Deck 1: An Overview of the Investment Process

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the coefficient of variation for your portfolio.

A) 0.043

B) 0.12

C) 1.40

D) 0.69

E) 1.04

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the coefficient of variation for your portfolio.

A) 0.043

B) 0.12

C) 1.40

D) 0.69

E) 1.04

Question

Question

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.What is your expected rate of return [E(Rᵢ)] for next year?

A) 4.25%

B) 6.00%

C) 6.25%

D) 7.75%

E) 8.00%

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.What is your expected rate of return [E(Rᵢ)] for next year?

A) 4.25%

B) 6.00%

C) 6.25%

D) 7.75%

E) 8.00%

Question

Question

Use the Information Below for the Following Problem(S)

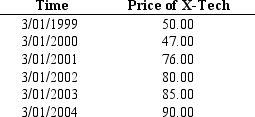

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your geometric mean annual yield for the investment in XMen?

A) 0.25

B) 0.40

C) 1.8

D) 0.1247

E) 0.1462

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your geometric mean annual yield for the investment in XMen?

A) 0.25

B) 0.40

C) 1.8

D) 0.1247

E) 0.1462

Question

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your annual holding period yield (Annual HPY)?

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your annual holding period yield (Annual HPY)?

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

Question

Question

Question

Question

Question

Given investments A and B with the following risk return characteristics,which one would you prefer and why?

A) Investment A because it has the highest expected return.

B) Investment A because it has the lowest relative risk.

C) Investment B because it has the lowest absolute risk.

D) Investment B because it has the lowest coefficient of variation.

E) Investment A because it has the highest coefficient of variation.

A) Investment A because it has the highest expected return.

B) Investment A because it has the lowest relative risk.

C) Investment B because it has the lowest absolute risk.

D) Investment B because it has the lowest coefficient of variation.

E) Investment A because it has the highest coefficient of variation.

Question

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your holding period return for the time period 3/1/1999 to 3/1/2004?

A) 0.1247

B) 1.8

C) 0.1462

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your holding period return for the time period 3/1/1999 to 3/1/2004?

A) 0.1247

B) 1.8

C) 0.1462

D) 0.40

E) 0.25

Question

Question

Question

Question

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the standard deviation of the rate of return for the one year period.

A) 0.65%

B) 1.45%

C) 4.0%

D) 6.25%

E) 6.4%

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the standard deviation of the rate of return for the one year period.

A) 0.65%

B) 1.45%

C) 4.0%

D) 6.25%

E) 6.4%

Question

Question

Question

Question

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your arithmetic mean annual yield for the investment in XMen Industries.

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your arithmetic mean annual yield for the investment in XMen Industries.

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

Question

Question

Question

Question

Question

Question

Question

Question

Use the Information Below for the Following Problem(S)

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

Refer to Exhibit 1.8.Calculate the HPY for stock 2.

A) 5%

B) 6%

C) 7%

D) 8%

E) 10%

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

Refer to Exhibit 1.8.Calculate the HPY for stock 2.

A) 5%

B) 6%

C) 7%

D) 8%

E) 10%

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/72

Play

Full screen (f)

Deck 1: An Overview of the Investment Process

1

In the phrase "nominal risk free rate," nominal means

A) Computed.

B) Historical.

C) Market.

D) Average.

E) Risk adverse.

A) Computed.

B) Historical.

C) Market.

D) Average.

E) Risk adverse.

C

2

The holding period return (HPR)is equal to the holding period yield (HPY)stated as a percentage.

False

3

The arithmetic mean is a superior measure of the long-term performance because it indicates the compound annual rate of return based on the ending value of the investment versus its beginning value.

False

4

The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

5

The geometric mean of a series of returns is always larger than the arithmetic mean and the difference increases with the volatility of the series.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

6

The coefficient of variation is a measure of

A) Central tendency.

B) Absolute variability.

C) Absolute dispersion.

D) Relative variability.

E) Relative return.

A) Central tendency.

B) Absolute variability.

C) Absolute dispersion.

D) Relative variability.

E) Relative return.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

7

An investment is the current commitment of dollars over time to derive future payments to compensate the investor for the time funds are committed,the expected rate of inflation and the uncertainty of future payments.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

8

The risk premium is a function of the volatility of operating earnings,sales volatility and inflation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

9

Nominal rates are averages of all possible real rates.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

10

The basic trade-off in the investment process is

A) between the anticipated rate of return for a given investment instrument and its degree of risk.

B) between understanding the nature of a particular investment and having the opportunity to purchase it.

C) between high returns available on single instruments and the diversification of instruments into a portfolio.

D) between the desired level of investment and possessing the resources necessary to carry it out.

E) None of the above.

A) between the anticipated rate of return for a given investment instrument and its degree of risk.

B) between understanding the nature of a particular investment and having the opportunity to purchase it.

C) between high returns available on single instruments and the diversification of instruments into a portfolio.

D) between the desired level of investment and possessing the resources necessary to carry it out.

E) None of the above.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

11

The nominal risk free rate of interest is a function of

A) The real risk free rate and the investment's variance.

B) The prime rate and the rate of inflation.

C) The T-bill rate plus the inflation rate.

D) The tax free rate plus the rate of inflation.

E) The real risk free rate and the rate of inflation.

A) The real risk free rate and the investment's variance.

B) The prime rate and the rate of inflation.

C) The T-bill rate plus the inflation rate.

D) The tax free rate plus the rate of inflation.

E) The real risk free rate and the rate of inflation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

12

Investors are willing to forgo current consumption in order to increase future consumption for a nominal rate of interest.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

13

The coefficient of variation is the expected return divided by the standard deviation of the expected return.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

14

The variance of expected returns is equal to the square root of the expected returns.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

15

The expected return is the average of all possible returns.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

16

The rate of exchange between future consumption and current consumption is

A) The nominal risk-free rate.

B) The coefficient of investment exchange.

C) The pure rate of interest.

D) The consumption/investment paradigm.

E) The expected rate of return.

A) The nominal risk-free rate.

B) The coefficient of investment exchange.

C) The pure rate of interest.

D) The consumption/investment paradigm.

E) The expected rate of return.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

17

The two most common calculations investors use to measure return performance are arithmetic means and geometric means.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

18

An individual who selects the investment that offers greater certainty when everything else is the same is known as a risk averse investor.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

19

Two measures of the risk premium are the standard deviation and the variance.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

20

The ____ the variance of returns,everything else remaining constant,the ____ the dispersion of expectations and the ____ the risk.

A) Larger, greater, lower

B) Larger, smaller, higher

C) Larger, greater, higher

D) Smaller, greater, lower

E) Smaller, greater, greater

A) Larger, greater, lower

B) Larger, smaller, higher

C) Larger, greater, higher

D) Smaller, greater, lower

E) Smaller, greater, greater

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

21

What will happen to the security market line (SML)if the following events occur,other things constant: (1)inflation expectations increase,and (2)investors become more risk averse?

A) Shift up and keep the same slope

B) Shift up and have less slope

C) Shift up and have a steeper slope

D) Shift down and keep the same slope

E) Shift down and have less slope

A) Shift up and keep the same slope

B) Shift up and have less slope

C) Shift up and have a steeper slope

D) Shift down and keep the same slope

E) Shift down and have less slope

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

22

The uncertainty of investment returns associated with how a firm finances its investments is known as

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is not a component of the required rate of return?

A) Expected rate of inflation

B) Time value of money

C) Risk

D) Holding period return

E) All of the above are components of the required rate of return

A) Expected rate of inflation

B) Time value of money

C) Risk

D) Holding period return

E) All of the above are components of the required rate of return

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

24

A decrease in the expected real growth in the economy,all other things constant,will cause the security market line to

A) Shift up

B) Shift down

C) Have a steeper slope

D) Have a flatter slope

E) Remain unchanged

A) Shift up

B) Shift down

C) Have a steeper slope

D) Have a flatter slope

E) Remain unchanged

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

25

All of the following are major sources of uncertainty EXCEPT

A) Business risk

B) Financial risk

C) Default risk

D) Country risk

E) Liquidity risk

A) Business risk

B) Financial risk

C) Default risk

D) Country risk

E) Liquidity risk

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

26

The total risk for a security can be measured by its

A) Beta with the market portfolio

B) Systematic risk

C) Standard deviation of returns

D) Unsystematic risk

E) Alpha with the market portfolio

A) Beta with the market portfolio

B) Systematic risk

C) Standard deviation of returns

D) Unsystematic risk

E) Alpha with the market portfolio

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

27

Unsystematic risk refers to risk that is

A) Undiversifiable

B) Diversifiable

C) Due to fundamental risk factors

D) Due to market risk

E) None of the above

A) Undiversifiable

B) Diversifiable

C) Due to fundamental risk factors

D) Due to market risk

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

28

Sources of risk for an investment include

A) Variance of returns and business risk

B) Coefficient of variation of returns and financial risk

C) Business risk and financial risk

D) Variance of returns and coefficient of variation of returns

E) All of the above

A) Variance of returns and business risk

B) Coefficient of variation of returns and financial risk

C) Business risk and financial risk

D) Variance of returns and coefficient of variation of returns

E) All of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

29

Modern portfolio theory assumes that most investors are

A) Risk averse

B) Risk neutral

C) Risk seekers

D) Risk tolerant

E) None of the above

A) Risk averse

B) Risk neutral

C) Risk seekers

D) Risk tolerant

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

30

The increase in yield spreads in late 2008 and early 2009 indicated that

A) Credit risk premiums decreased

B) Market risk premiums increased

C) Investors are more confident of the future cash flows of bonds

D) Non-investment grade bonds are less risky

E) Government bonds are no longer a risk free investment

A) Credit risk premiums decreased

B) Market risk premiums increased

C) Investors are more confident of the future cash flows of bonds

D) Non-investment grade bonds are less risky

E) Government bonds are no longer a risk free investment

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

31

The security market line (SML)graphs the expected relationship between

A) Business risk and financial risk

B) Systematic risk and unsystematic risk

C) Risk and return

D) Systematic risk and unsystematic return

E) None of the above

A) Business risk and financial risk

B) Systematic risk and unsystematic risk

C) Risk and return

D) Systematic risk and unsystematic return

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

32

The real risk-free rate is affected by a two factors;

A) The relative ease or tightness in capital markets and the expected rate of inflation.

B) The expected rate of inflation and the set of investment opportunities available in the economy.

C) The relative ease or tightness in capital markets and the set of investment opportunities available in the economy.

D) Time preference for income consumption and the relative ease or tightness in capital markets.

E) Time preference for income consumption and the set of investment opportunities available in the economy.

A) The relative ease or tightness in capital markets and the expected rate of inflation.

B) The expected rate of inflation and the set of investment opportunities available in the economy.

C) The relative ease or tightness in capital markets and the set of investment opportunities available in the economy.

D) Time preference for income consumption and the relative ease or tightness in capital markets.

E) Time preference for income consumption and the set of investment opportunities available in the economy.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

33

Measures of risk for an investment include

A) Variance of returns and business risk

B) Coefficient of variation of returns and financial risk

C) Business risk and financial risk

D) Variance of returns and coefficient of variation of returns

E) All of the above

A) Variance of returns and business risk

B) Coefficient of variation of returns and financial risk

C) Business risk and financial risk

D) Variance of returns and coefficient of variation of returns

E) All of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

34

If a significant change is noted in the yield of a T-bill,the change is most likely attributable to

A) A downturn in the economy.

B) A static economy.

C) A change in the expected rate of inflation.

D) A change in the real rate of interest.

E) A change in risk aversion.

A) A downturn in the economy.

B) A static economy.

C) A change in the expected rate of inflation.

D) A change in the real rate of interest.

E) A change in risk aversion.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is least likely to move a firm's position to the right on the Security Market Line (SML)?

A) An increase in the firm's beta

B) Adding more financial debt to the firm's balance sheet relative to equity

C) Changing the business strategy to include new product lines with more volatile expected cash flows

D) Investors perceive the stock as being more risky

E) An increase in the risk-free required rate of return.

A) An increase in the firm's beta

B) Adding more financial debt to the firm's balance sheet relative to equity

C) Changing the business strategy to include new product lines with more volatile expected cash flows

D) Investors perceive the stock as being more risky

E) An increase in the risk-free required rate of return.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

36

A decrease in the market risk premium,all other things constant,will cause the security market line to

A) Shift up

B) Shift down

C) Have a steeper slope

D) Have a flatter slope

E) Remain unchanged

A) Shift up

B) Shift down

C) Have a steeper slope

D) Have a flatter slope

E) Remain unchanged

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

37

The variability of operating earnings is associated with

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

38

Two factors that influence the nominal risk-free rate are;

A) The relative ease or tightness in capital markets and the expected rate of inflation.

B) The expected rate of inflation and the set of investment opportunities available in the economy.

C) The relative ease or tightness in capital markets and the set of investment opportunities available in the economy.

D) Time preference for income consumption and the relative ease or tightness in capital markets.

E) Time preference for income consumption and the set of investment opportunities available in the economy.

A) The relative ease or tightness in capital markets and the expected rate of inflation.

B) The expected rate of inflation and the set of investment opportunities available in the economy.

C) The relative ease or tightness in capital markets and the set of investment opportunities available in the economy.

D) Time preference for income consumption and the relative ease or tightness in capital markets.

E) Time preference for income consumption and the set of investment opportunities available in the economy.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is not a component of the risk premium?

A) Business risk

B) Financial risk

C) Liquidity risk

D) Exchange rate risk

E) Unsystematic market risk

A) Business risk

B) Financial risk

C) Liquidity risk

D) Exchange rate risk

E) Unsystematic market risk

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

40

The ability to sell an asset quickly at a fair price is associated with

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

A) Business risk.

B) Liquidity risk.

C) Exchange rate risk.

D) Financial risk.

E) Market risk.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

41

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the coefficient of variation for your portfolio.

A) 0.043

B) 0.12

C) 1.40

D) 0.69

E) 1.04

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the coefficient of variation for your portfolio.

A) 0.043

B) 0.12

C) 1.40

D) 0.69

E) 1.04

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

42

Use the Information Below for the Following Problem(S)

Suppose you bought a GM corporate bond on January 25, 2001 for $750, on January 25, 2004 sold it for $650.00.

Refer to Exhibit 1.2.What was your annual holding period return?

A) 0.8667

B) -0.1333

C) 0.0333

D) 0.9534

E) -0.0466

Suppose you bought a GM corporate bond on January 25, 2001 for $750, on January 25, 2004 sold it for $650.00.

Refer to Exhibit 1.2.What was your annual holding period return?

A) 0.8667

B) -0.1333

C) 0.0333

D) 0.9534

E) -0.0466

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

43

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.What is your expected rate of return [E(Rᵢ)] for next year?

A) 4.25%

B) 6.00%

C) 6.25%

D) 7.75%

E) 8.00%

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.What is your expected rate of return [E(Rᵢ)] for next year?

A) 4.25%

B) 6.00%

C) 6.25%

D) 7.75%

E) 8.00%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

44

Use the Information Below for the Following Problem(S)

Suppose you bought a GM corporate bond on January 25, 2001 for $750, on January 25, 2004 sold it for $650.00.

Refer to Exhibit 1.2.What was your annual holding period yield?

A) -0.0466

B) -0.1333

C) 0.0333

D) 0.3534

E) 0.8667

Suppose you bought a GM corporate bond on January 25, 2001 for $750, on January 25, 2004 sold it for $650.00.

Refer to Exhibit 1.2.What was your annual holding period yield?

A) -0.0466

B) -0.1333

C) 0.0333

D) 0.3534

E) 0.8667

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

45

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your geometric mean annual yield for the investment in XMen?

A) 0.25

B) 0.40

C) 1.8

D) 0.1247

E) 0.1462

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your geometric mean annual yield for the investment in XMen?

A) 0.25

B) 0.40

C) 1.8

D) 0.1247

E) 0.1462

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

46

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your annual holding period yield (Annual HPY)?

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your annual holding period yield (Annual HPY)?

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

47

Use the Information Below for the Following Problem(S)

You are provided with the following information:

Nominal return on risk-free asset = 4.5%

Expected return for asset i = 12.75%

Expected return on the market portfolio = 9.25%

Refer to Exhibit 1.6.Calculate the risk premium for the market portfolio.

A) 4.5%

B) 8.25%

C) 4.75%

D) 3.5%

E) None of the above

You are provided with the following information:

Nominal return on risk-free asset = 4.5%

Expected return for asset i = 12.75%

Expected return on the market portfolio = 9.25%

Refer to Exhibit 1.6.Calculate the risk premium for the market portfolio.

A) 4.5%

B) 8.25%

C) 4.75%

D) 3.5%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

48

Use the Information Below for the Following Problem(S)

Assume you bought 100 shares of NewTech common stock on January 15, 2003 at $50.00 per share and sold it on January 15, 2004 for $40.00 per share.

Refer to Exhibit 1.1.What was your holding period return?

A) -10%

B) -0.8

C) 25%

D) 0.8

E) -20%

Assume you bought 100 shares of NewTech common stock on January 15, 2003 at $50.00 per share and sold it on January 15, 2004 for $40.00 per share.

Refer to Exhibit 1.1.What was your holding period return?

A) -10%

B) -0.8

C) 25%

D) 0.8

E) -20%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

49

Use the Information Below for the Following Problem(S)

Assume that during the past year the consumer price index increased by 1.5 percent and the securities listed below returned the following nominal rates of return.

-Refer to Exhibit 1.5.If next year the real rates all rise by 10 percent while inflation climbs from 1.5 percent to 2.5 percent,what will be the nominal rate of return on each security?

A) 1.24% and 1.52%

B) 1.35% and 3.52%

C) 3.89% and 6.11%

D) 3.52% and 3.89%

E) 1.17% and 6.11%

Assume that during the past year the consumer price index increased by 1.5 percent and the securities listed below returned the following nominal rates of return.

-Refer to Exhibit 1.5.If next year the real rates all rise by 10 percent while inflation climbs from 1.5 percent to 2.5 percent,what will be the nominal rate of return on each security?

A) 1.24% and 1.52%

B) 1.35% and 3.52%

C) 3.89% and 6.11%

D) 3.52% and 3.89%

E) 1.17% and 6.11%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

50

Use the Information Below for the Following Problem(S)

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.T-bills.

A) 2.26%

B) 1.81%

C) -0.5%

D) 1.05%

E) None of the above

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.T-bills.

A) 2.26%

B) 1.81%

C) -0.5%

D) 1.05%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

51

Given investments A and B with the following risk return characteristics,which one would you prefer and why?

A) Investment A because it has the highest expected return.

B) Investment A because it has the lowest relative risk.

C) Investment B because it has the lowest absolute risk.

D) Investment B because it has the lowest coefficient of variation.

E) Investment A because it has the highest coefficient of variation.

A) Investment A because it has the highest expected return.

B) Investment A because it has the lowest relative risk.

C) Investment B because it has the lowest absolute risk.

D) Investment B because it has the lowest coefficient of variation.

E) Investment A because it has the highest coefficient of variation.

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

52

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your holding period return for the time period 3/1/1999 to 3/1/2004?

A) 0.1247

B) 1.8

C) 0.1462

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your holding period return for the time period 3/1/1999 to 3/1/2004?

A) 0.1247

B) 1.8

C) 0.1462

D) 0.40

E) 0.25

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

53

Use the Information Below for the Following Problem(S)

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.long-term bonds.

A) 3.06%

B) 2.27%

C) 2.51%

D) 3.5%

E) None of the above

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.long-term bonds.

A) 3.06%

B) 2.27%

C) 2.51%

D) 3.5%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

54

Use the Information Below for the Following Problem(S)

Assume that during the past year the consumer price index increased by 1.5 percent and the securities listed below returned the following nominal rates of return.

-Refer to Exhibit 1.5.What are the real rates of return for each of these securities?

A) 4.29% and 6.32%

B) 1.23% and 4.29%

C) 3.20% and 6.32%

D) 1.23% and 3.20%

E) 3.75% and 5.75%

Assume that during the past year the consumer price index increased by 1.5 percent and the securities listed below returned the following nominal rates of return.

-Refer to Exhibit 1.5.What are the real rates of return for each of these securities?

A) 4.29% and 6.32%

B) 1.23% and 4.29%

C) 3.20% and 6.32%

D) 1.23% and 3.20%

E) 3.75% and 5.75%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

55

Use the Information Below for the Following Problem(S)

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Compute the rate of inflation for the year 2009.

A) 2.42%

B) 4.0%

C) 1.69%

D) 1.24%

E) None of the above

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Compute the rate of inflation for the year 2009.

A) 2.42%

B) 4.0%

C) 1.69%

D) 1.24%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

56

Use the Information Below for the Following Problem(S)

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the standard deviation of the rate of return for the one year period.

A) 0.65%

B) 1.45%

C) 4.0%

D) 6.25%

E) 6.4%

You have concluded that next year the following relationships are possible:

Refer to Exhibit 1.4.Compute the standard deviation of the rate of return for the one year period.

A) 0.65%

B) 1.45%

C) 4.0%

D) 6.25%

E) 6.4%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

57

Use the Information Below for the Following Problem(S)

You are provided with the following information:

Nominal return on risk-free asset = 4.5%

Expected return for asset i = 12.75%

Expected return on the market portfolio = 9.25%

Refer to Exhibit 1.6.Calculate the risk premium for asset i.

A) 4.5%

B) 8.25%

C) 4.75%

D) 3.5%

E) None of the above

You are provided with the following information:

Nominal return on risk-free asset = 4.5%

Expected return for asset i = 12.75%

Expected return on the market portfolio = 9.25%

Refer to Exhibit 1.6.Calculate the risk premium for asset i.

A) 4.5%

B) 8.25%

C) 4.75%

D) 3.5%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

58

Use the Information Below for the Following Problem(S)

Assume you bought 100 shares of NewTech common stock on January 15, 2003 at $50.00 per share and sold it on January 15, 2004 for $40.00 per share.

Refer to Exhibit 1.1.What was your holding period yield?

A) -10%

B) -0.8

C) 25%

D) 0.8

E) -20%

Assume you bought 100 shares of NewTech common stock on January 15, 2003 at $50.00 per share and sold it on January 15, 2004 for $40.00 per share.

Refer to Exhibit 1.1.What was your holding period yield?

A) -10%

B) -0.8

C) 25%

D) 0.8

E) -20%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

59

If over the past 20 years the annual returns on the S&P 500 market index averaged 12% with a standard deviation of 18%,what was the coefficient of variation?

A) 0.6

B) 0.6%

C) 1.5

D) 1.5%

E) 0.66%

A) 0.6

B) 0.6%

C) 1.5

D) 1.5%

E) 0.66%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

60

Use the Information Below for the Following Problem(S)

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your arithmetic mean annual yield for the investment in XMen Industries.

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

The common stock of XMen Inc. had the following historic prices.

Refer to Exhibit 1.3.What was your arithmetic mean annual yield for the investment in XMen Industries.

A) 0.1462

B) 0.1247

C) 1.8

D) 0.40

E) 0.25

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

61

Use the Information Below for the Following Problem(S)

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.large-cap stocks.

A) 7.06%

B) 6.18%

C) 4.75%

D) 3.75%

E) None of the above

Consider the following information

Nominal annual return on U.S. government T-bills for year 2009 = 3.5%

Nominal annual return on U.S. government long-term bonds for year 2009 = 4.75%

Nominal annual return on U.S. large-cap stocks for year 2009= 8.75%

Consumer price index January 1, 2009 = 165

Consumer price index December 31, 2009 = 169

Refer to Exhibit 1.7.Calculate the annual real rate of return for U.S.large-cap stocks.

A) 7.06%

B) 6.18%

C) 4.75%

D) 3.75%

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

62

Economists project the long-run real growth rate for the next five years to be 2.5 percent and the average annual rate of inflation over this five year period to be 3 percent.What is the expected nominal rate of return over the next five years?

A) 0.500 percent

B) 1.056 percent

C) 2.750 percent

D) 5.500 percent

E) 5.575 percent

A) 0.500 percent

B) 1.056 percent

C) 2.750 percent

D) 5.500 percent

E) 5.575 percent

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

63

Use the Information Below for the Following Problem(S)

You purchased 100 shares of GE common stock on January 1, for $29 a share. A year later you received $1.25 in dividends per share and you sold it for $28 a share.

Refer to Exhibit 1.9.Calculate your holding period return (HPR)for this investment in GE stock.

A) 0.9655

B) 1.0086

C) 1.0357

D) 1.0804

E) 1.0973

You purchased 100 shares of GE common stock on January 1, for $29 a share. A year later you received $1.25 in dividends per share and you sold it for $28 a share.

Refer to Exhibit 1.9.Calculate your holding period return (HPR)for this investment in GE stock.

A) 0.9655

B) 1.0086

C) 1.0357

D) 1.0804

E) 1.0973

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

64

Use the Information Below for the Following Problem(S)

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the HPY for stock 1.

A) 10%

B) 20%

C) 15%

D) 12%

E) 7%

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the HPY for stock 1.

A) 10%

B) 20%

C) 15%

D) 12%

E) 7%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

65

Use the Information Below for the Following Problem(S)

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the standard deviation of the annual rate of return for Stock Z.

A) 0.0070

B) 0.0088

C) 0.0837

D) 0.0935

E) 0.1145

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the standard deviation of the annual rate of return for Stock Z.

A) 0.0070

B) 0.0088

C) 0.0837

D) 0.0935

E) 0.1145

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

66

Use the Information Below for the Following Problem(S)

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the coefficient of variation for Stock Z.

A) 0.837

B) 0.935

C) 1.070

D) 1.145

E) 1.281

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the coefficient of variation for Stock Z.

A) 0.837

B) 0.935

C) 1.070

D) 1.145

E) 1.281

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

67

Use the Information Below for the Following Problem(S)

You purchased 100 shares of GE common stock on January 1, for $29 a share. A year later you received $1.25 in dividends per share and you sold it for $28 a share.

Refer to Exhibit 1.9.Calculate your holding period yield (HPY)for this investment in GE stock.

A) -0.0345

B) -0.0090

C) 0.0086

D) 0.0643

E) 0.0804

You purchased 100 shares of GE common stock on January 1, for $29 a share. A year later you received $1.25 in dividends per share and you sold it for $28 a share.

Refer to Exhibit 1.9.Calculate your holding period yield (HPY)for this investment in GE stock.

A) -0.0345

B) -0.0090

C) 0.0086

D) 0.0643

E) 0.0804

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

68

Use the Information Below for the Following Problem(S)

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

Refer to Exhibit 1.8.Calculate the HPY for stock 2.

A) 5%

B) 6%

C) 7%

D) 8%

E) 10%

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

Refer to Exhibit 1.8.Calculate the HPY for stock 2.

A) 5%

B) 6%

C) 7%

D) 8%

E) 10%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

69

Use the Information Below for the Following Problem(S)

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the market weights for stock 1 and 2 based on period t values.

A) 39% for stock 1 and 61% for stock 2

B) 50% for stock 1 and 50% for stock 2

C) 71% for stock 1 and 29% for stock 2

D) 29% for stock 1 and 71% for stock 2

E) None of the above

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the market weights for stock 1 and 2 based on period t values.

A) 39% for stock 1 and 61% for stock 2

B) 50% for stock 1 and 50% for stock 2

C) 71% for stock 1 and 29% for stock 2

D) 29% for stock 1 and 71% for stock 2

E) None of the above

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

70

Use the Information Below for the Following Problem(S)

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the HPY for the portfolio.

A) 10.6%

B) 6.95%

C) 13.5%

D) 10%

E) 15.7%

Assume that you hold a two stock portfolio. You are provided with the following information on your holdings:

-Refer to Exhibit 1.8.Calculate the HPY for the portfolio.

A) 10.6%

B) 6.95%

C) 13.5%

D) 10%

E) 15.7%

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

71

Use the Information Below for the Following Problem(S)

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the geometric mean rate of return for Stock Z.

A) 0.051

B) 0.074

C) 0.096

D) 0.150

E) 1.090

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the geometric mean rate of return for Stock Z.

A) 0.051

B) 0.074

C) 0.096

D) 0.150

E) 1.090

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

72

Use the Information Below for the Following Problem(S)

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the arithmetic mean annual rate of return for Stock Z.

A) 0.03

B) 0.04

C) 0.06

D) 0.10

E) 0.40

The annual rates of return of Stock Z for the last four years are 0.10, 0.15, -0.05, and 0.20, respectively.

Refer to Exhibit 1.10.Compute the arithmetic mean annual rate of return for Stock Z.

A) 0.03

B) 0.04

C) 0.06

D) 0.10

E) 0.40

Unlock Deck

Unlock for access to all 72 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 72 flashcards in this deck.