Deck 7: Income From Property

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/9

Play

Full screen (f)

Deck 7: Income From Property

1

Jim Smith owns a rental property which had a UCC of $85,000 at the beginning of 20x0. After all allowable expenses other than CCA, Jim's total rental income was $1,000 in 20x0 and $10,000 in 20x1. Jim always deducts the maximum CCA allowed. What is the UCC for his rental property at the end of 20x1? (The property is a Class 1 building amortized at 4%.)

A) $78,336

B) $80,640

C) $84,000

D) $85,000

A) $78,336

B) $80,640

C) $84,000

D) $85,000

B

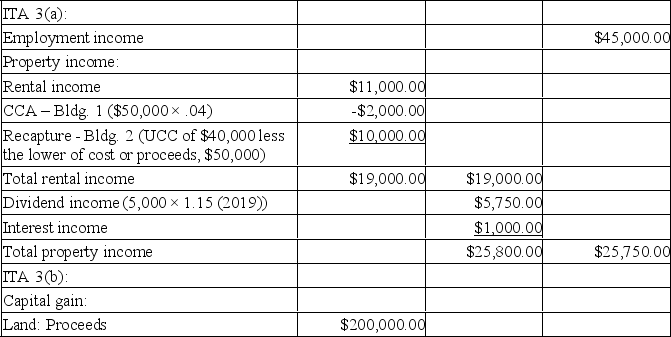

2

Martha Shine has provided you with the following information for 20xx:

She owns rental properties originally valued at $275,000. (Property 1: land $70,000, building $55,000) (Property 2: land $90,000, building $60,000)

The buildings are Class 1 (4%) properties.

-Net rental income before CCA in 20xx was $11,000.

-The UCC on building 1 at the beginning of 20xx was $50,000.

-The UCC on building 2 at the beginning of 20xx was $40,000.

-Property 2 was sold in 20xx for $250,000 (land $200,000, building $50,000)

She owns shares in ABC Inc. (a CCPC) valued at $50,000.

-She received $5,000 in non-eligible dividends on the shares in 20xx.

Martha purchased a 5-year GIC two years ago for $30,000.

-Interest earned in 20xx was $1,000.

Martha worked full-time as a baker in 20xx, earning a gross salary of $45,000.

Martha is in a 45% tax bracket.

Required:

Calculate Martha's net income for tax purposes in 20xx in accordance with Section 3 of the Income Tax Act. Martha will take the maximum CCA allowed this year on her rental properties. (Assume the tax year is 2019.)

She owns rental properties originally valued at $275,000. (Property 1: land $70,000, building $55,000) (Property 2: land $90,000, building $60,000)

The buildings are Class 1 (4%) properties.

-Net rental income before CCA in 20xx was $11,000.

-The UCC on building 1 at the beginning of 20xx was $50,000.

-The UCC on building 2 at the beginning of 20xx was $40,000.

-Property 2 was sold in 20xx for $250,000 (land $200,000, building $50,000)

She owns shares in ABC Inc. (a CCPC) valued at $50,000.

-She received $5,000 in non-eligible dividends on the shares in 20xx.

Martha purchased a 5-year GIC two years ago for $30,000.

-Interest earned in 20xx was $1,000.

Martha worked full-time as a baker in 20xx, earning a gross salary of $45,000.

Martha is in a 45% tax bracket.

Required:

Calculate Martha's net income for tax purposes in 20xx in accordance with Section 3 of the Income Tax Act. Martha will take the maximum CCA allowed this year on her rental properties. (Assume the tax year is 2019.)

3

Which of the following is true concerning dividends?

A) The system to eliminate double taxation assumes that the corporate tax rate is 27.5% when eligible dividends are grossed-up to include 138% of the dividend.

B) Dividends received from a CCPC's business income that is not subject to the small business deduction are typically grossed-up to include 115% of the dividend.

C) Dividends received from a CCPC's business income that is subject to the small business deduction are typically grossed-up to include 138% of the dividend.

D) Eligible dividends require a 115% gross-up.

A) The system to eliminate double taxation assumes that the corporate tax rate is 27.5% when eligible dividends are grossed-up to include 138% of the dividend.

B) Dividends received from a CCPC's business income that is not subject to the small business deduction are typically grossed-up to include 115% of the dividend.

C) Dividends received from a CCPC's business income that is subject to the small business deduction are typically grossed-up to include 138% of the dividend.

D) Eligible dividends require a 115% gross-up.

A

4

Joanne had rental income before CCA of $3,000 in 20x0. The UCC at the beginning of 20x0 was $50,000 (Class 1 - 4%). In 20x1 the rental income before CCA was $1,000. Joanne chose to expense the allowable CCA on her rental property both years. Which of the following statements is true?

A) Joanne has a net rental loss in 20x1 of $920.

B) Joanne has net rental income in 20x1 of $1,000.

C) Joanne has net rental income in 20x1 of $0.

D) Joanne has net rental income in 20x0 of $3,000.

A) Joanne has a net rental loss in 20x1 of $920.

B) Joanne has net rental income in 20x1 of $1,000.

C) Joanne has net rental income in 20x1 of $0.

D) Joanne has net rental income in 20x0 of $3,000.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following statements concerning the tax treatment of interest income is true?

A) Individuals must accrue interest on a daily basis.

B) The anniversary day accrual method of recognizing interest income requires that interest income received by a corporation be recognized for tax purposes for every twelve-month period from the date the investment is made.

C) Foreign interest income and Canadian interest income are recognized under different sets of tax rules.

D) The anniversary day accrual method of recognizing interest income requires that interest income received by an individual be recognized for tax purposes for every twelve-month period from the date the investment is made.

A) Individuals must accrue interest on a daily basis.

B) The anniversary day accrual method of recognizing interest income requires that interest income received by a corporation be recognized for tax purposes for every twelve-month period from the date the investment is made.

C) Foreign interest income and Canadian interest income are recognized under different sets of tax rules.

D) The anniversary day accrual method of recognizing interest income requires that interest income received by an individual be recognized for tax purposes for every twelve-month period from the date the investment is made.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

6

Pear Corporation earned $150,000 of pre-tax income. The tax rate for the company is 13%. The sole shareholder received all of the net earnings in the form of a non-eligible dividend during the year. The shareholder has a personal tax rate of 50%. Supposing the shareholder is entitled to a total (federal + provincial) dividend tax credit equal to $20,000, what is the net personal tax owing on the dividend (ignoring all other tax implications)? (Round all numbers to zero decimal places. Assume the year is 2019.)

A) $19,500

B) $20,000

C) $55,038

D) $75,038

A) $19,500

B) $20,000

C) $55,038

D) $75,038

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

7

Stella Flier has received an inheritance of $100,000. She is trying to decide what to do with this money and has come to you for some advice. She has an excellent credit rating and no outstanding debts. She would like to buy a $225,000 house and invest $100,000 in bonds as a safety net.

Required:

How could Stella minimize her tax liability, assuming only the facts given?

Required:

How could Stella minimize her tax liability, assuming only the facts given?

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

8

A public corporation earns $500,000 in pre-tax profits and pays out all of its after-tax earnings in dividends. The corporate tax rate is 27.5% and the sole shareholder is in a 50% tax bracket. The dividend gross-up rate is 1.38 and the total dividend tax credit (federal and provincial) is 27.5%.

Required:

A) Calculate the tax liability for (1) the corporation and (2) the shareholder.

B) Briefly explain how this tax structure illustrates the theory of integration.

Required:

A) Calculate the tax liability for (1) the corporation and (2) the shareholder.

B) Briefly explain how this tax structure illustrates the theory of integration.

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

9

On March 1, 20x1, Notes Inc. purchased a two-year guaranteed investment certificate (GIC) for $15,000. The interest compounds annually at 8% and will be received at the end of the full term. Notes Inc. has a marginal tax rate of 30%, which will increase to 34% for 20x2 and 20x3. Notes Inc. uses the calendar year as its fiscal year. (These tax rates are used here for illustration purposes only.)

Angela Major also invested $15,000 in a GIC with an 8% annual return, on March 1, 20x1, with interest to be paid at the end of each annual period. Angela's marginal tax rate is 40%.

(Assume there are no leap years in this time period.)

Required:

Calculate the after-tax interest income for each year for Notes Inc. and for Angela. (Round all numbers.)

Angela Major also invested $15,000 in a GIC with an 8% annual return, on March 1, 20x1, with interest to be paid at the end of each annual period. Angela's marginal tax rate is 40%.

(Assume there are no leap years in this time period.)

Required:

Calculate the after-tax interest income for each year for Notes Inc. and for Angela. (Round all numbers.)

Unlock Deck

Unlock for access to all 9 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 9 flashcards in this deck.