 1, 2007, for $250,000.The parties immediately elected to file consolidated tax returns.Gull generated taxable income of $30,000 for 2007 and paid a dividend of $25,000 to Finch.In 2008, Gull generated an operating loss of $90,000, and in 2009 produced taxable income of $30,000.As of the last day of 2009, what was Finch's basis in the stock of Gull?

A)$310,000.

B)$250,000.

C)$220,000.

D)$195,000.

E)Some other amount.

A)$310,000.

B)$250,000.

C)$220,000.

D)$195,000.

E)Some other amount.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

8

Starling and Bunting had the following items of income and deduction for the current year: Compute Starling and Bunting's consolidated taxable income or loss.

A)$106,200.

B)$107,000.

C)$124,200.

D)$127,700.

E)$138,000.

A)$106,200.

B)$107,000.

C)$124,200.

D)$127,700.

E)$138,000.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

9

Macaw owned 100% of Flamingo for the entire year.Macaw uses the accrual method of tax accounting, whereas Flamingo uses the cash method.During the year, Flamingo sold raw materials to Macaw for $10,000 under a contract that requires no payment to Flamingo until the following year. Exclusive of this transaction, Macaw had income for the year of $90,000, and Flamingo had income of $40,000.The group's consolidated taxable income for the year is:

A)$120,000.

B)$130,000.

C)$140,000.

D)Some other amount.

E)Cannot be determined.

A)$120,000.

B)$130,000.

C)$140,000.

D)Some other amount.

E)Cannot be determined.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

10

Quail's separate taxable income was $80,000, and Pigeon's was $150,000.Consolidated taxable income before contributions was $210,000.Charitable contributions made by the affiliated group included $20,000 by Quail and $18,000 by Pigeon.Compute the group's charitable contribution deduction.

A)$38,000.

B)$23,000.

C)$21,000.

D)$0.

E)Some other amount.

A)$38,000.

B)$23,000.

C)$21,000.

D)$0.

E)Some other amount.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 10 flashcards in this deck.