Deck 11: Corporations-An Introduction

Full screen (f)

Question

Question

Question

Question

Question

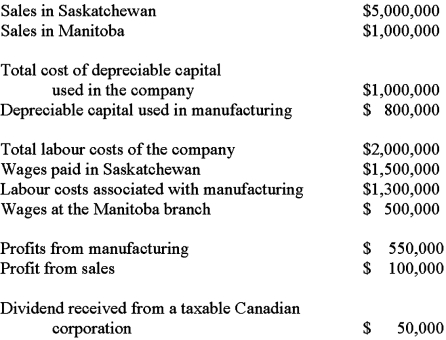

The Stevens Company is a public Canadian corporation that is primarily engaged in manufacturing.The company's head office is located in Saskatchewan.In 20X1,a small branch was established in Manitoba,to be used for sales purposes only.

In 20X2,the company's books showed the following: Required:

Required:

A)Calculate the company's net income for tax purposes for 20X2.

B)Calculate the company's taxable income,both federal and provincial.(Round all number to two decimal places.)

C)Calculate the manufacturing and processing profits for the company.

D)Calculate the federal tax liability.(Round all numbers to zero decimal points.)

In 20X2,the company's books showed the following:

Required:A)Calculate the company's net income for tax purposes for 20X2.

B)Calculate the company's taxable income,both federal and provincial.(Round all number to two decimal places.)

C)Calculate the manufacturing and processing profits for the company.

D)Calculate the federal tax liability.(Round all numbers to zero decimal points.)

Question

Question

Question

Question

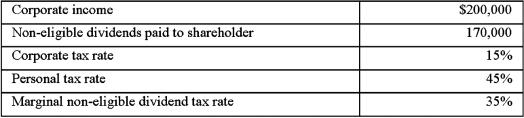

The Canadian tax system practices integration between corporations and individuals.Using the data in Table 1 and assumed rates,illustrate and explain the concept of integration.

Table 1

Table 1

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/10

Play

Full screen (f)

Deck 11: Corporations-An Introduction

1

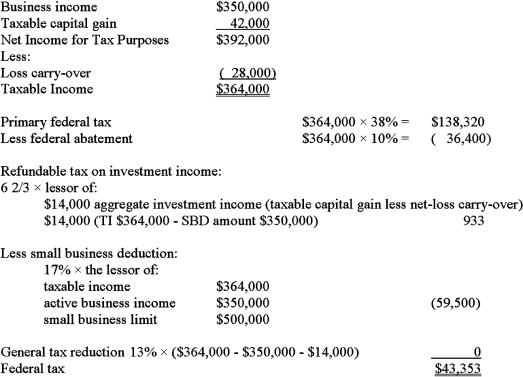

Johnson Co.is a CCPC with active business income of $350,000 in 20X2.The company engages in retail and wholesale activities.Capital gains in 20X0 were $84,000.

Johnson Co.will utilize a net capital loss carry-over of $28,000 on its 20X2

Johnson Co.will utilize a net capital loss carry-over of $28,000 on its 20X2

tax return.

Required:

Calculate the federal tax payable by Johnson Co.in 20X2.

Required:

Calculate the federal tax payable by Johnson Co.in 20X2.

2

Many corporations carry on business in more than one province.Assuming a corporation from Province A wishes to conduct business in Province B,the corporation will not have to pay tax in Province B if:

A)the parent corporation sets up a branch in Province B.

B)the permanent establishment in Province B has a lower sales to wage ratio than the ratio in Province A.

C)a branch treaty exists between the two provinces.

D)business is conducted with the other province by way of direct sales from Province A.

A)the parent corporation sets up a branch in Province B.

B)the permanent establishment in Province B has a lower sales to wage ratio than the ratio in Province A.

C)a branch treaty exists between the two provinces.

D)business is conducted with the other province by way of direct sales from Province A.

D

3

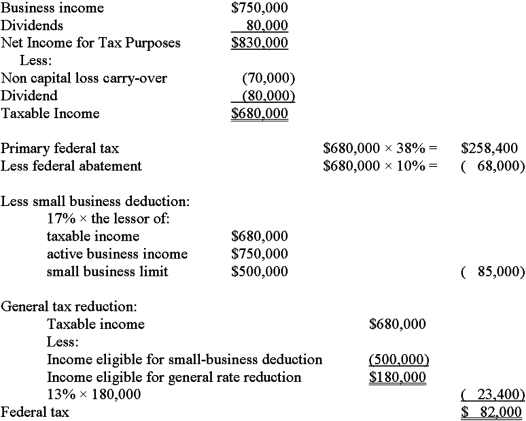

Bride and Groom Co.is a Canadian controlled private corporation with active business income of $750,000.The company is in the business of producing and selling bridal wear.Dividends were received from a taxable Canadian corporation in the amount of $80,000.

Additional information is as follows:

Net capital loss carry-over balance is $200,000.

Non capital loss carry-over balance is $70,000.

Required:

Calculate the minimum federal Part I tax payable by Bride and Groom Co.

Additional information is as follows:

Net capital loss carry-over balance is $200,000.

Non capital loss carry-over balance is $70,000.

Required:

Calculate the minimum federal Part I tax payable by Bride and Groom Co.

for the year.

4

Which of the following is false with regard to dividends,corporations,and shareholders?

A) Corporate taxable income is generally reduced by the amount of dividends received from other taxable Canadian corporations.

B) An individual's taxable income is generally reduced by the amount of dividends received from taxable Canadian corporations.

C) Corporate taxable income is generally reduced by the amount of dividends received from affiliated foreign corporations.

D) Generally, Canadian corporate after-tax profits may be shifted to other Canadian corporations by way of dividends, without a tax consequence.

A) Corporate taxable income is generally reduced by the amount of dividends received from other taxable Canadian corporations.

B) An individual's taxable income is generally reduced by the amount of dividends received from taxable Canadian corporations.

C) Corporate taxable income is generally reduced by the amount of dividends received from affiliated foreign corporations.

D) Generally, Canadian corporate after-tax profits may be shifted to other Canadian corporations by way of dividends, without a tax consequence.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

5

The Stevens Company is a public Canadian corporation that is primarily engaged in manufacturing.The company's head office is located in Saskatchewan.In 20X1,a small branch was established in Manitoba,to be used for sales purposes only.

In 20X2,the company's books showed the following: Required:

A)Calculate the company's net income for tax purposes for 20X2.

B)Calculate the company's taxable income,both federal and provincial.(Round all number to two decimal places.)

C)Calculate the manufacturing and processing profits for the company.

D)Calculate the federal tax liability.(Round all numbers to zero decimal points.)

In 20X2,the company's books showed the following:

Required:A)Calculate the company's net income for tax purposes for 20X2.

B)Calculate the company's taxable income,both federal and provincial.(Round all number to two decimal places.)

C)Calculate the manufacturing and processing profits for the company.

D)Calculate the federal tax liability.(Round all numbers to zero decimal points.)

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements accurately describes the tax treatment for Canadian corporations?

A) Public and private Canadian corporations are eligible for the small business deduction.

B) Public and private Canadian corporations are eligible for the general tax reduction.

C) Public corporations are granted beneficial tax treatment on the first $500,000 of business income.

D) CCPCs recognize the general tax reduction on all business income.

A) Public and private Canadian corporations are eligible for the small business deduction.

B) Public and private Canadian corporations are eligible for the general tax reduction.

C) Public corporations are granted beneficial tax treatment on the first $500,000 of business income.

D) CCPCs recognize the general tax reduction on all business income.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

7

Using general terms,explain how a change in control of a corporation can affect the net-capital losses and the non-capital losses.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

8

When shares are transferred from one group of shareholders to another and there is a change in control,which of the following is correct?

A) Any net capital losses that arise following the change in control will be lost.

B) Non-capital losses are automatically deemed to have expired.

C) Net capital losses arising prior to the change in control will be lost and any non-capital losses arising prior to the change in control may be used if the business that incurred the loss is terminated.

D) Non-capital business losses arising prior to the change in control may be used against income from the business that incurred the loss if that business is carried on at a profit or reasonable expectation of profit in the year in which the losses are applied.

A) Any net capital losses that arise following the change in control will be lost.

B) Non-capital losses are automatically deemed to have expired.

C) Net capital losses arising prior to the change in control will be lost and any non-capital losses arising prior to the change in control may be used if the business that incurred the loss is terminated.

D) Non-capital business losses arising prior to the change in control may be used against income from the business that incurred the loss if that business is carried on at a profit or reasonable expectation of profit in the year in which the losses are applied.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

9

The Canadian tax system practices integration between corporations and individuals.Using the data in Table 1 and assumed rates,illustrate and explain the concept of integration.

Table 1

Table 1

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

10

In 20X0,Coffee Co.recognized $37,000 in business income and $1,000 in taxable capital gains.In 20X1,the company incurred a business loss of $25,000,a taxable capital gain of $2,000,and an allowable capital loss of $5,000.Business income for 20X2 was $50,000,taxable capital gains were $4,000,and the company received $10,000 in dividends from a taxable Canadian corporation.Assuming Coffee Co.utilizes any unused losses in the earliest years possible,which of the following taxable incomes are correct,after all carry-over adjustments have been made?

A) 20X0: $12,000; 20X1: $0; 20X2: $52,000

B) 20X0: $38,000; 20X1: ($28,000); 20X2: $64,000

C) 20X0: $13,000; 20X1: ($2,000); 20X2: $62,000

D) 20X0: $37,000; 20X1: $0; 20X2: $27,000

A) 20X0: $12,000; 20X1: $0; 20X2: $52,000

B) 20X0: $38,000; 20X1: ($28,000); 20X2: $64,000

C) 20X0: $13,000; 20X1: ($2,000); 20X2: $62,000

D) 20X0: $37,000; 20X1: $0; 20X2: $27,000

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 10 flashcards in this deck.