Deck 16: Dilutive Securities and Earnings Per Share

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

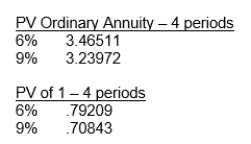

Mae Jong Corp.issues 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.When Mae Jong records the issuance of these bonds, how much will it credit to Share Premium-Conversion Equity? The following present value factors are available:

A)€ -0-

B)€97,187

C)€83,663

D)€250,000

A)€ -0-

B)€97,187

C)€83,663

D)€250,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

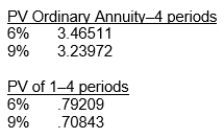

Mae Jong Corp.issues 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.Compute the liability component of Mae Jong's convertible dent.The following present value factors are available:

A)€1,000,000

B)€750,000

C)€902,813

D)€916,337

A)€1,000,000

B)€750,000

C)€902,813

D)€916,337

Question

Question

Question

On January 1, 2011 Reese Company granted Jack Buchanan, an employee, an option to buy 100 shares of Reese Co.shares for $40 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $1,200.Buchanan exercised his option on September 1, 2011, and sold his 100 shares on December 1, 2011.Quoted market prices of Reese Co.shares during 2011 were:

The service period is for two years beginning January 1, 2011.As a result of the option granted to Buchanan, using the fair value method, Reese should recognize compensation expense for 2011 on its books in the amount of

A)$0.

B)$600.

C)$1,200

D)$1,400

The service period is for two years beginning January 1, 2011.As a result of the option granted to Buchanan, using the fair value method, Reese should recognize compensation expense for 2011 on its books in the amount of

A)$0.

B)$600.

C)$1,200

D)$1,400

Question

Question

Question

Question

On January 1, 2012, Trent Company granted Dick Williams, an employee, an option to buy 100 shares of Trent Co.shares for $30 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $900.Williams exercised his option on September 1, 2012, and sold his 100 shares on December 1, 2012.Quoted market prices of Trent Co.shares during 2012 were:

The service period is for two years beginning January 1,2012.As a result of the option granted to Williams, using the fair value method, Trent should recognize compensation expense for 2012 on its books in the amount of

A)$1,000.

B)$900.

C)$450.

D)$0.

The service period is for two years beginning January 1,2012.As a result of the option granted to Williams, using the fair value method, Trent should recognize compensation expense for 2012 on its books in the amount of

A)$1,000.

B)$900.

C)$450.

D)$0.

Question

Question

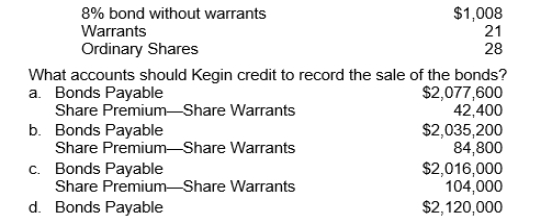

On April 7, 2012, Kegin Corporation sold a $2,000,000, twenty-year, 8 percent bond issue for $2,120,000.Each $1,000 bond has two detachable warrants, each of which permits the purchase of one share of the corporation's ordinary shares for $30.The shares have a par value of $25 per share.Immediately after the sale of the bonds, the corporation's securities had the following fair values:

Question

Question

Question

Question

Question

On July 1, 2012, Ellison Company granted Sam Wine, an employee, an option to buy 400 shares of Ellison Co.shares for $30 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $1,800.Wine exercised his option on October 1, 2012 and sold his 400 shares on December 1, 2010.Quoted market prices of Ellison Co.shares in 2012 were:

The service period is for three years beginning January 1, 2012.As a result of the option granted to Wine, using the fair value method, Ellison should recognize compensation expense on its books in the amount of

A)$1,800.

B)$600.

C)$450.

D)$0.

The service period is for three years beginning January 1, 2012.As a result of the option granted to Wine, using the fair value method, Ellison should recognize compensation expense on its books in the amount of

A)$1,800.

B)$600.

C)$450.

D)$0.

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2011, Evans Company granted Tim Telfer, an employee, an option to buy 1,000 ordinary shares of Evans Co.for $25 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $7,500.Telfer exercised his option on September 1, 2011, and sold his 1,000 shares on December 1, 2011.Quoted market prices of Evans Co.shares during 2011 were

The service period is for three years beginning January 1, 2011.As a result of the option granted to Telfer, using the fair value method, Evans should recognize compensation expense for 2011 on its books in the amount of

A)$9,000.

B)$7,500.

C)$2,500.

D)$1,500.

The service period is for three years beginning January 1, 2011.As a result of the option granted to Telfer, using the fair value method, Evans should recognize compensation expense for 2011 on its books in the amount of

A)$9,000.

B)$7,500.

C)$2,500.

D)$1,500.

Question

Question

In order to retain certain key executives, Jensen Corporation granted them incentive share options on December 31, 2009.50,000 options were granted at an option price of $35 per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $500,000.What amount of compensation expense should Jensen recognize as a result of this plan for the year ended

December 31, 2010 under the fair value method?

A)$250,000.

B)$500,000.

C)$550,000.

D)$1,750,000.

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $500,000.What amount of compensation expense should Jensen recognize as a result of this plan for the year ended

December 31, 2010 under the fair value method?

A)$250,000.

B)$500,000.

C)$550,000.

D)$1,750,000.

Question

In order to retain certain key executives, Smiley Corporation granted them incentive share options on December 31, 2009.80,000 options were granted at an option price of $35

Per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $800,000.What amount of compensation expense should Smiley recognize as a result of this plan for the year ended December 31, 2010 under the fair value method?

A)$1,400,000.

B)$880,000.

C)$800,000.

D)$400,000.

Per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $800,000.What amount of compensation expense should Smiley recognize as a result of this plan for the year ended December 31, 2010 under the fair value method?

A)$1,400,000.

B)$880,000.

C)$800,000.

D)$400,000.

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/71

Play

Full screen (f)

Deck 16: Dilutive Securities and Earnings Per Share

1

Preference dividends are subtracted from net income but not income from continuing operations in computing earnings per share.

False

2

Companies recognize a gain or loss on the conversion of convertible debt before maturity.

False

3

In computing diluted earnings per share, share options are considered dilutive when their option price is greater than the market price.

False

4

If a service condition exists, the company is not permitted to adjust the estimate of compensation expense.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

5

The number of contingent shares to be included indiluted earnings per share is based on the number of shares that would be issuable as if the end of the period were the end of the contingency period.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

6

The intrinsic value of a share option is the difference between the market price of the shares and the exercise price of the options at the grant date.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

7

If a share dividend occurs after year-end, but before the financial statements, are authorized for issuance, a company must restate the weighted-average number of shares outstanding for the year.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

8

A company should allocate the proceeds from the sale of debt with detachable share warrants between the two securities based on their a fair values.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

9

The service period in share option plans is the time between the grant date and the vesting date.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

10

Companies recognize a gain or loss when shareholders exercise convertible preference shares.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

11

IFRS requires that convertible debt be separated into its liability and equity components for accounting purposes.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

12

When share dividends or share splits occur, companies must restate the shares outstand-ing after the share dividend or split, in order to compute the weighted-average number of shares.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

13

If an employee fails to exercise a share option before its expiration date, the company should decrease compensation expense.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

14

Under the fair value method, companies compute total compensation expense based on the fair value of options on the date of exercise.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

15

A company should report per share amounts for income from continuing operations, but not for discontinued operations.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

16

The issuer of convertible preference shares uses the fair value method to record the conversion of the shares.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

17

Non detachable warrants, unlike detachable warrants, are not considered a compound instrument for accounting purposes.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

18

When a company has a complex capital structure, it must report both basic and diluted earnings per share.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

19

When an issuer offers some form of additional consideration (a sweetener) to encourage of its convertible debt, it reports the sweetener as a current period expense.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

20

If preference shares are cumulative and no dividends are declared, the company subtracts the current year preference dividend in computing earnings per share.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

21

Mae Jong Corp.issues 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.When Mae Jong records the issuance of these bonds, how much will it credit to Share Premium-Conversion Equity? The following present value factors are available:

A)€ -0-

B)€97,187

C)€83,663

D)€250,000

A)€ -0-

B)€97,187

C)€83,663

D)€250,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

22

Employee share purchase plans (ESPP)

A)Permit all employees to purchase shares at a discounted price.

B)Are generally considered noncompensatory and result in no compensation expense being recorded.

C)Distribute restricted shares to employees for a short period of time.

D)All of the choices are correct regarding ESPP.

A)Permit all employees to purchase shares at a discounted price.

B)Are generally considered noncompensatory and result in no compensation expense being recorded.

C)Distribute restricted shares to employees for a short period of time.

D)All of the choices are correct regarding ESPP.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

23

The conversion of preference shares may be recorded by the

A)incremental method.

B)book value method.

C)market value method.

D)par value method.

A)incremental method.

B)book value method.

C)market value method.

D)par value method.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

24

In accounting for share-appreciation rights plans, compensation expense is generally

A)not recognized because no excess of market price over the option price exists at the date of grant.

B)recognized in the period of the grant.

C)allocated over the service period of the employees.

D)recognized in the period of exercise.

A)not recognized because no excess of market price over the option price exists at the date of grant.

B)recognized in the period of the grant.

C)allocated over the service period of the employees.

D)recognized in the period of exercise.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

25

When the cash proceeds from bonds issued with detachable share warrants exceed the fair value of the bonds without the warrants, the excess should be credited to

A)share premium-ordinary.

B)retained earnings.

C)share a liability account.

D)premium-share warrants.

A)share premium-ordinary.

B)retained earnings.

C)share a liability account.

D)premium-share warrants.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

26

The date on which total compensation expense is computed in a share option plan is the date

A)of grant.

B)of exercise.

C)that the market price coincides with the option price.

D)that the market price exceeds the option price.

A)of grant.

B)of exercise.

C)that the market price coincides with the option price.

D)that the market price exceeds the option price.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

27

Convertible bonds

A)Are separated into the bond component and the expense component.

B)Allow a company to issue debt financing at cheaper rates.

C)Are separated into their components based on relative fair values.

D)All of the choices are correct.

A)Are separated into the bond component and the expense component.

B)Allow a company to issue debt financing at cheaper rates.

C)Are separated into their components based on relative fair values.

D)All of the choices are correct.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

28

According to IFRS, a company makes only a memorandum entry when

A)Companies give warrants to executives and employees as a form of compensation.

B)Companies include warrants to make a security more attractive.

C)Companies issue rights to existing shareholders.

D)All of the choices are correct.

A)Companies give warrants to executives and employees as a form of compensation.

B)Companies include warrants to make a security more attractive.

C)Companies issue rights to existing shareholders.

D)All of the choices are correct.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

29

According to IFRS, once the total compensation is measured at the date of grant

A)It can be changed in future periods related to a change in market conditions.

B)It can be changed to reflect the rise or fall in the market price of the company's ordinary shares.

C)A company is permitted to adjust the number of share options expected to the actual number of instruments vested.

D)All of the choices are correct.

A)It can be changed in future periods related to a change in market conditions.

B)It can be changed to reflect the rise or fall in the market price of the company's ordinary shares.

C)A company is permitted to adjust the number of share options expected to the actual number of instruments vested.

D)All of the choices are correct.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

30

Morgan Corporation had two issues of securities outstanding: ordinary shares and an 8% convertible bond issue in the face amount of $16,000,000.Interest payment dates of the bond issue are June 30th and December 31st.The conversion clause in the bond indenture entitles the bondholders to receive forty shares of $20 par value ordinary shares in exchange for each $1,000 bond.On June 30, 2010, the holders of $2,400,000 face value bonds exercised the conversion privilege.The market price of the bonds on that date was $1,100 per bond and the market price of the shares was $35.The total unamortized bond discount at the date of conversion was $1,000,000.What amount should Morgan credit to the account "share premium-ordinary," as a result of this conversion?

A)$330,000.

B)$160,000.

C)$1,440,000.

D)$720,000.

A)$330,000.

B)$160,000.

C)$1,440,000.

D)$720,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

31

Compensation expense resulting from a compensatory share option plan is generally

A)recognized in the period of exercise.

B)recognized in the period of the grant.

C)allocated to the periods benefited by the employee's required service.

D)allocated over the periods of the employee's service life to retirement.

A)recognized in the period of exercise.

B)recognized in the period of the grant.

C)allocated to the periods benefited by the employee's required service.

D)allocated over the periods of the employee's service life to retirement.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

32

Litke Corporation issued at a premium of $5,000 a $100,000 bond issue convertible into 2,000 ordinary shares (par value $40).At the time of the conversion, the unamortized premium is $2,000, the market value of the bonds is $110,000, and the shares are quoted on the market at $60 per share.If the bonds are converted ordinary shares, what is the amount of share premium to be recorded on the conversion of the bonds?

A)$25,000

B)$22,000

C)$32,000

D)$40,000

A)$25,000

B)$22,000

C)$32,000

D)$40,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

33

Convertible bonds

A)have priority over other indebtedness.

B)are usually secured by a first or second mortgage.

C)pay interest only in the event earnings are sufficient to cover the interest.

D)may be exchanged for equity securities.

A)have priority over other indebtedness.

B)are usually secured by a first or second mortgage.

C)pay interest only in the event earnings are sufficient to cover the interest.

D)may be exchanged for equity securities.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

34

An executive pays no taxes at time of exercise in a(an)

A)share appreciation rights plan.

B)incentive share option plan.

C)nonqualified share option plan.

D)Taxes would be paid in all of these.

A)share appreciation rights plan.

B)incentive share option plan.

C)nonqualified share option plan.

D)Taxes would be paid in all of these.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

35

Mae Jong Corp issues $1,000,000 of 10% bonds payable which may be converted into 10,000 shares of $2 par value ordinary shares.The market rate of interest on similar bonds is 12%.Interest is payable annually on December 31, and the bonds were issued for total proceeds of $1,000,000.In accounting for these bonds, Mae Jong Corp.will

A)First assign a value of the equity component, then determine the liability component.

B)Assign no value to the equity component since the conversion privilege is not separable from the bond.

C)First assign a value to the liability component based on the face amount of the bond.

D)Use the "with-and-without" method to value the compound instrument.

A)First assign a value of the equity component, then determine the liability component.

B)Assign no value to the equity component since the conversion privilege is not separable from the bond.

C)First assign a value to the liability component based on the face amount of the bond.

D)Use the "with-and-without" method to value the compound instrument.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

36

The conversion of bonds is most commonly recorded by the

A)incremental method.

B)proportional method.

C)fair value method.

D)book value method.

A)incremental method.

B)proportional method.

C)fair value method.

D)book value method.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

37

Fogel Co.has $2,500,000 of 8% convertible bonds outstanding.Each $1,000 bond is convertible into 30 shares of $30 par value ordinary shares.The bonds pay interest on January 31 and July 31.On July 31, 2012, the holders of $800,000 bonds exercised the conversion privilege.On that date the market price of the bonds was 105 and the market price of the ordinary shares was $36.The total unamortized bond premium at the date of conversion was $175,000.Fogel should record, as a result of this conversion, a

A)credit of $136,000 to Share Premium-Ordinary.

B)credit of $120,000 to Share Premium-Ordinary.

C)credit of $56,000 to on Bonds Payable.

D)loss of $8,000.

A)credit of $136,000 to Share Premium-Ordinary.

B)credit of $120,000 to Share Premium-Ordinary.

C)credit of $56,000 to on Bonds Payable.

D)loss of $8,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

38

For share appreciation rights, the measurement date for computing compensation is the date

A)the rights mature.

B)the share's price reaches a predetermined amount.

C)of grant.

D)of exercise.

A)the rights mature.

B)the share's price reaches a predetermined amount.

C)of grant.

D)of exercise.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

39

Mae Jong Corp.issues 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.Compute the liability component of Mae Jong's convertible dent.The following present value factors are available:

A)€1,000,000

B)€750,000

C)€902,813

D)€916,337

A)€1,000,000

B)€750,000

C)€902,813

D)€916,337

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

40

On July 1, 2012, an interest payment date, $60,000 of Parks Co.bonds were converted into 1,200 ordinary shares of Parks Co.each having a par value of $45 and a fair value of $54.There is $2,400 unamortized discount on the bonds.Parks would record

A)no change in share premium.

B)a $3,600 increase in share premium.

C)a $7,200 increase in share premium.

D)a $4,800 increase in share premium.

A)no change in share premium.

B)a $3,600 increase in share premium.

C)a $7,200 increase in share premium.

D)a $4,800 increase in share premium.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

41

Mae Jong Corp.issued 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.Assume that at the issuance date, €97,187 was credited to Share Premium-Conversion Equity.The bonds were not converted at maturity and Mae Jong pays off the convertible debt holders.What amount will Mae Jong record as a gain or a loss on this transaction?

A)€ -0-

B)€97,187

C)€24,297

D)€250,000

A)€ -0-

B)€97,187

C)€24,297

D)€250,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

42

On January 1, 2011 Reese Company granted Jack Buchanan, an employee, an option to buy 100 shares of Reese Co.shares for $40 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $1,200.Buchanan exercised his option on September 1, 2011, and sold his 100 shares on December 1, 2011.Quoted market prices of Reese Co.shares during 2011 were:

The service period is for two years beginning January 1, 2011.As a result of the option granted to Buchanan, using the fair value method, Reese should recognize compensation expense for 2011 on its books in the amount of

A)$0.

B)$600.

C)$1,200

D)$1,400

The service period is for two years beginning January 1, 2011.As a result of the option granted to Buchanan, using the fair value method, Reese should recognize compensation expense for 2011 on its books in the amount of

A)$0.

B)$600.

C)$1,200

D)$1,400

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

43

Pelton, Inc.issued £2,000,000 par value, 7% convertible bonds at 99 for cash.The net present value of the debt without the conversion feature is £1,9000,000.What amount will Peloton assign to the equity feature of these bonds?

A)£100,000

B)£ - 0 -

C)£99,000

D)£80,000

A)£100,000

B)£ - 0 -

C)£99,000

D)£80,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

44

Mae Jong Corp.issued 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.On December 31, 2012, Mae Jong wishes to reduce its annual interest cost.The company agrees to pay the holder of its convertible bonds an additional €40,000 if they will convert.Assuming conversion occurs, Mae Jong's journal entry to record the conversion will include all of the following except

A)Debit Bonds Payable €1,000,000.

B)Debit Share Premium-Ordinary €40,000.

C)Credit Cash €40,000.

D)Credit Share Capital-Ordinary €250,000.

A)Debit Bonds Payable €1,000,000.

B)Debit Share Premium-Ordinary €40,000.

C)Credit Cash €40,000.

D)Credit Share Capital-Ordinary €250,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

45

Use the following information for questions.

On May 1, 2012, Payne Co.issued $300,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable share warrants entitling the holder to purchase for $40 one share of Payne's ordinary shares, $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Payne's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Payne should credit Share Premium -Share Warrants for

A)$9,000.

B)$12,000.

C)$21,000.

D)$12,360.

On May 1, 2012, Payne Co.issued $300,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable share warrants entitling the holder to purchase for $40 one share of Payne's ordinary shares, $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Payne's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Payne should credit Share Premium -Share Warrants for

A)$9,000.

B)$12,000.

C)$21,000.

D)$12,360.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 2012, Trent Company granted Dick Williams, an employee, an option to buy 100 shares of Trent Co.shares for $30 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $900.Williams exercised his option on September 1, 2012, and sold his 100 shares on December 1, 2012.Quoted market prices of Trent Co.shares during 2012 were:

The service period is for two years beginning January 1,2012.As a result of the option granted to Williams, using the fair value method, Trent should recognize compensation expense for 2012 on its books in the amount of

A)$1,000.

B)$900.

C)$450.

D)$0.

The service period is for two years beginning January 1,2012.As a result of the option granted to Williams, using the fair value method, Trent should recognize compensation expense for 2012 on its books in the amount of

A)$1,000.

B)$900.

C)$450.

D)$0.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

47

In 2011, Eklund, Inc., issued for $103 per share, 60,000 shares of $100 par value convertible preference shares.One share of preference shares can be converted into three shares of Eklund's $25 par value ordinary shares at the option of the preference shareholder.In August 2012, all of the preference shares were converted.The fair value of the ordinary shares at the date of the conversion was $30 per share.What total amount should be credited to share premium-ordinary as a result of the conversion of the preference shares into ordinary shares?

A)$1,020,000.

B)$780,000.

C)$1,500,000.

D)$1,680,000.

A)$1,020,000.

B)$780,000.

C)$1,500,000.

D)$1,680,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

48

On April 7, 2012, Kegin Corporation sold a $2,000,000, twenty-year, 8 percent bond issue for $2,120,000.Each $1,000 bond has two detachable warrants, each of which permits the purchase of one share of the corporation's ordinary shares for $30.The shares have a par value of $25 per share.Immediately after the sale of the bonds, the corporation's securities had the following fair values:

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

49

Use the following information for questions.

On May 1, 2012, Payne Co.issued $300,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable share warrants entitling the holder to purchase for $40 one share of Payne's ordinary shares, $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Payne's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Payne should record bonds at payable

A)discount of $296,640.

B)discount of $288,000.

C)discount of $300,000.

D)premium of $309,000.

On May 1, 2012, Payne Co.issued $300,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable share warrants entitling the holder to purchase for $40 one share of Payne's ordinary shares, $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Payne's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Payne should record bonds at payable

A)discount of $296,640.

B)discount of $288,000.

C)discount of $300,000.

D)premium of $309,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

50

Mae Jong Corp.issued 1,000 convertible bonds at the beginning of 2011.The bonds have a four-year term with a stated rate of interest of 6 percent, and are issued at par with a face value of €1,000 per bond (the total proceeds received from issuance of the bonds are €1,000,000).Interest is payable annually at December 31.Each bond is convertible into 250 ordinary shares with a par value of €1.The market rate of interest on similar non-convertible debt is 9 percent.Assume that at the issuance date, €97,187 was credited to Share Premium-Conversion Equity and that the bonds were not converted at maturity.What amount will Mae Jong credit to Share Premium-Ordinary at the maturity date? The following present value factors are available:

A)€750,000

B)€652,813

C)€847,187

D)€347,187

A)€750,000

B)€652,813

C)€847,187

D)€347,187

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

51

During 2012, Gordon Company issued at 104 three hundred, $1,000 bonds due in ten years.One detachable share warrant entitling the holder to purchase 15 shares of Gordon's ordinary shares was attached to each bond.At the date of issuance, the market value of the bonds, without the share warrants, was quoted at 96.The fair value of each detachable warrant was quoted at $40.What amount, if any, of the proceeds from the issuance should be accounted for as part of Gordon's equity?

A)$0

B)$12,000

C)$24,000

D)$12,480

A)$0

B)$12,000

C)$24,000

D)$12,480

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

52

Use the following information for questions.

On May 1, 2012, Marly Co.issued $500,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable stock warrants entitling the holder to purchase for $40 one share of Marly's ordinary shares $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Marly's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Marly should record bonds payable at

A)$515,000.

B)$500,000.

C)$480,000.

D)$494,400.

On May 1, 2012, Marly Co.issued $500,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable stock warrants entitling the holder to purchase for $40 one share of Marly's ordinary shares $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Marly's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Marly should record bonds payable at

A)$515,000.

B)$500,000.

C)$480,000.

D)$494,400.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

53

On July 1, 2012, Ellison Company granted Sam Wine, an employee, an option to buy 400 shares of Ellison Co.shares for $30 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $1,800.Wine exercised his option on October 1, 2012 and sold his 400 shares on December 1, 2010.Quoted market prices of Ellison Co.shares in 2012 were:

The service period is for three years beginning January 1, 2012.As a result of the option granted to Wine, using the fair value method, Ellison should recognize compensation expense on its books in the amount of

A)$1,800.

B)$600.

C)$450.

D)$0.

The service period is for three years beginning January 1, 2012.As a result of the option granted to Wine, using the fair value method, Ellison should recognize compensation expense on its books in the amount of

A)$1,800.

B)$600.

C)$450.

D)$0.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

54

On March 1, 2012, Ruiz Corporation issued $800,000 of 8% nonconvertible bonds at 104, which are due on February 28, 2032.In addition, each $1,000 bond was issued with 25 detachable share warrants, each of which entitled the bondholder to purchase for $50 one share of Ruiz ordinary shares, par value $25.The bonds without the warrants would normally sell at 95.On March 1, 2012, the fair value of Ruiz's ordinary shares was $40 per share and the fair value of the warrants was $2.What amount should Ruiz record on March 1, 2012 as share premium-share warrants?

A)$40,000

B)$41,600

C)$72,000

D)$83,200

A)$40,000

B)$41,600

C)$72,000

D)$83,200

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

55

Vernon Corporation offered detachable 5-year warrants to buy one ordinary share (par value $5) at $20 (at a time when the shares were selling for $32).The price paid for 2,000, $1,000 bonds with the warrants attached was $205,000.The market price of the Vernon bonds without the warrants was $180,000, and the market price of the warrants without the bonds was $20,000.What amount should be allocated to the warrants?

A)$20,000

B)$25,000

C)$24,000

D)$20,500

A)$20,000

B)$25,000

C)$24,000

D)$20,500

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

56

On December 1, 2012, Lester Company issued at 103, two hundred of its 9%, $1,000 bonds.Attached to each bond was one detachable share warrant entitling the holder to purchase 10 shares of Lester's ordinary shares.On December 1, 2012, the fair value of the bonds, without the share warrants, was 95, and the fair value of each share warrant was $50.The amount of the proceeds from the issuance that should be accounted for as the initial carrying value of the bonds payable would be

A)$195,700.

B)$190,000.

C)$200,000.

D)$206,000.

A)$195,700.

B)$190,000.

C)$200,000.

D)$206,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

57

On June 30, 2010, Yang Corporation granted compensatory share options for 20,000 shares of its $24 par value ordinary shares to certain of its key employees.The market price of the ordinary shares on that date was $31 per share and the option price was $28.Using a fair value option pricing model, total compensation expense is determined to be $64,000.The options are exercisable beginning January 1, 2012, providing those key employees are still in the employ of the company at the time the options are exercised.The options expire on June 30, 2013.

On January 4, 2012, when the market price of the shares was $36 per share, all options for the 20,000 shares were exercised.The service period is for two years beginning January 1, 2010.Using the fair value method, what should be the amount of compensation expense recorded by Yang Corporation for these options on December 31, 2010?

A)$64,000

B)$32,000

C)$15,000

D)$0

On January 4, 2012, when the market price of the shares was $36 per share, all options for the 20,000 shares were exercised.The service period is for two years beginning January 1, 2010.Using the fair value method, what should be the amount of compensation expense recorded by Yang Corporation for these options on December 31, 2010?

A)$64,000

B)$32,000

C)$15,000

D)$0

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

58

On December 31, 2010, Gonzalez Company granted some of its executives options to purchase 100,000 shares of the company's $10 par ordinary shares at an option price of $50 per share.The Black-Scholes option pricing model determines total compensation expense to be $750,000.The options become exercisable on January 1, 2011, and represent compensation for executives' services over a three-year period beginning January 1, 2011.At December 31, 2011 none of the executives had exercised their options.What is the impact on Gonzalez's net income for the year ended December 31, 2011 as a result of this transaction under the fair value method?

A)$250,000 increase.

B)$750,000 decrease.

C)$250,000 decrease.

D)$0.

A)$250,000 increase.

B)$750,000 decrease.

C)$250,000 decrease.

D)$0.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

59

Use the following information for questions.

On May 1, 2012, Marly Co.issued $500,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable stock warrants entitling the holder to purchase for $40 one share of Marly's ordinary shares $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Marly's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Marly should credit Share Premium-Share Warrants for

A)$20,600

B)$35,000

C)$20,000

D)$15,000

On May 1, 2012, Marly Co.issued $500,000 of 7% bonds at 103, which are due on April 30, 2022.Twenty detachable stock warrants entitling the holder to purchase for $40 one share of Marly's ordinary shares $15 par value, were attached to each $1,000 bond.The bonds without the warrants would sell at 96.On May 1, 2012, the fair value of Marly's shares was $35 per share and of the warrants was $2.

On May 1, 2012, Marly should credit Share Premium-Share Warrants for

A)$20,600

B)$35,000

C)$20,000

D)$15,000

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

60

On January 2, 2012, LexxMark Co.issues 2,000 convertible preference shares that have a par value of €20 per share.The shares were issued at a price of €400 per share.On December 31, 2014, LexxMark Co.repurchases the convertible preference shares for €820,000.On this date, LexxMark will record

A)A loss of €20,000.

B)A credit to Share Premium-Conversion Equity €40,000.

C)A debit to Retained Earnings €20,000.

D)A credit to Share Capital-Preference €40,000.

A)A loss of €20,000.

B)A credit to Share Premium-Conversion Equity €40,000.

C)A debit to Retained Earnings €20,000.

D)A credit to Share Capital-Preference €40,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

61

On January 1, 2011, Evans Company granted Tim Telfer, an employee, an option to buy 1,000 ordinary shares of Evans Co.for $25 per share, the option exercisable for 5 years from date of grant.Using a fair value option pricing model, total compensation expense is determined to be $7,500.Telfer exercised his option on September 1, 2011, and sold his 1,000 shares on December 1, 2011.Quoted market prices of Evans Co.shares during 2011 were

The service period is for three years beginning January 1, 2011.As a result of the option granted to Telfer, using the fair value method, Evans should recognize compensation expense for 2011 on its books in the amount of

A)$9,000.

B)$7,500.

C)$2,500.

D)$1,500.

The service period is for three years beginning January 1, 2011.As a result of the option granted to Telfer, using the fair value method, Evans should recognize compensation expense for 2011 on its books in the amount of

A)$9,000.

B)$7,500.

C)$2,500.

D)$1,500.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

62

On January 1, 2011 (the date of grant), Henrik Co.issues 2,000 shares of restricted shares to its executives.The fair value of these shares is $75,000, and their par value is $10,000.The shares are forfeited if the executives do not complete 3 years of employment with the company.Assuming the service period is three years, how much compensation expense will Henrik Co.record on January 1, 2011?

A)$25,000.

B)$-0-

C)$3,333.

D)$21,667.

A)$25,000.

B)$-0-

C)$3,333.

D)$21,667.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

63

In order to retain certain key executives, Jensen Corporation granted them incentive share options on December 31, 2009.50,000 options were granted at an option price of $35 per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $500,000.What amount of compensation expense should Jensen recognize as a result of this plan for the year ended

December 31, 2010 under the fair value method?

A)$250,000.

B)$500,000.

C)$550,000.

D)$1,750,000.

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $500,000.What amount of compensation expense should Jensen recognize as a result of this plan for the year ended

December 31, 2010 under the fair value method?

A)$250,000.

B)$500,000.

C)$550,000.

D)$1,750,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

64

In order to retain certain key executives, Smiley Corporation granted them incentive share options on December 31, 2009.80,000 options were granted at an option price of $35

Per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $800,000.What amount of compensation expense should Smiley recognize as a result of this plan for the year ended December 31, 2010 under the fair value method?

A)$1,400,000.

B)$880,000.

C)$800,000.

D)$400,000.

Per share.Market prices of the shares were as follows:

The options were granted as compensation for executives' services to be rendered over a two-year period beginning January 1, 2010.The Black-Scholes option pricing model determines total compensation expense to be $800,000.What amount of compensation expense should Smiley recognize as a result of this plan for the year ended December 31, 2010 under the fair value method?

A)$1,400,000.

B)$880,000.

C)$800,000.

D)$400,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

65

On December 31, 2010, Kessler Company granted some of its executives options to purchase 50,000 shares of the company's $10 par ordinary shares at an option price of $50 per share.The options become exercisable on January 1, 2011, and represent compensation for executives' services over a three-year period beginning January 1, 2011.The Black-Scholes option pricing model determines total compensation expense to be $300,000.At December 31, 2011, none of the executives had exercised their options.What is the impact on Kessler's net income for the year ended December 31, 2011 as a result of this transaction under the fair value method?

A)$100,000 increase

B)$0

C)$100,000 decrease

D)$300,000 decrease

A)$100,000 increase

B)$0

C)$100,000 decrease

D)$300,000 decrease

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

66

Anazazi Co.offers all its 10,000 employees the opportunity to participate in an employee share-purchase plan.Under the terms of the plan, the employees are entitled to purchase 100 ordinary shares (par value $1 per share) at a 20 percent discount.The purchase price must be paid immediately upon acceptance of the offer.In total, 8,500 employees accept the offer, and each employee purchases on average 80 shares at $22 share (market price $27.50).Under IFRS, Anazazi Co.will record

A)No compensation since the plan is used to raise capital, not compensate employees.

B)Compensation expense of $5,500,000.

C)Compensation expense of $18,700,000.

D)Compensation expense of $3,740,000.

A)No compensation since the plan is used to raise capital, not compensate employees.

B)Compensation expense of $5,500,000.

C)Compensation expense of $18,700,000.

D)Compensation expense of $3,740,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

67

On June 30, 2008, Norman Corporation granted compensatory share options for 30,000 shares of its $20 par value ordinary shares to certain of its key employees.The market price of the shares on that date was $36 per share and the option price was $30.The Black-Scholes option pricing model determines total compensation expense to be $360,000.The options are exercisable beginning January 1, 2011, provided those key employees are still in Norman's employ at the time the options are exercised.The options expire on June 30, 2012.

On January 4, 2011, when the market price of the shares was $42 per share, all 30,000 options were exercised.What should be the amount of compensation expense recorded by Norman Corporation for the calendar year 2010 using the fair value method?

A)$0.

B)$144,000.

C)$180,000.

D)$360,000.

On January 4, 2011, when the market price of the shares was $42 per share, all 30,000 options were exercised.What should be the amount of compensation expense recorded by Norman Corporation for the calendar year 2010 using the fair value method?

A)$0.

B)$144,000.

C)$180,000.

D)$360,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

68

Weiser Corp.on January 1, 2009, granted share options for 40,000 shares of its $10 par value ordinary shares to its key employees.The market price of the shares on that date was $23 per share and the option price was $20.The Black-Scholes option pricing model determines total compensation expense to be $240,000.The options are exercisable beginning January 1, 2012, provided those key employees are still in Weiser's employ at the time the options are exercised.The options expire on January 1, 2013.

On January 1, 2012, when the market price of the shares was $29 per share, all 40,000 options were exercised.The amount of compensation expense Weiser should record for 2011 under the fair value method is

A)$0.

B)$40,000.

C)$80,000.

D)$120,000.

On January 1, 2012, when the market price of the shares was $29 per share, all 40,000 options were exercised.The amount of compensation expense Weiser should record for 2011 under the fair value method is

A)$0.

B)$40,000.

C)$80,000.

D)$120,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

69

Grant, Inc.had 40,000 treasury shares ($10 par value) at December 31, 2010, which it acquired at $11 per share.On June 4, 2011, Grant issued 20,000 treasury shares to employees who exercised options under Grant's employee share option plan.The fair value per share was $13 at December 31, 2010, $15 at June 4, 2011, and $18 at December 31, 2011.The share options had been granted for $12 per share.The cost method is used.What is the balance of the treasury shares on Grant's statement of financial position at December 31, 2011?

A)$140,000.

B)$180,000.

C)$220,000.

D)$240,000.

A)$140,000.

B)$180,000.

C)$220,000.

D)$240,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

70

On December 31, 2010, Houser Company granted some of its executives options to purchase 45,000 shares of the company's $50 par ordinary shares at an option price of $60 per share.The Black-Scholes option pricing model determines total compensation expense to be $900,000.The options become exercisable on January 1, 2011, and represent compensation for executives' past and future services over a three-year period beginning January 1, 2011.What is the impact on Houser's total equity for the year ended December 31, 2010, as a result of this transaction under the fair value method?

A)$900,000 decrease

B)$300,000 decrease

C)$0

D)$300,000 increase

A)$900,000 decrease

B)$300,000 decrease

C)$0

D)$300,000 increase

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

71

On January 1, 2011, Ritter Company granted share options to officers and key employees for the purchase of 10,000 ordinary shares of the company's $1 par at $20 per share as additional compensation for services to be rendered over the next three years.The options are exercisable during a five-year period beginning January 1, 2014 by grantees still employed by Ritter.The Black-Scholes option pricing model determines total compensation expense to be $90,000.The market price of ordinary shares was $26 per share at the date of grant.The journal entry to record the compensation expense related to these options for 2011 would include a credit to the Share Premium-Share Options account for

A)$0.

B)$18,000.

C)$20,000.

D)$30,000.

A)$0.

B)$18,000.

C)$20,000.

D)$30,000.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 71 flashcards in this deck.