Deck 7: Futures and Options on Foreign Exchange

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which equation is used to define the futures price?

A) =

=

B) =

=

C) =

=

D) =

=

A)

= B)

= C)

= D)

= Question

Question

Question

Question

Question

Question

Question

Question

Question

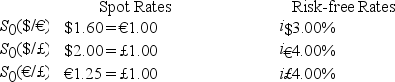

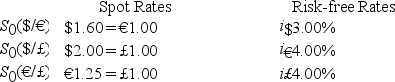

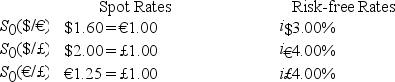

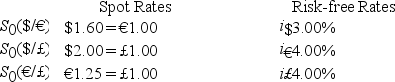

Suppose you observe the following one-year interest rates,spot exchange rates and futures prices.Futures contracts are available on €10,000.How much risk-free arbitrage profit could you make on one contract at maturity from this mispricing?

A)$159.22

B)$153.10

C)$439.42

D)none of the options

A)$159.22

B)$153.10

C)$439.42

D)none of the options

Question

Question

Question

Question

Question

Question

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500.For this option to be considered at-the-money,the strike price must be

A)$1.60 = €1.00.

B)$1.55 = €1.00.

C)$1.55 × = €1.00 ×

= €1.00 ×  .

.

D)none of the options

A)$1.60 = €1.00.

B)$1.55 = €1.00.

C)$1.55 ×

= €1.00 × .D)none of the options

Question

Question

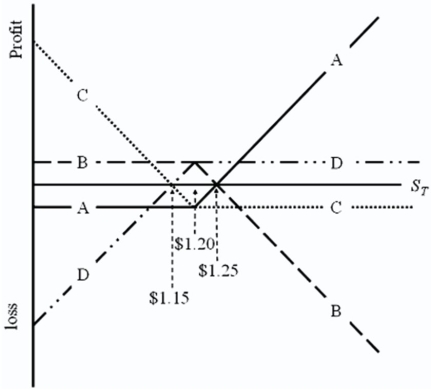

Which of the lines is a graph of the profit at maturity of writing a call option on €62,500 with a strike price of $1.20 = €1.00 and an option premium of $3,125?

A)A

B)B

C)C

D)D

A)A

B)B

C)C

D)D

Question

Question

Consider this graph of a call option.The option is a three-month American call option on €62,500 with a strike price of $1.50 = €1.00 and an option premium of $3,125.What are the values of A,B,and C,respectively?

A)A = $3,125 (or $.05 depending on your scale); B = $1.50; C = $1.55

B)A = €3,750 (or €.06 depending on your scale); B = $1.50; C = $1.55

C)A = $.05; B = $1.55; C = $1.60

D)none of the options

A)A = $3,125 (or $.05 depending on your scale); B = $1.50; C = $1.55

B)A = €3,750 (or €.06 depending on your scale); B = $1.50; C = $1.55

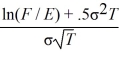

C)A = $.05; B = $1.55; C = $1.60

D)none of the options

Question

Question

Question

Question

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500 with a strike price of $1.50 = €1.00.Immediate exercise of this option will generate a profit of

A)$6,125.

B)$6,125/(1 + )3/12.

)3/12.

C)negative profit,so exercise would not occur.

D)$3,125.

A)$6,125.

B)$6,125/(1 +

)3/12.C)negative profit,so exercise would not occur.

D)$3,125.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

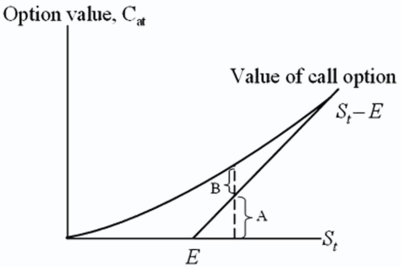

For an American call option,A and B in the graph are

A)time value and intrinsic value.

B)intrinsic value and time value.

C)in-the-money and out-of-the money.

D)none of the options

A)time value and intrinsic value.

B)intrinsic value and time value.

C)in-the-money and out-of-the money.

D)none of the options

Question

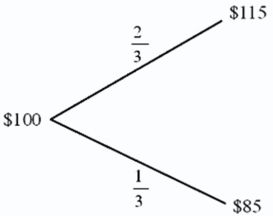

Find the value of a call option written on €100 with a strike price of $1.00 = €1.00.In one period,there are two possibilities: the exchange rate will move up by 15 percent or down by 15 percent .The U.S.risk-free rate is 5 percent over the period.The risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability of the dollar strengthening is 1/3.

A)$9.5238

B)$0.0952

C)$0

D)$3.1746

A)$9.5238

B)$0.0952

C)$0

D)$3.1746

Question

Question

The hedge ratio

A)Is the size of the long (short)position the investor must have in the underlying asset per option the investor must write (buy)to have a risk-free offsetting investment that will result in the investor perfectly hedging the option.

B)

C)Is related to the number of options that an investor can write without unlimited loss while holding a certain amount of the underlying asset.

D)all of the options

A)Is the size of the long (short)position the investor must have in the underlying asset per option the investor must write (buy)to have a risk-free offsetting investment that will result in the investor perfectly hedging the option.

B)

C)Is related to the number of options that an investor can write without unlimited loss while holding a certain amount of the underlying asset.

D)all of the options

Question

Question

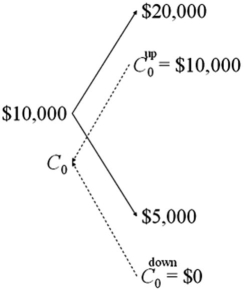

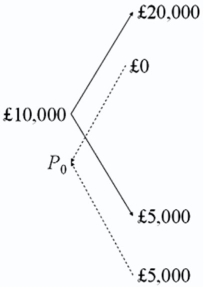

Draw the tree for a call option on $20,000 with a strike price of £10,000.The current exchange rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in half.The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C)both of the options

D)none of the options

A)

B)

C)both of the options

D)none of the options

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Assume that the dollar-euro spot rate is $1.28 and the six-month forward rate is  = $1.28

= $1.28  = $1.2864.The six-month U.S.dollar rate is 5 percent and the Eurodollar rate is 4 percent.The minimum price that a six-month American call option with a striking price of $1.25 should sell for in a rational market is

= $1.2864.The six-month U.S.dollar rate is 5 percent and the Eurodollar rate is 4 percent.The minimum price that a six-month American call option with a striking price of $1.25 should sell for in a rational market is

A)0 cents.

B)3.47 cents.

C)3.55 cents.

D)3 cents.

= $1.28 = $1.2864.The six-month U.S.dollar rate is 5 percent and the Eurodollar rate is 4 percent.The minimum price that a six-month American call option with a striking price of $1.25 should sell for in a rational market isA)0 cents.

B)3.47 cents.

C)3.55 cents.

D)3 cents.

Question

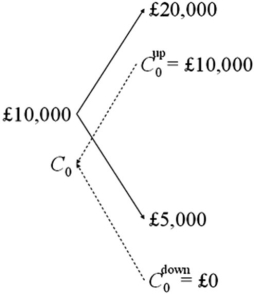

Draw the tree for a put option on $20,000 with a strike price of £10,000.The current exchange rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in half.The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C)both of the options

D)none of the options

A)

B)

C)both of the options

D)none of the options

Question

Question

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the hedge ratio.

Calculate the hedge ratio.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the hedge ratio. Question

Question

Question

Question

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

USING RISK NEUTRAL VALUATION (i.e.,the binomial option pricing model)find the value of the call (in euro).

USING RISK NEUTRAL VALUATION (i.e.,the binomial option pricing model)find the value of the call (in euro).

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

USING RISK NEUTRAL VALUATION (i.e.,the binomial option pricing model)find the value of the call (in euro). Question

Question

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

State the composition of the replicating portfolio; your answer should contain "trading orders" of what to buy and what to sell at time zero.

State the composition of the replicating portfolio; your answer should contain "trading orders" of what to buy and what to sell at time zero.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

State the composition of the replicating portfolio; your answer should contain "trading orders" of what to buy and what to sell at time zero. Question

Question

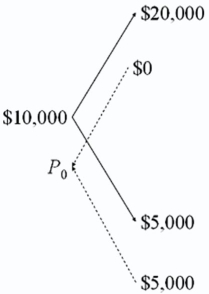

Find the dollar value today of a 1-period at-the-money call option on €10,000.The spot exchange rate is €1.00 = $1.25.In the next period,the euro can increase in dollar value to $2.00 or fall to $1.00.The interest rate in dollars is i$ = 27.50%; the interest rate in euro is  .

.

A)$3,308.82

B)$0

C)$3,294.12

D)$4,218.75

.A)$3,308.82

B)$0

C)$3,294.12

D)$4,218.75

Question

Question

Question

Question

Question

Question

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the current €/£ spot exchange rate.

Calculate the current €/£ spot exchange rate.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the current €/£ spot exchange rate. Question

Question

Question

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Find the risk neutral probability of an "up" move.

Find the risk neutral probability of an "up" move.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Find the risk neutral probability of an "up" move. Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/94

Play

Full screen (f)

Deck 7: Futures and Options on Foreign Exchange

1

Yesterday,you entered into a futures contract to buy €62,500 at $1.50 per €.Suppose the futures price closes today at $1.46.How much have you made/lost?

A)Depends on your margin balance.

B)You have made $2,500.00.

C)You have lost $2,500.00.

D)You have neither made nor lost money,yet.

A)Depends on your margin balance.

B)You have made $2,500.00.

C)You have lost $2,500.00.

D)You have neither made nor lost money,yet.

C

2

Yesterday,you entered into a futures contract to sell €75,000 at $1.79 per €.Your initial performance bond is $1,500 and your maintenance level is $500.At what settle price will you get a demand for additional funds to be posted?

A)$1.7767 per €.

B)$1.2084 per €.

C)$1.6676 per €.

D)$1.1840 per €.

A)$1.7767 per €.

B)$1.2084 per €.

C)$1.6676 per €.

D)$1.1840 per €.

A

3

What paradigm is used to define the futures price?

A)IRP

B)Hedge Ratio

C)Black Scholes

D)Risk Neutral Valuation

A)IRP

B)Hedge Ratio

C)Black Scholes

D)Risk Neutral Valuation

A

4

In reference to the futures market,a "speculator"

A)attempts to profit from a change in the futures price.

B)wants to avoid price variation by locking in a purchase price of the underlying asset through a long position in the futures contract or a sales price through a short position in the futures contract.

C)stands ready to buy or sell contracts in unlimited quantity.

D)wants to avoid price variation by locking in a purchase price of the underlying asset through a long position in the futures contract or a sales price through a short position in the futures contract,and also stands ready to buy or sell contracts in unlimited quantity.

A)attempts to profit from a change in the futures price.

B)wants to avoid price variation by locking in a purchase price of the underlying asset through a long position in the futures contract or a sales price through a short position in the futures contract.

C)stands ready to buy or sell contracts in unlimited quantity.

D)wants to avoid price variation by locking in a purchase price of the underlying asset through a long position in the futures contract or a sales price through a short position in the futures contract,and also stands ready to buy or sell contracts in unlimited quantity.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

5

Comparing "forward" and "futures" exchange contracts,we can say that

A)they are both "marked-to-market" daily.

B)their major difference is in the way the underlying asset is priced for future purchase or sale: futures settle daily and forwards settle at maturity.

C)a futures contract is negotiated by open outcry between floor brokers or traders and is traded on organized exchanges,while forward contract is tailor-made by an international bank for its clients and is traded OTC.

D)their major difference is in the way the underlying asset is priced for future purchase or sale: futures settle daily and forwards settle at maturity,and a futures contract is negotiated by open outcry between floor brokers or traders and is traded on organized exchanges,while a forward contract is tailor-made by an international bank for its clients and is traded OTC.

A)they are both "marked-to-market" daily.

B)their major difference is in the way the underlying asset is priced for future purchase or sale: futures settle daily and forwards settle at maturity.

C)a futures contract is negotiated by open outcry between floor brokers or traders and is traded on organized exchanges,while forward contract is tailor-made by an international bank for its clients and is traded OTC.

D)their major difference is in the way the underlying asset is priced for future purchase or sale: futures settle daily and forwards settle at maturity,and a futures contract is negotiated by open outcry between floor brokers or traders and is traded on organized exchanges,while a forward contract is tailor-made by an international bank for its clients and is traded OTC.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

6

Yesterday,you entered into a futures contract to buy €62,500 at $1.50 per €.Your initial performance bond is $1,500 and your maintenance level is $500.At what settle price will you get a demand for additional funds to be posted?

A)$1.5160 per €.

B)$1.208 per €.

C)$1.1920 per €.

D)$1.4840 per €.

A)$1.5160 per €.

B)$1.208 per €.

C)$1.1920 per €.

D)$1.4840 per €.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

7

Which equation is used to define the futures price?

A) =

B) =

C) =

D)F($ / €)- S($ / €)= -

A) =

B) =

C) =

D)F($ / €)- S($ / €)= -

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

8

If a currency futures contract (direct quote)is priced below the price implied by Interest Rate Parity (IRP),arbitrageurs could take advantage of the mispricing by simultaneously

A)going short in the futures contract,borrowing in the domestic currency,and going long in the foreign currency in the spot market.

B)going short in the futures contract,lending in the domestic currency,and going long in the foreign currency in the spot market.

C)going long in the futures contract,borrowing in the domestic currency,and going short in the foreign currency in the spot market.

D)going long in the futures contract,borrowing in the foreign currency,and going long in the domestic currency,investing the proceeds at the local rate of interest.

A)going short in the futures contract,borrowing in the domestic currency,and going long in the foreign currency in the spot market.

B)going short in the futures contract,lending in the domestic currency,and going long in the foreign currency in the spot market.

C)going long in the futures contract,borrowing in the domestic currency,and going short in the foreign currency in the spot market.

D)going long in the futures contract,borrowing in the foreign currency,and going long in the domestic currency,investing the proceeds at the local rate of interest.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

9

Which equation is used to define the futures price?

A) =

B) =

C) =

D) =

A)

= B)

= C)

= D)

= Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

10

A put option on $15,000 with a strike price of €10,000 is the same thing as a call option on €10,000 with a strike price of $15,000.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

11

In which market does a clearinghouse serve as a third party to all transactions?

A)Futures

B)Forwards

C)Swaps

D)none of the options

A)Futures

B)Forwards

C)Swaps

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

12

A CME contract on €125,000 with September delivery

A)is an example of a forward contract.

B)is an example of a futures contract.

C)is an example of a put option.

D)is an example of a call option.

A)is an example of a forward contract.

B)is an example of a futures contract.

C)is an example of a put option.

D)is an example of a call option.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

13

Suppose the futures price is below the price predicted by IRP.What steps would assure an arbitrage profit?

A)Go short in the spot market,go long in the futures contract.

B)Go long in the spot market,go short in the futures contract.

C)Go short in the spot market,go short in the futures contract.

D)Go long in the spot market,go long in the futures contract.

A)Go short in the spot market,go long in the futures contract.

B)Go long in the spot market,go short in the futures contract.

C)Go short in the spot market,go short in the futures contract.

D)Go long in the spot market,go long in the futures contract.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

14

In the event of a default on one side of a futures trade,

A)the clearing member stands in for the defaulting party.

B)the clearing member will seek restitution for the defaulting party.

C)if the default is on the short side,a randomly selected long contract will not get paid.That party will then have standing to initiate a civil suit against the defaulting short.

D)the clearing member stands in for the defaulting party and will seek restitution for the defaulting party.

A)the clearing member stands in for the defaulting party.

B)the clearing member will seek restitution for the defaulting party.

C)if the default is on the short side,a randomly selected long contract will not get paid.That party will then have standing to initiate a civil suit against the defaulting short.

D)the clearing member stands in for the defaulting party and will seek restitution for the defaulting party.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

15

Three days ago,you entered into a futures contract to sell €62,500 at $1.50 per €.Over the past three days the contract has settled at $1.50,$1.52,and $1.54.How much have you made or lost?

A)Lost $0.04 per € or $2,500

B)Made $0.04 per € or $2,500

C)Lost $0.06 per € or $3,750

D)none of the options

A)Lost $0.04 per € or $2,500

B)Made $0.04 per € or $2,500

C)Lost $0.06 per € or $3,750

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

16

Today's settlement price on a Chicago Mercantile Exchange (CME)yen futures contract is $0.8011/¥100.Your margin account currently has a balance of $2,000.The next three days' settlement prices are $0.8057/¥100,$0.7996/¥100,and $0.7985/¥100.(The contractual size of one CME yen contract is ¥12,500,000).If you have a short position in one futures contract,the changes in the margin account from daily marking-to-market will result in the balance of the margin account after the third day to be

A)$1,425.

B)$2,000.

C)$2,325.

D)$3,425.

A)$1,425.

B)$2,000.

C)$2,325.

D)$3,425.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

17

Comparing "forward" and "futures" exchange contracts,we can say that

A)delivery of the underlying asset is seldom made in futures contracts.

B)delivery of the underlying asset is usually made in forward contracts.

C)delivery of the underlying asset is seldom made in either contract-they are typically cash settled at maturity.

D)delivery of the underlying asset is seldom made in futures contracts and delivery of the underlying asset is usually made in forward contracts.

A)delivery of the underlying asset is seldom made in futures contracts.

B)delivery of the underlying asset is usually made in forward contracts.

C)delivery of the underlying asset is seldom made in either contract-they are typically cash settled at maturity.

D)delivery of the underlying asset is seldom made in futures contracts and delivery of the underlying asset is usually made in forward contracts.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

18

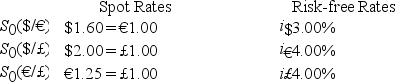

Suppose you observe the following one-year interest rates,spot exchange rates and futures prices.Futures contracts are available on €10,000.How much risk-free arbitrage profit could you make on one contract at maturity from this mispricing?

A)$159.22

B)$153.10

C)$439.42

D)none of the options

A)$159.22

B)$153.10

C)$439.42

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

19

Yesterday,you entered into a futures contract to buy €62,500 at $1.50/€.Your initial margin was $3,750 (= 0.04 × €62,500 × $1.50/€ = 4 percent of the contract value in dollars).Your maintenance margin is $2,000 (meaning that your broker leaves you alone until your account balance falls to $2,000).At what settle price (use 4 decimal places)do you get a margin call?

A)$1.4720/€

B)$1.5280/€

C)$1.500/€

D)none of the options

A)$1.4720/€

B)$1.5280/€

C)$1.500/€

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

20

Today's settlement price on a Chicago Mercantile Exchange (CME)yen futures contract is $0.8011/¥100.Your margin account currently has a balance of $2,000.The next three days' settlement prices are $0.8057/¥100,$0.7996/¥100,and $0.7985/¥100.(The contractual size of one CME yen contract is ¥12,500,000).If you have a long position in one futures contract,the changes in the margin account from daily marking-to-market,will result in the balance of the margin account after the third day to be

A)$1,425.

B)$1,675.

C)$2,000.

D)$3,425

A)$1,425.

B)$1,675.

C)$2,000.

D)$3,425

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the follow options strategies are consistent in their belief about the future behavior of the underlying asset price?

A)Selling calls and selling puts

B)Buying calls and buying puts

C)Buying calls and selling puts

D)none of the options

A)Selling calls and selling puts

B)Buying calls and buying puts

C)Buying calls and selling puts

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

22

Exercise of a currency futures option results in

A)a long futures position for the call buyer or put writer.

B)a short futures position for the call buyer or put writer.

C)a long futures position for the put buyer or call writer.

D)a short futures position for the call buyer or put buyer.

A)a long futures position for the call buyer or put writer.

B)a short futures position for the call buyer or put writer.

C)a long futures position for the put buyer or call writer.

D)a short futures position for the call buyer or put buyer.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

23

A European option is different from an American option in that

A)one is traded in Europe and one in traded in the United States.

B)European options can only be exercised at maturity; American options can be exercised prior to maturity.

C)European options tend to be worth more than American options,ceteris paribus.

D)American options have a fixed exercise price; European options' exercise price is set at the average price of the underlying asset during the life of the option.

A)one is traded in Europe and one in traded in the United States.

B)European options can only be exercised at maturity; American options can be exercised prior to maturity.

C)European options tend to be worth more than American options,ceteris paribus.

D)American options have a fixed exercise price; European options' exercise price is set at the average price of the underlying asset during the life of the option.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

24

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500.For this option to be considered at-the-money,the strike price must be

A)$1.60 = €1.00.

B)$1.55 = €1.00.

C)$1.55 × = €1.00 × .

D)none of the options

A)$1.60 = €1.00.

B)$1.55 = €1.00.

C)$1.55 ×

= €1.00 × .D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

25

If you think that the dollar is going to appreciate against the euro,you should

A)buy put options on the euro.

B)sell call options on the euro.

C)buy call options on the euro.

D)none of the options

A)buy put options on the euro.

B)sell call options on the euro.

C)buy call options on the euro.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the lines is a graph of the profit at maturity of writing a call option on €62,500 with a strike price of $1.20 = €1.00 and an option premium of $3,125?

A)A

B)B

C)C

D)D

A)A

B)B

C)C

D)D

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

27

With currency futures options the underlying asset is

A)foreign currency.

B)a call or put option written on foreign currency.

C)a futures contract on the foreign currency.

D)none of the options

A)foreign currency.

B)a call or put option written on foreign currency.

C)a futures contract on the foreign currency.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

28

Consider this graph of a call option.The option is a three-month American call option on €62,500 with a strike price of $1.50 = €1.00 and an option premium of $3,125.What are the values of A,B,and C,respectively?

A)A = $3,125 (or $.05 depending on your scale); B = $1.50; C = $1.55

B)A = €3,750 (or €.06 depending on your scale); B = $1.50; C = $1.55

C)A = $.05; B = $1.55; C = $1.60

D)none of the options

A)A = $3,125 (or $.05 depending on your scale); B = $1.50; C = $1.55

B)A = €3,750 (or €.06 depending on your scale); B = $1.50; C = $1.55

C)A = $.05; B = $1.55; C = $1.60

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

29

Most exchange traded currency options

A)mature every month,with daily resettlement.

B)have original maturities of 1,2,and 3 years.

C)have original maturities of 3,6,9,and 12 months.

D)mature every month,without daily resettlement.

A)mature every month,with daily resettlement.

B)have original maturities of 1,2,and 3 years.

C)have original maturities of 3,6,9,and 12 months.

D)mature every month,without daily resettlement.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

30

In the CURRENCY TRADING section of The Wall Street Journal,the following appeared under the heading OPTIONS:

Which combination of the following statements are true?

(i)The time values of the 68 May and 69 May put options are respectively .30 cents and .50 cents.

(ii)The 68 May put option has a lower time value (price)than the 69 May put option.

(iii)If everything else is kept constant,the spot price and the put premium are inversely related.

(iv)The time values of the 68 May and 69 May put options are,respectively,1.63 cents and 0.83 cents.

(v)If everything else is kept constant,the strike price and the put premium are inversely related.

A)(i),(ii),and (iii)

B)(ii),(iii),and (iv)

C)(iii)and (iv)

D)(iv)and (v)

| Philadelphia Exchange | Puts | ||

| Swiss France | 69.33 | ||

| 62,500 Swiss Francs-cents per unit | Vol. | Last | |

| 68 May | 12 | 0.30 | |

| 69 May | 50 | 0.50 |

(i)The time values of the 68 May and 69 May put options are respectively .30 cents and .50 cents.

(ii)The 68 May put option has a lower time value (price)than the 69 May put option.

(iii)If everything else is kept constant,the spot price and the put premium are inversely related.

(iv)The time values of the 68 May and 69 May put options are,respectively,1.63 cents and 0.83 cents.

(v)If everything else is kept constant,the strike price and the put premium are inversely related.

A)(i),(ii),and (iii)

B)(ii),(iii),and (iv)

C)(iii)and (iv)

D)(iv)and (v)

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

31

From the perspective of the writer of a put option written on €62,500.If the strike price is $1.55/€,and the option premium is $1,875,at what exchange rate do you start to lose money?

A)$1.52/€

B)$1.55/€

C)$1.58/€

D)none of the options

A)$1.52/€

B)$1.55/€

C)$1.58/€

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

32

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500 with a strike price of $1.50 = €1.00.Immediate exercise of this option will generate a profit of

A)$6,125.

B)$6,125/(1 + )3/12.

C)negative profit,so exercise would not occur.

D)$3,125.

A)$6,125.

B)$6,125/(1 +

)3/12.C)negative profit,so exercise would not occur.

D)$3,125.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

33

An investor believes that the price of a stock,say IBM's shares,will increase in the next 60 days.If the investor is correct,which combination of the following investment strategies will show a profit in all the choices? (i)buy the stock and hold it for 60 days

(ii)buy a put option

(iii)sell (write)a call option

(iv)buy a call option

(v)sell (write)a put option

A)(i),(ii),and (iii)

B)(i),(ii),and (iv)

C)(i),(iv),and (v)

D)(ii)and (iii)

(ii)buy a put option

(iii)sell (write)a call option

(iv)buy a call option

(v)sell (write)a put option

A)(i),(ii),and (iii)

B)(i),(ii),and (iv)

C)(i),(iv),and (v)

D)(ii)and (iii)

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

34

The volume of OTC currency options trading is

A)much smaller than that of organized-exchange currency option trading.

B)much larger than that of organized-exchange currency option trading.

C)larger,because the exchanges are only repackaging OTC options for their customers.

D)none of the options

A)much smaller than that of organized-exchange currency option trading.

B)much larger than that of organized-exchange currency option trading.

C)larger,because the exchanges are only repackaging OTC options for their customers.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

35

Open interest in currency futures contracts

A)tends to be greatest for the near-term contracts.

B)tends to be greatest for the longer-term contracts.

C)typically decreases with the term to maturity of most futures contracts.

D)tends to be greatest for the near-term contracts,and typically decreases with the term to maturity of most futures contracts.

A)tends to be greatest for the near-term contracts.

B)tends to be greatest for the longer-term contracts.

C)typically decreases with the term to maturity of most futures contracts.

D)tends to be greatest for the near-term contracts,and typically decreases with the term to maturity of most futures contracts.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

36

The "open interest" shown in currency futures quotations is

A)the total number of people indicating interest in buying the contracts in the near future.

B)the total number of people indicating interest in selling the contracts in the near future.

C)the total number of people indicating interest in buying or selling the contracts in the near future.

D)the total number of long or short contracts outstanding for the particular delivery month.

A)the total number of people indicating interest in buying the contracts in the near future.

B)the total number of people indicating interest in selling the contracts in the near future.

C)the total number of people indicating interest in buying or selling the contracts in the near future.

D)the total number of long or short contracts outstanding for the particular delivery month.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

37

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500 with a strike price of $1.50 = €1.00.If you pay an option premium of $5,000 to buy this call,at what exchange rate will you break-even?

A)$1.58 = €1.00

B)$1.62 = €1.00

C)$1.50 = €1.00

D)$1.68 = €1.00

A)$1.58 = €1.00

B)$1.62 = €1.00

C)$1.50 = €1.00

D)$1.68 = €1.00

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

38

A currency futures option amounts to a derivative on a derivative.Why would something like that exist?

A)For some assets,the futures contract can have lower transaction costs and greater liquidity than the underlying asset.

B)Tax consequences matter as well,and for some users an option contract on a future is more tax efficient.

C)Transaction costs and liquidity

D)all of the options

A)For some assets,the futures contract can have lower transaction costs and greater liquidity than the underlying asset.

B)Tax consequences matter as well,and for some users an option contract on a future is more tax efficient.

C)Transaction costs and liquidity

D)all of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

39

An "option" is

A)a contract giving the seller (writer)of the option the right,but not the obligation,to buy (call)or sell (put)a given quantity of an asset at a specified price at some time in the future.

B)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (call)or sell (put)a given quantity of an asset at a specified price at some time in the future.

C)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (put)or sell (call)a given quantity of an asset at a specified price at some time in the future.

D)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (put)or sell (sell)a given quantity of an asset at a specified price at some time in the future.

A)a contract giving the seller (writer)of the option the right,but not the obligation,to buy (call)or sell (put)a given quantity of an asset at a specified price at some time in the future.

B)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (call)or sell (put)a given quantity of an asset at a specified price at some time in the future.

C)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (put)or sell (call)a given quantity of an asset at a specified price at some time in the future.

D)a contract giving the owner (buyer)of the option the right,but not the obligation,to buy (put)or sell (sell)a given quantity of an asset at a specified price at some time in the future.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

40

The current spot exchange rate is $1.55 = €1.00; the three-month U.S.dollar interest rate is 2 percent.Consider a three-month American call option on €62,500 with a strike price of $1.50 = €1.00.What is the least that this option should sell for?

A)$0.05 × 62,500 = $3,125

B)$3,125/1.02 = $3,063.73

C)$0.00

D)none of the options

A)$0.05 × 62,500 = $3,125

B)$3,125/1.02 = $3,063.73

C)$0.00

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following is correct?

A)European options can be exercised early.

B)American options can be exercised early.

C)Asian options can be exercised early.

D)all of the options

A)European options can be exercised early.

B)American options can be exercised early.

C)Asian options can be exercised early.

D)all of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

42

For an American call option,A and B in the graph are

A)time value and intrinsic value.

B)intrinsic value and time value.

C)in-the-money and out-of-the money.

D)none of the options

A)time value and intrinsic value.

B)intrinsic value and time value.

C)in-the-money and out-of-the money.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

43

Find the value of a call option written on €100 with a strike price of $1.00 = €1.00.In one period,there are two possibilities: the exchange rate will move up by 15 percent or down by 15 percent .The U.S.risk-free rate is 5 percent over the period.The risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability of the dollar strengthening is 1/3.

A)$9.5238

B)$0.0952

C)$0

D)$3.1746

A)$9.5238

B)$0.0952

C)$0

D)$3.1746

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

44

For European currency options written on euro with a strike price in dollars,what is the effect of an increase in the exchange rate S(€/$)?

A)Decreases the value of calls and puts ceteris paribus

B)Increases the value of calls and puts ceteris paribus

C)Decreases the value of calls,increases the value of puts ceteris paribus

D)Increases the value of calls,decreases the value of puts ceteris paribus

A)Decreases the value of calls and puts ceteris paribus

B)Increases the value of calls and puts ceteris paribus

C)Decreases the value of calls,increases the value of puts ceteris paribus

D)Increases the value of calls,decreases the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

45

The hedge ratio

A)Is the size of the long (short)position the investor must have in the underlying asset per option the investor must write (buy)to have a risk-free offsetting investment that will result in the investor perfectly hedging the option.

B)

C)Is related to the number of options that an investor can write without unlimited loss while holding a certain amount of the underlying asset.

D)all of the options

A)Is the size of the long (short)position the investor must have in the underlying asset per option the investor must write (buy)to have a risk-free offsetting investment that will result in the investor perfectly hedging the option.

B)

C)Is related to the number of options that an investor can write without unlimited loss while holding a certain amount of the underlying asset.

D)all of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

46

Find the hedge ratio for a call option on £10,000 with a strike price of €12,500.The current exchange rate is €1.50/£1.00 and in the next period the exchange rate can increase to €2.40/£ or decrease to €0.9375/€1.00 . The current interest rates are i€ = 3% and are i£ = 4%.

Choose the answer closest to yours.

A)5/9

B)8/13

C)2/3

D)3/8

E)none of the options

Choose the answer closest to yours.

A)5/9

B)8/13

C)2/3

D)3/8

E)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

47

Draw the tree for a call option on $20,000 with a strike price of £10,000.The current exchange rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in half.The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C)both of the options

D)none of the options

A)

B)

C)both of the options

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

48

For European options,what is the effect of an increase in the strike price E?

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

49

You have written a call option on £10,000 with a strike price of $20,000.The current exchange rate is $2.00/£1.00 and in the next period the exchange rate can increase to $4.00/£1.00 or decrease to $1.00/€1.00 .The current interest rates are i$ = 3% and are i£ = 2%.Find the hedge ratio and use it to create a position in the underlying asset that will hedge your option position.

A)Enter into a short position in a futures contract on £6,666.67

B)Lend the present value of £6,666.67 today at i£ = 2%

C)Enter into a long position in a futures contract on £6,666.67

D)Lending the present value of £6,666.67 today at i£ = 2% or entering into a long position in a futures contract on £6,666.67 would both work.

A)Enter into a short position in a futures contract on £6,666.67

B)Lend the present value of £6,666.67 today at i£ = 2%

C)Enter into a long position in a futures contract on £6,666.67

D)Lending the present value of £6,666.67 today at i£ = 2% or entering into a long position in a futures contract on £6,666.67 would both work.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

50

For European currency options written on euro with a strike price in dollars,what is the effect of an increase in r$?

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following is correct?

A)Time value = intrinsic value + option premium

B)Intrinsic value = option premium + time value

C)Option premium = intrinsic value - time value

D)Option premium = intrinsic value + time value

A)Time value = intrinsic value + option premium

B)Intrinsic value = option premium + time value

C)Option premium = intrinsic value - time value

D)Option premium = intrinsic value + time value

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

52

For European options,what is the effect of an increase in St?

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

53

Use the binomial option pricing model to find the value of a call option on £10,000 with a strike price of €12,500.The current exchange rate is €1.50/£1.00 and in the next period the exchange rate can increase to €2.40/£ or decrease to €0.9375/€1.00 .The current interest rates are i€ = 3% and are i£ = 4%.Choose the answer closest to yours.

A)€3,275

B)€2,500

C)€3,373

D)€3,243

A)€3,275

B)€2,500

C)€3,373

D)€3,243

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

54

American call and put premiums

A)should be at least as large as their intrinsic value.

B)should be no larger than their intrinsic value.

C)should be exactly equal to their time value.

D)should be no larger than their speculative value.

A)should be at least as large as their intrinsic value.

B)should be no larger than their intrinsic value.

C)should be exactly equal to their time value.

D)should be no larger than their speculative value.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

55

For European currency options written on euro with a strike price in dollars,what is the effect of an increase in the exchange rate S($/€)?

A)Decreases the value of calls and puts ceteris paribus

B)Increases the value of calls and puts ceteris paribus

C)Decreases the value of calls,increases the value of puts ceteris paribus

D)Increases the value of calls,decreases the value of puts ceteris paribus

A)Decreases the value of calls and puts ceteris paribus

B)Increases the value of calls and puts ceteris paribus

C)Decreases the value of calls,increases the value of puts ceteris paribus

D)Increases the value of calls,decreases the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

56

For European currency options written on euro with a strike price in dollars,what is the effect of an increase in r€?

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

57

For European currency options written on euro with a strike price in dollars,what is the effect of an increase in r$ relative to r€?

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

A)Decrease the value of calls and puts ceteris paribus

B)Increase the value of calls and puts ceteris paribus

C)Decrease the value of calls,increase the value of puts ceteris paribus

D)Increase the value of calls,decrease the value of puts ceteris paribus

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

58

Assume that the dollar-euro spot rate is $1.28 and the six-month forward rate is = $1.28 = $1.2864.The six-month U.S.dollar rate is 5 percent and the Eurodollar rate is 4 percent.The minimum price that a six-month American call option with a striking price of $1.25 should sell for in a rational market is

A)0 cents.

B)3.47 cents.

C)3.55 cents.

D)3 cents.

= $1.28 = $1.2864.The six-month U.S.dollar rate is 5 percent and the Eurodollar rate is 4 percent.The minimum price that a six-month American call option with a striking price of $1.25 should sell for in a rational market isA)0 cents.

B)3.47 cents.

C)3.55 cents.

D)3 cents.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

59

Draw the tree for a put option on $20,000 with a strike price of £10,000.The current exchange rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in half.The current interest rates are i$ = 3% and are i£ = 2%.

A)

B)

C)both of the options

D)none of the options

A)

B)

C)both of the options

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

60

A binomial call option premium is calculated as

A)C0 = [qCuT + (1 - q)CdT] / (1 + r$)

B)C0 = [qCdT + (1 - q)CuT] / (1 + r$)

C)C0 = [qCuT + (1 - q)CdT] / (1 - r$)

D)C0 = [qCdT + (1 - q)CuT] / (1 - r$)

A)C0 = [qCuT + (1 - q)CdT] / (1 + r$)

B)C0 = [qCdT + (1 - q)CuT] / (1 + r$)

C)C0 = [qCuT + (1 - q)CdT] / (1 - r$)

D)C0 = [qCdT + (1 - q)CuT] / (1 - r$)

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

61

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the hedge ratio.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the hedge ratio. Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

62

The Black-Scholes option pricing formula

A)is used widely in practice,especially by international banks in trading OTC options.

B)is not widely used outside of the academic world.

C)works well enough,but is not used in the real world because no one has the time to flog their calculator for five minutes on the trading floor.

D)none of the options

A)is used widely in practice,especially by international banks in trading OTC options.

B)is not widely used outside of the academic world.

C)works well enough,but is not used in the real world because no one has the time to flog their calculator for five minutes on the trading floor.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

63

Find the Black-Scholes price of a six-month call option written on €100,000 with a strike price of $1.00 = €1.00.The current exchange rate is $1.25 = €1.00; The U.S.risk-free rate is 5 percent over the period and the euro-zone risk-free rate is 4 percent.The volatility of the underlying asset is 10.7 percent.

A)Ce = $0.63577

B)Ce = $0.0998

C)Ce = $1.6331

D)none of the options

A)Ce = $0.63577

B)Ce = $0.0998

C)Ce = $1.6331

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

64

Find the input d1 of the Black-Scholes price of a six-month call option written on €100,000 with a strike price of $1.00 = €1.00.The current exchange rate is $1.25 = €1.00; The U.S.risk-free rate is 5% over the period and the euro-zone risk-free rate is 4%.The volatility of the underlying asset is 10.7 percent.

A)d1 = 0.103915

B)d1 = 2.9871

C)d1 = 0.0283

D)none of the options

A)d1 = 0.103915

B)d1 = 2.9871

C)d1 = 0.0283

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

65

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

USING RISK NEUTRAL VALUATION (i.e.,the binomial option pricing model)find the value of the call (in euro).

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

USING RISK NEUTRAL VALUATION (i.e.,the binomial option pricing model)find the value of the call (in euro). Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

66

With regard to trading costs,

A)forward contracts involve the bid-ask spread plus the broker's commission.

B)futures contracts involve the bid-ask spread plus the broker's commission.

C)futures contracts involve the bid-ask spread plus indirect bank charges via compensating balance requirements.

D)none of the options

A)forward contracts involve the bid-ask spread plus the broker's commission.

B)futures contracts involve the bid-ask spread plus the broker's commission.

C)futures contracts involve the bid-ask spread plus indirect bank charges via compensating balance requirements.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

67

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

State the composition of the replicating portfolio; your answer should contain "trading orders" of what to buy and what to sell at time zero.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

State the composition of the replicating portfolio; your answer should contain "trading orders" of what to buy and what to sell at time zero. Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

68

Empirical tests of the Black-Scholes option pricing formula

A)have faced difficulties due to nonsynchronous data.

B)suggest that when using simultaneous price data and incorporating transaction costs they conclude that the PHLX American currency options are efficiently priced.

C)suggest that the European option-pricing model works well for pricing American currency options that are at- or out-of-the money,but does not do well in pricing in-the-money calls and puts.

D)all of the options

A)have faced difficulties due to nonsynchronous data.

B)suggest that when using simultaneous price data and incorporating transaction costs they conclude that the PHLX American currency options are efficiently priced.

C)suggest that the European option-pricing model works well for pricing American currency options that are at- or out-of-the money,but does not do well in pricing in-the-money calls and puts.

D)all of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

69

Find the dollar value today of a 1-period at-the-money call option on €10,000.The spot exchange rate is €1.00 = $1.25.In the next period,the euro can increase in dollar value to $2.00 or fall to $1.00.The interest rate in dollars is i$ = 27.50%; the interest rate in euro is .

A)$3,308.82

B)$0

C)$3,294.12

D)$4,218.75

.A)$3,308.82

B)$0

C)$3,294.12

D)$4,218.75

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

70

Suppose that you have written a call option on €10,000 with a strike price in dollars.Suppose further that the hedge ratio is 1/2.Which of the following would be an appropriate hedge for a short position in this call option?

A)Buy €5,000 today at today's spot exchange rate.

B)Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity of the option that prevails today .

C)Buy the present value of €5,000 discounted at i€ for the maturity of the option.

D)Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity of the option that prevails today or buy the present value of €5,000 discounted at i€ for the maturity of the option.

A)Buy €5,000 today at today's spot exchange rate.

B)Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity of the option that prevails today .

C)Buy the present value of €5,000 discounted at i€ for the maturity of the option.

D)Agree to buy €5,000 at the maturity of the option at the forward exchange rate for the maturity of the option that prevails today or buy the present value of €5,000 discounted at i€ for the maturity of the option.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

71

Empirical tests of the Black-Scholes option pricing formula

A)shows that binomial option pricing is used widely in practice,especially by international banks in trading OTC options.

B)works well for pricing American currency options that are at-the-money or out-of-the-money.

C)does not do well in pricing in-the-money calls and puts.

D)works well for pricing American currency options that are at-the-money or out-of-the-money,but does not do well in pricing in-the-money calls and puts.

A)shows that binomial option pricing is used widely in practice,especially by international banks in trading OTC options.

B)works well for pricing American currency options that are at-the-money or out-of-the-money.

C)does not do well in pricing in-the-money calls and puts.

D)works well for pricing American currency options that are at-the-money or out-of-the-money,but does not do well in pricing in-the-money calls and puts.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is correct?

A)The value (in dollars)of a call option on £5,000 with a strike price of $10,000 is equal to the value (in dollars)of a put option on $10,000 with a strike price of £5,000 only when the spot exchange rate is $2 = £1.

B)The value (in dollars)of a call option on £5,000 with a strike price of $10,000 is equal to the value (in dollars)of a put option on $10,000 with a strike price of £5,000.

A)The value (in dollars)of a call option on £5,000 with a strike price of $10,000 is equal to the value (in dollars)of a put option on $10,000 with a strike price of £5,000 only when the spot exchange rate is $2 = £1.

B)The value (in dollars)of a call option on £5,000 with a strike price of $10,000 is equal to the value (in dollars)of a put option on $10,000 with a strike price of £5,000.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

73

With regard to contractual size,

A)forward contracts are characterized by a standardized amount of the underlying asset.

B)futures contracts are tailor-made to the needs of the participant.

C)futures contracts are characterized by a standardized amount of the underlying asset.

D)none of the options

A)forward contracts are characterized by a standardized amount of the underlying asset.

B)futures contracts are tailor-made to the needs of the participant.

C)futures contracts are characterized by a standardized amount of the underlying asset.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

74

The one-step binomial model assumes that at the end of the option period,the call will have appreciated to SuT = S0u or depreciated to SdT = S0d.How is u calculated?

A)1/d

B)e^(σt0.5)

C)both 1/d and e^(σt0.5)

D)none of these options

A)1/d

B)e^(σt0.5)

C)both 1/d and e^(σt0.5)

D)none of these options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

75

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the current €/£ spot exchange rate.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Calculate the current €/£ spot exchange rate. Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

76

Use the European option pricing formula to find the value of a six-month call option on Japanese yen.The strike price is $1 = ¥100.The volatility is 25 percent per annum; r$ = 5.5% and r¥ = 6%.

A)0.005395

B)0.005982

C)$0.006137/¥

D)none of the options

A)0.005395

B)0.005982

C)$0.006137/¥

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

77

With regard to trading location,

A)forward contracts are traded competitively on organized exchanges.

B)futures contracts are traded competitively on organized exchanges.

C)futures contracts are traded by bank dealers via a network of telephones and computerized dealing systems.

D)none of the options

A)forward contracts are traded competitively on organized exchanges.

B)futures contracts are traded competitively on organized exchanges.

C)futures contracts are traded by bank dealers via a network of telephones and computerized dealing systems.

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

78

Consider an option to buy £10,000 for €12,500.In the next period,if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent.On the other hand,the euro could depreciate against the pound by 20 percent.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Find the risk neutral probability of an "up" move.

Big hint: don't round,keep exchange rates out to at least 4 decimal places.

Find the risk neutral probability of an "up" move. Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

79

Find the input d1 of the Black-Scholes price of a six-month call option on Japanese yen.The strike price is $1 = ¥100.The volatility is 25 percent per annum; r$ = 5.5% and r¥ = 6%.

A)d1 = 0.074246

B)d1 = 0.005982

C)d1 = $0.006137/¥

D)none of the options

A)d1 = 0.074246

B)d1 = 0.005982

C)d1 = $0.006137/¥

D)none of the options

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

80

With regard to expiration date,

A)futures contracts do not have delivery dates.

B)forward contracts have standardized delivery dates.

C)futures contracts have tailor-made delivery dates that meet the needs of the investor.

D)futures contracts have standardized delivery dates.

A)futures contracts do not have delivery dates.

B)forward contracts have standardized delivery dates.

C)futures contracts have tailor-made delivery dates that meet the needs of the investor.

D)futures contracts have standardized delivery dates.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 94 flashcards in this deck.