Deck 21: Cost Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit.

B) 0.90 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit.

B) 0.90 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

Question

Question

Question

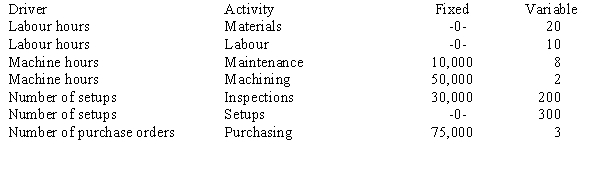

Figure 21-4

Rollo Company has developed cost formulas for the drivers of the following production activities:

Refer to Figure 21-4. The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Rollo Company has developed cost formulas for the drivers of the following production activities:

Refer to Figure 21-4. The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Question

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit.

B) 1.80 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit.

B) 1.80 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

Question

Question

Question

Question

Question

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%.

B) 2.5%.

C) 1.5%.

D) 0%.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%.

B) 2.5%.

C) 1.5%.

D) 0%.

Question

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's defective units as a percentage of total units produced would be

A) 3.16%.

B) 3.00%.

C) 1.67%.

D) 1.50%.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's defective units as a percentage of total units produced would be

A) 3.16%.

B) 3.00%.

C) 1.67%.

D) 1.50%.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Which of the following stages comes first?

A) Introduction

B) Growth

C) Development

D) Decline

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Which of the following stages comes first?

A) Introduction

B) Growth

C) Development

D) Decline

Question

Question

Question

Question

Question

Question

Question

Question

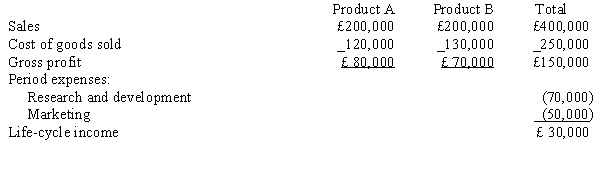

Figure 21-6

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years. A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.

A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.

Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product B would be

A) £35,000.

B) £20,000.

C) £12,000.

D) £7,000.

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years.

A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product B would be

A) £35,000.

B) £20,000.

C) £12,000.

D) £7,000.

Question

Figure 21-6

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years. A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.

Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product A would be

A) £38,000.

B) £27,000.

C) £23,000.

D) £15,000.

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years.

A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product A would be

A) £38,000.

B) £27,000.

C) £23,000.

D) £15,000.

Question

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, external failure costs are what percentage of sales?

A) 1.5350%

B) 1.1875%

C) 1.0000%

D) 0.8350%

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, external failure costs are what percentage of sales?

A) 1.5350%

B) 1.1875%

C) 1.0000%

D) 0.8350%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. If quality costs had been reduced to 2.5 per cent of sales in the current year, profits would have increased by

A) £110,000.

B) £108,400.

C) £103,200.

D) £100,200.

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. If quality costs had been reduced to 2.5 per cent of sales in the current year, profits would have increased by

A) £110,000.

B) £108,400.

C) £103,200.

D) £100,200.

Question

Question

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, prevention costs are what percentage of sales?

A) 9.00%

B) 8.25%

C) 7.00%

D) 2.00%

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, prevention costs are what percentage of sales?

A) 9.00%

B) 8.25%

C) 7.00%

D) 2.00%

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/95

Play

Full screen (f)

Deck 21: Cost Management

1

A time-and-motion study revealed that it should take 2 hours to produce a product that currently takes 6 hours to produce. Labour is £8 per hour. The nonvalue-added costs are

A) £16.

B) £32.

C) £48.

D) £-0-.

A) £16.

B) £32.

C) £48.

D) £-0-.

B

2

Which of the following is NOT a necessary condition for classification as a value-added activity?

A) the activity produces no change of state

B) the change of state was not achievable by preceding activities

C) activity enables other activities to be performed

D) All of the above are necessary conditions.

A) the activity produces no change of state

B) the change of state was not achievable by preceding activities

C) activity enables other activities to be performed

D) All of the above are necessary conditions.

A

3

____ is an effort to reduce costs of existing products and processes.

A) Kaizen costing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Kaizen costing

B) Activity elimination

C) Activity selection

D) Activity reduction

A

4

____ is the process of identifying, describing, and evaluating the activities an organization performs.

A) Activity inputs

B) Activity analysis

C) Cost driver analysis

D) Value-added activities

A) Activity inputs

B) Activity analysis

C) Cost driver analysis

D) Value-added activities

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

5

Figure 21-1

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-1. The value-added costs are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-1. The value-added costs are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is a value-added activity?

A) moving

B) inspection

C) processing

D) waiting

A) moving

B) inspection

C) processing

D) waiting

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

7

____ focuses on nonvalue-added activities.

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following process dimensions of the activity-based management model deals with "why"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is an example of a value-added activity?

A) supervision of production workers

B) inspection of products

C) scheduling of production

D) All are value-added activities.

A) supervision of production workers

B) inspection of products

C) scheduling of production

D) All are value-added activities.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following process dimensions of the activity-based management model deals with "what"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is NOT an expected outcome of activity analysis?

A) What activities are performed?

B) How many people perform the activities?

C) The time and resources required to perform the activities.

D) All of the above are expected outcomes.

A) What activities are performed?

B) How many people perform the activities?

C) The time and resources required to perform the activities.

D) All of the above are expected outcomes.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following process dimensions of the activity-based management model deals with "how well"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is an example of a nonvalue-added manufacturing activity?

A) assembly

B) scheduling

C) finishing

D) All are value-added activities.

A) assembly

B) scheduling

C) finishing

D) All are value-added activities.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

14

Figure 21-2

A company has 20 days of finished goods inventory on hand to avoid stockouts. The carrying costs of the inventory average £5,000 per day.

Refer to Figure 21-2. The nonvalue-added costs are

A) £100,000.

B) £10,000.

C) £5,000.

D) £250.

A company has 20 days of finished goods inventory on hand to avoid stockouts. The carrying costs of the inventory average £5,000 per day.

Refer to Figure 21-2. The nonvalue-added costs are

A) £100,000.

B) £10,000.

C) £5,000.

D) £250.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

15

Figure 21-1

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-1. The nonvalue-added costs for the company are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-1. The nonvalue-added costs for the company are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

16

The major source of information for the activity cost management system is

A) cost driver analysis.

B) an activity- based costing system.

C) a performance measurement system.

D) product information.

A) cost driver analysis.

B) an activity- based costing system.

C) a performance measurement system.

D) product information.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following focuses on the relationship of activity inputs to activity outputs?

A) activity reduction

B) quality

C) time

D) efficiency

A) activity reduction

B) quality

C) time

D) efficiency

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

18

Figure 21-1

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-2. The value-added costs would be

A) £100,000.

B) £10,000.

C) £5,000.

D) £-0-.

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day.

Refer to Figure 21-2. The value-added costs would be

A) £100,000.

B) £10,000.

C) £5,000.

D) £-0-.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is a reason for managerial activity to be considered a value-added activity?

A) It is an enabling resource for operational activities that bring about a change of state.

B) Managing activities brings order by changing the state from uncoordinated activities to coordinated activities.

C) Both are reasons for classifying managerial activities as value-added activity.

D) Neither is a reason for classifying managerial activities as value-added activity.

A) It is an enabling resource for operational activities that bring about a change of state.

B) Managing activities brings order by changing the state from uncoordinated activities to coordinated activities.

C) Both are reasons for classifying managerial activities as value-added activity.

D) Neither is a reason for classifying managerial activities as value-added activity.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

20

____ are those activities necessary to remain in business.

A) Activity inputs

B) Activity outputs

C) Activity drivers

D) Value-added activities

A) Activity inputs

B) Activity outputs

C) Activity drivers

D) Value-added activities

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

21

An activity analysis is used to determine

A) the activities an organization performs.

B) how many people perform activities.

C) the time and resources required to perform activities.

D) all of the above.

A) the activities an organization performs.

B) how many people perform activities.

C) the time and resources required to perform activities.

D) all of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

22

Kaizen costing is

A) continuous improvement with the objective of cost reduction.

B) characterized by constant improvements to existing processes and products.

C) characterized by incremental improvement to existing processes and products.

D) all of the above.

A) continuous improvement with the objective of cost reduction.

B) characterized by constant improvements to existing processes and products.

C) characterized by incremental improvement to existing processes and products.

D) all of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

23

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit.

B) 0.90 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit.

B) 0.90 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

24

Activity-based management attempts to

A) identify and eliminate all unnecessary activities.

B) increase the efficiency of necessary activities.

C) add new activities that increase value.

D) do all of the above.

A) identify and eliminate all unnecessary activities.

B) increase the efficiency of necessary activities.

C) add new activities that increase value.

D) do all of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

25

Product life-cycle costs do NOT include which of the following?

A) development costs

B) production costs

C) costs of logistics support

D) All of the above are life-cycle costs.

A) development costs

B) production costs

C) costs of logistics support

D) All of the above are life-cycle costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

26

Figure 21-4

Rollo Company has developed cost formulas for the drivers of the following production activities:

Refer to Figure 21-4. The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Rollo Company has developed cost formulas for the drivers of the following production activities:

Refer to Figure 21-4. The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

27

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit.

B) 1.80 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit.

B) 1.80 hours per unit.

C) 0.56 hours per unit.

D) 0.50 hours per unit.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

28

Figure 21-3

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year.

Refer to Figure 21-3. The nonvalue-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £0.

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year.

Refer to Figure 21-3. The nonvalue-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £0.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

29

Inspecting the components and the finished product is

A) necessary to assure TQM.

B) a nonvalue-added activity.

C) a value-added activity.

D) none of the above.

A) necessary to assure TQM.

B) a nonvalue-added activity.

C) a value-added activity.

D) none of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

30

A target cost is

A) the standard cost.

B) the difference between the sales price needed to capture a predetermined market share and the desired per-unit profit.

C) the long-run average cost over the life cycle of the product.

D) none of the above.

A) the standard cost.

B) the difference between the sales price needed to capture a predetermined market share and the desired per-unit profit.

C) the long-run average cost over the life cycle of the product.

D) none of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

31

Life-cycle cost management is particularly important for firms that have

A) short life cycles because those firms have less opportunity to take advantage of the time value of money.

B) long life cycles because those firms have more opportunity to take advantage of the time value of money.

C) long life cycles because those firms have more opportunity to enhance profit performance through product redesign or cost reduction.

D) short life cycles because those firms have less opportunity to enhance profit performance through product redesign or cost reduction.

A) short life cycles because those firms have less opportunity to take advantage of the time value of money.

B) long life cycles because those firms have more opportunity to take advantage of the time value of money.

C) long life cycles because those firms have more opportunity to enhance profit performance through product redesign or cost reduction.

D) short life cycles because those firms have less opportunity to enhance profit performance through product redesign or cost reduction.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

32

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%.

B) 2.5%.

C) 1.5%.

D) 0%.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%.

B) 2.5%.

C) 1.5%.

D) 0%.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

33

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's defective units as a percentage of total units produced would be

A) 3.16%.

B) 3.00%.

C) 1.67%.

D) 1.50%.

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 21-5. Sammie's defective units as a percentage of total units produced would be

A) 3.16%.

B) 3.00%.

C) 1.67%.

D) 1.50%.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

34

Figure 21-3

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year.

Refer to Figure 21-3. The value-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £-0-.

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year.

Refer to Figure 21-3. The value-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £-0-.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is not an objective of activity-based management?

A) to improve decision making through better cost information

B) to increase the activity it takes to perform processes

C) to encourage cost reduction through continuous improvement

D) to increase profitability

A) to improve decision making through better cost information

B) to increase the activity it takes to perform processes

C) to encourage cost reduction through continuous improvement

D) to increase profitability

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following describes a kaizen cost reduction process?

A) It has two process cycles, namely, continuous improvement and maintenance.

B) It includes a kaizen standard, which is an ideal standard.

C) A maximum standard is set for future performance based on the current kaizen standard attained.

D) both a and c

A) It has two process cycles, namely, continuous improvement and maintenance.

B) It includes a kaizen standard, which is an ideal standard.

C) A maximum standard is set for future performance based on the current kaizen standard attained.

D) both a and c

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

37

Reengineering is another name for

A) product innovation.

B) process innovation.

C) process improvement.

D) product improvement.

A) product innovation.

B) process innovation.

C) process improvement.

D) product improvement.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

38

A technique for improving performance of activities and processes that searches for best practices is called

A) value-added reporting.

B) kaizen costing.

C) trend reporting.

D) benchmarking.

A) value-added reporting.

B) kaizen costing.

C) trend reporting.

D) benchmarking.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

39

In a continuous improvement environment, waste includes

A) inventories.

B) rework.

C) setup time.

D) all of the above.

A) inventories.

B) rework.

C) setup time.

D) all of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

40

Benchmarking

A) is an approach to standard setting that is used to identify opportunities for activity improvement.

B) uses best practices as the standard for evaluating activity performance.

C) Both a and b are correct.

D) Neither a nor b is correct.

A) is an approach to standard setting that is used to identify opportunities for activity improvement.

B) uses best practices as the standard for evaluating activity performance.

C) Both a and b are correct.

D) Neither a nor b is correct.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

41

The just-in-time (JIT) approach to inventory management

A) allows greater flexibility as to when products can be manufactured.

B) results in higher inventory levels but reduces ordering and setup costs.

C) results in lower inventory carrying costs.

D) None of the above are correct.

A) allows greater flexibility as to when products can be manufactured.

B) results in higher inventory levels but reduces ordering and setup costs.

C) results in lower inventory carrying costs.

D) None of the above are correct.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following is NOT a detection activity?

A) inspecting products and processes

B) developing environmental performance measures

C) testing for contamination

D) operating pollution control equipment

A) inspecting products and processes

B) developing environmental performance measures

C) testing for contamination

D) operating pollution control equipment

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

43

The Kanban system controls inventory through the use of

A) electronic data interchange.

B) markers or cards.

C) rigid control of safety stock.

D) reengineering the production process.

A) electronic data interchange.

B) markers or cards.

C) rigid control of safety stock.

D) reengineering the production process.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

44

With JIT manufacturing, the major variable cost remaining is

A) direct materials.

B) overhead.

C) inventory.

D) direct labour.

A) direct materials.

B) overhead.

C) inventory.

D) direct labour.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

45

JIT reduces lead times to meet delivery dates by

A) reducing setup times.

B) expediting delivery to customers.

C) having more inventory available.

D) working overtime to fill orders.

A) reducing setup times.

B) expediting delivery to customers.

C) having more inventory available.

D) working overtime to fill orders.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

46

The Kanban system is used to

A) ensure parts or materials are available when needed.

B) signal when preventive maintenance is needed.

C) signal when a defective unit has been produced.

D) ensure idle time of workers is not wasted.

A) ensure parts or materials are available when needed.

B) signal when preventive maintenance is needed.

C) signal when a defective unit has been produced.

D) ensure idle time of workers is not wasted.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

47

____ are costs of activities performed because contaminants and waste have been produced but not discharged into the environment.

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external costs

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external costs

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

48

JIT avoids shutdowns due to materials shortages in all of the following ways EXCEPT

A) using total preventive maintenance.

B) holding inventory.

C) using total quality control to reduce defective materials.

D) working with suppliers to ensure the availability of materials.

A) using total preventive maintenance.

B) holding inventory.

C) using total quality control to reduce defective materials.

D) working with suppliers to ensure the availability of materials.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

49

____ are the costs of activities executed to determine if products, processes, and other activities within the firm are in compliance with appropriate environmental standards.

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external costs

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external costs

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

50

The majority of the product cost is "locked in" during which of the following life-cycle stages?

A) Introduction

B) Growth

C) Development

D) Decline

A) Introduction

B) Growth

C) Development

D) Decline

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

51

In comparison to a traditional environment, a JIT environment has more overhead assigned by

A) direct tracing.

B) driver tracing.

C) allocation.

D) Overhead assignment is the same between traditional and JIT.

A) direct tracing.

B) driver tracing.

C) allocation.

D) Overhead assignment is the same between traditional and JIT.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following is NOT a prevention activity?

A) evaluating and selecting supplies

B) evaluating and selecting pollution control equipment

C) auditing environmental activities

D) designing processes

A) evaluating and selecting supplies

B) evaluating and selecting pollution control equipment

C) auditing environmental activities

D) designing processes

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

53

Under JIT, the number and magnitude of direct fixed costs

A) decreases.

B) increases.

C) stays the same.

D) are eliminated.

A) decreases.

B) increases.

C) stays the same.

D) are eliminated.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

54

A withdrawal Kanban specifies

A) how much should be produced to replace inventory.

B) the quantity that a subsequent process should withdraw from the preceding process.

C) when customers should be notified to pick up orders.

D) when suppliers should be notified to deliver more parts.

A) how much should be produced to replace inventory.

B) the quantity that a subsequent process should withdraw from the preceding process.

C) when customers should be notified to pick up orders.

D) when suppliers should be notified to deliver more parts.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

55

Figure 21-5

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Which of the following stages comes first?

A) Introduction

B) Growth

C) Development

D) Decline

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Which of the following stages comes first?

A) Introduction

B) Growth

C) Development

D) Decline

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is TRUE about a manufacturing cell?

A) There is increased movement of work in process.

B) It usually produces a particular product or product family.

C) Workers are highly specialized.

D) Supervision is important.

A) There is increased movement of work in process.

B) It usually produces a particular product or product family.

C) Workers are highly specialized.

D) Supervision is important.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

57

The demand-pull system requires goods to be manufactured based on the

A) current demand.

B) anticipated demand.

C) previous year's demand.

D) average of the next five years' demand.

A) current demand.

B) anticipated demand.

C) previous year's demand.

D) average of the next five years' demand.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

58

____ are the costs of activities performed after discharging contaminants and waste into the environment.

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external failure costs

A) Environmental prevention costs

B) Environmental detection costs

C) Environmental internal failure costs

D) Environmental external failure costs

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

59

Cell workers have responsibility over

A) multiple tasks within the cell.

B) providing input for continuous improvement.

C) support activities within the cell.

D) all of the above.

A) multiple tasks within the cell.

B) providing input for continuous improvement.

C) support activities within the cell.

D) all of the above.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

60

How can JIT avoid shutdowns?

A) increase in defective inventory

B) increase in the number of workers

C) preventive maintenance

D) short-term contracts with suppliers

A) increase in defective inventory

B) increase in the number of workers

C) preventive maintenance

D) short-term contracts with suppliers

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

61

The costs of a consumer complaint department are

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is NOT an internal failure activity?

A) treating and disposing of toxic waste

B) maintaining pollution equipment

C) licensing facilities for producing contaminants

D) cleaning up a polluted lake

A) treating and disposing of toxic waste

B) maintaining pollution equipment

C) licensing facilities for producing contaminants

D) cleaning up a polluted lake

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

63

Figure 21-6

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years. A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.

Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product B would be

A) £35,000.

B) £20,000.

C) £12,000.

D) £7,000.

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years.

A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product B would be

A) £35,000.

B) £20,000.

C) £12,000.

D) £7,000.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

64

Figure 21-6

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years. A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.

Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product A would be

A) £38,000.

B) £27,000.

C) £23,000.

D) £15,000.

Brad Company developed the following budgeted life-cycle income statement for two proposed products. Each product's life cycle is expected to be two years.

A 10 per cent return on sales is required for new products. Because the proposed products did not have a 10 per cent return on sales, the products were going to be dropped.Relative to Product B, Product A requires more research and development costs but fewer resources to market the product. Sixty per cent of the research and development costs are traceable to Product A, and 30 per cent of the marketing costs are traceable to Product A.

Refer to Figure 21-6. If research and development costs and marketing costs are traced to each product, life-cycle income for Product A would be

A) £38,000.

B) £27,000.

C) £23,000.

D) £15,000.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

65

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, external failure costs are what percentage of sales?

A) 1.5350%

B) 1.1875%

C) 1.0000%

D) 0.8350%

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, external failure costs are what percentage of sales?

A) 1.5350%

B) 1.1875%

C) 1.0000%

D) 0.8350%

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

66

Lower sales due to poor product performance is an example of

A) external failure costs.

B) an internal failure cost.

C) an appraisal cost.

D) a prevention cost.

A) external failure costs.

B) an internal failure cost.

C) an appraisal cost.

D) a prevention cost.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is NOT an external failure activity?

A) obtaining ISO 14001 certification

B) cleaning up oil spills

C) cleaning up contaminated soil

D) settling personal injury claims (environmentally related)

A) obtaining ISO 14001 certification

B) cleaning up oil spills

C) cleaning up contaminated soil

D) settling personal injury claims (environmentally related)

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

68

Product recalls are

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

69

In the zero-defects view of quality,

A) control costs do not increase without limit.

B) control costs initially increase and then decrease as the firm approaches the robust start.

C) failure costs can be driven to zero.

D) all of the above are true.

A) control costs do not increase without limit.

B) control costs initially increase and then decrease as the firm approaches the robust start.

C) failure costs can be driven to zero.

D) all of the above are true.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

70

Over the LONG-TERM, prevention costs are expected to

A) decrease as failure costs decrease.

B) increase as failure costs increase.

C) increase as failure costs decrease.

D) decrease as failure costs increase.

A) decrease as failure costs decrease.

B) increase as failure costs increase.

C) increase as failure costs decrease.

D) decrease as failure costs increase.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

71

Costs incurred to determine whether products and services are conforming to requirements are called

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

72

Inspection labour costs are

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

73

Costs incurred because products or services fail to meet requirements after delivery to customers are called

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

74

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. If quality costs had been reduced to 2.5 per cent of sales in the current year, profits would have increased by

A) £110,000.

B) £108,400.

C) £103,200.

D) £100,200.

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. If quality costs had been reduced to 2.5 per cent of sales in the current year, profits would have increased by

A) £110,000.

B) £108,400.

C) £103,200.

D) £100,200.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

75

Downtime attributed to quality problems is a(n)

A) external failure cost.

B) internal failure cost.

C) appraisal cost.

D) prevention cost.

A) external failure cost.

B) internal failure cost.

C) appraisal cost.

D) prevention cost.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

76

Figure 21-7

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, prevention costs are what percentage of sales?

A) 9.00%

B) 8.25%

C) 7.00%

D) 2.00%

At the beginning of the year, Andrew Company initiated a quality improvement program. The program was successful in reducing scrap and rework costs. To help assess the impact of the quality improvement program, the following data were collected for the current and preceding years:

Refer to Figure 21-7. For the current year, prevention costs are what percentage of sales?

A) 9.00%

B) 8.25%

C) 7.00%

D) 2.00%

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

77

Costs incurred because products or services fail to meet requirements after delivery to customers are called

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

A) external failure costs.

B) internal failure costs.

C) appraisal costs.

D) prevention costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

78

Quality training programs are

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

A) prevention costs.

B) appraisal costs.

C) internal failure costs.

D) external failure costs.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

79

Labour and overhead incurred for rework of defective products is a(n)

A) prevention cost.

B) appraisal cost.

C) internal failure cost.

D) external failure cost.

A) prevention cost.

B) appraisal cost.

C) internal failure cost.

D) external failure cost.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

80

Warranty work is a(n)

A) prevention cost.

B) appraisal cost.

C) internal failure cost.

D) external failure cost.

A) prevention cost.

B) appraisal cost.

C) internal failure cost.

D) external failure cost.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 95 flashcards in this deck.