Deck 10: Pensions and Other Fiduciary Activities

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

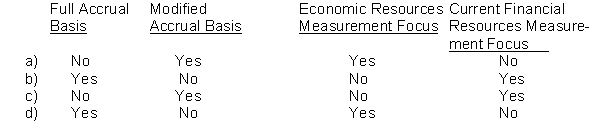

The liabilities related to benefits and refunds of a defined benefit pension plan are reported in a government's fiduciary fund financial statements using the

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Briana City provides a defined benefit pension plan for its full-time employees. The city includes the plan as a pension trust fund in its fund financial statements.

REQUIRED:

Using the information below, prepare a statement of fiduciary net position and a statement of changes in fiduciary net position for the pension trust fund.

REQUIRED:

Using the information below, prepare a statement of fiduciary net position and a statement of changes in fiduciary net position for the pension trust fund.

Question

Question

Question

The statement of fiduciary net position for a school district's defined benefit pension plan shows the following (in condensed form and in thousands)

A. The plan has been in operation for over 20 years and covers all school district employees. What is the most reasonable explanation of why the benefits payable to current employees and retirees is so small relative to plan assets?

The plan has been in operation for over 20 years and covers all school district employees. What is the most reasonable explanation of why the benefits payable to current employees and retirees is so small relative to plan assets?

B. Suppose that in the current year the school district's annual required contribution was $6,300,000. In the past, the district has always paid the annual required contribution in full. However, in the current year the district budgeted and paid into the pension trust fund only $5,000,000.

1. Prepare the journal entry that the district (not the plan) should make to record the year's pension contribution. You need not make budgetary or closing entries. The plan is accounted for in a governmental fund.

2. Prepare the journal entry to record the year's pension contribution for reporting in the district's government-wide statements.

C. The district's annual financial report indicated that its "normal cost" was $530,000 and that the "amortization of the unfunded actuarial accrued liability" was $100,000.

1. What is meant by "normal cost?"

2. What is meant by "unfunded actuarial accrued liability"? What are its principal causes? Why must it be amortized?

A.

The plan has been in operation for over 20 years and covers all school district employees. What is the most reasonable explanation of why the benefits payable to current employees and retirees is so small relative to plan assets?B. Suppose that in the current year the school district's annual required contribution was $6,300,000. In the past, the district has always paid the annual required contribution in full. However, in the current year the district budgeted and paid into the pension trust fund only $5,000,000.

1. Prepare the journal entry that the district (not the plan) should make to record the year's pension contribution. You need not make budgetary or closing entries. The plan is accounted for in a governmental fund.

2. Prepare the journal entry to record the year's pension contribution for reporting in the district's government-wide statements.

C. The district's annual financial report indicated that its "normal cost" was $530,000 and that the "amortization of the unfunded actuarial accrued liability" was $100,000.

1. What is meant by "normal cost?"

2. What is meant by "unfunded actuarial accrued liability"? What are its principal causes? Why must it be amortized?

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/74

Play

Full screen (f)

Deck 10: Pensions and Other Fiduciary Activities

1

Fiduciary funds focus on current financial resources and use the modified accrual basis of accounting.

False

2

Carl City received $200,000 to help maintain a local art museum that is owned and operated by a not-for-profit organization. During the year the city transferred net earnings of $20,000 to the appropriate entity/fund.

-The $200,000 gift would be reported in a (an):

A) Special revenue fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

-The $200,000 gift would be reported in a (an):

A) Special revenue fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

Private-purpose trust fund.

3

An employer may have a liability to a defined benefit pension plan other than for its annual required contributions, depending on the future financial health of the plan.

True

4

Employers that provide postemployment healthcare benefit plans should account for them in private-purpose trust funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

5

In an agency fund, assets always equal fund balances because there are no liabilities.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

6

Accounting for the employer's contribution to a defined benefit pension plan is straight forward, because the employer is obligated only to make annual contributions in the amount specified in the plan terms.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

7

In the current year, Loma City earned $24,000 on the principal of a private-purpose trust fund but disbursed only $20,000.

-During the current year the private-purpose trust fund will recognize, related to earnings:

A) $24,000 revenues.

B) $20,000 revenues.

C) $24,000 addition to net position.

D) $20,000 addition to net position.

-During the current year the private-purpose trust fund will recognize, related to earnings:

A) $24,000 revenues.

B) $20,000 revenues.

C) $24,000 addition to net position.

D) $20,000 addition to net position.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

8

In contrast to most private-sector pension plans, most government plans are defined contribution plans.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

9

A government receives a gift of cash and investments with a fair value of $200,000. The donor specified that the earnings from the gift must be used to beautify city-owned parks and the principal must be re-invested. The $200,000 gift should be accounted for in which of the following funds?

A) General fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

A) General fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

10

Pension and OEB trust funds, custodial funds and internal service funds are examples of fiduciary funds

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

11

In accounting for permanent funds only the income can be spent; the principal must be preserved intact.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

12

Accounting for the employer's contribution to a defined contribution pension plan is straight forward, because the employer is obligated only to make annual contributions in the amount specified in the plan terms.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

13

Per GASB Statement No. 34, permanent funds are classified as fiduciary funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

14

Permanent funds focus on measuring current financial resources and use a modified accrual basis of accounting.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

15

In previous years, Boze City had received a $400,000 gift of cash and investments. The donor had specified that the earnings from the gift must be used to beautify city-owned parks and the principal must be re-invested. During the current year, the earnings from this gift were $24,000. The earnings from this gift should generally be considered revenue to which of the following funds?

A) Special revenue fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

A) Special revenue fund.

B) Private-purpose trust fund.

C) Agency fund.

D) Permanent fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

16

The concept of major versus nonmajor funds does not apply to permanent funds, as it does to governmental and proprietary funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

17

Colleges that use a fixed rate of return approach to manage the distribution of income from their endowments must apply the same rate to determine how much investment income to report in their financial statements.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

18

Carl City received $200,000 to help maintain a local art museum that is owned and operated by a not-for-profit organization. During the year the city transferred net earnings of $20,000 to the appropriate entity/fund.

-The $20,000 transfer would be reported by the fund that made the transfer as a (an)

A) Transfer-out.

B) Expenditure.

C) Deduction from net position-benefits.

D) Expense.

-The $20,000 transfer would be reported by the fund that made the transfer as a (an)

A) Transfer-out.

B) Expenditure.

C) Deduction from net position-benefits.

D) Expense.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

19

GASB standards require a defined benefit pension plan to report investments at fair market value even if the plan's actuary uses a different value in determining the employer's contribution requirements.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

20

Fiduciary funds are excluded from the government-wide financial statements.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following would NOT be accounted for in a fiduciary fund of a government?

A) Nonexpendable resources held for the benefit of other governments.

B) Nonexpendable resources held for the benefit of the government holding the resources.

C) Expendable resources held for the benefit of other governments.

D) Funds held as an agent for other entities.

A) Nonexpendable resources held for the benefit of other governments.

B) Nonexpendable resources held for the benefit of the government holding the resources.

C) Expendable resources held for the benefit of other governments.

D) Funds held as an agent for other entities.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

22

During the year, a state-owned university received a $5 million gift. The donor specified that the principal of the gift must be held intact for 3 years, but the earnings from the gift can be used to support technology improvements in the college of business. At the end of the 3 years, the donor together with the university president and the college dean will decide how the $5 million gift can be used. The university will report the gift in what type of fund?

A) Permanent fund.

B) Private-purpose trust fund.

C) Plant fund.

D) Special revenue fund

A) Permanent fund.

B) Private-purpose trust fund.

C) Plant fund.

D) Special revenue fund

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

23

Previously a local private-sector charity received a $1 million gift, the income from which was restricted to support activities for senior citizens. During the current year the endowment earned $40,000 of interest revenues, of which the charity designated $30,000 to support senior citizen activities.

-On its year-end statement of financial position, the charity would report restricted net assets of:

A) $1 million.

B) $1.04 million.

C) $1.03 million.

D) $1.01 million.

-On its year-end statement of financial position, the charity would report restricted net assets of:

A) $1 million.

B) $1.04 million.

C) $1.03 million.

D) $1.01 million.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

24

Previously a local private-sector charity received a $1 million gift, the income from which was restricted to support activities for senior citizens. During the current year the endowment earned $40,000 of interest revenues, of which the charity designated $30,000 to support senior citizen activities.

-On its year-end statement of activities, the charity would report interest revenues of:

A) $0

B) $30,000

C) $40,000

D) None of the above.

-On its year-end statement of activities, the charity would report interest revenues of:

A) $0

B) $30,000

C) $40,000

D) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

25

Permanent funds are classified as

A) Governmental funds.

B) Proprietary funds.

C) Fiduciary funds.

D) Trust funds.

A) Governmental funds.

B) Proprietary funds.

C) Fiduciary funds.

D) Trust funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

26

A defined contribution pension plan is one in which the employer agrees to do which of the following?

A) To make payments to a specified pension plan with no guarantee of a specific pension amount to be paid to the employees.

B) To make actuarially determined payments to a pension plan AND to guarantee that the employees will receive a specified pension benefit (usually determined by length of service and salary).

C) To make actuarially determined payments to a pension plan that guarantees employees will receive a specified pension (usually determined by length of service and salary).

C) To pay specified amounts (usually determined by length of service and salary) to the employees upon retirement.

A) To make payments to a specified pension plan with no guarantee of a specific pension amount to be paid to the employees.

B) To make actuarially determined payments to a pension plan AND to guarantee that the employees will receive a specified pension benefit (usually determined by length of service and salary).

C) To make actuarially determined payments to a pension plan that guarantees employees will receive a specified pension (usually determined by length of service and salary).

C) To pay specified amounts (usually determined by length of service and salary) to the employees upon retirement.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

27

In which of the following funds would the account "net pension obligation" be most likely to appear?

A) General fund.

B) Enterprise fund.

C) Private-purpose trust fund.

D) Agency fund.

A) General fund.

B) Enterprise fund.

C) Private-purpose trust fund.

D) Agency fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

28

In the current year, Loma City earned $24,000 on the principal of a private-purpose trust fund but disbursed only $20,000.

-During the current year the private-purpose trust fund will recognize, related to the cash outflow:

A) $20,000 transfer-out.

B) $20,000 expenses.

C) $24,000 deduction from net position.

D) $20,000 deduction from net position.

-During the current year the private-purpose trust fund will recognize, related to the cash outflow:

A) $20,000 transfer-out.

B) $20,000 expenses.

C) $24,000 deduction from net position.

D) $20,000 deduction from net position.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

29

A wealthy citizen provided in her will for a gift of cash and other assets to Balsa City. The will specified that the gift was to be kept intact and that the earnings from the gift were to be used to support public parks. At the time of the donation, the gift had a book value in the hands of the donor of $300,000 and a fair value of $500,000. When recording this gift the city would credit

A) Contributions revenues $500,000.

B) Other financing sources-contributions $500,000.

C) Contributions revenues $300,000.

D) Other financing sources-contributions $300,000.

A) Contributions revenues $500,000.

B) Other financing sources-contributions $500,000.

C) Contributions revenues $300,000.

D) Other financing sources-contributions $300,000.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following activities of a government should be accounted for in a fiduciary fund?

A) Funds received from the federal government to support public transportation activities.

B) Funds received from an individual who specified that the principal must be kept intact but the income can be used to support families of police officers killed in the line of duty.

C) Funds received from the state government that must be used to purchase capital assets.

D) Funds received from a contractor to assist with the development of utility infrastructure.

A) Funds received from the federal government to support public transportation activities.

B) Funds received from an individual who specified that the principal must be kept intact but the income can be used to support families of police officers killed in the line of duty.

C) Funds received from the state government that must be used to purchase capital assets.

D) Funds received from a contractor to assist with the development of utility infrastructure.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

31

What basis of accounting is used to account for the transactions of a government's permanent fund?

A) Full accrual basis of accounting.

B) Modified accrual basis of accounting.

C) Cash basis of accounting.

D) Budgetary basis of accounting.

A) Full accrual basis of accounting.

B) Modified accrual basis of accounting.

C) Cash basis of accounting.

D) Budgetary basis of accounting.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

32

Dale City Light & Water (a proprietary fund) contributes to a defined benefit pension plan for its employees. During 2017, the city contributed $36 million to the pension plan. The city also made a $4 million contribution related to 2016. The actuarially determined contribution requirement for 2017 was $43 million. The amount of pension expense recognized by Dale City Light & Water for 2017 should be:

A) $ 0

B) $ 36 million

C) $ 40 million

D) $ 43 million

A) $ 0

B) $ 36 million

C) $ 40 million

D) $ 43 million

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

33

At the beginning of the year, the permanent fund of Rose City had an investment portfolio with a historical cost of $300,000 and a fair value of $330,000. There were no purchases or sales of securities during the year. At the end of the year the portfolio had a fair value of $360,000. At year-end, the city s account for this increase in fair value in which of the following ways?

A) Credit Investment income, $30,000.

B) Credit Investment income, $60,000.

C) Credit Fund balance, $30,000.

D) No entry should be made to recognize an increase in fair value.

A) Credit Investment income, $30,000.

B) Credit Investment income, $60,000.

C) Credit Fund balance, $30,000.

D) No entry should be made to recognize an increase in fair value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

34

What basis of accounting is used to account for transactions of a government's private-purpose trust fund?

A) Full accrual basis of accounting.

B) Modified accrual basis of accounting.

C) Cash basis of accounting.

D) Budgetary basis of accounting.

A) Full accrual basis of accounting.

B) Modified accrual basis of accounting.

C) Cash basis of accounting.

D) Budgetary basis of accounting.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

35

In which of the following funds would a government report depreciation expense?

A) Private-purpose trust fund.

B) Agency fund.

C) Permanent fund.

D) None of the above

A) Private-purpose trust fund.

B) Agency fund.

C) Permanent fund.

D) None of the above

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

36

Several years ago, a donor gave $5 million to Denton City and specified that the principal was to be kept intact but the earnings were to be used to support the operations of city parks. During the current year, the city earned $300,000 on the gift. To what type of fund, should the city transfer the $300,000 earnings?

A) It should not make any transfers. The $300,000 should remain in the city's permanent fund.

B) A special revenue fund.

C) The general fund.

D) An enterprise fund.

A) It should not make any transfers. The $300,000 should remain in the city's permanent fund.

B) A special revenue fund.

C) The general fund.

D) An enterprise fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

37

Maple City has a permanent fund that reported current-year investment earnings (realized and unrealized) of $80,000. The endowment principal is $800,000 and the city council has adopted a policy of considering only the inflation-adjusted rate of return to be available for transfer to the recipient fund. During the current year the council declared the inflation-adjusted rate of return to be 8 percent. How much revenue would be recognized in the permanent fund?

A) $ 0.

B) $ 64,000.

C) $ 80,000.

D) Insufficient information to determine.

A) $ 0.

B) $ 64,000.

C) $ 80,000.

D) Insufficient information to determine.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

38

Previously a local private-sector charity received a $1 million gift, the income from which was restricted to support activities for senior citizens. During the current year the endowment earned $40,000 of interest revenues, of which the charity designated $30,000 to support senior citizen activities.

-On its year-end statement of financial position, the charity would report non restricted net assets of:

A) $40,000.

B) $ 0.

C) $30,000.

D) $1.04 million.

-On its year-end statement of financial position, the charity would report non restricted net assets of:

A) $40,000.

B) $ 0.

C) $30,000.

D) $1.04 million.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

39

During the fiscal year ended December 31, 2016, Glen City's general fund contributed $60 million to a defined benefit pension plan for city employees. On February 27, 2017, the general fund made an additional $3 million contribution related to the 2016 pension contribution requirements. The actuarially determined contribution requirement for 2016 is $65 million. The amount of pension expenditure recognized by the general fund for 2016 should be:

A) $ 0

B) $ 60 million

C) $ 63 million

D) $ 65 million

A) $ 0

B) $ 60 million

C) $ 63 million

D) $ 65 million

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is NOT a fiduciary fund?

A) Pension trust fund.

B) Investment trust fund.

C) Permanent fund.

D) Private-purpose trust fund.

A) Pension trust fund.

B) Investment trust fund.

C) Permanent fund.

D) Private-purpose trust fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

41

The fiduciary fund financial statements in a government's annual financial report comprise

A) Consolidated statements only--no separate statements for individual pension plans.

B) A separate column in each statement for each fiduciary fund type.

C) A consolidated assets and benefits statement showing three classes of net assets.

D) Statements reporting information by major fund.

A) Consolidated statements only--no separate statements for individual pension plans.

B) A separate column in each statement for each fiduciary fund type.

C) A consolidated assets and benefits statement showing three classes of net assets.

D) Statements reporting information by major fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

42

The funded status of a defined benefit pension plan is

A) The result of comparing the actuarial value of plan assets with the plan's actuarial accrued liability for benefits.

B) The amount by which plan assets exceed benefits due to current retirees.

C) Current-year contributions less amounts currently due but not paid to current retirees,

D) The policy as to whether the plan is being financed on a pay-as-you-go (cash) basis or through actuarially determined employer contributions.

A) The result of comparing the actuarial value of plan assets with the plan's actuarial accrued liability for benefits.

B) The amount by which plan assets exceed benefits due to current retirees.

C) Current-year contributions less amounts currently due but not paid to current retirees,

D) The policy as to whether the plan is being financed on a pay-as-you-go (cash) basis or through actuarially determined employer contributions.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

43

A plan's unfunded actuarially accrued liability is the excess of the:

A) Actuarially determined plan cost over the actual contribution.

B) Actuarially determined plan cost over the plan assets.

C) Actuarially determined pension liability over the plan assets.

D) Actuarially determined pension liability over the total contributions

A) Actuarially determined plan cost over the actual contribution.

B) Actuarially determined plan cost over the plan assets.

C) Actuarially determined pension liability over the plan assets.

D) Actuarially determined pension liability over the total contributions

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

44

GASB standards of accounting for other postemployment benefits (OPEB) require that governments

A) Fund their OPEB benefits on an actuarially determined basis.

B) Report actuarially determined required contributions as OPEB expense, regardless of whether the government actually makes the contributions.

C) Report OPEB costs in accordance with the FASB's standards of accounting for OPEB.

D) Only disclose an estimate of their OPEB liabilities.

A) Fund their OPEB benefits on an actuarially determined basis.

B) Report actuarially determined required contributions as OPEB expense, regardless of whether the government actually makes the contributions.

C) Report OPEB costs in accordance with the FASB's standards of accounting for OPEB.

D) Only disclose an estimate of their OPEB liabilities.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

45

A major difference between defined benefit pension plans and defined contribution pension plans is that

A) In defined benefit plans, the risk of loss is borne primarily by the employer.

B) Accounting for defined benefit plans is much simpler than accounting for defined contribution plans.

C) Employees generally are required to contribute to defined contribution plans but not to defined benefit plans.

D) There is no major difference between the two kinds of pension plans.

A) In defined benefit plans, the risk of loss is borne primarily by the employer.

B) Accounting for defined benefit plans is much simpler than accounting for defined contribution plans.

C) Employees generally are required to contribute to defined contribution plans but not to defined benefit plans.

D) There is no major difference between the two kinds of pension plans.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

46

The liabilities related to benefits and refunds of a defined benefit pension plan are reported in a government's fiduciary fund financial statements using the

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

47

Required disclosure by the general fund of a government related to its pension plan does NOT include which of the following?

A) The employer's funding policy.

B) The components of the pension cost.

C) The key assumptions used in determining the pension cost.

D) The present value of the future benefits to be paid.

A) The employer's funding policy.

B) The components of the pension cost.

C) The key assumptions used in determining the pension cost.

D) The present value of the future benefits to be paid.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

48

The schedule of changes in long-term obligations contains an account "net pension obligation." Which of the following describes the event that gave rise to this account?

A) The actual contribution by a proprietary fund was less than the annual required contribution per the actuary.

B) The actual contribution by a governmental fund was less than the annual required contribution per the actuary.

C) The actuarially computed pension liability exceeded the pension plan assets.

D) The actuarially computed pension liability was less than the pension plan assets.

A) The actual contribution by a proprietary fund was less than the annual required contribution per the actuary.

B) The actual contribution by a governmental fund was less than the annual required contribution per the actuary.

C) The actuarially computed pension liability exceeded the pension plan assets.

D) The actuarially computed pension liability was less than the pension plan assets.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

49

Ashby City receives a federal grant to assist in nutrition programs for its senior citizens. Senior citizens whose income is below a specified amount (the amount was specified by the Federal government) are eligible to participate in the program. Monthly checks of $100 (this amount was specified by the Federal government) will be mailed to eligible senior citizens. The proceeds of this grant should be accounted for in which of the following funds of the city?

A) General fund.

B) Special revenue fund.

C) Agency fund.

D) Private-purpose trust fund.

A) General fund.

B) Special revenue fund.

C) Agency fund.

D) Private-purpose trust fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

50

Citizens within a defined geographic area of Dolan City created a special assessment district to facilitate the construction of sidewalks. The city was responsible for overseeing the entire construction project. The city issued bonds in its own name to pay the contractor for the construction. However, the city was not responsible in any manner for the bonds. The bonds were secured by the special assessments that are levied against properties within the special assessment district. Collections of special assessments would be recorded in which of the following funds of Dolan City?

A) Special assessment fund.

B) Agency fund.

C) Special revenue fund.

D) Debt service fund.

A) Special assessment fund.

B) Agency fund.

C) Special revenue fund.

D) Debt service fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

51

The primary financial statements for a government-sponsored pension plan are:

A) Balance sheet and statement of activities.

B) Balance sheet, statement of activities, and cash flows statement.

C) Statement of fiduciary net assets and a statement of changes in fiduciary net assets

D) Balance sheet, statement of activities, cash flows statement, and statement of funding progress.

A) Balance sheet and statement of activities.

B) Balance sheet, statement of activities, and cash flows statement.

C) Statement of fiduciary net assets and a statement of changes in fiduciary net assets

D) Balance sheet, statement of activities, cash flows statement, and statement of funding progress.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

52

Whether gains on the sale of a government endowment's investments should be considered additions to principal or expendable income for accounting purposes is:

A) An issue that has been resolved by federal law.

B) Debatable, but generally resolved in favor of adding the gains to unrestricted assets (expendable), absent donor or legal stipulations.

C) A matter for governments to decide, independent of donor or legal considerations.

D) Debatable, but generally resolved in favor of adding the gains to principal (nonexpendable assets), absent donor or legal stipulations.

A) An issue that has been resolved by federal law.

B) Debatable, but generally resolved in favor of adding the gains to unrestricted assets (expendable), absent donor or legal stipulations.

C) A matter for governments to decide, independent of donor or legal considerations.

D) Debatable, but generally resolved in favor of adding the gains to principal (nonexpendable assets), absent donor or legal stipulations.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

53

Lomond City receives a federal grant to assist in nutrition programs for its senior citizens. The city will select the contractors that will provide meals and approve the participants in the program. The proceeds of this grant should be accounted for in which of the following funds of the city?

A) A governmental fund.

B) An enterprise fund.

C) An agency fund.

D) A private-purpose trust fund.

A) A governmental fund.

B) An enterprise fund.

C) An agency fund.

D) A private-purpose trust fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

54

Assets reported in a government's investment trust fund should include:

A) Only investments owned by external participants in the investment pool.

B) Investments of both the sponsoring government and of external participants in the investment pool.

C) Investments related to the sponsoring government's governmental funds and of external participants in the investment pool.

D) Investments related to the sponsoring government's other fiduciary funds and of external participants in the investment pool.

A) Only investments owned by external participants in the investment pool.

B) Investments of both the sponsoring government and of external participants in the investment pool.

C) Investments related to the sponsoring government's governmental funds and of external participants in the investment pool.

D) Investments related to the sponsoring government's other fiduciary funds and of external participants in the investment pool.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is NOT a criterion that an employer's annual required contribution must satisfy to be considered acceptable?

A) It must consist of the employer's normal cost plus a provision for amortizing the plan's unfunded actuarially accrued liability.

B) Actual assumptions must be in accordance with standards of the Actuarial Standards Board.

C) Actuarial value of pension plan assets must be based on market values on the financial statement date.

D) Assumptions as to investment earnings should be based on long-term projections.

A) It must consist of the employer's normal cost plus a provision for amortizing the plan's unfunded actuarially accrued liability.

B) Actual assumptions must be in accordance with standards of the Actuarial Standards Board.

C) Actuarial value of pension plan assets must be based on market values on the financial statement date.

D) Assumptions as to investment earnings should be based on long-term projections.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is NOT true of agency funds?

A) Governments use them to account for resources held as trustee or agent for another government, fund, not-for-profit entity, or individual.

B) They are required to use a modified accrual basis of accounting.

C) They have no operations and therefore are not required to prepare financial statements.

D) Agency fund assets are always offset by liabilities.

A) Governments use them to account for resources held as trustee or agent for another government, fund, not-for-profit entity, or individual.

B) They are required to use a modified accrual basis of accounting.

C) They have no operations and therefore are not required to prepare financial statements.

D) Agency fund assets are always offset by liabilities.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

57

Governments must present which of the following financial statements for fiduciary funds?

A) Statement of assets and benefits and statement of cash flows.

B) Statement of fiduciary net assets and statement of changes in benefits,

C) Statement of fiduciary net position and statement of changes in fiduciary net position.

D) Statement of net assets and statement of accrued benefit obligations.

A) Statement of assets and benefits and statement of cash flows.

B) Statement of fiduciary net assets and statement of changes in benefits,

C) Statement of fiduciary net position and statement of changes in fiduciary net position.

D) Statement of net assets and statement of accrued benefit obligations.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

58

Financial assets reported by most investment trust funds of governments should be reported at

A) Cost

B) Amortized historical cost.

C) Fair value on the date of the financial statements.

D) Fair value computed by a weighted-average approach.

A) Cost

B) Amortized historical cost.

C) Fair value on the date of the financial statements.

D) Fair value computed by a weighted-average approach.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

59

Financial assets reported by investment pools should be reported at

A) Fair value at the date of the financial statements.

B) Amortized historical cost.

C) Fair value computed using a weighted-average approach.

D) Cost.

A) Fair value at the date of the financial statements.

B) Amortized historical cost.

C) Fair value computed using a weighted-average approach.

D) Cost.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

60

Liabilities reported in pension trust funds consist of

A) Liabilities accrued using the accrual basis of accounting, including the actuarial accrued liability for the plan.

B) Liabilities accrued using the modified accrual basis of accounting, excluding the actuarial accrued liability for the plan.

C) Liabilities accrued using the accrual basis of accounting, excluding the actuarial accrued liability for the plan.

D) Liabilities accrued using the modified accrual basis of accounting, including the plan benefits that will be paid with measurable and available financial resources.

A) Liabilities accrued using the accrual basis of accounting, including the actuarial accrued liability for the plan.

B) Liabilities accrued using the modified accrual basis of accounting, excluding the actuarial accrued liability for the plan.

C) Liabilities accrued using the accrual basis of accounting, excluding the actuarial accrued liability for the plan.

D) Liabilities accrued using the modified accrual basis of accounting, including the plan benefits that will be paid with measurable and available financial resources.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

61

How does a defined contribution pension plan differ from a defined benefit pension plan? What are some of the advantages and disadvantages of each type of plan? How do they differ for accounting and financial reporting? Which type of plan would you prefer to belong to? Why?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

62

Kilmore City received a cash gift of $125,000 from a citizen who specified that the gift must be used to support recreational activities for the city's youth. The city accounted for this gift in the appropriate fund. During the year the city engaged in the following activities.

REQUIRED:

Prepare the appropriate journal entries. Be sure to indicate in which fund the entries should be recorded.

a) The city accepted the donation.

b) The city engaged in a fund-raising effort to provide additional funds to support youth recreational activities and raised $6,000 in pledges. The city collected $2,000 in cash with the remaining pledges collectible shortly after the end of the year.

c) The city temporarily invested $50,000 of the gift in marketable securities.

d) The city spent $26,000 on goal posts, nets, etc., for a soccer field.

e) The city received $2,000 in dividends and interest earned on the temporary investment.

f) At year-end the temporary investments had a market value of $51,000.

g) The city closed the revenue and expense accounts.

REQUIRED:

Prepare the appropriate journal entries. Be sure to indicate in which fund the entries should be recorded.

a) The city accepted the donation.

b) The city engaged in a fund-raising effort to provide additional funds to support youth recreational activities and raised $6,000 in pledges. The city collected $2,000 in cash with the remaining pledges collectible shortly after the end of the year.

c) The city temporarily invested $50,000 of the gift in marketable securities.

d) The city spent $26,000 on goal posts, nets, etc., for a soccer field.

e) The city received $2,000 in dividends and interest earned on the temporary investment.

f) At year-end the temporary investments had a market value of $51,000.

g) The city closed the revenue and expense accounts.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

63

At the end of 2015, Learning Tree, a not-for-profit organization, received a $5 million contribution (fair value), consisting entirely of investment securities. The contribution is required to be used to establish a permanent endowment, the income from which must be used exclusively to provide free "chapter books" to elementary school children. The endowment specifies that both realized and unrealized gains may be used for this purpose in addition to investment income. Learning Tree applies FASB accounting standards for not-for-profit organizations.

At the start of 2016, Learning Tree had $600,000 in unrestricted net assets.

During 2016, the endowment earns $100,000 in dividends and interest. Learning Tree spends the entire amount on books and distribution costs. At year-end, the value of the endowment portfolio is $5.5 million.

During 2017, the endowment earns $100,000 in dividends and interest. The entire amount is spent on books. At year-end, the fair value of the endowment portfolio has decreased by $1 million to $4.5 million.

During 2018, the endowment earns $100,000 in dividends and interest. The entire amount is spent on books. At year-end, the fair value of the endowment portfolio has gone back up by $0.4 million to $4.9 million.

REQUIRED:

a) Assuming no other transactions, prepare a schedule showing the balances in unrestricted, temporarily restricted, and permanently restricted net assets for the years ending in 2016, 2017, and 2018.

b) What effect would there be on these three balances of net assets if the donor specified that all gains (realized and unrealized) must be reinvested?

At the start of 2016, Learning Tree had $600,000 in unrestricted net assets.

During 2016, the endowment earns $100,000 in dividends and interest. Learning Tree spends the entire amount on books and distribution costs. At year-end, the value of the endowment portfolio is $5.5 million.

During 2017, the endowment earns $100,000 in dividends and interest. The entire amount is spent on books. At year-end, the fair value of the endowment portfolio has decreased by $1 million to $4.5 million.

During 2018, the endowment earns $100,000 in dividends and interest. The entire amount is spent on books. At year-end, the fair value of the endowment portfolio has gone back up by $0.4 million to $4.9 million.

REQUIRED:

a) Assuming no other transactions, prepare a schedule showing the balances in unrestricted, temporarily restricted, and permanently restricted net assets for the years ending in 2016, 2017, and 2018.

b) What effect would there be on these three balances of net assets if the donor specified that all gains (realized and unrealized) must be reinvested?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

64

Wilmer County provides a defined benefit pension plan for its employees. The county accounts for the pension plan in a pension trust fund, which is included in the county's basic financial statements. In the years indicated, the county engaged in the following transactions related to the pension trust fund.

REQUIRED:

Prepare all necessary journal entries. Clearly indicate the fund in which the entry is being made. If no entry is needed, please write "No entry required."

a) In Year 1, the pension trust fund sent billings to the general fund and the City Utility (enterprise) Fund for the actuarially determined amount of required contributions. The general fund was billed $300,000 but paid only $220,000 during the year. The enterprise fund was billed $450,000 and paid $530,000.

b) In Year 2, the pension trust fund sent billings to the general fund and the City Utility Fund for the actuarially determined amount of required contributions. The general fund was billed $320,000 and paid the entire amount plus $30,000 of last year's underpayment. The enterprise fund was billed $480,000 and paid only $380,000.

REQUIRED:

Prepare all necessary journal entries. Clearly indicate the fund in which the entry is being made. If no entry is needed, please write "No entry required."

a) In Year 1, the pension trust fund sent billings to the general fund and the City Utility (enterprise) Fund for the actuarially determined amount of required contributions. The general fund was billed $300,000 but paid only $220,000 during the year. The enterprise fund was billed $450,000 and paid $530,000.

b) In Year 2, the pension trust fund sent billings to the general fund and the City Utility Fund for the actuarially determined amount of required contributions. The general fund was billed $320,000 and paid the entire amount plus $30,000 of last year's underpayment. The enterprise fund was billed $480,000 and paid only $380,000.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

65

You are asked by a wealthy businesswoman to help construct a permanent endowment for a local university. She asks you whether you believe the university should be required to add investment gains to the principal of the endowment or whether it would be preferable for the gains to be available for spending. How would you respond and why?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

66

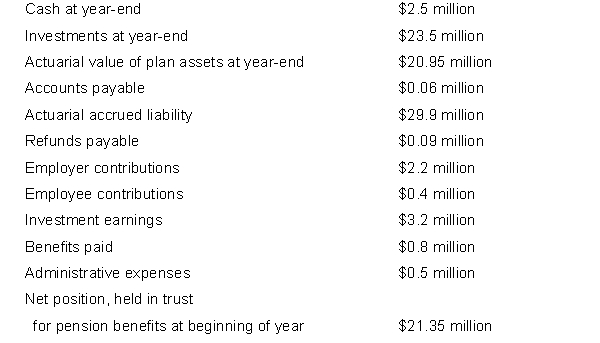

Briana City provides a defined benefit pension plan for its full-time employees. The city includes the plan as a pension trust fund in its fund financial statements.

REQUIRED:

Using the information below, prepare a statement of fiduciary net position and a statement of changes in fiduciary net position for the pension trust fund.

REQUIRED:

Using the information below, prepare a statement of fiduciary net position and a statement of changes in fiduciary net position for the pension trust fund.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is a NOT a true statement concerning postemployment benefits other than pensions (OPEB)?

A) OPEB comprise predominantly healthcare benefits.

B) Many governments do not provide OPEB or provide them on a pay-as-you-go basis.

C) GASB standards of accounting for OPEB are very similar to those for pension benefits.

D) OPEB plans should be accounted for in permanent funds.

A) OPEB comprise predominantly healthcare benefits.

B) Many governments do not provide OPEB or provide them on a pay-as-you-go basis.

C) GASB standards of accounting for OPEB are very similar to those for pension benefits.

D) OPEB plans should be accounted for in permanent funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is a potential reform for defined benefit plans?

A) Refuse to pay benefits for more than 10 years after retirement

B) Reduce the age of retirement to allow employees to develop a second career to save for retirement

C) Eliminate "spiking" or using overtime to increase the salary on which benefits are determined

D) None of the above.

ANSWERS TO MULTIPLE CHOICE (CHAPTER 10)

A) Refuse to pay benefits for more than 10 years after retirement

B) Reduce the age of retirement to allow employees to develop a second career to save for retirement

C) Eliminate "spiking" or using overtime to increase the salary on which benefits are determined

D) None of the above.

ANSWERS TO MULTIPLE CHOICE (CHAPTER 10)

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

69

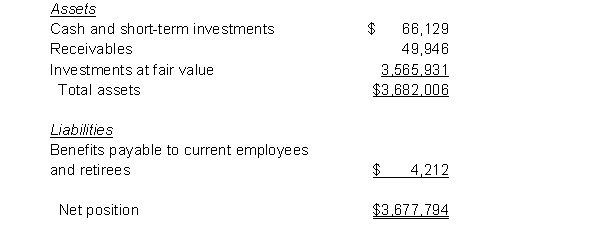

The statement of fiduciary net position for a school district's defined benefit pension plan shows the following (in condensed form and in thousands)

A. The plan has been in operation for over 20 years and covers all school district employees. What is the most reasonable explanation of why the benefits payable to current employees and retirees is so small relative to plan assets?

B. Suppose that in the current year the school district's annual required contribution was $6,300,000. In the past, the district has always paid the annual required contribution in full. However, in the current year the district budgeted and paid into the pension trust fund only $5,000,000.

1. Prepare the journal entry that the district (not the plan) should make to record the year's pension contribution. You need not make budgetary or closing entries. The plan is accounted for in a governmental fund.

2. Prepare the journal entry to record the year's pension contribution for reporting in the district's government-wide statements.

C. The district's annual financial report indicated that its "normal cost" was $530,000 and that the "amortization of the unfunded actuarial accrued liability" was $100,000.

1. What is meant by "normal cost?"

2. What is meant by "unfunded actuarial accrued liability"? What are its principal causes? Why must it be amortized?

A.

The plan has been in operation for over 20 years and covers all school district employees. What is the most reasonable explanation of why the benefits payable to current employees and retirees is so small relative to plan assets?B. Suppose that in the current year the school district's annual required contribution was $6,300,000. In the past, the district has always paid the annual required contribution in full. However, in the current year the district budgeted and paid into the pension trust fund only $5,000,000.

1. Prepare the journal entry that the district (not the plan) should make to record the year's pension contribution. You need not make budgetary or closing entries. The plan is accounted for in a governmental fund.

2. Prepare the journal entry to record the year's pension contribution for reporting in the district's government-wide statements.

C. The district's annual financial report indicated that its "normal cost" was $530,000 and that the "amortization of the unfunded actuarial accrued liability" was $100,000.

1. What is meant by "normal cost?"

2. What is meant by "unfunded actuarial accrued liability"? What are its principal causes? Why must it be amortized?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

70

State University maintains accounts for each of its student groups. The monies collected by the Accounting Fraternity are deposited with the university. As the fraternity authorizes disbursements of its funds, the university disburses the monies. During the year, the fraternity engaged in the following transactions.

REQUIRED:

Prepare the appropriate entries on the books of the university. Be sure to indicate in which fund the entries should be recorded.

a) The fraternity deposited $400 in student dues.

b) The fraternity authorized payments of $350 to Delta Airlines for an airline ticket for a member to fly to the national meeting, and of $100 to the National Accounting Fraternity for registration.

c) The fraternity received a contribution of $500 from a major accounting firm to be used by the fraternity to offset the cost of attending the national meeting.

d) The fraternity operated a book exchange on a consignment basis and collected revenues of $10,000. It authorized the university to write $9,000 of checks to the students whose books the fraternity had sold. The fraternity was pleased with the $1,000 profit.

e) The fraternity received a reimbursement of $150 from the National office to offset the costs of attending the National meeting.

REQUIRED:

Prepare the appropriate entries on the books of the university. Be sure to indicate in which fund the entries should be recorded.

a) The fraternity deposited $400 in student dues.

b) The fraternity authorized payments of $350 to Delta Airlines for an airline ticket for a member to fly to the national meeting, and of $100 to the National Accounting Fraternity for registration.

c) The fraternity received a contribution of $500 from a major accounting firm to be used by the fraternity to offset the cost of attending the national meeting.

d) The fraternity operated a book exchange on a consignment basis and collected revenues of $10,000. It authorized the university to write $9,000 of checks to the students whose books the fraternity had sold. The fraternity was pleased with the $1,000 profit.

e) The fraternity received a reimbursement of $150 from the National office to offset the costs of attending the National meeting.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

71

A donor gives your city $100,000 to be used to support youth recreational programs. What type of fund should be used to account for this gift? How or why did you select this fund? Include in your answer other types of funds that could be considered to account for similar donations and why you did not select one of those funds.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

72

Scofield City received a donation from the estate of the late Lisa O'Reilly to be used to support the city's public library. The gift consisted of $200,000 cash and a portfolio of securities with a market value of $350,000. The securities have a book value of $250,000. The donor stipulated that the principal of the gift, including investment gains (realized and unrealized) but excluding investment losses, must be kept intact. The income must be used to care for and maintain the book collection at the newly renamed O'Reilly Public Library. All appropriate costs, including investment losses, may be charged against the revenues yearly to determine the amount available for the specified purposes. During the year, the city engaged in the following transactions on behalf of the library.

REQUIRED:

Prepare the appropriate entries in the city's permanent fund.

a) Accepted the donation.

b) Received dividends and interest of $18,000.

c) Purchased securities for $200,000.

d) Sold securities that were part of the original gift (market value at date of gift $72,000; book value in hands of donor $68,000) for $78,000.

e) Sold some of the securities that were acquired in transaction (c) for $53,000. They were acquired at a price of $55,000.

f) The portfolio of securities at year-end had a market value of $432,000.

g) Closed the fund's revenue and expense accounts and transferred the amount available for expenditure to the appropriate fund. Close the transfer account.

REQUIRED:

Prepare the appropriate entries in the city's permanent fund.

a) Accepted the donation.

b) Received dividends and interest of $18,000.

c) Purchased securities for $200,000.

d) Sold securities that were part of the original gift (market value at date of gift $72,000; book value in hands of donor $68,000) for $78,000.

e) Sold some of the securities that were acquired in transaction (c) for $53,000. They were acquired at a price of $55,000.

f) The portfolio of securities at year-end had a market value of $432,000.

g) Closed the fund's revenue and expense accounts and transferred the amount available for expenditure to the appropriate fund. Close the transfer account.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

73

Investment trust funds are one of four types of fiduciary funds. What is the purpose of investment trust funds? What is the nature of the assets and liabilities that they report? Can the government that provides an investment trust fund invest its own assets in that fund?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

74

Under GASB standards, agency funds are excluded from the face of the government-wide financial statements. What are agency funds? Do you believe they should be presented in the government-wide statements? Could they--or should they--be presented elsewhere?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 74 flashcards in this deck.