Deck 21: Options and Corporate Finance

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

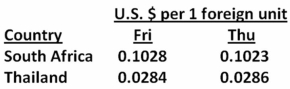

Which one of the following statements is correct given the following exchange rates?

A)On Thursday, one U.S.dollar was equal to 0.1023 South African rand.

B)On Friday, one Thai baht was equal to $35.21.

C)Both the South African rand and the Thai baht appreciated against the U.S.dollar from Thursday to Friday.

D)The South African rand appreciated from Thursday to Friday against the U.S.dollar.

E)The U.S.dollar depreciated from Thursday to Friday against the Thai baht.

A)On Thursday, one U.S.dollar was equal to 0.1023 South African rand.

B)On Friday, one Thai baht was equal to $35.21.

C)Both the South African rand and the Thai baht appreciated against the U.S.dollar from Thursday to Friday.

D)The South African rand appreciated from Thursday to Friday against the U.S.dollar.

E)The U.S.dollar depreciated from Thursday to Friday against the Thai baht.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

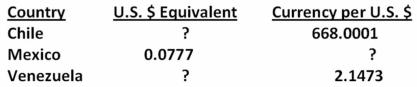

You just returned from some extensive traveling throughout the Americas.You started your trip with $20,000 in your pocket.You spent 3.4 million pesos while in Chile and 16,500 bolivares in Venezuela.Then on the way home, you spent 47,500 pesos in Mexico.How many dollars did you have left by the time you returned to the U.S.given the following exchange rates? (Note: Multiple symbols are used to designate various currencies.For example, the U.S.dollar is notated as "$" or as "USD".)

A)1,113 USD

B)3,535 USD

C)4,117 USD

D)4,244 USD

E)7,408 USD

A)1,113 USD

B)3,535 USD

C)4,117 USD

D)4,244 USD

E)7,408 USD

Question

Question

Question

Question

Question

You are planning a trip to Australia.Your hotel will cost you A$145 per night for seven nights.You expect to spend another A$2,800 for meals, tours, souvenirs, and so forth.How much will this trip cost you in U.S.dollars given the following exchange rates?

A)$2,559

B)$2,604

C)$2,631

D)$5,452

E)$5,688

A)$2,559

B)$2,604

C)$2,631

D)$5,452

E)$5,688

Question

Question

Question

Question

Question

You have 100 British pounds.A friend of yours is willing to exchange 180 Canadian dollars for your 100 British pounds.What will be your profit or loss if you accept your friend's offer, given the following exchange rates?

A)£10.20 loss

B)£13.29 loss

C)£28.51 loss

D)£10.20 profit

E)£28.51 profit

A)£10.20 loss

B)£13.29 loss

C)£28.51 loss

D)£10.20 profit

E)£28.51 profit

Question

Question

Question

Question

Question

Question

Assume you can buy 52 British pounds with 100 Canadian dollars.How much profit can you earn on a triangle arbitrage given the following rates if you start out with 100 U.S.dollars?

A)$0.78

B)$1.04

C)$1.33

D)$1.56

E)$1.64

A)$0.78

B)$1.04

C)$1.33

D)$1.56

E)$1.64

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A new coat costs 3,900 Russian rubles.How much will the identical coat cost in Euros if absolute purchasing power parity exists and the following exchange rates apply?

A)€97.23

B)€112.97

C)€119.05

D)€181.27

E)€183.99

A)€97.23

B)€112.97

C)€119.05

D)€181.27

E)€183.99

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/98

Play

Full screen (f)

Deck 21: Options and Corporate Finance

1

U.S.dollars deposited in a bank in Switzerland are called:

A)foreign depository receipts.

B)international exchange certificates.

C)francs.

D)Eurocurrency.

E)Eurodollars.

A)foreign depository receipts.

B)international exchange certificates.

C)francs.

D)Eurocurrency.

E)Eurodollars.

D

2

You would like to purchase a security that is issued by the British government.Which one of the following should you purchase?

A)Samurai bond

B)kronor

C)Euro

D)LIBOR

E)gilt

A)Samurai bond

B)kronor

C)Euro

D)LIBOR

E)gilt

E

3

The condition stating that the interest rate differential between two countries is equal to the percentage difference between the forward exchange rate and the spot exchange rate is called:

A)the unbiased forward rates condition.

B)uncovered interest rate parity.

C)the international Fisher effect.

D)purchasing power parity.

E)interest rate parity.

A)the unbiased forward rates condition.

B)uncovered interest rate parity.

C)the international Fisher effect.

D)purchasing power parity.

E)interest rate parity.

E

4

Which one of the following securities is used as a means of investing in a foreign stock that otherwise could not be traded in the United States?

A)American Depository Receipt

B)Yankee bond

C)Yankee stock

D)LIBOR

E)gilt

A)American Depository Receipt

B)Yankee bond

C)Yankee stock

D)LIBOR

E)gilt

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

5

A large U.S.company has £500,000 in excess cash from its foreign operations.The company would like to exchange these funds for U.S.dollars.In which of the following markets can this exchange be arranged?

A)ADR

B)national registry

C)national discount window

D)foreign exchange market

E)Eurobond market

A)ADR

B)national registry

C)national discount window

D)foreign exchange market

E)Eurobond market

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

6

Assume that $1 is equal to ¥98 and also equal to C$1.21.Based on this, you could say that C$1 is equal to: C$1(¥98/C$1.21) = ¥80.99.The exchange rate of C$1 = ¥80.99 is referred to as the:

A)open exchange rate.

B)cross-rate.

C)backward rate.

D)forward rate.

E)interest rate.

A)open exchange rate.

B)cross-rate.

C)backward rate.

D)forward rate.

E)interest rate.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

7

On Friday evening, Bank A loans Bank B Eurodollars that must be repaid the following Monday morning.Which one of the following is most likely the interest rate that will be charged on this loan?

A)Eurodollar yield to maturity

B)London Interbank Offer Rate

C)Paris Opening Interest Rate

D)United States Treasury bill rate

E)international prime rate

A)Eurodollar yield to maturity

B)London Interbank Offer Rate

C)Paris Opening Interest Rate

D)United States Treasury bill rate

E)international prime rate

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

8

Which one of the following states that the expected percentage change in the exchange rate between two countries is equal to the difference in the countries' interest rates?

A)unbiased forward rates condition

B)uncovered interest parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

A)unbiased forward rates condition

B)uncovered interest parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

9

A trader has just agreed to exchange $2 million U.S.dollars for $1.55 million Euros six months from today.This exchange is an example of a:

A)spot trade.

B)forward trade.

C)currency swap.

D)floating swap.

E)triangle arbitrage.

A)spot trade.

B)forward trade.

C)currency swap.

D)floating swap.

E)triangle arbitrage.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

10

George and Pat just made an agreement to exchange currencies based on today's exchange rate.Settlement will occur tomorrow.Which one of the following is the exchange rate that applies to this agreement?

A)spot exchange rate

B)forward exchange rate

C)triangle rate

D)cross rate

E)current rate

A)spot exchange rate

B)forward exchange rate

C)triangle rate

D)cross rate

E)current rate

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

11

Trader A has agreed to give 100,000 U.S.dollars to Trader B in exchange for British pounds based on today's exchange rate of $1 = £0.62.The traders agree to settle this trade within two business day.What is this exchange called?

A)swap

B)option trade

C)futures trade

D)forward trade

E)spot trade

A)swap

B)option trade

C)futures trade

D)forward trade

E)spot trade

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

12

Mr.Black has agreed to a currency exchange with Mr.White.The parties have agreed to exchange C$12,500 for $10,000 with the exchange occurring 4 months from now.This agreed-upon exchange rate is called the:

A)spot rate.

B)swap rate.

C)forward rate.

D)parity rate.

E)triangle rate.

A)spot rate.

B)swap rate.

C)forward rate.

D)parity rate.

E)triangle rate.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

13

International bonds issued in a single country and denominated in that country's currency are called:

A)Treasury bonds.

B)Eurobonds.

C)gilts.

D)Brady bonds.

E)foreign bonds.

A)Treasury bonds.

B)Eurobonds.

C)gilts.

D)Brady bonds.

E)foreign bonds.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

14

International bonds issued in multiple countries but denominated solely in the issuer's currency are called:

A)Treasury bonds.

B)Bulldog bonds.

C)Eurobonds.

D)Yankee bonds.

E)Samurai bonds.

A)Treasury bonds.

B)Bulldog bonds.

C)Eurobonds.

D)Yankee bonds.

E)Samurai bonds.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

15

Which one of the following supports the idea that real interest rates are equal across countries?

A)unbiased forward rates condition

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

A)unbiased forward rates condition

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

16

Which one of the following is the risk that a firm faces when it opens a facility in a foreign country, given that the exchange rate between the firm's home country and this foreign country fluctuates over time?

A)international risk

B)diversifiable risk

C)purchasing power risk

D)exchange rate risk

E)political risk

A)international risk

B)diversifiable risk

C)purchasing power risk

D)exchange rate risk

E)political risk

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

17

Which one of the following states that the current forward rate is an unbiased predictor of the future spot exchange rate?

A)unbiased forward rates

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

A)unbiased forward rates

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

18

Assume that an item costs $100 in the U.S.and the exchange rate between the U.S.and Canada is: $1 = C$1.27.Which one of the following concepts supports the idea that the item that sells for $100 in the U.S.is currently selling in Canada for $127?

A)unbiased forward rates condition

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

A)unbiased forward rates condition

B)uncovered interest rate parity

C)international Fisher effect

D)purchasing power parity

E)interest rate parity

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

19

Party A has agreed to exchange $1 million U.S.dollars for $1.21 million Canadian dollars.What is this agreement called?

A)gilt

B)LIBOR

C)SWIFT

D)Yankee agreements

E)swap

A)gilt

B)LIBOR

C)SWIFT

D)Yankee agreements

E)swap

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

20

The price of one Euro expressed in U.S.dollars is referred to as a(n):

A)ADR rate.

B)cross inflation rate.

C)depository rate.

D)exchange rate.

E)foreign interest rate.

A)ADR rate.

B)cross inflation rate.

C)depository rate.

D)exchange rate.

E)foreign interest rate.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following variables used in the covered interest arbitrage formula are correctly defined?

I)RFC: Foreign country nominal risk-free interest rate

II)RUS: U.S.real risk-free interest rate

III)F1: 360-day forward rate

IV)S0: Current spot rate expressed in units of foreign currency per one U.S.dollar

A)I and II only

B)III and IV only

C)I, III, and IV only

D)II, III, and IV only

E)I, II, III, and IV

I)RFC: Foreign country nominal risk-free interest rate

II)RUS: U.S.real risk-free interest rate

III)F1: 360-day forward rate

IV)S0: Current spot rate expressed in units of foreign currency per one U.S.dollar

A)I and II only

B)III and IV only

C)I, III, and IV only

D)II, III, and IV only

E)I, II, III, and IV

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

22

Which one of the following statements is correct given the following exchange rates?

A)On Thursday, one U.S.dollar was equal to 0.1023 South African rand.

B)On Friday, one Thai baht was equal to $35.21.

C)Both the South African rand and the Thai baht appreciated against the U.S.dollar from Thursday to Friday.

D)The South African rand appreciated from Thursday to Friday against the U.S.dollar.

E)The U.S.dollar depreciated from Thursday to Friday against the Thai baht.

A)On Thursday, one U.S.dollar was equal to 0.1023 South African rand.

B)On Friday, one Thai baht was equal to $35.21.

C)Both the South African rand and the Thai baht appreciated against the U.S.dollar from Thursday to Friday.

D)The South African rand appreciated from Thursday to Friday against the U.S.dollar.

E)The U.S.dollar depreciated from Thursday to Friday against the Thai baht.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

23

The unbiased forward rate is a:

A)condition where a future spot rate is equal to the current spot rate.

B)guarantee of a future spot rate at one point in time.

C)condition where the spot rate is expected to remain constant over a period of time.

D)relationship between the future spot rate of two currencies at an equivalent point in time.

E)predictor of the future spot rate at the equivalent point in time.

A)condition where a future spot rate is equal to the current spot rate.

B)guarantee of a future spot rate at one point in time.

C)condition where the spot rate is expected to remain constant over a period of time.

D)relationship between the future spot rate of two currencies at an equivalent point in time.

E)predictor of the future spot rate at the equivalent point in time.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

24

Spot trades must be settled:

A)at the time of the trade.

B)on the day following the trade date.

C)within two business days.

D)within three business days.

E)within one week of the trade date.

A)at the time of the trade.

B)on the day following the trade date.

C)within two business days.

D)within three business days.

E)within one week of the trade date.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following conditions are required for absolute purchasing power parity to exist?

I)goods must be identical

II)goods must have equal economic value

III)transaction costs must be zero

IV)there can be no barriers to trade

A)I and III only

B)II and IV only

C)I, III, and IV only

D)I, II, and III only

E)I, II, III, and IV

I)goods must be identical

II)goods must have equal economic value

III)transaction costs must be zero

IV)there can be no barriers to trade

A)I and III only

B)II and IV only

C)I, III, and IV only

D)I, II, and III only

E)I, II, III, and IV

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

26

Absolute purchasing power parity is most apt to exist for which one of the following items?

A)lumber

B)computer

C)silver

D)automobile

E)cell phone

A)lumber

B)computer

C)silver

D)automobile

E)cell phone

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

27

Which one of the following statements is correct concerning the foreign exchange market?

A)The trading floor of the foreign exchange market is located in London, England.

B)The foreign exchange market is the world's second largest financial market.

C)The four primary currencies that are traded in the foreign exchange market are the U.S.dollar, the British pound, the French franc, and the euro.

D)Importers, exporters, and speculators are key players in the foreign exchange market.

E)The U.S.created a communications network called SWIFT to facilitate currency trading.

A)The trading floor of the foreign exchange market is located in London, England.

B)The foreign exchange market is the world's second largest financial market.

C)The four primary currencies that are traded in the foreign exchange market are the U.S.dollar, the British pound, the French franc, and the euro.

D)Importers, exporters, and speculators are key players in the foreign exchange market.

E)The U.S.created a communications network called SWIFT to facilitate currency trading.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

28

Which one of the following formulas correctly describes the relative purchasing power parity relationship?

A)E(St) = S0 × [1 + (hFC - hUS)]t

B)E(St) = S0 × [1 - (hFC - hUS)]t

C)E(St) = S0 × [1 + (hUS + hFC)]t

D)E(St) = S0 × [1 - (hUS - hFC)]t

E)E(St) = S0 × [1 + (hUS - hFC)]t

A)E(St) = S0 × [1 + (hFC - hUS)]t

B)E(St) = S0 × [1 - (hFC - hUS)]t

C)E(St) = S0 × [1 + (hUS + hFC)]t

D)E(St) = S0 × [1 - (hUS - hFC)]t

E)E(St) = S0 × [1 + (hUS - hFC)]t

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

29

The forward rate market is dependent upon:

A)current forward rates exceeding current spot rates.

B)current spot rates exceeding current forward rates over time.

C)current spot rates equaling current forward rates, on average, over time.

D)forward rates equaling the actual future spot rates on average over time.

E)current spot rates equaling the actual future spot rates on average over time.

A)current forward rates exceeding current spot rates.

B)current spot rates exceeding current forward rates over time.

C)current spot rates equaling current forward rates, on average, over time.

D)forward rates equaling the actual future spot rates on average over time.

E)current spot rates equaling the actual future spot rates on average over time.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

30

Assume the euro is selling in the spot market for $1.33.Simultaneously, in the 3-month forward market the euro is selling for $1.35.Which one of the following statements correctly describes this situation?

A)The spot market is out of equilibrium.

B)The forward market is out of equilibrium.

C)The dollar is selling at a premium relative to the euro.

D)The euro is selling at a premium relative to the dollar.

E)The euro is expected to depreciate in value.

A)The spot market is out of equilibrium.

B)The forward market is out of equilibrium.

C)The dollar is selling at a premium relative to the euro.

D)The euro is selling at a premium relative to the dollar.

E)The euro is expected to depreciate in value.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

31

Which one of the following formulas expresses the absolute purchasing power parity relationship between the U.S.dollar and the British pound?

A)S0 = PUK × PUS

B)PUS = Ft × PUK

C)PUK = S0 × PUS

D)Ft = PUS × PUK

E)S0 × Ft = PUK × PUS

A)S0 = PUK × PUS

B)PUS = Ft × PUK

C)PUK = S0 × PUS

D)Ft = PUS × PUK

E)S0 × Ft = PUK × PUS

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

32

Relative purchasing power parity:

A)states that identical items should cost the same regardless of the currency used to make the purchase.

B)relates differences in inflation rates to differences in exchange rates.

C)compares the real rate of return to the nominal rate of return.

D)explains the differences in real rates across national boundaries.

E)relates future exchange rates to current spot rates.

A)states that identical items should cost the same regardless of the currency used to make the purchase.

B)relates differences in inflation rates to differences in exchange rates.

C)compares the real rate of return to the nominal rate of return.

D)explains the differences in real rates across national boundaries.

E)relates future exchange rates to current spot rates.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

33

Which one of the following names matches the country where the bond is issued?

A)Empire: United Kingdom

B)Western: United States

C)Samurai: China

D)Bulldog: France

E)Rembrandt: Netherlands

A)Empire: United Kingdom

B)Western: United States

C)Samurai: China

D)Bulldog: France

E)Rembrandt: Netherlands

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

34

Interest rate parity:

A)eliminates covered interest arbitrage opportunities.

B)exists when spot rates are equal for multiple countries.

C)means the nominal risk-free rate of return must be the same across countries.

D)exists when the spot rate is equal to the futures rate.

E)eliminates exchange rate fluctuations.

A)eliminates covered interest arbitrage opportunities.

B)exists when spot rates are equal for multiple countries.

C)means the nominal risk-free rate of return must be the same across countries.

D)exists when the spot rate is equal to the futures rate.

E)eliminates exchange rate fluctuations.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

35

The market value of the Blackwell Corporation just declined by 5 percent.Analysts believe this decrease in value was caused by recent legislation passed by Congress.Which type of risk does this illustrate?

A)international risk

B)diversifiable risk

C)purchasing power risk

D)exchange rate risk

E)political risk

A)international risk

B)diversifiable risk

C)purchasing power risk

D)exchange rate risk

E)political risk

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

36

A basic interest rate swap generally involves trading a:

A)short-term rate for a long-term rate.

B)foreign rate for a domestic rate.

C)government rate for a corporate rate.

D)fixed rate for a variable rate.

E)taxable rate for a tax-exempt rate.

A)short-term rate for a long-term rate.

B)foreign rate for a domestic rate.

C)government rate for a corporate rate.

D)fixed rate for a variable rate.

E)taxable rate for a tax-exempt rate.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

37

Triangle arbitrage:

I)is a profitable situation involving three separate currency exchange transactions.

II)helps keep the currency market in equilibrium.

III)opportunities can exist in either the spot or the forward market.

IV)is based solely on differences in exchange ratios between spot and futures markets.

A)I and IV only

B)II and III only

C)I, II, and III only

D)II, III, and IV only

E)I, II, III, and IV

I)is a profitable situation involving three separate currency exchange transactions.

II)helps keep the currency market in equilibrium.

III)opportunities can exist in either the spot or the forward market.

IV)is based solely on differences in exchange ratios between spot and futures markets.

A)I and IV only

B)II and III only

C)I, II, and III only

D)II, III, and IV only

E)I, II, III, and IV

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

38

The LIBOR is primarily used as the basis for the rate charged on:

A)short-term debt in the Lisbon market.

B)mortgage loans in the Lisbon market.

C)Eurodollar loans in the London market.

D)U.S.federal funds.

E)interbank loans in the U.S.

A)short-term debt in the Lisbon market.

B)mortgage loans in the Lisbon market.

C)Eurodollar loans in the London market.

D)U.S.federal funds.

E)interbank loans in the U.S.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

39

The interest rate parity approximation formula is:

A)Ft = S0 × [1 + (RFC + RUS)]t.

B)Ft = S0 × [1 - (RFC - RUS)]t.

C)Ft = S0 × [1 + (RFC - RUS)]t.

D)Ft = S0 × [1 + (RFC × RUS)]t.

E)Ft = S0 × [1 - (RFC + RUS)]t.

A)Ft = S0 × [1 + (RFC + RUS)]t.

B)Ft = S0 × [1 - (RFC - RUS)]t.

C)Ft = S0 × [1 + (RFC - RUS)]t.

D)Ft = S0 × [1 + (RFC × RUS)]t.

E)Ft = S0 × [1 - (RFC + RUS)]t.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

40

Where does most of the trading in Eurobonds occur?

A)Munich

B)Frankfurt

C)London

D)New York

E)Paris

A)Munich

B)Frankfurt

C)London

D)New York

E)Paris

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

41

Which one of the following types of operations would be subject to the most political risk if the operation were conducted outside of a firm's home country?

A)accounting and payroll functions

B)partial assembly of components manufactured in the firm's home country

C)military weapons manufacturing

D)packing materials manufacturing for use by the home country firm

E)production of minor parts, such as nuts and bolts, for use by the home country firm

A)accounting and payroll functions

B)partial assembly of components manufactured in the firm's home country

C)military weapons manufacturing

D)packing materials manufacturing for use by the home country firm

E)production of minor parts, such as nuts and bolts, for use by the home country firm

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

42

You just returned from some extensive traveling throughout the Americas.You started your trip with $20,000 in your pocket.You spent 3.4 million pesos while in Chile and 16,500 bolivares in Venezuela.Then on the way home, you spent 47,500 pesos in Mexico.How many dollars did you have left by the time you returned to the U.S.given the following exchange rates? (Note: Multiple symbols are used to designate various currencies.For example, the U.S.dollar is notated as "$" or as "USD".)

A)1,113 USD

B)3,535 USD

C)4,117 USD

D)4,244 USD

E)7,408 USD

A)1,113 USD

B)3,535 USD

C)4,117 USD

D)4,244 USD

E)7,408 USD

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

43

Currently, $1 will buy C$1.2103 while $1.2762 will buy €1.What is the exchange rate between the Canadian dollar and the euro?

A)C$1 = €0.6474

B)C$1 = €0.6539

C)C$1 = €1.2762

D)C$1.5446 = €1

E)C$1.5528 = €1

A)C$1 = €0.6474

B)C$1 = €0.6539

C)C$1 = €1.2762

D)C$1.5446 = €1

E)C$1.5528 = €1

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

44

The home currency approach:

A)generally produces more reliable results than those found using the foreign currency approach.

B)requires an applicable exchange rate for every time period for which there is a cash flow.

C)uses the current risk-free nominal rate to discount all cash flows related to a project.

D)stresses the use of the real rate of return to compute the net present value (NPV) of a project.

E)converts a foreign denominated NPV into a dollar denominated NPV.

A)generally produces more reliable results than those found using the foreign currency approach.

B)requires an applicable exchange rate for every time period for which there is a cash flow.

C)uses the current risk-free nominal rate to discount all cash flows related to a project.

D)stresses the use of the real rate of return to compute the net present value (NPV) of a project.

E)converts a foreign denominated NPV into a dollar denominated NPV.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

45

How many Euros can you get for $2,200 if one euro is worth $1.2762?

A)€1,638.09

B)€1,723.87

C)€2,676.67

D)€2,680.02

E)€2,684.15

A)€1,638.09

B)€1,723.87

C)€2,676.67

D)€2,680.02

E)€2,684.15

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

46

Assume that ¥95.42 equal $1.Also assume that SKr7.7274 equal $1.How many Japanese yen can you acquire in exchange for 3,000 Swedish krone?

A)¥235

B)¥261

C)¥37,045

D)¥39,024

E)¥39,520

A)¥235

B)¥261

C)¥37,045

D)¥39,024

E)¥39,520

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

47

You are planning a trip to Australia.Your hotel will cost you A$145 per night for seven nights.You expect to spend another A$2,800 for meals, tours, souvenirs, and so forth.How much will this trip cost you in U.S.dollars given the following exchange rates?

A)$2,559

B)$2,604

C)$2,631

D)$5,452

E)$5,688

A)$2,559

B)$2,604

C)$2,631

D)$5,452

E)$5,688

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following statements are correct?

I)The usage of forward rates increases the short-run exposure to exchange rate risk.

II)Accounting translation gains and losses are recorded in the equity section of the balance sheet.

III)The long-run exchange rate risk faced by an international firm can be reduced if a firm borrows money in the foreign country where the firm has operations.

IV)Unexpected changes in economic conditions are classified as short-run exposure to exchange rate risk.

A)I and III only

B)II and III only

C)I, II, and III only

D)II, III, and IV only

E)I, III, and IV only

I)The usage of forward rates increases the short-run exposure to exchange rate risk.

II)Accounting translation gains and losses are recorded in the equity section of the balance sheet.

III)The long-run exchange rate risk faced by an international firm can be reduced if a firm borrows money in the foreign country where the firm has operations.

IV)Unexpected changes in economic conditions are classified as short-run exposure to exchange rate risk.

A)I and III only

B)II and III only

C)I, II, and III only

D)II, III, and IV only

E)I, III, and IV only

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

49

The type of exchange rate risk known as translation exposure is best described as:

A)the risk that a positive net present value (NPV) project could turn into a negative NPV project because of changes in the exchange rate between two countries.

B)the problem encountered by an accountant of an international firm who is trying to record balance sheet account values.

C)the fluctuation in prices faced by importers of foreign goods.

D)the variance in relative pay rates based on the currency used to pay an employee.

E)the variance between the revenue of an exporter who uses forward rates and an equivalent exporter who does not use forward rates.

A)the risk that a positive net present value (NPV) project could turn into a negative NPV project because of changes in the exchange rate between two countries.

B)the problem encountered by an accountant of an international firm who is trying to record balance sheet account values.

C)the fluctuation in prices faced by importers of foreign goods.

D)the variance in relative pay rates based on the currency used to pay an employee.

E)the variance between the revenue of an exporter who uses forward rates and an equivalent exporter who does not use forward rates.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

50

You want to import $147,000 worth of rugs from India.How many rupees will you need to pay for this purchase if one rupee is worth $0.0203?

A)Rs 6,887,424

B)Rs 7,238,911

C)Rs 7,241,379

D)Rs 8,367,594

E)Rs 8,415,096

A)Rs 6,887,424

B)Rs 7,238,911

C)Rs 7,241,379

D)Rs 8,367,594

E)Rs 8,415,096

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

51

Today, you can get either 121 Canadian dollars or 1,288 Mexican pesos for 100 U.S.dollars.Last year, 100 U.S.dollars was worth 115 Canadian dollars or 1,291 Mexican pesos.Which one of the following statements is correct given this information?

A)$100 converted into Canadian dollars last year would now be worth $105.22.

B)$100 converted into Mexican pesos last year would now be worth $99.77.

C)$100 converted into Mexican pesos last year would now be worth $100.36.

D)$100 converted into Canadian dollars last year would now be worth $95.05.

E)$100 invested in Canadian dollars last year would now be worth $100.

A)$100 converted into Canadian dollars last year would now be worth $105.22.

B)$100 converted into Mexican pesos last year would now be worth $99.77.

C)$100 converted into Mexican pesos last year would now be worth $100.36.

D)$100 converted into Canadian dollars last year would now be worth $95.05.

E)$100 invested in Canadian dollars last year would now be worth $100.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

52

You have 100 British pounds.A friend of yours is willing to exchange 180 Canadian dollars for your 100 British pounds.What will be your profit or loss if you accept your friend's offer, given the following exchange rates?

A)£10.20 loss

B)£13.29 loss

C)£28.51 loss

D)£10.20 profit

E)£28.51 profit

A)£10.20 loss

B)£13.29 loss

C)£28.51 loss

D)£10.20 profit

E)£28.51 profit

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

53

The foreign currency approach to capital budgeting analysis:

I)is computationally easier to use than the home currency approach.

II)produces the same results as the home currency approach.

III)requires an exchange rate for each time period for which there is a cash flow.

IV)computes the NPV of a project in both the foreign and the domestic currency.

A)I and III only

B)II and IV only

C)I, II, and IV only

D)II, III, and IV only

E)I, II, III, and IV

I)is computationally easier to use than the home currency approach.

II)produces the same results as the home currency approach.

III)requires an exchange rate for each time period for which there is a cash flow.

IV)computes the NPV of a project in both the foreign and the domestic currency.

A)I and III only

B)II and IV only

C)I, II, and IV only

D)II, III, and IV only

E)I, II, III, and IV

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

54

The international Fisher effect states that _____ rates are equal across countries.

A)spot

B)one-year future

C)nominal

D)inflation

E)real

A)spot

B)one-year future

C)nominal

D)inflation

E)real

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

55

Today, you can exchange $1 for £0.6522.Last week, £1 was worth $1.6104.How much profit or loss would you now have if you had converted £100 into dollars last week?

A)loss of ₤1.57

B)loss of ₤0.39

C)loss of ₤0.07

D)profit of ₤5.03

E)profit of ₤5.59

A)loss of ₤1.57

B)loss of ₤0.39

C)loss of ₤0.07

D)profit of ₤5.03

E)profit of ₤5.59

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

56

The home currency approach:

A)discounts all of a project's foreign cash flows using the current spot rate.

B)employs uncovered interest parity to project future exchange rates.

C)computes the net present value (NPV) of a project in the foreign currency and then converts that NPV into U.S.dollars.

D)utilizes the international Fisher effect to compute the NPV of foreign cash flows in the foreign currency.

E)utilizes the international Fisher effect to compute the relevant exchange rates needed to compute the NPV of foreign cash flows in U.S.dollars.

A)discounts all of a project's foreign cash flows using the current spot rate.

B)employs uncovered interest parity to project future exchange rates.

C)computes the net present value (NPV) of a project in the foreign currency and then converts that NPV into U.S.dollars.

D)utilizes the international Fisher effect to compute the NPV of foreign cash flows in the foreign currency.

E)utilizes the international Fisher effect to compute the relevant exchange rates needed to compute the NPV of foreign cash flows in U.S.dollars.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

57

Which one of the following is a suggested method of reducing a U.S.importer's short-run exposure to exchange rate risk?

A)entering a forward exchange agreement timed to match the invoice date

B)investing U.S.dollars when an order is placed and using the investment proceeds to pay the invoice

C)exchanging funds on the spot market at the time an order is placed with a foreign supplier

D)exchanging funds on the spot market at the time an order is received

E) exchanging funds on the spot market at the time an invoice is payable

A)entering a forward exchange agreement timed to match the invoice date

B)investing U.S.dollars when an order is placed and using the investment proceeds to pay the invoice

C)exchanging funds on the spot market at the time an order is placed with a foreign supplier

D)exchanging funds on the spot market at the time an order is received

E) exchanging funds on the spot market at the time an invoice is payable

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

58

Assume you can buy 52 British pounds with 100 Canadian dollars.How much profit can you earn on a triangle arbitrage given the following rates if you start out with 100 U.S.dollars?

A)$0.78

B)$1.04

C)$1.33

D)$1.56

E)$1.64

A)$0.78

B)$1.04

C)$1.33

D)$1.56

E)$1.64

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

59

The camera you want to buy costs $230 in the U.S.How much will the identical camera cost in Canada if the exchange rate is C$1 = $0.8262? Assume absolute purchasing power parity exists.

A)$238.77

B)$242.19

C)$243.52

D)$248.60

E)$278.38

A)$238.77

B)$242.19

C)$243.52

D)$248.60

E)$278.38

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

60

Uncovered interest parity is defined as:

A)E(St) = S0 × [1 + (hFC - hUS)]t.

B)E(St) = S0 × [1 + (RFC - RUS)]t.

C)E(St) = S0 × [1 - (RFC - RUS)]t.

D)E(St) = S0 × [1 + (RUS - RFC)]t.

E)E(St) = S0 × [1 + (RFC + RUS)]t.

A)E(St) = S0 × [1 + (hFC - hUS)]t.

B)E(St) = S0 × [1 + (RFC - RUS)]t.

C)E(St) = S0 × [1 - (RFC - RUS)]t.

D)E(St) = S0 × [1 + (RUS - RFC)]t.

E)E(St) = S0 × [1 + (RFC + RUS)]t.

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

61

Assume the spot rate for the British pound currently is £0.6211 per $1.Also assume the one-year forward rate is £0.6347 per $1.A risk-free asset in the U.S.is currently earning 3.4 percent.If interest rate parity holds, what rate can you earn on a one-year risk-free British security?

A)1.18 percent

B)1.57 percent

C)3.67 percent

D)5.66 percent

E)5.92 percent

A)1.18 percent

B)1.57 percent

C)3.67 percent

D)5.66 percent

E)5.92 percent

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

62

In the spot market, $1 is currently equal to A$1.4910.Assume the expected inflation rate in Australia is 3.5 percent and in the U.S.4.0 percent.What is the expected exchange rate one year from now if relative purchasing power parity exists?

A)A$1.4810

B)A$1.4835

C)A$1.4875

D)A$1.4985

E)A$1.5005

A)A$1.4810

B)A$1.4835

C)A$1.4875

D)A$1.4985

E)A$1.5005

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

63

Assume the current spot rate is C$1.2103 and the one-year forward rate is C$1.1925.The nominal risk-free rate in Canada is 3 percent while it is 4 percent in the U.S.Using covered interest arbitrage you can earn an extra _____ profit over that which you would earn if you invested $1 in the U.S.

A)$0.005

B)$0.006

C)$0.008

D)$0.015

E)$0.018

A)$0.005

B)$0.006

C)$0.008

D)$0.015

E)$0.018

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

64

You are considering a project in Poland which has an initial cost of 275,000PLN.The project is expected to return a one-time payment of 390,000PLN four years from now.The risk-free rate of return is 4.5 percent in the U.S.and 3 percent in Poland.The inflation rate is 4 percent in the U.S.and 2 percent in Poland.Currently, you can buy 277PLN for 100USD.How much will the payment of 390,000PLN be worth in U.S.dollars four years from now?

A)$149,568

B)$180,560

C)$987,251

D)$1,016,926

E)$1,304,357

A)$149,568

B)$180,560

C)$987,251

D)$1,016,926

E)$1,304,357

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

65

You want to invest in a riskless project in Sweden.The project has an initial cost of SKr3.8million and is expected to produce cash inflows of SKr1.75 million a year for three years.The project will be worthless after three years.The expected inflation rate in Sweden is 3.2 percent while it is 4.3 percent in the U.S.A risk-free security is paying 5.5 percent in the U.S.The current spot rate is $1 = SKr7.7274.What is the net present value of this project in Swedish kroner? Assume the international Fisher effect applies.

A)SKr587,561

B)SKr701,458

C)SKr823,333

D)SKr958,029

E)SKr1,019,774

A)SKr587,561

B)SKr701,458

C)SKr823,333

D)SKr958,029

E)SKr1,019,774

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

66

Suppose the current spot rate for the Norwegian kroner is $1 = NKr6.7119.The expected inflation rate in Norway is 4 percent and in the U.S.3 percent.A risk-free asset in the U.S.is yielding 4.5 percent.What approximate real rate of return should you expect on a risk-free Norwegian security?

A)1.0 percent

B)1.5 percent

C)2.0 percent

D)2.5 percent

E)3.0 percent

A)1.0 percent

B)1.5 percent

C)2.0 percent

D)2.5 percent

E)3.0 percent

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

67

In the spot market, $1 is currently equal to £0.6211.Assume the expected inflation rate in the U.K.is 4.2 percent while it is 3.1 percent in the U.S.What is the expected exchange rate one year from now if relative purchasing power parity exists?

A)£0.6161

B)£0.6178

C)£0.6239

D)£0.6279

E)£0.6291

A)£0.6161

B)£0.6178

C)£0.6239

D)£0.6279

E)£0.6291

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

68

You are expecting a payment of 450,000PLN three years from now.The risk-free rate of return is 3 percent in the U.S.and 4 percent in Poland.The inflation rate is 2.5percent in the U.S.and 3 percent in Poland.Currently, you can buy 277PLN for 100USD.How much will the payment three years from now be worth in U.S.dollars?

A)$154,751

B)$157,677

C)$219,511

D)$1,317,269

E)$1,369,888

A)$154,751

B)$157,677

C)$219,511

D)$1,317,269

E)$1,369,888

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

69

The expected inflation rate in Finland is 2.8 percent while it is 3.2 percent in the U.S.A risk-free asset in the U.S.is yielding 4.9 percent.What approximate real rate of return should you expect on a risk-free Finnish security?

A)1.2 percent

B)1.7 percent

C)2.1 percent

D)2.5 percent

E)2.8 percent

A)1.2 percent

B)1.7 percent

C)2.1 percent

D)2.5 percent

E)2.8 percent

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

70

Assume that $1 can buy you either ¥95.42 or £0.6211.If a TV in London costs £990, what will that identical TV cost in Tokyo if absolute purchasing power parity exists?

A)¥58,797

B)¥60,554

C)¥152,094

D)¥161,855

E)¥163,542

A)¥58,797

B)¥60,554

C)¥152,094

D)¥161,855

E)¥163,542

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

71

In the spot market, $1 is currently equal to £0.6211.Assume the expected inflation rate in the U.K.is 2.6 percent while it is 4.3 percent in the U.S.What is the expected exchange rate four years from now if relative purchasing power parity exists?

A)£0.5799

B)£0.5822

C)£0.6105

D)£0.6623

E)£0.6644

A)£0.5799

B)£0.5822

C)£0.6105

D)£0.6623

E)£0.6644

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

72

Assume the current spot rate is C$1.1875 and the one-year forward rate is C$1.1724.The nominal risk-free rate in Canada is 4 percent while it is 3 percent in the U.S.Using covered interest arbitrage you can earn an extra _____ profit over that which you would earn if you invested $1 in the U.S.

A)$0.018

B)$0.023

C)$0.029

D)$0.031

E)$0.035

A)$0.018

B)$0.023

C)$0.029

D)$0.031

E)$0.035

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

73

A risk-free asset in the U.S.is currently yielding 4 percent while a Canadian risk-free asset is yielding 2 percent.Assume the current spot rate is C$1.2103.What is the approximate three-year forward rate if interest rate parity holds?

A)C$1.1391

B)C$1.1744

C)C$1.2241

D)C$1.2295

E)C$1.2470

A)C$1.1391

B)C$1.1744

C)C$1.2241

D)C$1.2295

E)C$1.2470

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

74

You are expecting a payment of C$100,000 four years from now.The risk-free rate of return is 3.8 percent in the U.S.and 4.1 percent in Canada.The inflation rate is 2 percent in the U.S.and 3 percent in Canada.Suppose the current exchange rate is C$1 = $0.8273.How much will the payment four years from now be worth in U.S.dollars?

A)$61,129

B)$62,414

C)$66,667

D)$78,202

E)$81,745

A)$61,129

B)$62,414

C)$66,667

D)$78,202

E)$81,745

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

75

You want to invest in a project in Canada.The project has an initial cost of C$2.2 million and is expected to produce cash inflows of C$900,000 a year for 3 years.The project will be worthless after the first 3 years.The expected inflation rate in Canada is 4 percent while it is only 3 percent in the U.S.The applicable interest rate for the project in Canada is 13 percent.The current spot rate is C$1 = $0.8158.What is the net present value of this project in Canadian dollars?

A)-C$91,889

B)-C$87,924

C)-C$74,963

D)C$165,139

E)C$167,528

A)-C$91,889

B)-C$87,924

C)-C$74,963

D)C$165,139

E)C$167,528

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

76

Suppose the current spot rate for the Norwegian kroner is $1 = NKr6.6869.The expected inflation rate in Norway is 6 percent and in the U.S.it is 3.1 percent.A risk-free asset in the U.S.is yielding 4 percent.What risk-free rate of return should you expect on a Norwegian security?

A)3.5 percent

B)4.0 percent

C)4.5 percent

D)5.0 percent

E)6.9 percent

A)3.5 percent

B)4.0 percent

C)4.5 percent

D)5.0 percent

E)6.9 percent

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

77

Assume the spot rate for the Japanese yen currently is ¥99.31 per $1 and the one-year forward rate is ¥97.62 per $1.A risk-free asset in Japan is currently earning 2.5 percent.If interest rate parity holds, approximately what rate can you earn on a one-year risk-free U.S.security?

A)1.63 percent

B)2.11 percent

C)4.20 percent

D)4.96 percent

E)5.01 percent

A)1.63 percent

B)2.11 percent

C)4.20 percent

D)4.96 percent

E)5.01 percent

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

78

A new coat costs 3,900 Russian rubles.How much will the identical coat cost in Euros if absolute purchasing power parity exists and the following exchange rates apply?

A)€97.23

B)€112.97

C)€119.05

D)€181.27

E)€183.99

A)€97.23

B)€112.97

C)€119.05

D)€181.27

E)€183.99

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

79

Assume the spot rate on the Canadian dollar is C$1.1847.The risk-free nominal rate in the U.S.is 5 percent while it is only 4 percent in Canada.What one-year forward rate will create interest rate parity?

A)C$1.1362

B)C$1.1429

C)C$1.1734

D)C$1.1799

E)C$1.1961

A)C$1.1362

B)C$1.1429

C)C$1.1734

D)C$1.1799

E)C$1.1961

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

80

Assume the spot rate on the Canadian dollar is C$0.9872.The risk-free nominal rate in the U.S.is 5.4 percent while it is only 4.2 percent in Canada.Which one of the following four-year forward rates best establishes the approximate interest rate parity condition?

A)C$0.9407

B)C$0.9608

C)C$1.0267

D)C$1.0519

E)C$1.0597

A)C$0.9407

B)C$0.9608

C)C$1.0267

D)C$1.0519

E)C$1.0597

Unlock Deck

Unlock for access to all 98 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 98 flashcards in this deck.