Deck 18: Related-Party Disclosures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

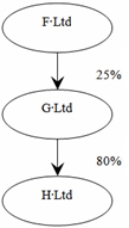

The following diagram shows three companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and G, and G and H are related parties.

B)F and G, G and H, and F and H are related parties.

C)Only G and H are related parties.

D)Only F and H are related parties.

A)F and G, and G and H are related parties.

B)F and G, G and H, and F and H are related parties.

C)Only G and H are related parties.

D)Only F and H are related parties.

Question

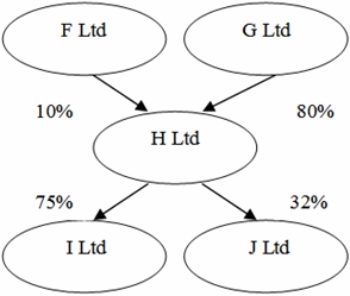

The following diagram shows five companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and H, G and H, H and I, I and J are related parties.

B)G and H, H and I, H and J, J and G are related parties.

C)G and H, H and I, H and J, J and G, F and H are related parties.

D)G and H, H and I, H and J, J and G, I and J are related parties.

A)F and H, G and H, H and I, I and J are related parties.

B)G and H, H and I, H and J, J and G are related parties.

C)G and H, H and I, H and J, J and G, F and H are related parties.

D)G and H, H and I, H and J, J and G, I and J are related parties.

Question

Question

Question

Question

Question

Question

Question

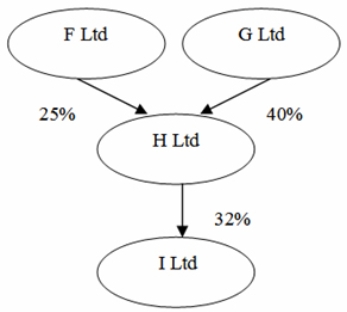

The following diagram shows four companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and H, G and H, H and I are related parties.

B)F and G, F and H, G and H, H and I are related parties.

C)F and G, F and H, G and H, H and I, I and G are related parties.

D)F and G, F and H, G and H, H and I, I and G, I and F are related parties.

A)F and H, G and H, H and I are related parties.

B)F and G, F and H, G and H, H and I are related parties.

C)F and G, F and H, G and H, H and I, I and G are related parties.

D)F and G, F and H, G and H, H and I, I and G, I and F are related parties.

Question

Question

Question

Question

Question

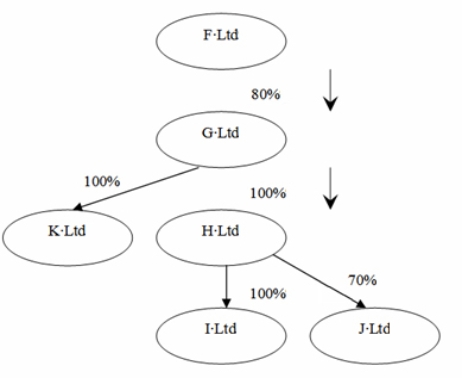

In the following diagram,which entities would be included in a wholly owned group according to the definition in IAS 24?

A)F Ltd, G Ltd, H Ltd, I Ltd

B)F Ltd, G Ltd, K Ltd, H Ltd, I Ltd

C)G Ltd, K Ltd, H Ltd, I Ltd

D)G Ltd, K Ltd, H Ltd, I Ltd, J Ltd

A)F Ltd, G Ltd, H Ltd, I Ltd

B)F Ltd, G Ltd, K Ltd, H Ltd, I Ltd

C)G Ltd, K Ltd, H Ltd, I Ltd

D)G Ltd, K Ltd, H Ltd, I Ltd, J Ltd

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 18: Related-Party Disclosures

1

A frequently applied practice in relation to the disclosure of related-party transactions of directors is to:

A)make a general statement that there were some transactions.

B)not report that there were any transactions.

C)state that the transaction is at arm's length terms and conditions.

D)specify the number, nature and amount of the transactions with comparisons to arm's length transactions of a similar nature and type.

A)make a general statement that there were some transactions.

B)not report that there were any transactions.

C)state that the transaction is at arm's length terms and conditions.

D)specify the number, nature and amount of the transactions with comparisons to arm's length transactions of a similar nature and type.

C

2

In order for control to exist as the basis for a related-party disclosure the capacity to control must have been demonstrated as having been exercised in the past.

False

3

Good corporate governance recommends a renumeration report be included in the financial statements.

True

4

Transactions involving related parties cannot be presumed to be carried out on an arm's length basis.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

Entities that have a controlling entity in common are considered to be 'other related parties'.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

A close family member of someone who is key management personnel is considered to be a related party.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Reasons for the requirement to disclose related-party transactions include:

A)the risk that the performance and position of the reporting entity will be negatively affected by the transactions.

B)key stakeholders of the entity include related parties who should be kept informed of their transactions.

C)they may be used to minimise total taxation payable by a group of related entities.

D)the risk that the performance and position of the reporting entity will be negatively affected by the transactions and related-party transactions may be used to minimise total taxation payable by a group of related entities.

A)the risk that the performance and position of the reporting entity will be negatively affected by the transactions.

B)key stakeholders of the entity include related parties who should be kept informed of their transactions.

C)they may be used to minimise total taxation payable by a group of related entities.

D)the risk that the performance and position of the reporting entity will be negatively affected by the transactions and related-party transactions may be used to minimise total taxation payable by a group of related entities.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

IAS 24 reflects the view that transactions carried out by related parties cannot be presumed to be at arm's length.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

A major supplier with whom an entity transacts a significant volume of business is considered a related party in IAS 24 Related Party Disclosures.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

A related party relationship can affect the profit and loss of an entity.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

An alternate director who is not acting in that capacity is considered a related party in IAS 24.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

The most common example of a relationship reflecting control is that between an investor and its associate company.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

In IAS 24 Related Party Disclosures,two entities having a director in common are assumed related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Reasons for the requirement to disclose related-party transactions include:

A)These transactions will always be eliminated in a consolidation so otherwise there would be no record of them in a set of consolidated accounts.

B)There is a history of corporate scandals involving related-party transactions in Europe, Australia, the US, and Canada.

C)There is a risk that the auditor may be a related party and this must be disclosed.

D)There is a history of corporate scandals involving related-party transactions in Europe, Australia, the US, and Canada and a risk that the auditor may be a related party and this must be disclosed.

A)These transactions will always be eliminated in a consolidation so otherwise there would be no record of them in a set of consolidated accounts.

B)There is a history of corporate scandals involving related-party transactions in Europe, Australia, the US, and Canada.

C)There is a risk that the auditor may be a related party and this must be disclosed.

D)There is a history of corporate scandals involving related-party transactions in Europe, Australia, the US, and Canada and a risk that the auditor may be a related party and this must be disclosed.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

A related-party transaction is material if:

A)Its omission from the report or misstatement would result in significant financial disadvantage to a third party, whether it be an owner, debt-holder or other stakeholder, or if it involves the auditor.

B)Its omission, non-disclosure or misstatement has the potential to affect decisions about the allocation of scarce resources by users of the accounts and consolidated accounts, or the discharge of accountability by directors or if it is a transaction by a director with the reporting entity.

C)Its omission from the report or misstatement would result in the accounts not providing an accurate representation of the financial position or performance of the reporting entity, or if it is a transaction by any member of the senior management of the reporting entity.

D)Its omission, non-disclosure or misstatement has the potential to affect decisions about the allocation of scarce resources by users of the accounts and consolidated accounts, or the discharge of accountability by directors.

A)Its omission from the report or misstatement would result in significant financial disadvantage to a third party, whether it be an owner, debt-holder or other stakeholder, or if it involves the auditor.

B)Its omission, non-disclosure or misstatement has the potential to affect decisions about the allocation of scarce resources by users of the accounts and consolidated accounts, or the discharge of accountability by directors or if it is a transaction by a director with the reporting entity.

C)Its omission from the report or misstatement would result in the accounts not providing an accurate representation of the financial position or performance of the reporting entity, or if it is a transaction by any member of the senior management of the reporting entity.

D)Its omission, non-disclosure or misstatement has the potential to affect decisions about the allocation of scarce resources by users of the accounts and consolidated accounts, or the discharge of accountability by directors.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

IAS 24 Related Party Disclosures,requires relationships between parents and subsidiaries be disclosed irrespective of whether there have been transactions between those related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

Related parties are not considered to be interdependent.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

In order for two parties to be related they must be under the common control or influence of a third party.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

Related-party transactions pose serious risks to the reporting entity and generate no benefits.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

IAS 24 requires a standard,detailed set of disclosure requirements for all related-party transactions.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

The disclosure requirements of IAS 24 include:

A)disclosure of the fair value of a transaction with a related party.

B)restatement of the transaction to its fair value in the accounts of the entity.

C)comparative transactions with non-related parties to form a basis for a fair value assessment by users of the accounts.

D)none of the given answers.

A)disclosure of the fair value of a transaction with a related party.

B)restatement of the transaction to its fair value in the accounts of the entity.

C)comparative transactions with non-related parties to form a basis for a fair value assessment by users of the accounts.

D)none of the given answers.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

Disclosure information under IAS 24 is aggregated by:

A)forex currency base, size of the transaction and class of related party.

B)size of the transaction, type of transaction and frequency of the transaction.

C)type of transaction, nature of terms and conditions and class of related party.

D)nature of terms and conditions, class of related party and frequency of the transaction.

A)forex currency base, size of the transaction and class of related party.

B)size of the transaction, type of transaction and frequency of the transaction.

C)type of transaction, nature of terms and conditions and class of related party.

D)nature of terms and conditions, class of related party and frequency of the transaction.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

The disclosures that IAS 24 requires for other related parties are:

A)limited to the aggregate amount, nature and type of transaction.

B)largely the same as the disclosure requirements for directors of the entity.

C)fairly consistent with the requirements for the wholly owned group.

D)limited to the nature and terms and conditions of each different type of transaction.

A)limited to the aggregate amount, nature and type of transaction.

B)largely the same as the disclosure requirements for directors of the entity.

C)fairly consistent with the requirements for the wholly owned group.

D)limited to the nature and terms and conditions of each different type of transaction.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following transactions is usually not considered a 'related party' in IAS 24?

A)leasing arrangement with a local government

B)sale of inventory to a subsidiary

C)write-off of an immaterial loan to a director

D)sale of non-current assets to an associate

A)leasing arrangement with a local government

B)sale of inventory to a subsidiary

C)write-off of an immaterial loan to a director

D)sale of non-current assets to an associate

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

The disclosure requirements of IAS 24 are grouped in part by:

A)currency of transaction-transactions should be grouped by currency of the transaction so that users can identify any forex risk associated.

B)size-three broad categories of disclosure are required depending on the percentage size of the transaction relative to the turnover of the entity.The categories are 0.5 per cent-9 per cent, 10 per cent-20 per cent, 21 per cent and over.

C)frequency-transactions repeated during the period are distinguished from one-off transactions.

D)subsidiaries, associates-joint venturers in which the entity is a joint venturer.

A)currency of transaction-transactions should be grouped by currency of the transaction so that users can identify any forex risk associated.

B)size-three broad categories of disclosure are required depending on the percentage size of the transaction relative to the turnover of the entity.The categories are 0.5 per cent-9 per cent, 10 per cent-20 per cent, 21 per cent and over.

C)frequency-transactions repeated during the period are distinguished from one-off transactions.

D)subsidiaries, associates-joint venturers in which the entity is a joint venturer.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Some business leaders argue that related-party transactions have benefits for the reporting entity.The benefits are said to include:

A)lower legal costs associated with contracts.

B)increased profits for the related entity.

C)reduced competition among suppliers.

D)better, more reliable service and better prices.

A)lower legal costs associated with contracts.

B)increased profits for the related entity.

C)reduced competition among suppliers.

D)better, more reliable service and better prices.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

The following diagram shows three companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and G, and G and H are related parties.

B)F and G, G and H, and F and H are related parties.

C)Only G and H are related parties.

D)Only F and H are related parties.

A)F and G, and G and H are related parties.

B)F and G, G and H, and F and H are related parties.

C)Only G and H are related parties.

D)Only F and H are related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

The following diagram shows five companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and H, G and H, H and I, I and J are related parties.

B)G and H, H and I, H and J, J and G are related parties.

C)G and H, H and I, H and J, J and G, F and H are related parties.

D)G and H, H and I, H and J, J and G, I and J are related parties.

A)F and H, G and H, H and I, I and J are related parties.

B)G and H, H and I, H and J, J and G are related parties.

C)G and H, H and I, H and J, J and G, F and H are related parties.

D)G and H, H and I, H and J, J and G, I and J are related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

According to IAS 24,disclosures required for transactions with related parties in the wholly owned group include:

A)the aggregate amounts receivable from and payable to related parties as at the reporting date classified into current and non-current categories.

B)aggregate number of shares and options held by the related party as at the reporting date including the class of share, unit, option or other equity instrument.

C)the nature of terms and conditions of share and option transactions.

D)the fair value of any equity transaction with any related party as at the reporting date.

A)the aggregate amounts receivable from and payable to related parties as at the reporting date classified into current and non-current categories.

B)aggregate number of shares and options held by the related party as at the reporting date including the class of share, unit, option or other equity instrument.

C)the nature of terms and conditions of share and option transactions.

D)the fair value of any equity transaction with any related party as at the reporting date.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

IAS 24 defines directors as including:

A)any employee of the entity whether or not they are validly appointed to occupy the position.

B)any person that directs an entity in its financial and operating activities regardless of whether they are known by the title of director.

C)any person in accordance with whose instructions the directors of an entity are accustomed to act.

D)any person that directs an entity in its financial and operating activities regardless of whether they are known by the title of director and any person in accordance with whose instructions the directors of an entity are accustomed to act.

A)any employee of the entity whether or not they are validly appointed to occupy the position.

B)any person that directs an entity in its financial and operating activities regardless of whether they are known by the title of director.

C)any person in accordance with whose instructions the directors of an entity are accustomed to act.

D)any person that directs an entity in its financial and operating activities regardless of whether they are known by the title of director and any person in accordance with whose instructions the directors of an entity are accustomed to act.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

The definition of related parties relies on three key terms.These are:

A)directors, control and significant influence.

B)input, effect and common control.

C)authorised trustee corporations, material influence and control.

D)common control, directors and material influence.

A)directors, control and significant influence.

B)input, effect and common control.

C)authorised trustee corporations, material influence and control.

D)common control, directors and material influence.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

IAS 24 defines control as:

A)the exercise of power to direct the decision making of another entity in relation to financial and operational decisions so as to enable the controlling entity to benefit as a result.

B)the capacity to influence the financial and operational decision making of another entity through the board of directors so as to achieve the co-operation of the other entity in obtaining the ends of the controlling entity.

C)the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

D)the potential ability to obtain desired outcomes through another entity by influence through representatives on the governing board of the other entity.

A)the exercise of power to direct the decision making of another entity in relation to financial and operational decisions so as to enable the controlling entity to benefit as a result.

B)the capacity to influence the financial and operational decision making of another entity through the board of directors so as to achieve the co-operation of the other entity in obtaining the ends of the controlling entity.

C)the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

D)the potential ability to obtain desired outcomes through another entity by influence through representatives on the governing board of the other entity.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

The disclosures required by IAS 24 for key management personnel include:

A)the name of the person.

B)the position held.

C)dates identifying the period of responsibility.

D)all of the given answers.

A)the name of the person.

B)the position held.

C)dates identifying the period of responsibility.

D)all of the given answers.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Tests to indicate whether significant influence exits include:

A)participating in decisions on the distribution or retention of the associate's profits.

B)the ability to dominate the decision making of the board of directors.

C)the extent of ownership interest between the entities.

D)participating in decisions on the distribution or retention of the associate's profits and the extent of ownership interest between the entities.

A)participating in decisions on the distribution or retention of the associate's profits.

B)the ability to dominate the decision making of the board of directors.

C)the extent of ownership interest between the entities.

D)participating in decisions on the distribution or retention of the associate's profits and the extent of ownership interest between the entities.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

The following diagram shows four companies and their associated equity ownership percentages.Which of the companies shown would most likely be considered related entities?

A)F and H, G and H, H and I are related parties.

B)F and G, F and H, G and H, H and I are related parties.

C)F and G, F and H, G and H, H and I, I and G are related parties.

D)F and G, F and H, G and H, H and I, I and G, I and F are related parties.

A)F and H, G and H, H and I are related parties.

B)F and G, F and H, G and H, H and I are related parties.

C)F and G, F and H, G and H, H and I, I and G are related parties.

D)F and G, F and H, G and H, H and I, I and G, I and F are related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

Significant influence is defined in IAS 24 as:

A)a majority ownership relationship such that the parent entity is able to dominate the decision making of the other entity.

B)the exercised ability to materially affect the financial and operational decisions of another entity.

C)the influence that is attached to owning a parcel of shares or other equity instruments of another entity.

D)the power to participate in the financial and operating policy decisions of an entity, but not the control over those policies.

A)a majority ownership relationship such that the parent entity is able to dominate the decision making of the other entity.

B)the exercised ability to materially affect the financial and operational decisions of another entity.

C)the influence that is attached to owning a parcel of shares or other equity instruments of another entity.

D)the power to participate in the financial and operating policy decisions of an entity, but not the control over those policies.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

The definition of related parties under IAS 24 excludes entities (other than those specified earlier in the relevant paragraph)where the related-party relationship:

A)is a relationship formed more than 5 years prior to the current reporting period.

B)results solely from normal dealings of local governments.

C)is a commonly known and transparent link between entities in the public sphere.

D)is based on a relationship to the directors through marriage only.

A)is a relationship formed more than 5 years prior to the current reporting period.

B)results solely from normal dealings of local governments.

C)is a commonly known and transparent link between entities in the public sphere.

D)is based on a relationship to the directors through marriage only.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

If there had been a related-party transaction during the period,the disclosures required by IAS 24 director-related entities include:

A)annual income in aggregate amount and the number in £10 000 bands.

B)retirement benefits.

C)aggregate number of shares, units, options and other equity instruments acquired and disposed of, by issuing entity and class of share, unit, option or equity instrument.

D)their names.

A)annual income in aggregate amount and the number in £10 000 bands.

B)retirement benefits.

C)aggregate number of shares, units, options and other equity instruments acquired and disposed of, by issuing entity and class of share, unit, option or equity instrument.

D)their names.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

The commentary to IAS 24 identifies factors that would normally indicate the existence of control.These factors include:

A)the capacity to withdraw a material amount of loan capital.

B)the power to dominate the composition of the board of directors or governing body.

C)the authority to determine the outcome of significant local council decisions relevant to the entity.

D)the capacity to withdraw a material amount of loan capital and the power to dominate the composition of the board of directors or governing body.

A)the capacity to withdraw a material amount of loan capital.

B)the power to dominate the composition of the board of directors or governing body.

C)the authority to determine the outcome of significant local council decisions relevant to the entity.

D)the capacity to withdraw a material amount of loan capital and the power to dominate the composition of the board of directors or governing body.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

In the following diagram,which entities would be included in a wholly owned group according to the definition in IAS 24?

A)F Ltd, G Ltd, H Ltd, I Ltd

B)F Ltd, G Ltd, K Ltd, H Ltd, I Ltd

C)G Ltd, K Ltd, H Ltd, I Ltd

D)G Ltd, K Ltd, H Ltd, I Ltd, J Ltd

A)F Ltd, G Ltd, H Ltd, I Ltd

B)F Ltd, G Ltd, K Ltd, H Ltd, I Ltd

C)G Ltd, K Ltd, H Ltd, I Ltd

D)G Ltd, K Ltd, H Ltd, I Ltd, J Ltd

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following statements is not in accordance with IAS 24 Related Party Disclosures?

A)A related-party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged.

B)If there have been transactions between related parties, an entity shall disclose the nature of the related party relationship as well as information about the transactions and outstanding balances necessary for an understanding of the potential effect of the relationship on the financial statements.

C)Transactions between the reporting entity and its key management personnel are deemed material.

D)In IAS 24 Related Party Disclosures, two entities having a director in common are assumed related parties.

A)A related-party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged.

B)If there have been transactions between related parties, an entity shall disclose the nature of the related party relationship as well as information about the transactions and outstanding balances necessary for an understanding of the potential effect of the relationship on the financial statements.

C)Transactions between the reporting entity and its key management personnel are deemed material.

D)In IAS 24 Related Party Disclosures, two entities having a director in common are assumed related parties.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following disclosures on key management personnel is/are required in IAS 24 for disclosing entities?

A)name of the person

B)position held

C)qualification(s) of the person

D)name of the person and position held

A)name of the person

B)position held

C)qualification(s) of the person

D)name of the person and position held

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

Tennant Creek Plc has following transactions during the year: Which of the following lists all the related-party transactions that are required to be disclosed in IAS 24 Related Party Disclosures?

A)I and III

B)III and V

C)II, III and IV

D)I, IV and V

A)I and III

B)III and V

C)II, III and IV

D)I, IV and V

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

The definition of control adopted in IAS 24 relies on the power to:

A)agree.

B)govern.

C)vote.

D)manage.

A)agree.

B)govern.

C)vote.

D)manage.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following parties is/are covered by the definition of a related party in IAS 24?

A)independent directors

B)chief executive officer

C)son-in-law of an executive director

D)all of the given answers

A)independent directors

B)chief executive officer

C)son-in-law of an executive director

D)all of the given answers

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

What is the rationale for disclosing related-party transactions with key management personnel regardless of its materiality?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

Directors' income is defined in IAS 24 as including only:

A)the regularly paid salary of the directors.

B)the regularly paid salary, any bonuses paid and retirement benefits.

C)bonuses, commissions or salaries, retirement benefits and any brokerage or commission made on the subscription or agreement to subscribe to equity instruments in the entity or any of its related parties.

D)none of the given answers.

A)the regularly paid salary of the directors.

B)the regularly paid salary, any bonuses paid and retirement benefits.

C)bonuses, commissions or salaries, retirement benefits and any brokerage or commission made on the subscription or agreement to subscribe to equity instruments in the entity or any of its related parties.

D)none of the given answers.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

IAS 24 provides guidance regarding the measurement of remuneration amounts for directors such that:

A)Remuneration should be measured at cost to the entity or related party and includes any money, consideration or employee benefits paid, payable or provided.

B)Where directly identifiable, the remuneration should be measured at cost; however, where the measurement of considerations or benefit requires an estimation, the amount should be reflected at fair value according to an arm's length transaction for a similar consideration or benefit.

C)Remuneration amounts should be disclosed at the fair value of the elements of the emoluments package offered, including any benefits or consideration that take the form of access to resources of the entity or its related parties.

D)Remuneration amounts should be disclosed at the net realisable value of the elements of the emoluments package offered.In the case of benefits or considerations that take the form of access to resources of the entity or its related parties, these should be disclosed at the deprival value to the relevant entity.

A)Remuneration should be measured at cost to the entity or related party and includes any money, consideration or employee benefits paid, payable or provided.

B)Where directly identifiable, the remuneration should be measured at cost; however, where the measurement of considerations or benefit requires an estimation, the amount should be reflected at fair value according to an arm's length transaction for a similar consideration or benefit.

C)Remuneration amounts should be disclosed at the fair value of the elements of the emoluments package offered, including any benefits or consideration that take the form of access to resources of the entity or its related parties.

D)Remuneration amounts should be disclosed at the net realisable value of the elements of the emoluments package offered.In the case of benefits or considerations that take the form of access to resources of the entity or its related parties, these should be disclosed at the deprival value to the relevant entity.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

IAS 24 requires disclosure of:

A)all material related-party transactions only.

B)all material transactions with directors and its close family members.

C)all material related-party transactions except those derived by virtue of normal dealings with a customer.

D)all material related-party transactions only and all material transactions with directors and its close family members.

A)all material related-party transactions only.

B)all material transactions with directors and its close family members.

C)all material related-party transactions except those derived by virtue of normal dealings with a customer.

D)all material related-party transactions only and all material transactions with directors and its close family members.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following statements is correct?

A)A related-party transaction is a transfer of resources, services or obligations between related parties that is not at arm's length.

B)The existence of a related-party transaction can expose an entity to risks or opportunities that otherwise would not have existed in the absence of the relationship.

C)Related parties include organisations that are under the control or significant influence of the entity and individuals such as key management personnel and their close family members.

D)The existence of a related-party transaction can expose an entity to risks or opportunities that otherwise would not have existed in the absence of the relationship, and related parties include organisations that are under the control or significant influence of the entity and individuals such as key management personnel and their close family members.

A)A related-party transaction is a transfer of resources, services or obligations between related parties that is not at arm's length.

B)The existence of a related-party transaction can expose an entity to risks or opportunities that otherwise would not have existed in the absence of the relationship.

C)Related parties include organisations that are under the control or significant influence of the entity and individuals such as key management personnel and their close family members.

D)The existence of a related-party transaction can expose an entity to risks or opportunities that otherwise would not have existed in the absence of the relationship, and related parties include organisations that are under the control or significant influence of the entity and individuals such as key management personnel and their close family members.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

The most common form of relationship based on significant influence is that between:

A)subsidiary and parent entity.

B)associate and parent entity.

C)investor and its associate.

D)subsidiary and another subsidiary.

A)subsidiary and parent entity.

B)associate and parent entity.

C)investor and its associate.

D)subsidiary and another subsidiary.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

What additional disclosures are required of disclosing entities with regards to related-party transactions?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is typically a related-party transaction within the provisions of IAS 24 Related Party Disclosures?

A)transactions between two entities with a common non-executive director

B)transactions between two entities that share control over another joint venture

C)transactions between an entity and its biggest finance provider

D)transactions between entities under common control of another entity

A)transactions between two entities with a common non-executive director

B)transactions between two entities that share control over another joint venture

C)transactions between an entity and its biggest finance provider

D)transactions between entities under common control of another entity

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Entities included in a wholly owned group as defined by IAS 24 include:

A)entities that have an equity ownership of 20 per cent or greater in an entity that is a subsidiary of an entity that is wholly owned by a party related to the reporting entity.

B)entities that are an associate or joint venture of the other entity.

C)entities that are controlled or have significant influence exercised over them by an entity that is wholly owned by a related party of the reporting entity.

D)subsidiary companies that are wholly owned by a parent company.

A)entities that have an equity ownership of 20 per cent or greater in an entity that is a subsidiary of an entity that is wholly owned by a party related to the reporting entity.

B)entities that are an associate or joint venture of the other entity.

C)entities that are controlled or have significant influence exercised over them by an entity that is wholly owned by a related party of the reporting entity.

D)subsidiary companies that are wholly owned by a parent company.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

IAS 24 requires an entity to disclose total compensation of key management personnel.What items are included in key management personnel's remuneration/compensation?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

Transactions with and amounts receivable from or payable to a key management person and their related parties are excluded from additional disclosures when:

A)the transactions occur within a normal employee, customer or supplier relationship on terms and conditions no more favourable than those that it is reasonable to expect the entity would have adopted if dealing with an unrelated person.

B)the information about them does not have a potential to affect adversely decisions about the allocation of scarce resources made by the users of the financial report, or the discharge of accountability by the key management person.

C)these are trivial or domestic in nature.

D)All of the given answers are correct.

A)the transactions occur within a normal employee, customer or supplier relationship on terms and conditions no more favourable than those that it is reasonable to expect the entity would have adopted if dealing with an unrelated person.

B)the information about them does not have a potential to affect adversely decisions about the allocation of scarce resources made by the users of the financial report, or the discharge of accountability by the key management person.

C)these are trivial or domestic in nature.

D)All of the given answers are correct.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following is usually not a related party as referred to in IAS 24 Related Party Disclosures?

A)subsidiary

B)associate

C)son-in law of the chief executive officer

D)trade union official

A)subsidiary

B)associate

C)son-in law of the chief executive officer

D)trade union official

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

In accordance with IAS 24,the categories of compensation to key management personnel required to be disclosed include:

A)short-term employee benefits.

B)post-employment benefits.

C)termination benefits

D)all of the given answers.

A)short-term employee benefits.

B)post-employment benefits.

C)termination benefits

D)all of the given answers.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following is not a related party within the provisions of IAS 24 Related Party Disclosures?

A)associates

B)non-executive directors

C)executive personnel

D)bankers

A)associates

B)non-executive directors

C)executive personnel

D)bankers

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

Cobourg Plc has following transactions during the year: Which of the following lists all the related-party transactions required to be disclosed in IAS 24 Related Party Disclosures?

A)I and II

B)III and IV

C)II, IV and V

D)I, II, IV and VI

A)I and II

B)III and IV

C)II, IV and V

D)I, II, IV and VI

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

Discuss the current debate regarding the setting and disclosure of executive compensation.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

Discuss the objective of IAS 24 Related Party Disclosures.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

Discuss the performance conditions utilised in the compensation plans for key management personnel.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.